Author: Munehisa

Translation: Baihua Blockchain

Abstract

Throughout history, currency has continuously evolved around three core functions: as a medium of exchange, a store of value, and a unit of account. Meanwhile, the pursuit of faster settlement, lower costs, and borderless usage has driven the transformation of currency from localized barter systems to today’s global digital networks.

Since the end of World War II, the US dollar has become the dominant global currency, more effectively meeting the key attributes of currency than any other.

Stablecoins represent the next stage of evolution for currency and payment systems, laying the foundation for a financial system with faster settlement speeds, lower fees, seamless cross-border functionality, native programmability, and robust audit trails. Today’s stablecoin ecosystem includes several different types of stablecoins, primarily distinguished by their collateral support, degree of decentralization, and mechanisms for maintaining price pegs.

Dollar-pegged stablecoins are in high demand due to their various use cases, including: store of value, cross-border remittances, payments, yield generation, cryptocurrency trading, and as tools for shadow monetary policy.

Stablecoins are becoming a powerful tool for shadow monetary policy, increasingly viewed by governments and fiscal authorities as strategic instruments for managing sovereign debt and promoting the influence of monetary and financial systems.

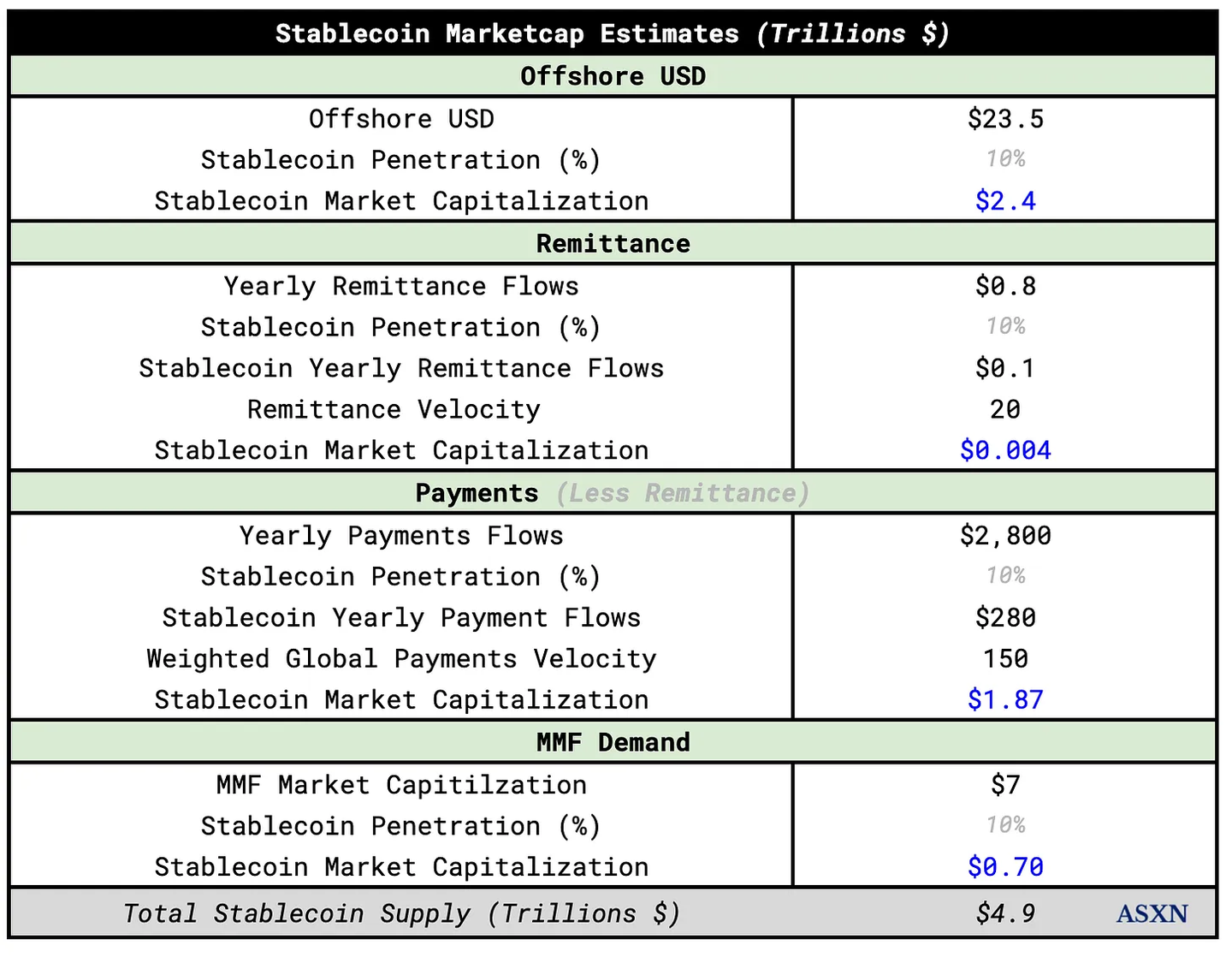

We expect that over the next decade, the total market capitalization of stablecoins will reach approximately $4.9 trillion, growing nearly 20 times from current levels.

Introduction

We provide a brief historical overview of currency, the US dollar, and central banks below. If you wish to directly understand stablecoin-related content, you can skip to the "Stablecoins" section.

Following the global financial crisis and subsequent government bailouts of over-leveraged financial institutions ("The Chancellor is about to bail out the banks again"), Bitcoin emerged as a non-sovereign alternative aimed at achieving "a purely peer-to-peer electronic cash system that allows online payments to be sent directly from one party to another without going through a financial institution." While Bitcoin has successfully served as a censorship-resistant asset for holders, independent of any central authority, it has yet to become a practical tool for everyday payments due to limitations such as low transaction throughput, slow settlement times, high fees, significant price volatility, and poor user experience. Although Bitcoin may ultimately prove to be a superior form of currency (capable of withstanding fiat currency devaluation and arbitrary decisions by central bankers), the vast majority of global trade is still conducted in US dollars. The digital representation of the dollar—stablecoins—is increasingly replacing the role of Bitcoin as the originally envisioned electronic cash system.

These "room-temperature superconductors of financial services" are transforming value transfer for individuals in high-inflation or authoritarian regimes through low-cost peer-to-peer remittance payments, while enhancing user experience and real-time functionality for multinational corporations. Additionally, we believe that the structural debt dynamics in the US, the demand for new marginal buyers of US Treasury bonds, the need to maintain dollar hegemony, and the Trump administration's deregulatory stance and macroeconomic policies are laying the groundwork for a long-term bull market in stablecoin adoption. Against this backdrop, we expect the total circulating market capitalization of stablecoins to expand into the trillions of dollars.

History of Currency

To understand why stablecoins represent the future of currency and settlement, it is essential to trace the historical evolution of currency and identify the core attributes that enable currency systems to effectively serve society. This includes not only the macro trajectory of currency development but also the rise of dollar hegemony and the "exorbitant privilege" enjoyed by the US as the world’s dominant reserve currency issuer.

- Barter and Commodity Money

Early civilizations relied on barter, directly exchanging goods and services. As societal complexity increased, the inefficiency of barter led to the emergence of commodity money, such as livestock (9000-6000 BC) and shells (around 1200 BC in Asia). These early forms of money had intrinsic or socially recognized value, laying the groundwork for standardized mediums of exchange.

- Metal Money

As trade networks expanded, societies gradually adopted metals as mediums of exchange due to their durability and divisibility. In China during the Zhou Dynasty (around 1000 BC), metal money appeared in the form of small bronze tools and cast shell replicas. By the 7th century BC, true coins independently developed in India, China, and the Aegean region. Indian currency consisted of punched metal discs, while Chinese currency was cast bronze coins, often with holes for stringing. In Anatolia, the Kingdom of Lydia introduced the first standardized coins, certifying their metal content with stamps. This innovation marked the unification of the functions of value storage and medium of exchange, while allowing states to regulate the money supply and profit from seigniorage. The transition from commodity barter to metal money significantly expanded long-distance trade, exemplified by Athenian silver coins financing imperial expansion and circulating widely, while Chinese bronze coins helped unify the East Asian market.

- Paper Money and Credit

While metal money dominated the classical era, medieval China experienced the next major leap with the introduction of paper money. During the Tang Dynasty (618-907 AD), merchants used "flying money" in the form of promissory notes to avoid transporting heavy copper coins over long distances. This system evolved into formal paper currency during the Song and Yuan Dynasties, allowing China to use paper money 500 years ahead of the rest of the world. However, over-issuance led to inflation, and by 1455, the Ming Dynasty abandoned paper currency due to severe devaluation. Although paper money did not reach Europe until centuries later, China's experience highlighted the efficiencies and risks associated with fiat currency. Meanwhile, in 12th century England, the Royal Exchequer used tally sticks to record debts and taxes as a form of credit money. These sticks circulated as "accounting currency" for transactions with the crown and remained in use until the 19th century. These innovations marked the transition of currency to more abstract forms—written instruments and credit records, laying the foundation for modern banking.

- Banknotes, Trading Platforms, and Central Banks

By the late medieval and Renaissance periods (15th-17th centuries), formal banking and the first paper currencies emerged in Europe. Wealthy families, such as the Medici in Florence, operated banks, held deposits, extended credit, and pioneered double-entry bookkeeping, laying the groundwork for modern financial accounting. In the 16th century, Antwerp and Amsterdam became financial centers, with bills of exchange, marine insurance, and international credit supporting the expanding global trade. The establishment of public banks was a significant breakthrough. The Bank of Amsterdam, founded in 1609, accepted various currencies and issued deposit receipts, creating stable ledger money or "bank money" widely used in European trade. Merchants could directly transfer balances on bank ledgers, foreshadowing modern checking accounts. In the 17th century, paper money made its debut in Europe. In 1661, the Stockholm Bank in Sweden issued the first public paper currency, backed by heavy copper coin deposits. Although initially successful, over-issuance led to the bank's collapse in 1664. In 1694, the Bank of England was established, beginning to issue receipts for deposits and government loans as banknotes. These early notes represented currency redeemable for gold and silver. Over time, the Bank of England gained a monopoly on note issuance, marking a key transition from private to centralized, state-controlled currency systems. This period marked the rise of central banks and national currencies.

- Fiat Currency and National Currency

By the 18th century, paper money and banknotes were common in Western economies, but not always stable. During the American Revolutionary War and the French Revolution, governments issued paper money not fully backed by metals—an early form of fiat currency. The "Continental Currency" issued by the Continental Congress rapidly depreciated due to over-issuance, leading to the saying "not worth a Continental." In the 19th century, national currencies began to take on modern forms. Many countries established central banks or treasuries to issue standardized notes and currency. Metal-backed banknotes became the norm in peacetime, restoring public trust. In the UK, the Bank Charter Act of 1844 required Bank of England notes to be backed by gold, becoming the dominant fiat currency. Other countries followed suit, linking their currencies to precious metals to enhance credibility. This marked the beginning of the gold standard era.

- The Gold Standard

In the 19th century, intense debates arose over whether currency should be based on gold, silver, or both. At the century's start, many countries adopted a bimetallic standard, recognizing both gold and silver as legal tender. For example, the Coinage Act of 1792 in the US set a silver-to-gold weight ratio of 15:1. However, as global trade grew and new metal supplies emerged, fluctuations in relative value led to one metal driving the other out of circulation—an example of Gresham's Law. The UK was the first to shift to a pure gold standard in 1816, defining the pound solely in terms of gold and ceasing the minting of high-value silver coins. By the end of the 19th century, other major economies followed suit, with gold becoming the dominant standard for international trade. In the US, the bimetallic debate was particularly intense. After large silver discoveries depressed its value, the "Crime of '73" in 1873 ended the minting of silver dollars, pushing the US toward a de facto gold standard. Despite strong populist pressure to restore silver, gold supporters ultimately prevailed. The Gold Standard Act of 1900 formally defined the dollar as approximately 1/20.67 ounces of gold, solidifying the US commitment to the gold standard monetary system.

- Modern Central Banks and Global Institutions

To manage national currencies and ensure financial stability, countries increasingly relied on central banks. Early examples include Sweden's Riksbank (1668) and the Bank of England (1694). In the 19th and early 20th centuries, more central banks were established, such as the Bank of France (1800), the Imperial Bank of Germany (1876), and the Bank of Japan (1882). In the US, the Federal Reserve System was created in 1913 to address recurring bank panics and regulate credit. Under the gold standard, central banks were typically granted exclusive rights to issue banknotes, such as the Bank of England becoming the sole legal issuer in the mid-19th century, with the Federal Reserve System assuming this role after 1913. Central banks also managed gold reserves and maintained fixed exchange rates, ensuring the convertibility of paper currency into gold was a core responsibility. However, during World War I (1914-1918), many countries suspended gold convertibility to finance war expenditures through money printing. The US also suspended gold convertibility for domestic transactions during the Great Depression in 1933.

- Electronic Money

Forms of currency have continuously evolved with technological advancements. In the mid-20th century, banks began using computers, leading to electronic money transfers. By the 1970s, the SWIFT system enabled instant global movement of funds through electronic signals, replacing the need for physical cash. At the consumer level, payment cards changed how people accessed money, starting with the Diners Club credit card in 1950, followed by widespread adoption of credit and debit cards in the 1960s and 70s. By the end of the 20th century, most currency existed in the form of digital ledger entries rather than paper money. The internet accelerated this shift. By the 1990s and 2000s, online banking and platforms like PayPal allowed anyone to send money electronically. In the 2010s, innovations in mobile payments and fintech surged, from Kenya's M-Pesa to applications like Alipay and Venmo. Today, in developed economies, most currency is fully digital, with physical cash accounting for only a small portion of the total money supply.

Throughout history and civilization, currency has independently evolved around a set of fundamental characteristics that enable it to effectively serve as a medium of exchange, a store of value, and a unit of account. These attributes include:

Interchangeability: Each unit of currency must be interchangeable with other units of the same denomination. For example, a $100 bill functions identically to any other $100 bill, ensuring value uniformity and eliminating the need to distinguish between individual units.

Durability: Currency must withstand long-term physical wear. It should maintain its shape and function after repeated use and transactions, ensuring long-lasting circulation.

Portability: Effective currency must be easy to transport and usable over long distances. Whether physical or digital, it must be efficiently transferable between parties, avoiding excessive friction or costs.

Divisibility: Currency must be easily divisible into smaller units to facilitate transactions of varying sizes.

Uniformity: All banknotes of the same denomination should look and value the same. Standardization can enhance trust, simplify recognition, and reduce transaction errors.

Scarcity: To maintain purchasing power, currency must exist in limited supply. If the supply grows too quickly relative to demand, the value of the currency will diminish, leading to inflation and a collapse of trust.

Acceptability: Currency must be widely recognized and accepted as a valid form of payment. Broad social and institutional recognition is the foundation of its practicality and legitimacy.

Over time, the nature of currency has continuously evolved in the pursuit of greater efficiency. People have always been committed to developing forms of currency that enable faster transaction settlements, lower circulation costs, and are not limited by geography, evolving from localized barter systems to global digital networks.

Dollar Hegemony

The United States has not always enjoyed the privilege of issuing the world’s reserve currency, nor has its financial system always been the most dominant, centralized, and legally monetized, with the deepest and most investable capital markets globally. The rise of the dollar has been accompanied by a long struggle to establish national currencies and central banks. In fact, the evolution of American currency bears a striking resemblance to the current stablecoin ecosystem, from the circulation of banknotes during the National Banking Era to the rise, regulation, and controversy surrounding money market funds (MMFs).

We will briefly explore how the dollar ascended to global hegemony, providing important context for understanding the long-term tailwinds supporting stablecoin adoption. In our view, understanding stablecoins requires not only a technological perspective but also an appreciation of the political and economic forces that shape their trajectory.

The History of the US Banking System and the Dollar

Hamilton's Blueprint (1775-1791)

Before establishing a formal banking system, the American Revolutionary War and the Confederation period plunged the nation into financial chaos. The war was financed through "Continental Currency," which rapidly depreciated, leading to the saying "not worth a Continental." To restore order, President George Washington appointed Alexander Hamilton as the first Secretary of the Treasury. Hamilton proposed that the federal government assume state debts, issue federal bonds, and create a national bank to regulate currency and credit. Disturbed by the chaos of competing state currencies, Hamilton persuaded Congress to charter the First Bank of the United States, calling it "an indispensable political machine for the nation," believing it was key to unifying the republic's financial system.

The Era of the First Bank (1791-1811)

In 1791, Congress chartered the First Bank of the United States, signed by President Washington, becoming the nation’s de facto first central bank. Headquartered in Philadelphia, it had a capital of $10 million, with 20% held by the government and 80% privately owned. The bank acted as the federal government’s fiscal agent, managing deposits, taxes, payments, and issuing currency backed by gold and silver that was accepted nationwide. Under President Thomas Willing, the bank opened branches in major cities, stabilizing the post-war economy. However, the establishment of the bank sparked strong opposition from Jefferson and Madison, who deemed it unconstitutional and elitist. Despite the bank's effective operations, political resistance grew, and in 1811, Congress narrowly voted against renewing its charter. Without a central bank, the US faced financial chaos during the War of 1812, highlighting the need for new national institutions and laying the groundwork for the establishment of the Second Bank of the United States.

The Second Bank and Jackson's "Bank War" (1816-1836)

To address the financial chaos following the War of 1812, Congress chartered the Second Bank of the United States in 1816 for a 20-year term with a capital of $35 million, also headquartered in Philadelphia. Even President James Madison, who had opposed the First Bank, acknowledged the need for a central financial institution to stabilize the post-war economy. Under Nicholas Biddle's leadership, the Second Bank aimed to regulate credit and the money supply. However, it became the target of a populist movement led by President Andrew Jackson opposing concentrated financial power. Jackson labeled the bank a "nest of vipers and thieves," vetoed its charter renewal, and withdrew federal deposits, effectively destroying the institution.

Free Banking and "Wildcat Currency" (1837-1862)

From the late 1830s until the Civil War, a period known as the Free Banking Era emerged, where banking affairs were controlled by state governments, and the collapse of the Second Bank left a lack of federal oversight. States like New York passed "Free Banking" laws, allowing almost anyone who met basic requirements and provided bond collateral to open a bank. Without federal supervision, over 8,000 different banknotes circulated, each trading at different discounts based on the issuing bank's creditworthiness and the distance to the redemption location. Some institutions, known as "wildcat banks," operated in remote areas to avoid redemption, issuing notes not fully backed by gold and silver, leading to widespread instability and fraud. Bank failures were common in places like Michigan, and the panics of 1837 and 1857 intensified public demand for a national banking framework and a unified currency.

Civil War Financing and the National Banking Act (1863-1879)

The Civil War triggered a financial revolution, with the federal government eager to fund the war. Initially relying on bond sales and tax increases, the North soon faced a cash shortage, suspending gold and silver convertibility by the end of 1861, causing currency to vanish from circulation. In 1862, Congress passed the Legal Tender Act, authorizing the issuance of $150 million in paper currency known as "greenbacks," which were non-interest-bearing Treasury notes designated as legal tender but not backed by gold. These legal tender notes filled a critical currency gap, although trading at a discount to gold led to inflation. Ultimately, about $450 million in greenbacks were issued, marking the first large-scale use of legal tender in US history, continuing into the 20th century. While the system provided stability and funded victory, it also triggered significant inflation, with Northern prices rising about 80% during the war. After 1865, efforts were made to restore a gold-backed currency, ultimately reestablishing gold and silver convertibility at a fixed rate of $20.67 per ounce in 1879.

Gold, Populism, and Morgan's Midnight Rescue (1879-1907)

The successful restoration of gold and silver payments in 1879 marked the official entry of the US into the classical gold standard era, with the dollar pegged to gold at $20.67 per ounce, and greenbacks, gold certificates, and national bank notes freely convertible into gold. From 1880 to 1914, this period saw robust economic growth and rapid industrialization, with the US rising as a global economic power. However, bank panics occurred frequently (in 1884, 1890, 1893, and 1907), highlighting deep structural flaws in the financial system. During these crises, credit and money dried up, interest rates soared, and banks hoarded reserves, leading to a contraction in lending. Clearinghouse associations in major cities attempted to stem losses by issuing emergency loan certificates, but these temporary measures underscored the lack of a formal liquidity injection mechanism. Debates over monetary policy intensified, with farmers and debtors in the West and South demanding the free coinage of silver to expand the money supply in response to deflation and falling agricultural prices. The panic of 1907 forced financier J.P. Morgan to personally organize a private sector rescue, locking in the heads of New York trust companies until a rescue agreement was reached, an event that ultimately catalyzed the creation of the Federal Reserve System.

From Jekyll Island to the Federal Reserve System (1907-1913)

In 1910, Senator Nelson Aldrich secretly convened five prominent financiers at Jekyll Island to devise a new central banking scheme, which Paul Warburg mockingly referred to as "secretive as a Confederate Navy." The result was the Aldrich Plan, proposing the establishment of a central institution with regional branches, ensuring flexibility through currency backed by commercial paper and gold, governed by bankers. In 1912, Aldrich unveiled the plan, but the political winds had shifted: the Democratic Party, long skeptical of concentrated financial power, won the White House and Congress after Woodrow Wilson's election. The Aldrich Plan was obstructed due to its perceived closeness to Wall Street and its secretive origins. However, its core ideas were retained. Wilson acknowledged that the plan was "60-70% correct." A proposal was reworked by Congressman Carter Glass and Senator Robert Latham Owen, and after intense debate, Wilson finalized it. On December 23, 1913, the Federal Reserve Act was signed, establishing the Federal Reserve System, granting 12 regional "bankers' banks" the authority to issue flexible Federal Reserve notes and manage the national monetary system.

Early Federal Reserve and the Roaring Twenties (1914-1928)

The Federal Reserve System began operations at the outbreak of World War I (1914-1918). Although the US remained neutral until 1917, the war had an immediate impact on the economy. Capital flowed from war-torn Europe into the US, which became the primary supplier of weapons and materials to the Allies, primarily financed through massive loans. The New York financial market rapidly expanded, and the dollar began to replace the pound in international transactions. Many belligerent nations suspended the gold standard to print money to finance the war, while the US maintained the gold standard, leading to a surge in gold inflows. By 1917, the US held about one-third of the world's central bank and Treasury reserves (approximately 11,000-12,000 tons). By the 1920s, the US share of reserves increased to about 40%. At the end of the war, the US emerged as the world's largest creditor, financing most of the Allies' war expenditures, shifting the global financial center from London to New York. By the mid-1920s, the dollar had become a strong competitor to the pound as a reserve and loan currency. However, imbalances intensified: the US accumulated vast gold reserves and actively lent abroad, while much of Europe remained mired in post-war debt and economic fragility.

The Great Depression and the New Deal (1929-1945)

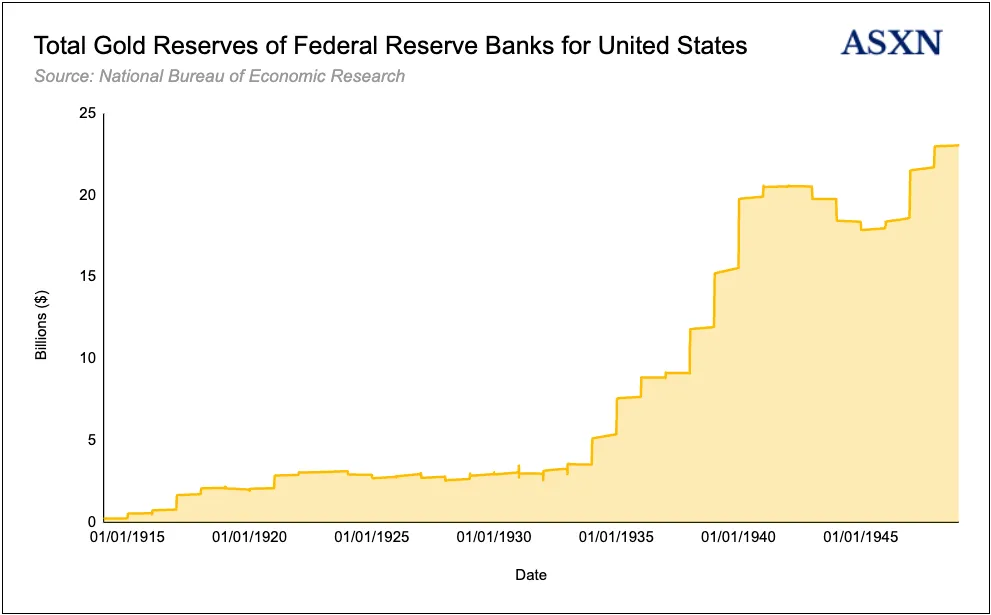

In October 1929, the long-accumulated stock market bubble burst, triggering the Wall Street crash and evaporating billions of dollars in wealth. This collapse destroyed confidence and rippled through the banking system, causing many institutions to fail due to exposure to stock loans or securities affiliates. Nearly 9,000 banks (about one-third of all banks in the US) closed, and the Federal Reserve failed to act decisively. Its decentralized structure led to internal disagreements, prioritizing the protection of the gold standard over expanding credit. Some officials took a "liquidationist" stance, believing that weak banks and borrowers should be allowed to fail. The result was a one-third contraction in the money supply, leading to deflation, a halving of GDP, and an unemployment rate of 25%. President Roosevelt declared a bank holiday, created the FDIC through the Glass-Steagall Act, and separated commercial banks from investment banks. Through Executive Order 6102, Americans were forced to surrender gold at a price of $20.67 per ounce in exchange for dollars, effectively nationalizing gold to prevent a run on the dollar and achieve monetary expansion. The Gold Reserve Act of 1934 confirmed this, devaluing the dollar and raising the gold price to $35 per ounce. With most of the world's gold and a stable banking system, the dollar became the dominant currency, laying the foundation for the post-war global monetary order.

Bretton Woods System (1944-1971)

After World War II, the United States emerged with unparalleled economic dominance, producing half of the world's output and holding about 70% of official gold reserves, placing it in a unique position to rebuild the international monetary system. The pound was weakened by massive war debts and a shortage of dollars, leading many countries to implement currency controls. Learning from the failures of post-World War I and the 1930s devaluations, 44 allied nations established a new framework at the Bretton Woods Conference in July 1944. Led by US Treasury official Harry Dexter White and British economist John Maynard Keynes, representatives created the Bretton Woods system, establishing the International Monetary Fund and the World Bank, and fixing exchange rates to the dollar, which was convertible to gold. This system effectively established the dollar's core position in global finance, supported by US economic strength and gold reserves, a status later referred to as "exorbitant privilege," allowing the US to borrow freely and run external deficits. For the next quarter-century, the Bretton Woods system defined international finance until its collapse opened the era of fiat dollars.

Nixon Shock and Petrodollars (1971-early 1980s)

On August 15, 1971, President Nixon unilaterally suspended the dollar's convertibility into gold, ending the Bretton Woods system and severing the last link between the dollar and gold. This marked a shift to a fiat currency regime, with the dollar and other major currencies floating freely, their values determined by market forces. Despite losing gold backing, the dollar retained and expanded its status as a global reserve currency due to a lack of alternatives and continued confidence in the US financial markets. After the oil crisis of 1973-74, OPEC significantly raised oil prices, forcing importing countries to acquire more dollars to pay for energy costs. In 1974, the US reached a strategic agreement with Saudi Arabia: in exchange for military protection and weapons, Saudi Arabia would price oil in dollars and invest its oil revenues in US Treasury securities. This arrangement was quickly emulated by other OPEC member countries, establishing the petrodollar system. Oil-exporting countries accumulated large dollar surpluses, depositing them in international banks or reinvesting in dollar assets, a process known as the petrodollar recycling. By 1975, all OPEC countries adopted dollar pricing, embedding the dollar in global trade and finance. This supported ongoing US budget and trade deficits while suppressing interest rates, reinforcing dollar hegemony and granting the US new "exorbitant privilege." In the 1970s, money market funds emerged as corporate cash management tools, with the first (the Reserve Fund) launched in 1971, holding assets of $1 million.

Deregulation, Globalization, and Eurodollars (1980s-1999)

In the 1980s and 1990s, the dollar's hegemony was solidified against the backdrop of financial deregulation, victory over inflation, and accelerated globalization. Under Federal Reserve Chairman Paul Volcker, inflation fell from about 13% in 1980 to about 3% in 1983, restoring confidence in the dollar as a stable store of value. By the mid-1980s, the dollar soared to historical highs, prompting the Plaza Accord in 1985, where the US coordinated with major allies to devalue the dollar, leading to a roughly 40% decline against the yen and mark by 1987, helping to reduce trade imbalances. Financial deregulation, including the Depository Institutions Deregulation and Monetary Control Act of 1980, eliminated interest rate ceilings on deposits and expanded the Federal Reserve's services, allowing banks to compete for deposits more effectively. In the 1990s, globalization intensified, and the dollar became the preferred currency for expanding global capital markets. The Eurodollar market flourished, and by the late 1990s, about 64% of global debt was denominated in dollars, with the dollar accounting for 59% of foreign exchange reserves and 58% of international payments, solidifying its core position in the global financial system.

Global Financial Crisis and Quantitative Easing (2000s)

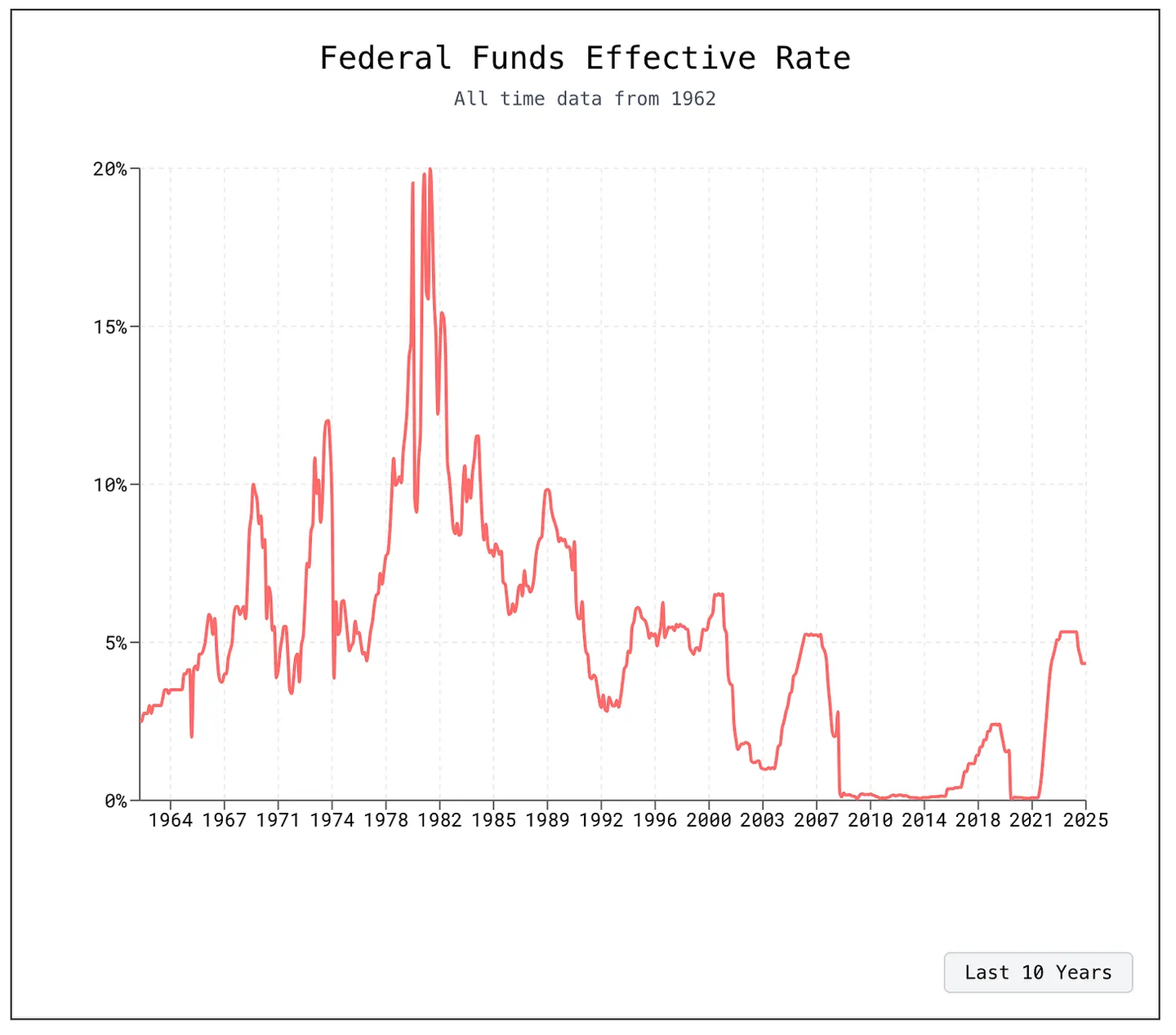

The 2000s tested the US banking system and the dollar, particularly during the global financial crisis of 2007-2009, the most severe economic recession since the Great Depression. Although the crisis began in the US housing and banking sectors, it ultimately reinforced the dollar's status as a global safe haven. In 2007, hedge funds and mortgage institutions began to fail; by March 2008, Bear Stearns was absorbed by JPMorgan with Federal Reserve support. The bankruptcy of Lehman Brothers in September 2008 marked the peak of the crisis, freezing interbank lending and triggering runs on money market funds, with one "breaking the buck." A global contagion followed, as many foreign banks held US mortgage securities or relied on dollar financing. The US implemented massive countermeasures: the Federal Reserve lowered interest rates to near zero, created emergency lending facilities, and established dollar swap lines with foreign central banks, becoming the global lender of last resort. The Treasury launched a $700 billion TARP program to inject capital into banks and stabilize institutions like AIG. The FDIC guaranteed bank debt and expanded deposit insurance to $250,000. Starting at the end of 2008, the Federal Reserve initiated quantitative easing (QE), purchasing long-term Treasury bonds and mortgage-backed securities. The Dodd-Frank Act of 2010 implemented stricter capital and liquidity rules, while subsequent rounds of QE (QE2 in 2010, QE3 from 2012-2014) supported a slow but steady recovery, expanding the Federal Reserve's balance sheet to $4.5 trillion.

Pandemic Quantitative Easing and De-dollarization (2010-2025)

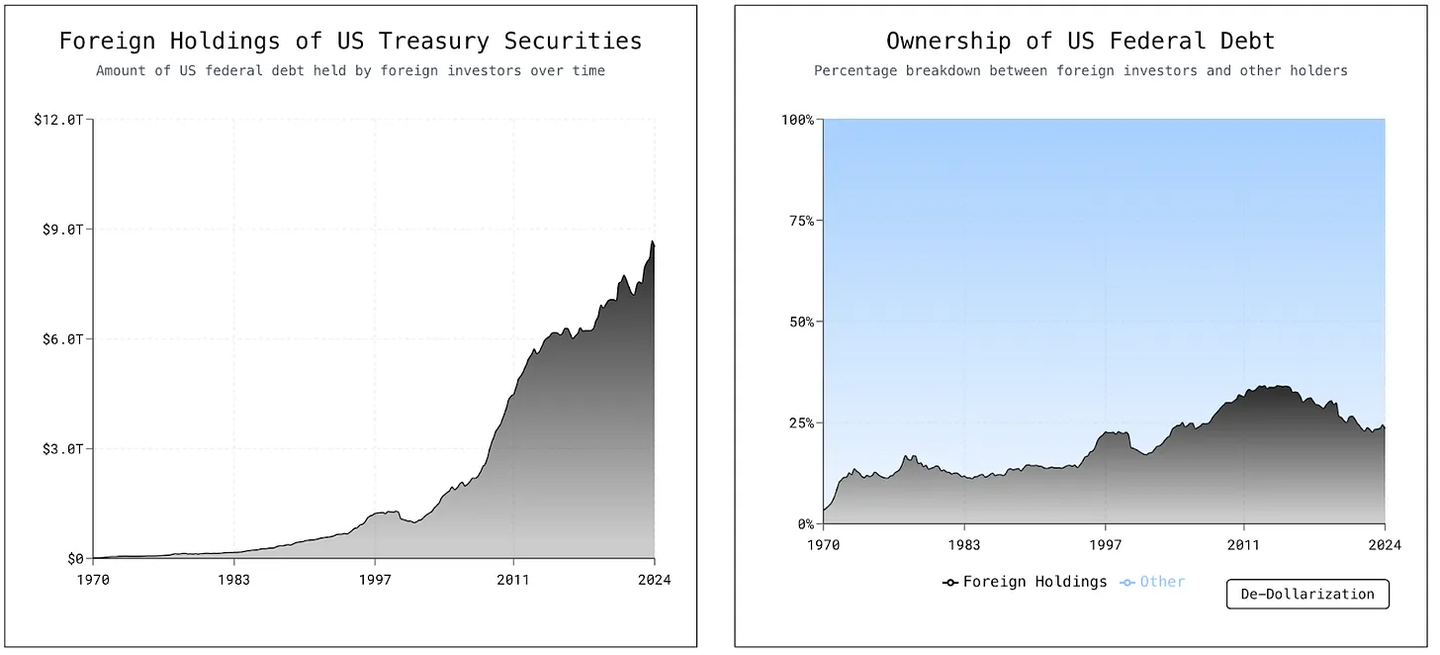

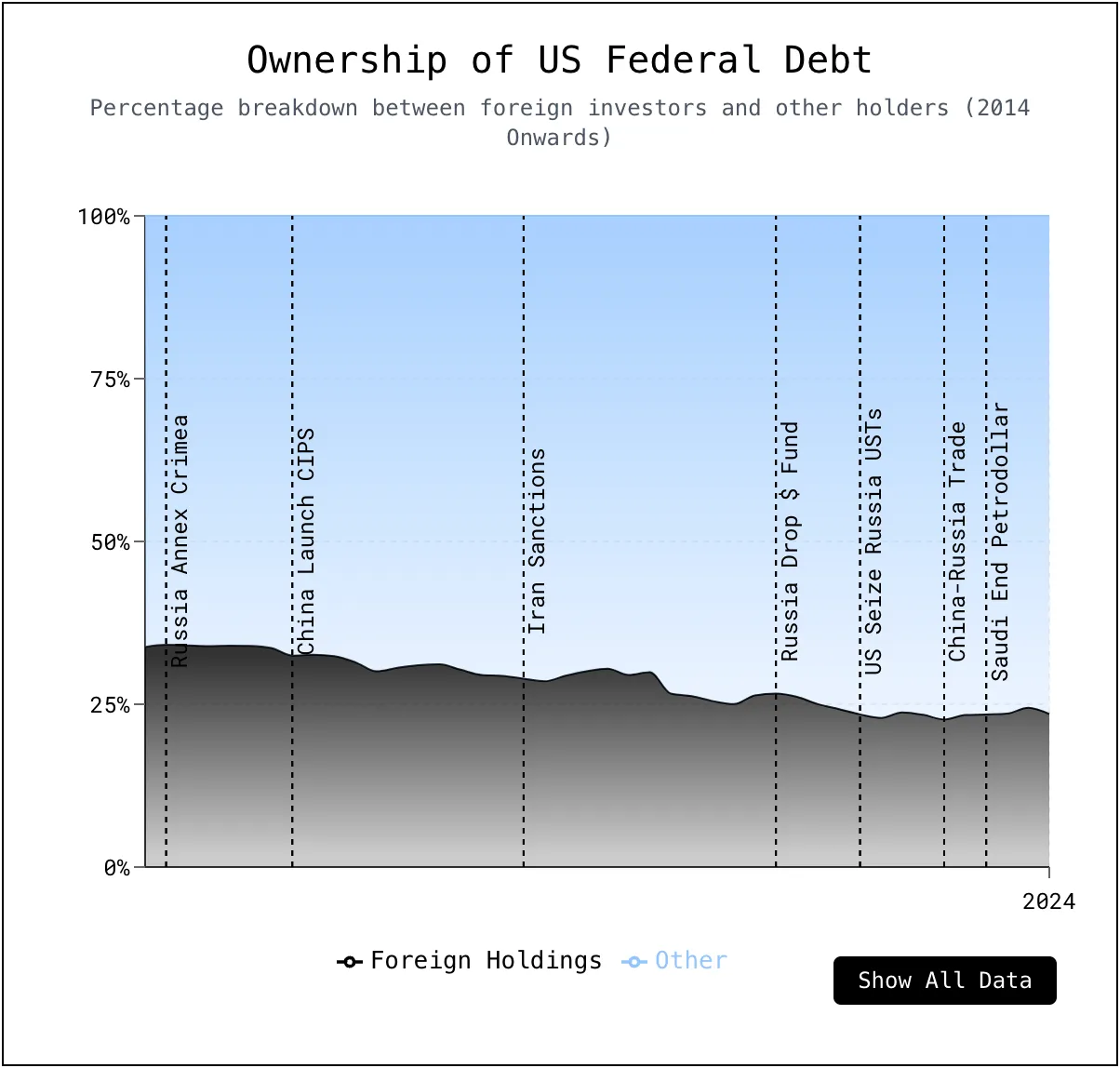

Over the past decade, the US has experienced an unprecedented expansion of monetary stimulus. After QE3 ended in 2014, the Federal Reserve's balance sheet exceeded $4 trillion, four times its pre-crisis size. A brief attempt to shrink the balance sheet in 2017 was interrupted by a 2019 repo market shock that exposed the system's reliance on Federal Reserve liquidity. In response to COVID-19, the Federal Reserve lowered interest rates to zero, restarted QE, and launched emergency tools, nearly doubling assets to nearly $9 trillion by mid-2022, accounting for 36% of GDP. Meanwhile, over $5 trillion in fiscal stimulus pushed federal debt to 98% of GDP for the fiscal year 2024. Inflation reached 9% in 2022, forcing the Federal Reserve to reverse course, raising interest rates above 5% and reducing the balance sheet to $6.8 trillion by early 2025. The dollar still dominates the foreign exchange market, accounting for 88% of transactions reported by the BIS, but its global reserve share has declined from 66% in 2015 to 57.8% in the fourth quarter of 2024. The trend of de-dollarization is accelerating: Russia's frozen reserves due to the invasion of Ukraine have raised awareness of dollar risks; Saudi Arabia's decision not to renew the petrodollar agreement marks a symbolic shift; Iran increasingly settles trade in non-dollar currencies; and China is promoting renminbi trade settlement, especially after the intensification of tensions with the US during the Trump tariff war.

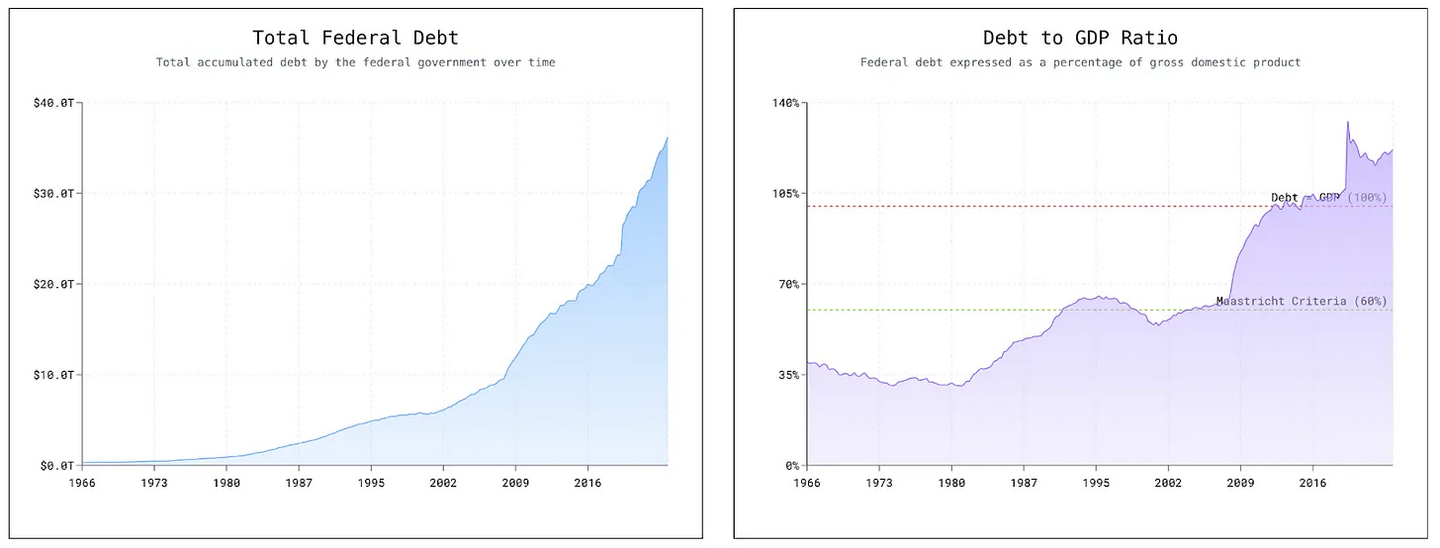

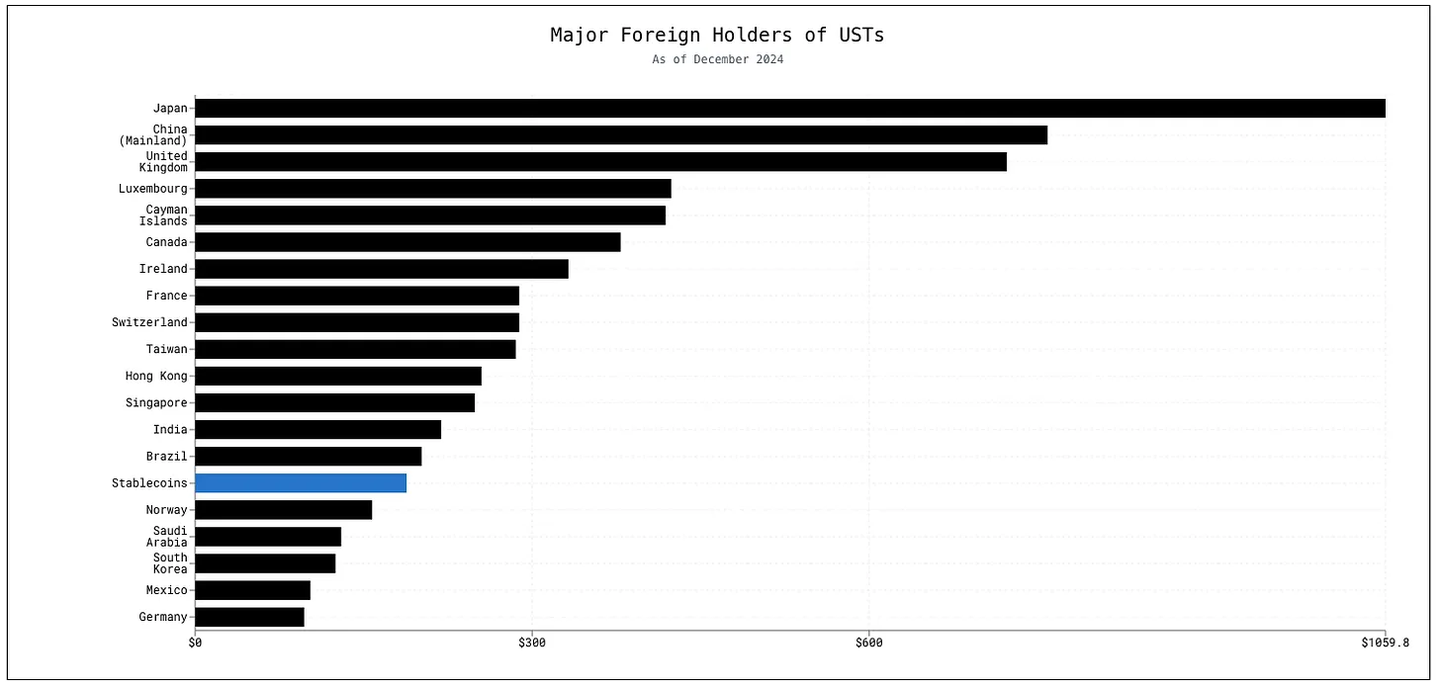

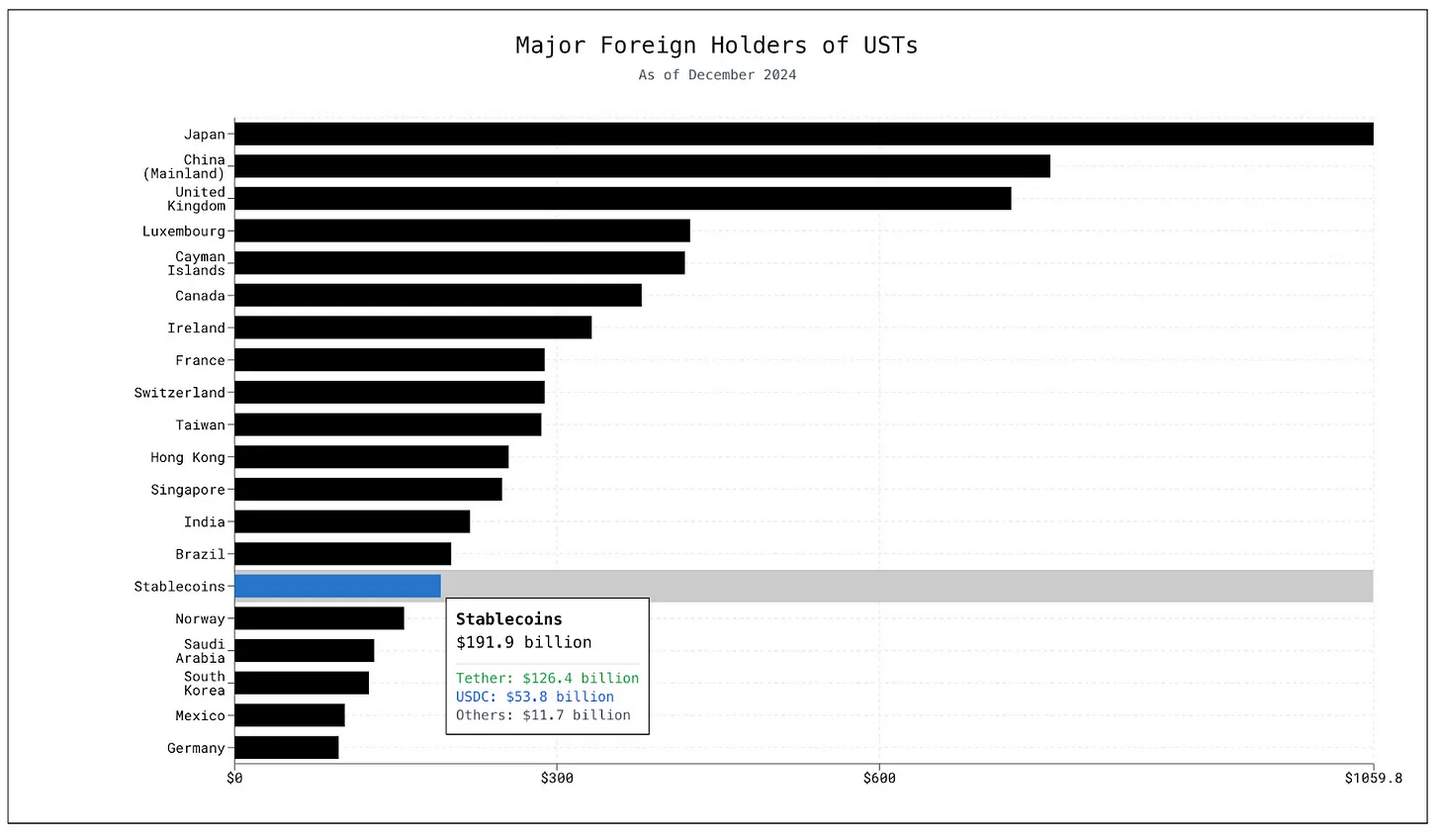

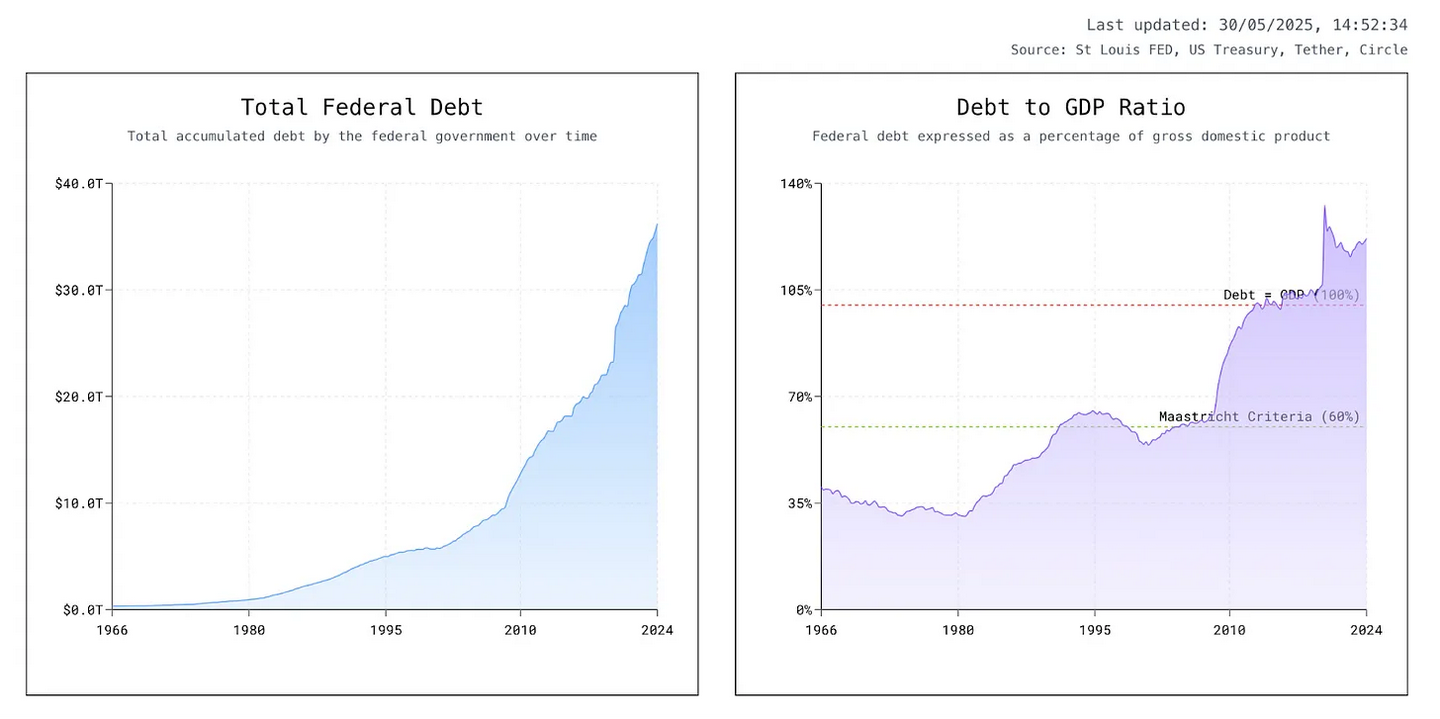

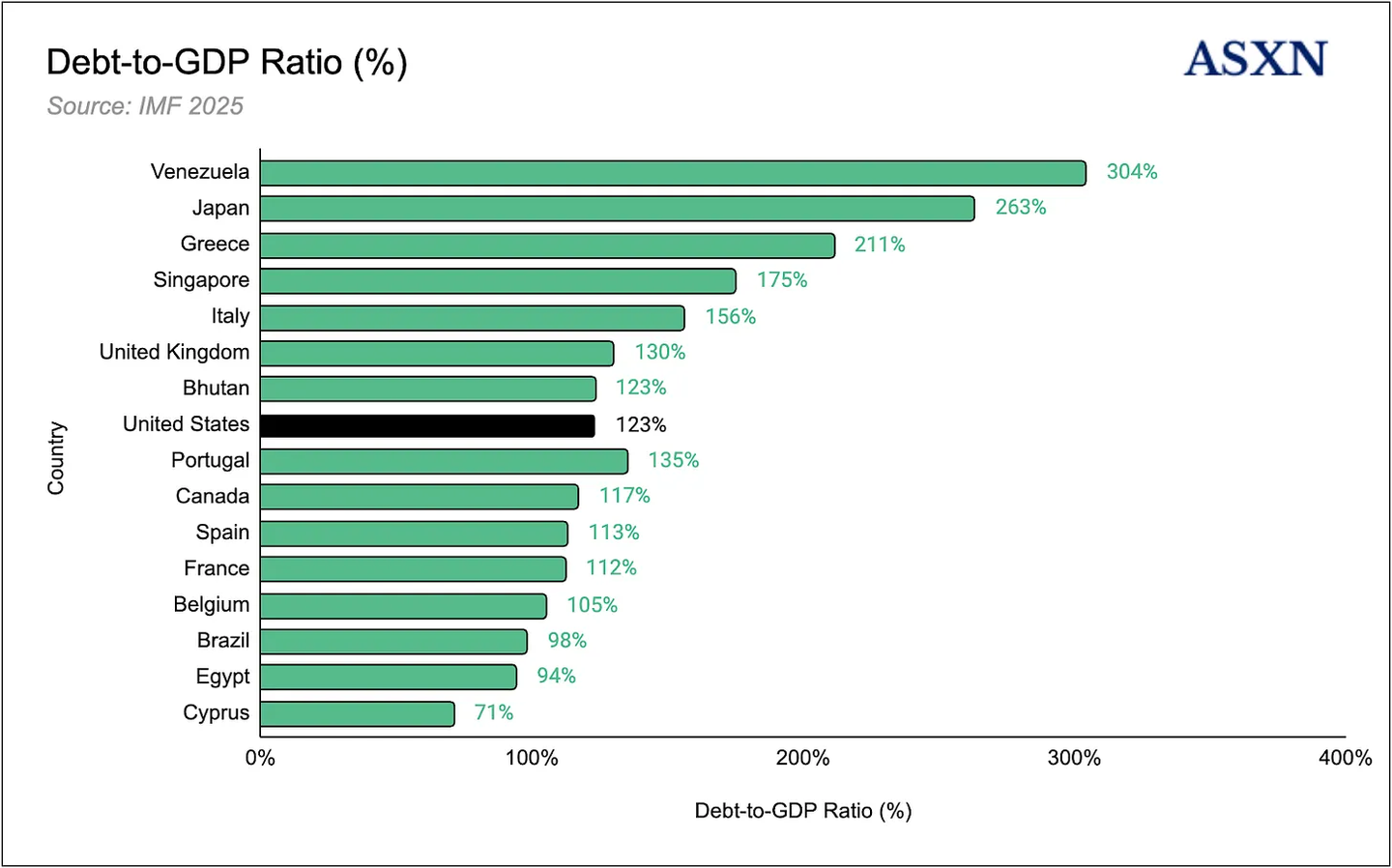

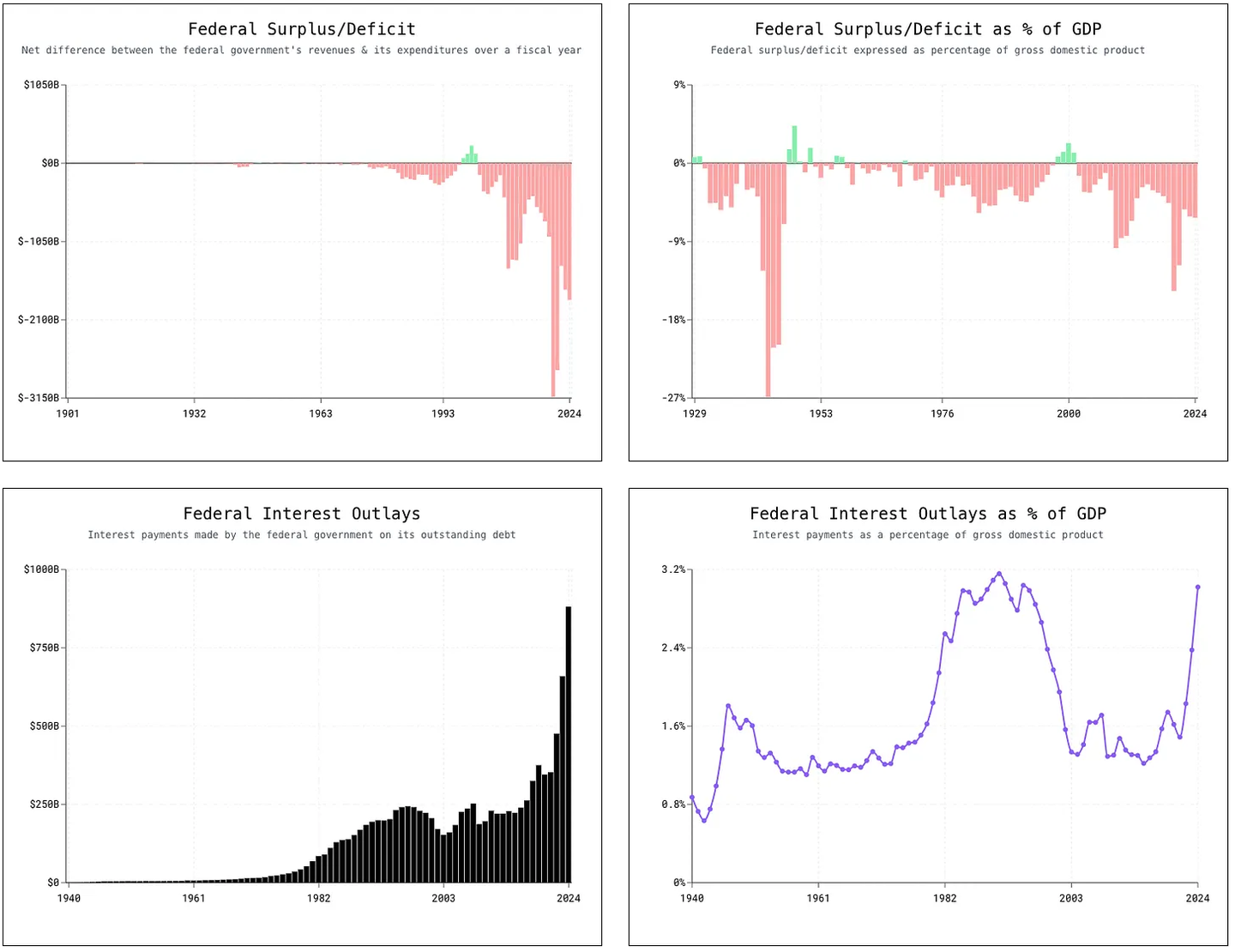

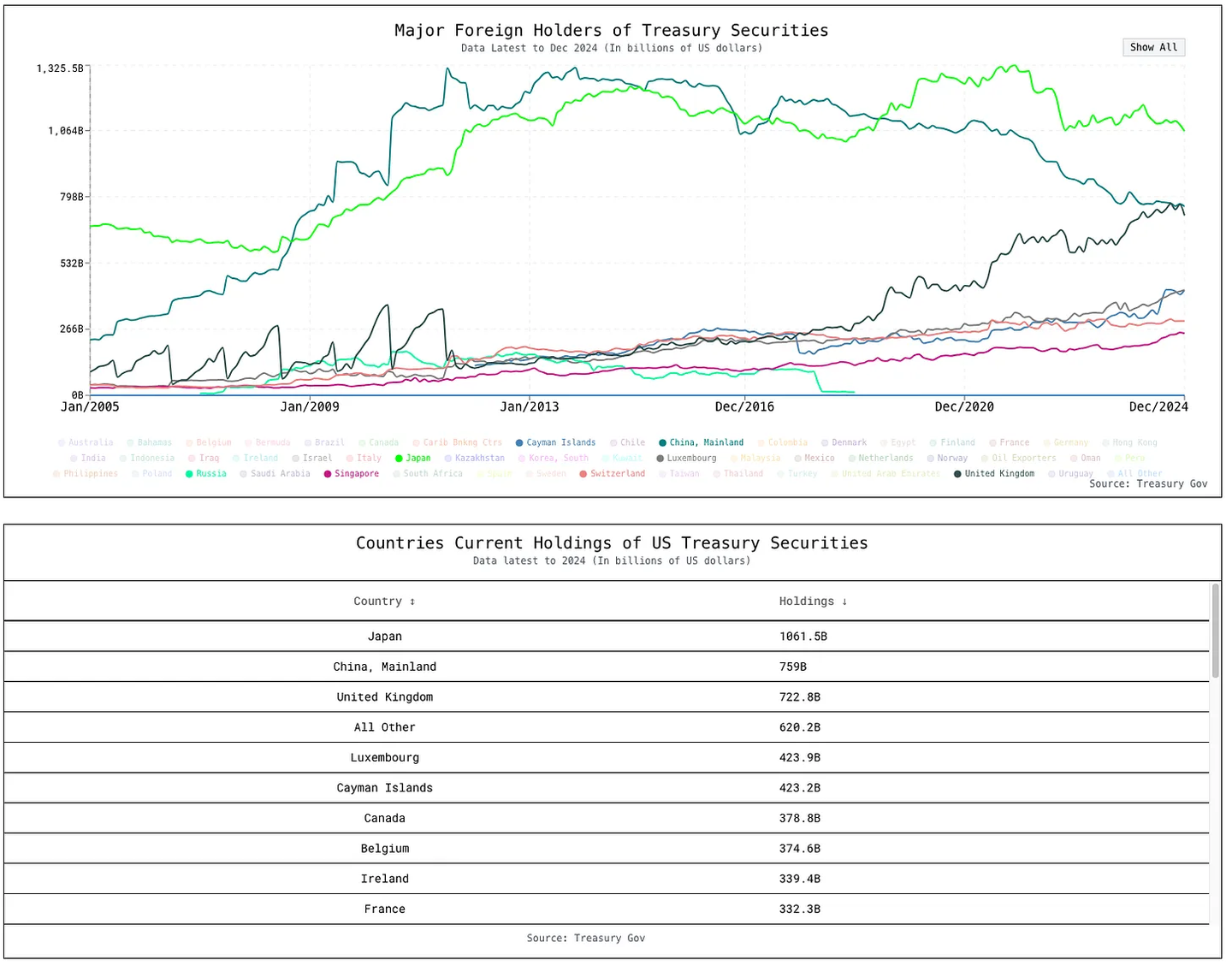

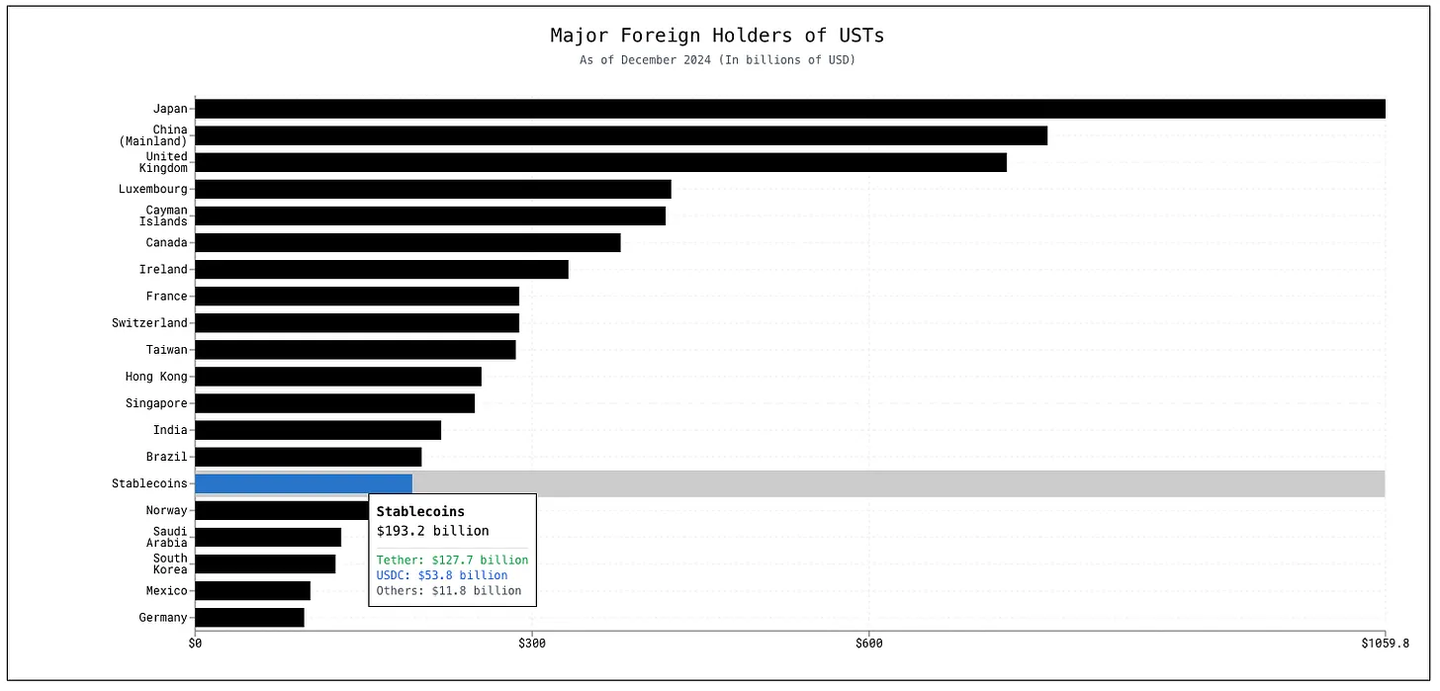

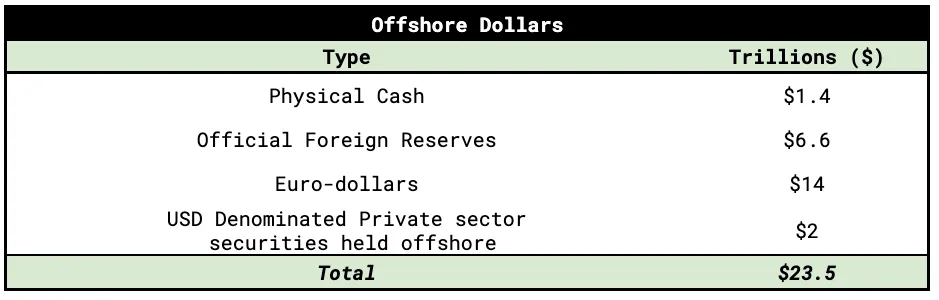

Since Nixon closed the gold window in 1971, the dollar has floated freely as a pure fiat currency. Today, 12 regional Federal Reserve Banks issue a single national currency—the Federal Reserve note—while the US Treasury mints coins. Almost all other "dollars" exist in the form of electronic bank deposits settled through the Federal Reserve system. The federal government finances itself by selling Treasury securities, and the Treasury market remains the deepest pool of safe-haven assets globally: foreigners hold about $8.8 trillion in Treasury securities, with Japan alone holding $1.13 trillion. Ongoing global demand keeps yields relatively low, with the yield on 10-year Treasuries hovering around 4%, despite publicly held debt now reaching 122% of GDP and continuing to rise. This "reserve currency dividend" is another facet of dollar hegemony: the US can run large deficits and borrow at low costs because the world needs dollar assets for trade, security, and regulation.

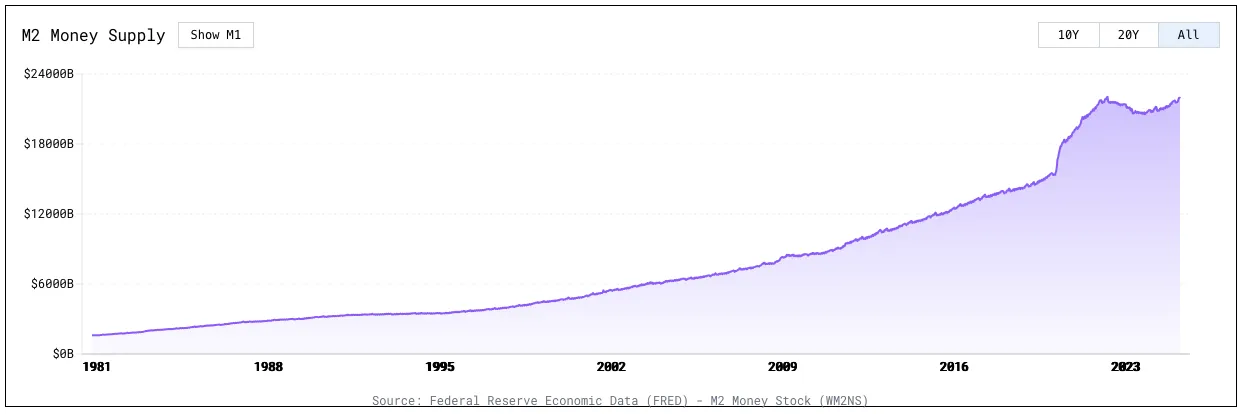

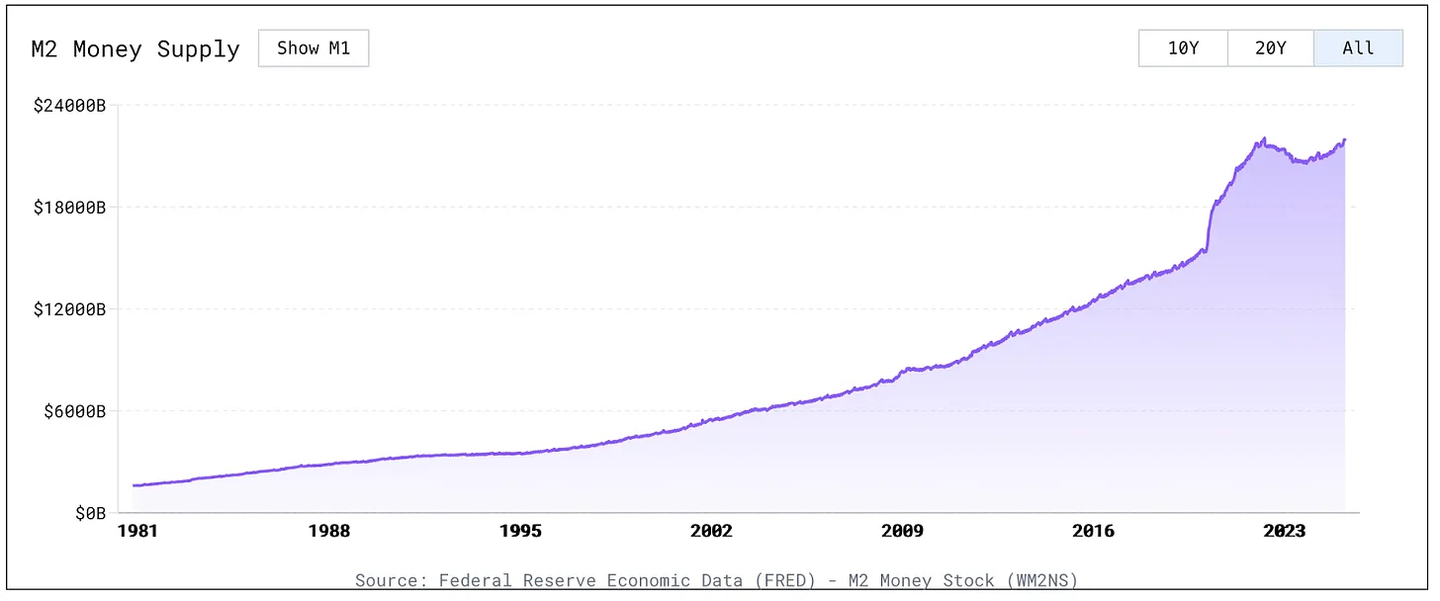

Another characteristic of the modern American monetary system is its high degree of digitization. Of the approximately $21 trillion in broad money (M2), about $18.5 trillion (nearly 90%) consists of digital ledger entries in commercial banks or the Federal Reserve's reserve database. The physical currency in circulation amounts to only $2.36 trillion, with the Federal Reserve estimating that about 60% (especially $100 bills) is held overseas as a portable store of value. Despite the digitization of currency, most US retail payments still rely on traditional infrastructure like the ACH system from half a century ago, with transfers often settling the next day or longer.

In summary, today's dollar primarily exists in digital form, officially unified, based on fiat currency, globally coveted, yet its payment network is only partially modernized, and the scale of the Federal Reserve's balance sheet and its future affordability remain long-term critical issues for the system.

Overview of Stablecoins

Stablecoins represent the next stage in the evolution of currency and payment systems, laying the foundation for a financial system with faster settlement speeds, lower costs, seamless cross-border functionality, native programmability, and robust audit trails. They essentially encapsulate the dollar in software, enabling it to move at lightning speed anywhere with internet coverage. In simple terms, stablecoins are the fastest form of the dollar's existence.

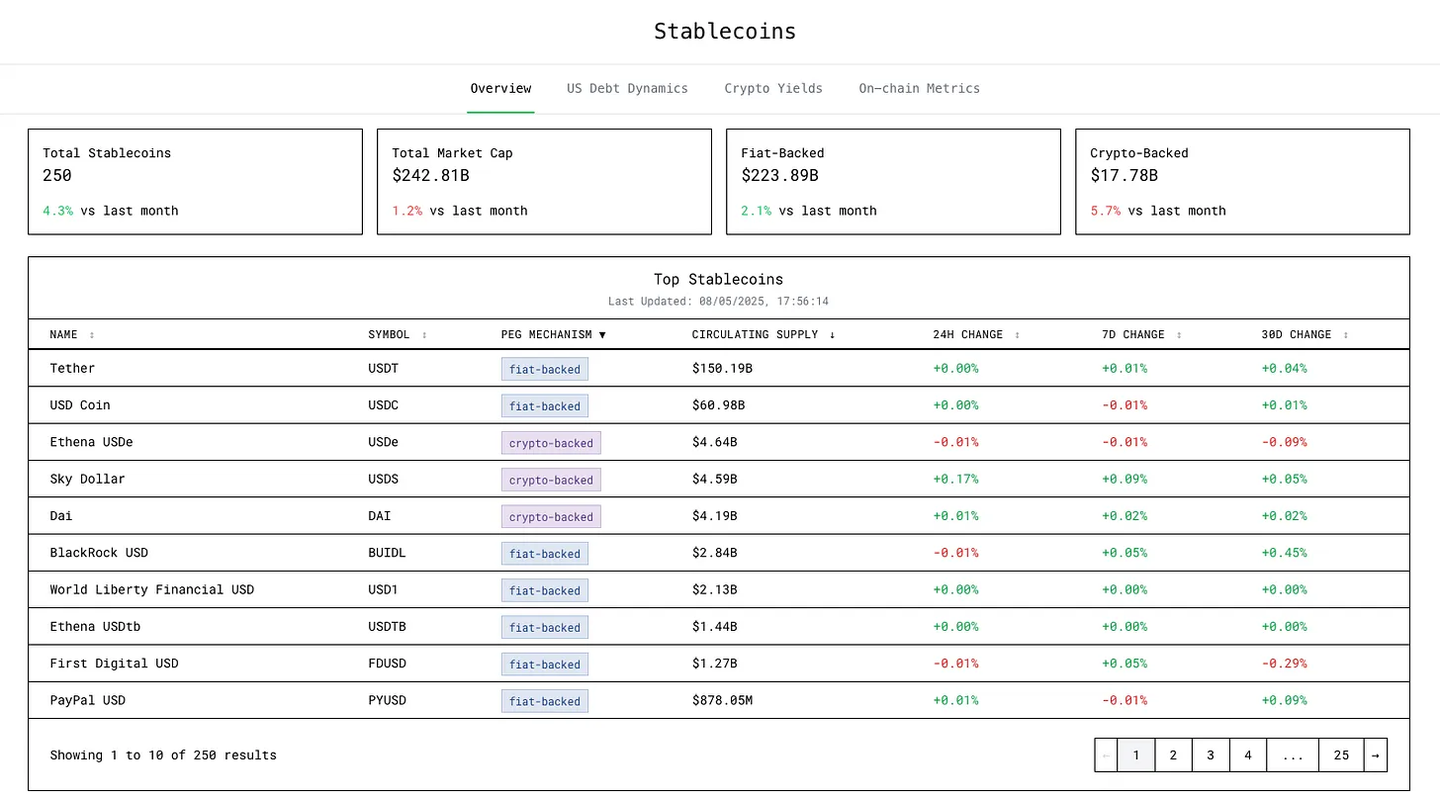

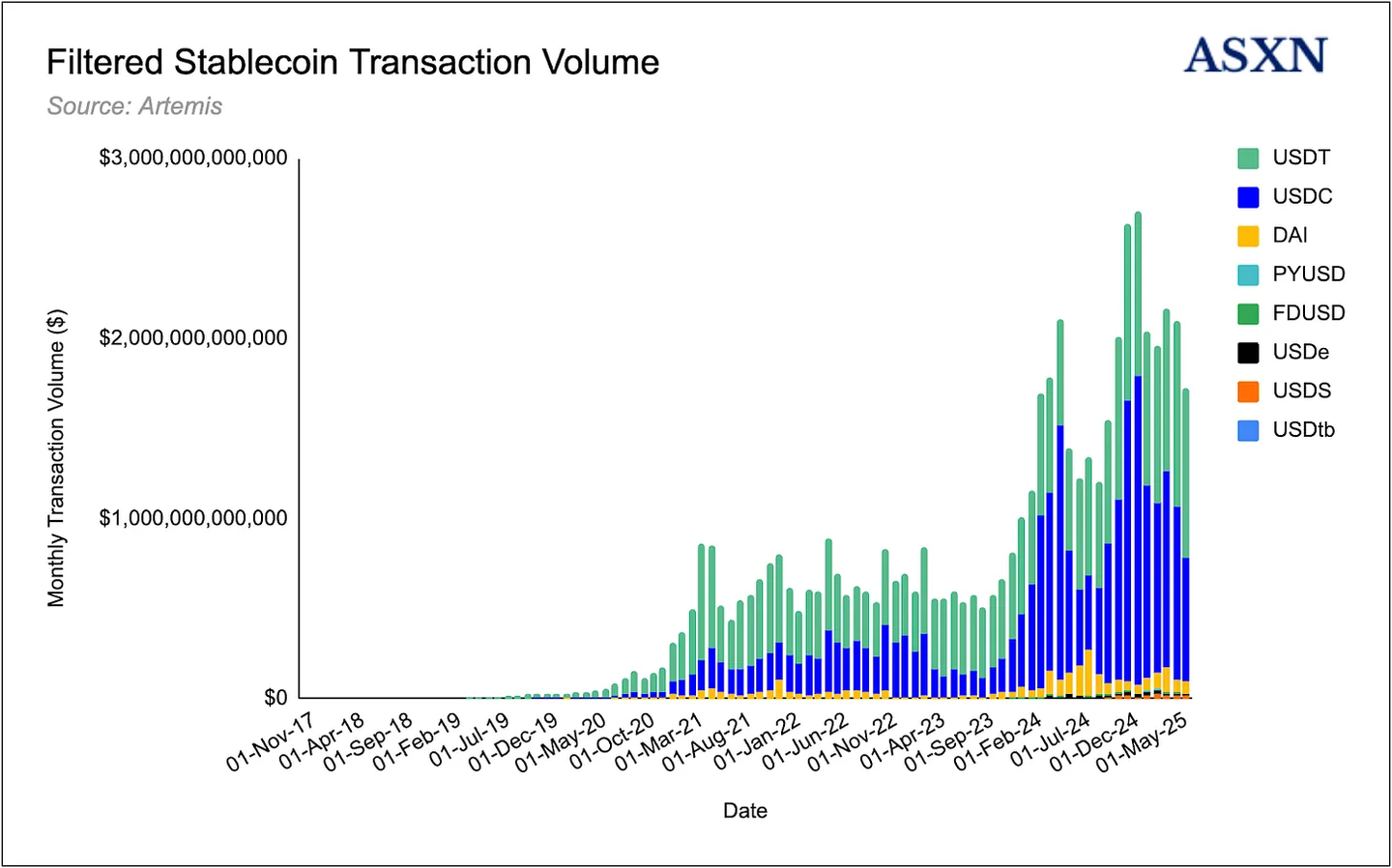

Stablecoins have become the most prominent product in cryptocurrency—market fit, with a growth trajectory reflecting extraordinary adoption rates. The market has expanded from a total market capitalization of $30 million in 2018 to over $250 billion today, with a compound annual growth rate of 263%. Initially used as crypto-native collateral and settlement mechanisms, particularly by market makers and arbitrageurs, stablecoins have now evolved into widely adopted financial primitives. Today, trading firms and market makers regularly hold stablecoins on their balance sheets, while decentralized finance (DeFi) protocols have deeply embedded stablecoins into collateral structures and trading pairs. Centralized exchanges are increasingly shifting from Bitcoin-collateralized perpetual contracts to margin trading based on stablecoins. In addition to internal applications within crypto, stablecoins are gaining traction among citizens in high-inflation or politically unstable regions as a means of storing value and as a fast, low-cost remittance tool. This broader adoption has benefited from significant improvements in infrastructure, including more efficient deposit and withdrawal channels, high-throughput low-fee blockchains, better-designed wallets, and user-friendly applications based on private key management advancements.

Categories of Stablecoins

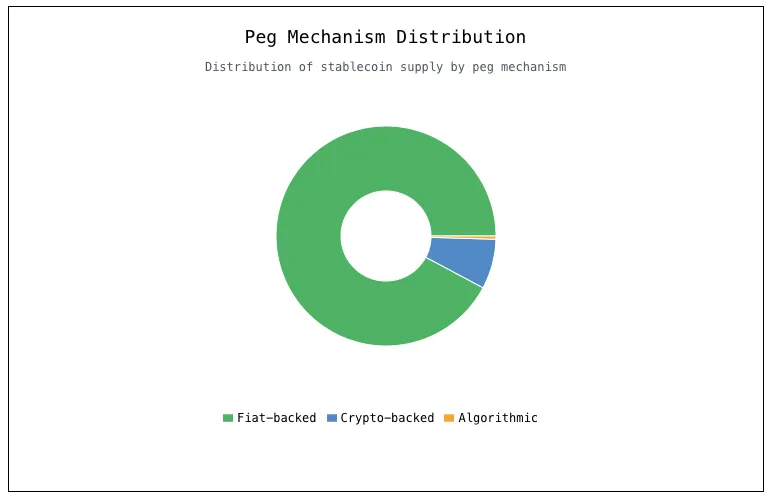

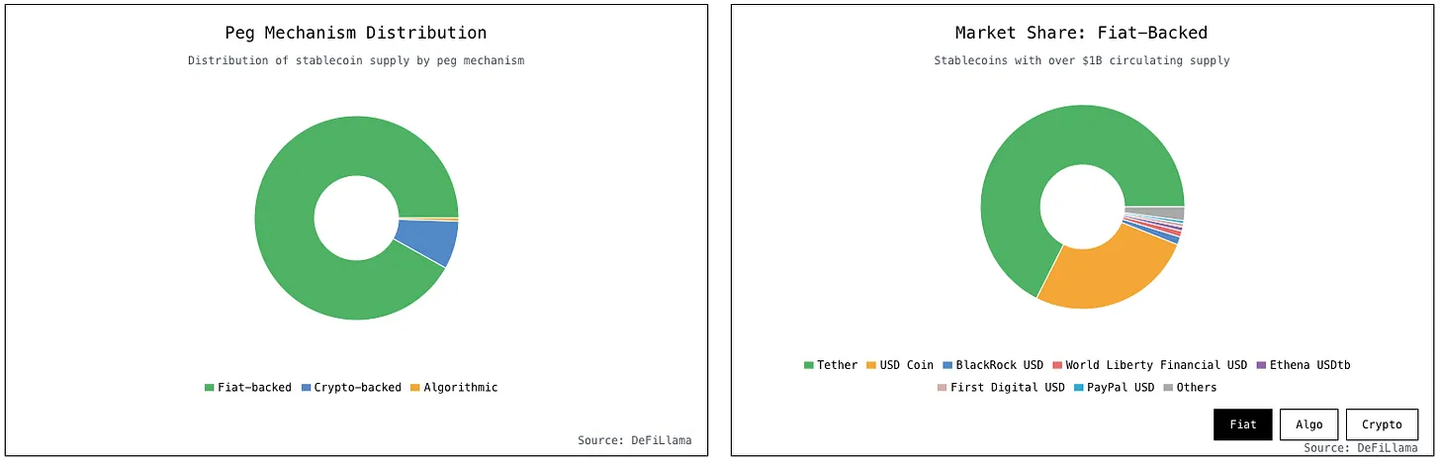

Today's stablecoin ecosystem includes several different types of stablecoins, primarily distinguished by their collateral support, degree of decentralization, and mechanisms for maintaining price pegs. Fiat-backed stablecoins dominate the market, accounting for over 92% of the total stablecoin market capitalization. Other categories include cryptocurrency-backed stablecoins, algorithmic stablecoins, and recently emerged strategy-backed stablecoins. Broadly, stablecoins are digital tokens that maintain a 1:1 value with a designated currency (usually the US dollar).

Fiat-Backed Stablecoins

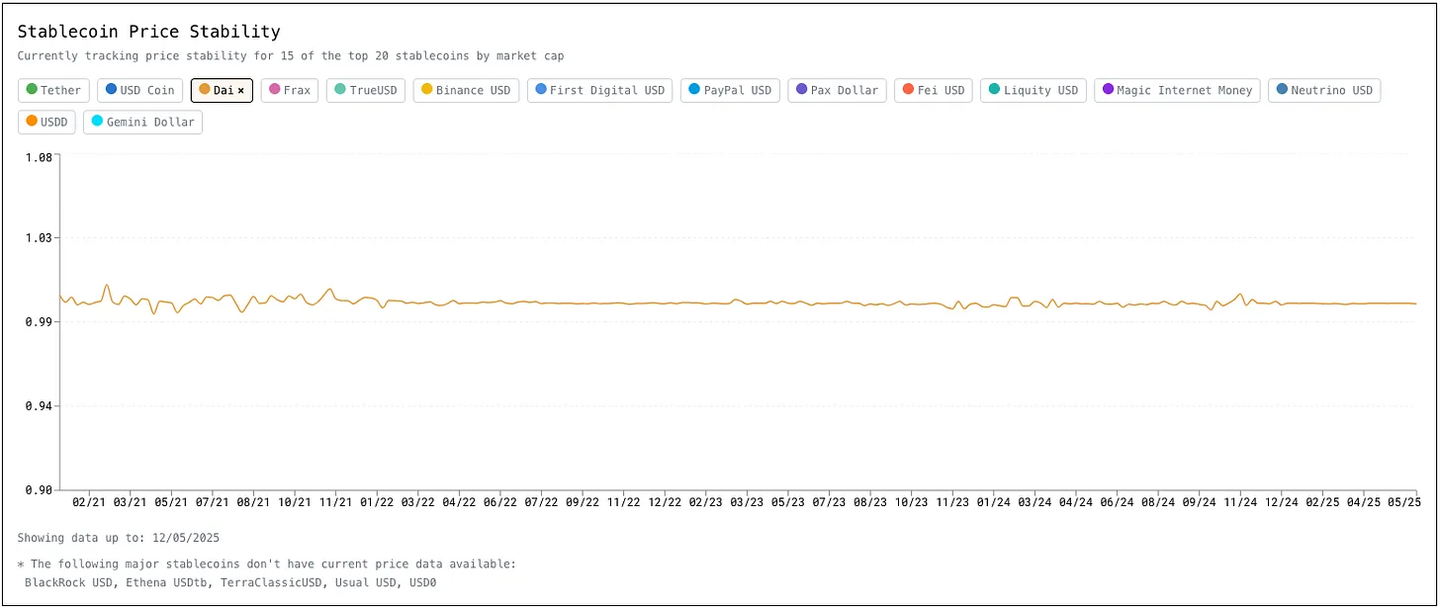

Fiat-backed stablecoins are similar to banknotes issued by note-issuing banks during the era of national banks in the United States (1865-1913): at that time, various banks issued notes redeemable for government greenbacks or gold and silver, with their value depending on the bank's creditworthiness and the note holder's ability to redeem them. Today's fiat-backed stablecoins promise 1:1 convertibility with a given fiat currency, but just as 19th-century note holders relied on secondary markets to redeem notes that could not be directly redeemed, modern users rely on platforms like Uniswap or centralized exchanges to exchange tokens for dollars at par (if direct redemption is not possible). This reliable convertibility—enforced through audited reserves and robust trading infrastructure—establishes the same level of confidence in fiat-backed stablecoins as the widely redeemable guarantees of banknotes over a century ago.

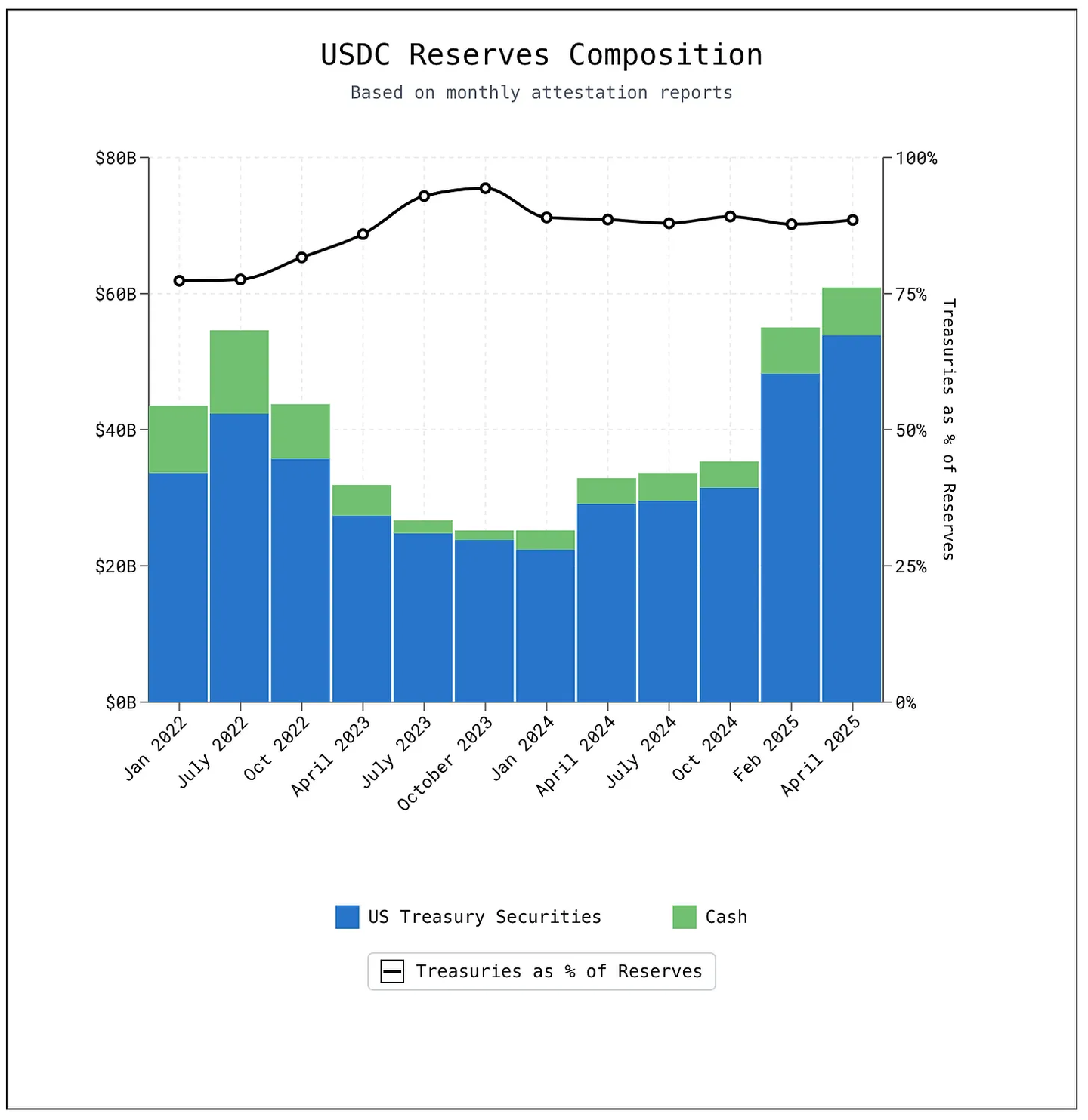

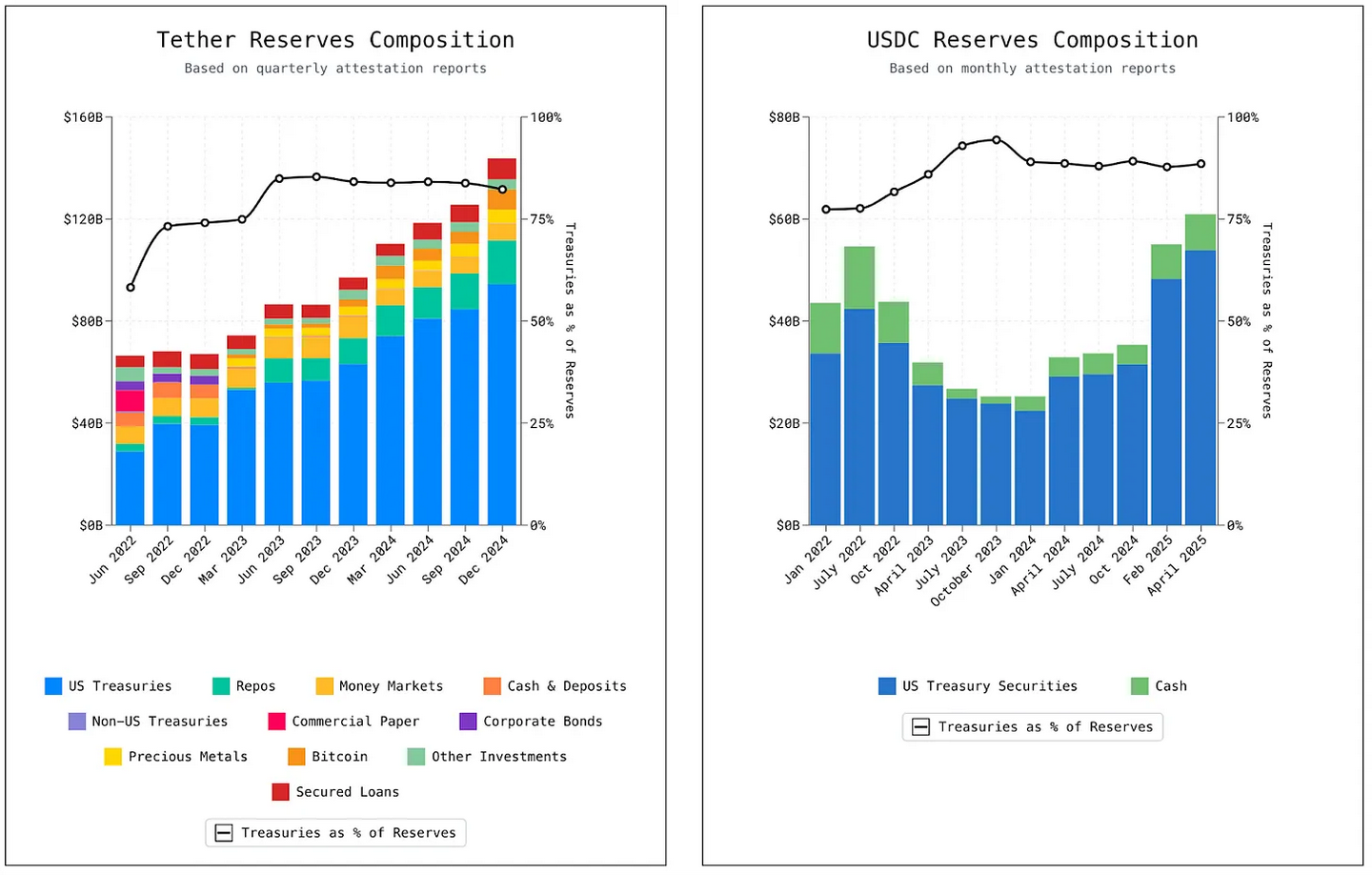

Fiat-backed stablecoins maintain their 1:1 peg by fully collateralizing each digital token with an equivalent amount of fiat currency held off-chain. For example, each USDC token is backed by a combination of $1 in cash and short-term US government debt. According to current reserve disclosures, each USDC is supported by approximately $0.885 in US Treasury securities and $0.115 in cash. The cash portion is held by regulated financial institutions, while the Treasury securities (including short-term securities and overnight repurchase agreements) are custodied by BNY Mellon and managed by BlackRock.

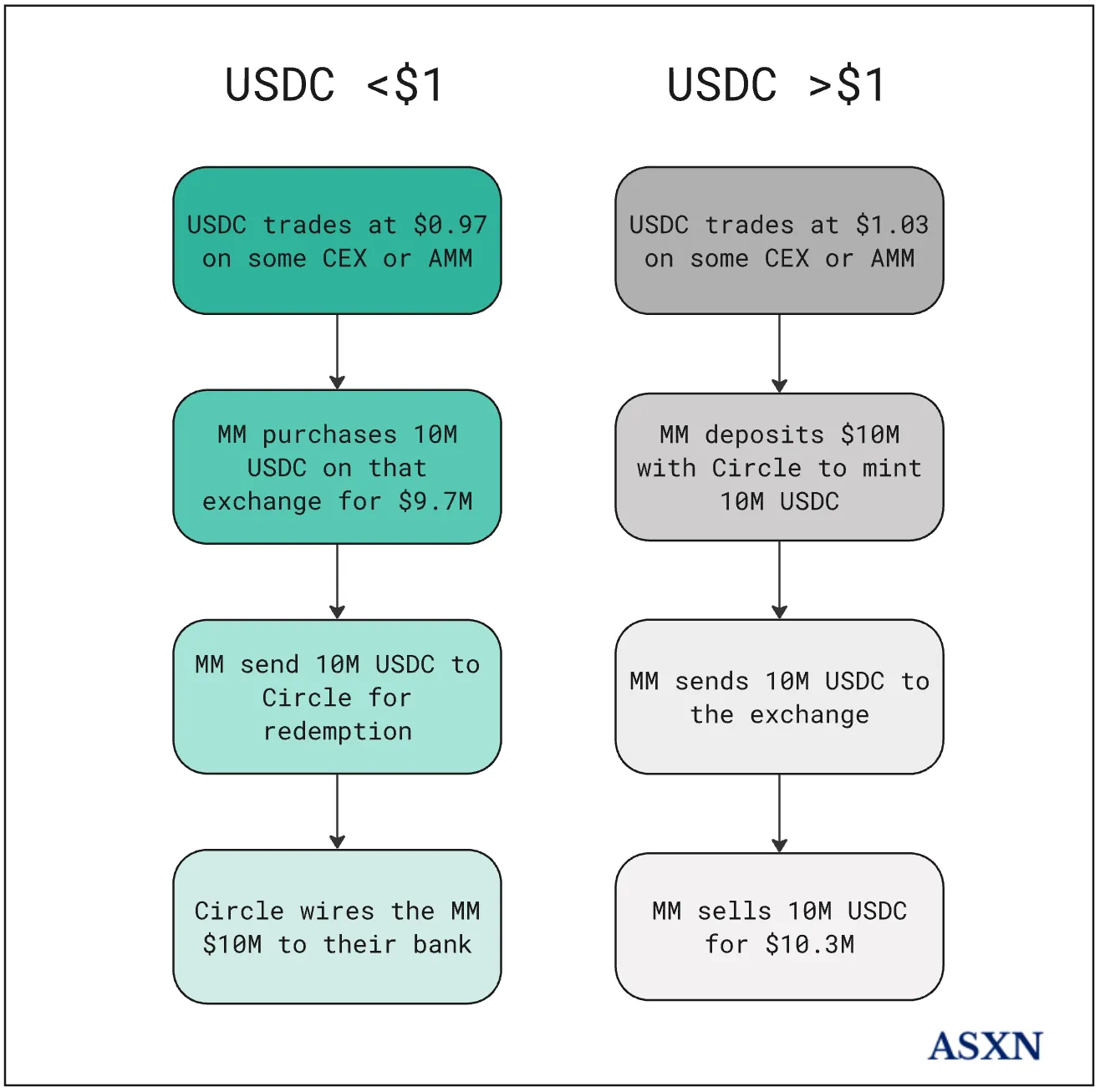

Typically, only specific entities can mint and redeem fiat-backed stablecoins. For example, Circle Mint clients (businesses and institutions with verified accounts) can redeem USDC directly at a 1:1 ratio through Circle. Redemption is initiated by sending USDC to the smart contract's burn function via the Circle Mint dashboard or API and submitting a redemption request. Clients can choose between two options: standard redemption, which provides near-real-time settlement with a daily limit of $15 million free of charge (with a 0.1% fee for amounts exceeding this limit); or basic redemption, which is completely fee-free but may take up to two business days for settlement. Once processed, Circle transfers the dollars to the client's associated bank account via ACH or wire transfer, depending on the chosen payment channel. This structure supports the 1:1 peg of USDC through arbitrage: when the secondary market deviates from par, traders can exploit the price difference, helping to restore price stability.

Stablecoin issuers primarily earn income by investing their reserves in interest-bearing US debt instruments. For example, Tether earned approximately $7 billion in 2024 from holding US Treasuries and repurchase agreements. Therefore, stablecoin issuers have an incentive to expand their supply, allowing them to invest more capital and capture yields close to the federal funds rate (currently around 4.25%).

Fiat-backed stablecoins bear strong similarities to money market funds (MMFs). After the Great Depression, the Glass-Steagall Act of 1933 aimed to prevent commercial banks from engaging in risky behaviors that could lead to bank failures, one provision of which, the "Q Regulation," limited the deposit rates banks could offer. As market interest rates exceeded the deposit rate ceiling, depositors missed out on earning opportunities. Bruce Bent and Henry Brown launched the first money market mutual fund in 1971, pooling cash from small investors to purchase short-term commercial paper and repurchase agreements. These funds were not subject to the Q Regulation interest rate ceilings (as they were managed by investment companies), allowing them to offer returns that banks could not match while maintaining a value of $1 per share.

The similarities between fiat-backed stablecoins and MMFs extend beyond structural design. Their regulatory and political debates are also highly similar. When MMFs first emerged, they faced criticisms similar to those currently directed at stablecoins, including concerns about financial stability, regulatory inadequacy, and systemic risk:

Financial stability risk: Money market funds (MMFs) do not have federal deposit insurance or central bank support, unlike regulated banks. This structural flaw makes them susceptible to liquidity crises and investor runs, as demonstrated during the 2008 financial crisis.

Regulatory arbitrage: MMFs effectively mimic core banking functions, such as providing stable dollar-denominated value storage, but are not subject to the stringent regulatory and capital frameworks that traditional deposit institutions face. This creates a parallel credit system with less regulation.

Erosion of monetary policy: The growth of MMFs may undermine the effectiveness of Federal Reserve policy tools. As assets shift from the regulated banking system to less-regulated instruments, the effectiveness of tools like reserve requirements diminishes, weakening the central bank's ability to control liquidity and credit conditions.

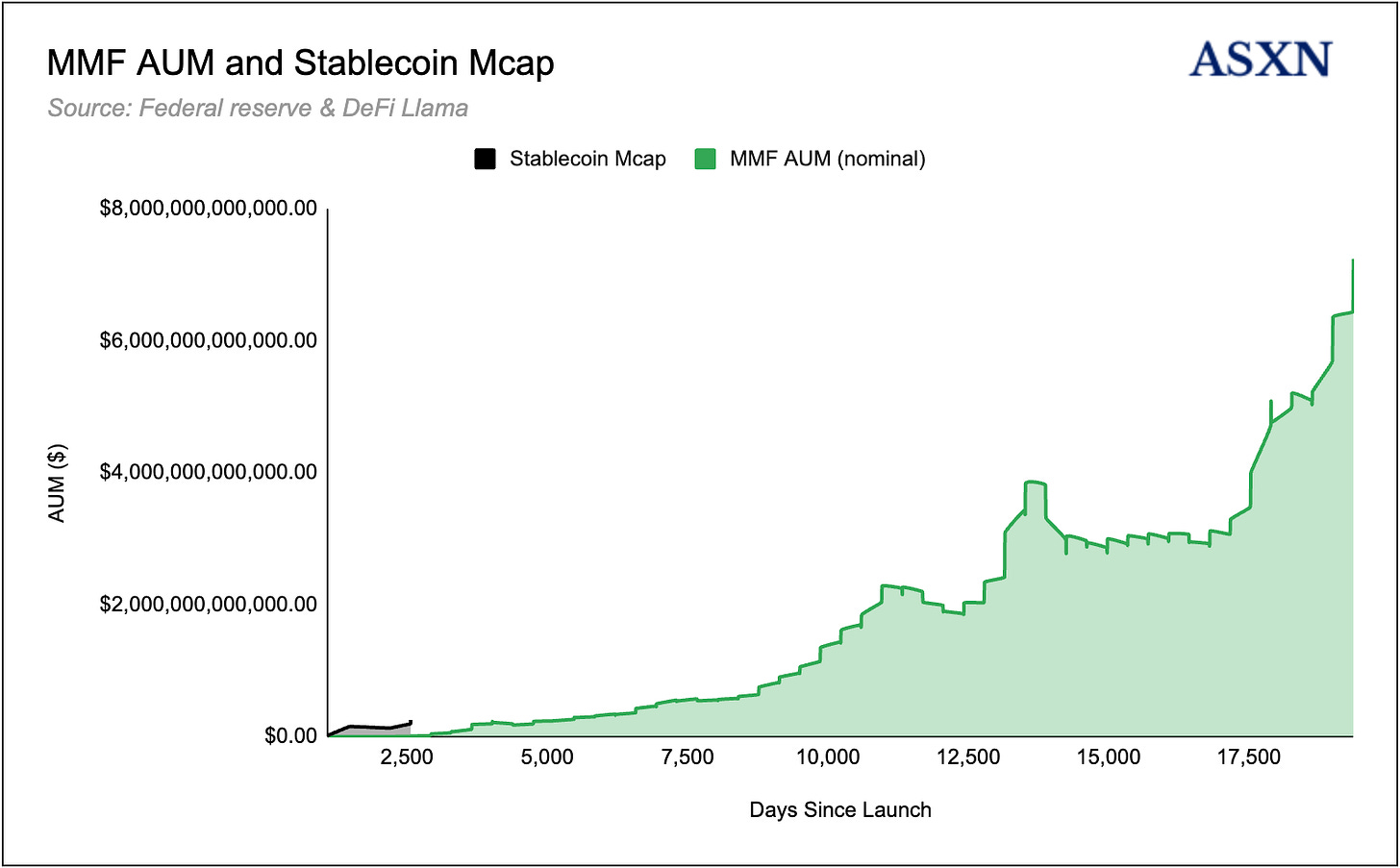

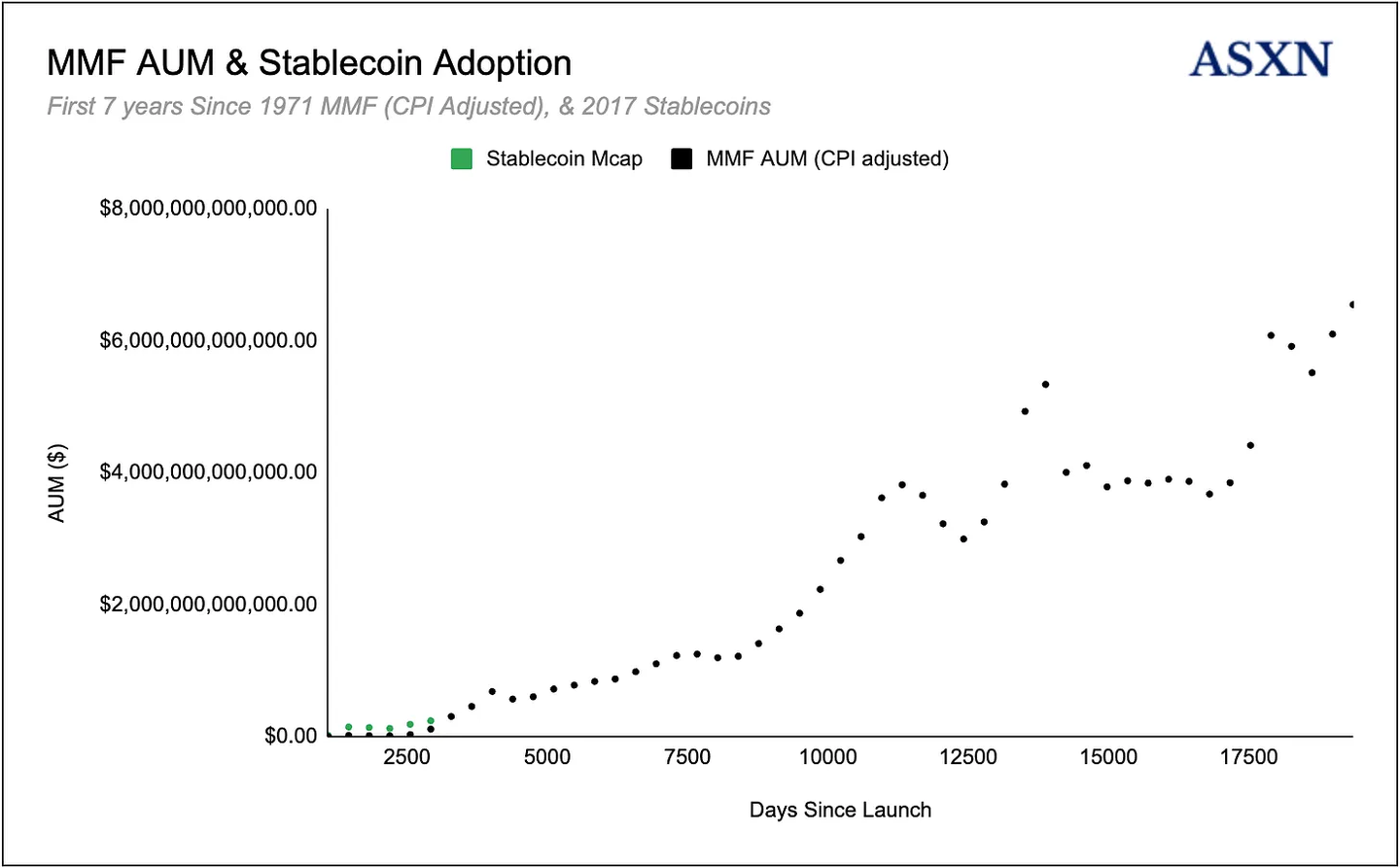

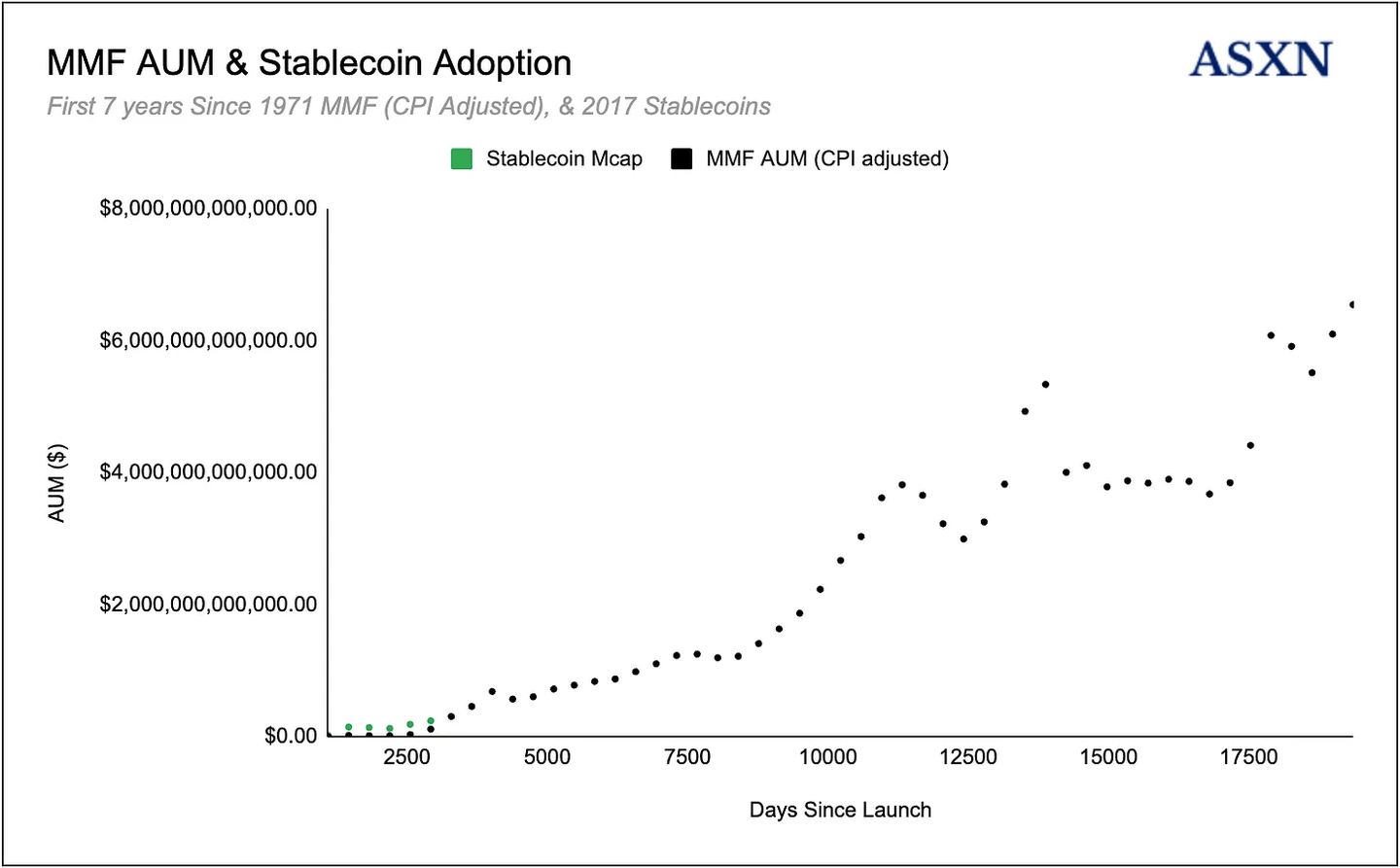

Although MMFs were introduced in the early 1970s, they only began to attract significant asset management scale after financial deregulation, legislative support, and technological advancements (such as electronic settlement systems and the internet) laid the groundwork. The Gramm-Leach-Bliley Act, passed in November 1999, was a pivotal moment, as it repealed key provisions of the 1933 Banking Act, removing long-standing legal barriers to the sponsorship and distribution of investment funds by commercial banks. This regulatory shift allowed banks to fully integrate MMFs into their product offerings, becoming part of the "financial supermarket" model. Banks quickly took advantage of these new powers, launching and distributing their own MMFs as part of core deposit accounts and yield products similar to Treasuries, attracting record amounts of funding from institutional and retail investors. By the end of 1998, before the Gramm-Leach-Bliley Act was passed, the US MMF industry had reached approximately $1.4 trillion in assets. Despite the turmoil caused by the 2008 financial crisis, MMFs continued to grow, reaching approximately $3.8 trillion in assets under management by the end of 2008. In many ways, their growth pattern is similar to the current trajectory of stablecoins, which also benefit from structural tailwinds and the evolution of financial infrastructure.

The assets under management of MMFs have now exceeded $7 trillion and continue to grow steadily. In contrast, seven years after the launch of MMFs, the assets under management were only $12.8 billion, which adjusts to about $62.8 billion in today's dollars. By this measure, stablecoins have outpaced MMFs by nearly four times at the same stage in their lifecycle. Observing the inflation-adjusted asset management scale trajectory of MMFs, the growth path of stablecoins is strikingly similar. Over the next 15,000 days (approximately 41 years), the actual assets under management of MMFs grew 55 times, driven by broader distribution, regulatory clarity, and technological advancements in financial infrastructure.

Cryptocurrency-Backed Stablecoins

Cryptocurrency-backed stablecoins are very similar to private banknotes from the era of free banking in the United States (1837-1862), which predates the National Banking Act of 1863-64 and the Federal Reserve Act of 1913. In the absence of federal regulation, states enacted "free banking" laws that allowed groups meeting minimum capital and collateral requirements (usually state bonds) to open banks. By 1860, over 8,000 different banknotes were in circulation, each trading at a discount or premium based on the issuer's creditworthiness, the cost of redeeming gold and silver, and local market conditions. Similar to today's cryptocurrency-backed stablecoin issuers, these free banks accepted gold and silver coins and (in some states) short-term government securities as reserves, then issued their own notes based on these reserves while extending loans under a fractional reserve system.

This mechanism of money creation still exists today, operating as follows:

A customer deposits $1,000 in a checking account, creating $1,000 in assets (reserves) and $1,000 in liabilities (deposits) on the bank's balance sheet.

Regulators require a 10% reserve ratio, for example, so for the $1,000 deposit, the bank holds $100 in reserves and can lend out $900.

Each time a loan is issued and redeposited in another bank, the process repeats, multiplying the original base money into a larger total of bank-created deposits. In fact, most broad money (M2) is created in this manner.

Cryptocurrency-backed stablecoins operate in a similar manner but mostly adopt an over-collateralized loan system due to their decentralized/KYC-free nature. Typically, users deposit collateral (e.g., BTC worth $1,000) into a protocol, which can mint up to $800 in stablecoins, reflecting an 80% loan-to-value (LTV) ratio. To prevent the devaluation of collateral from leading to system insolvency, the protocol enforces liquidation thresholds. If the value of the collateral falls below the specified LTV ratio, the system automatically liquidates the user's BTC to cover the outstanding debt, thereby preventing the accumulation of bad debt.

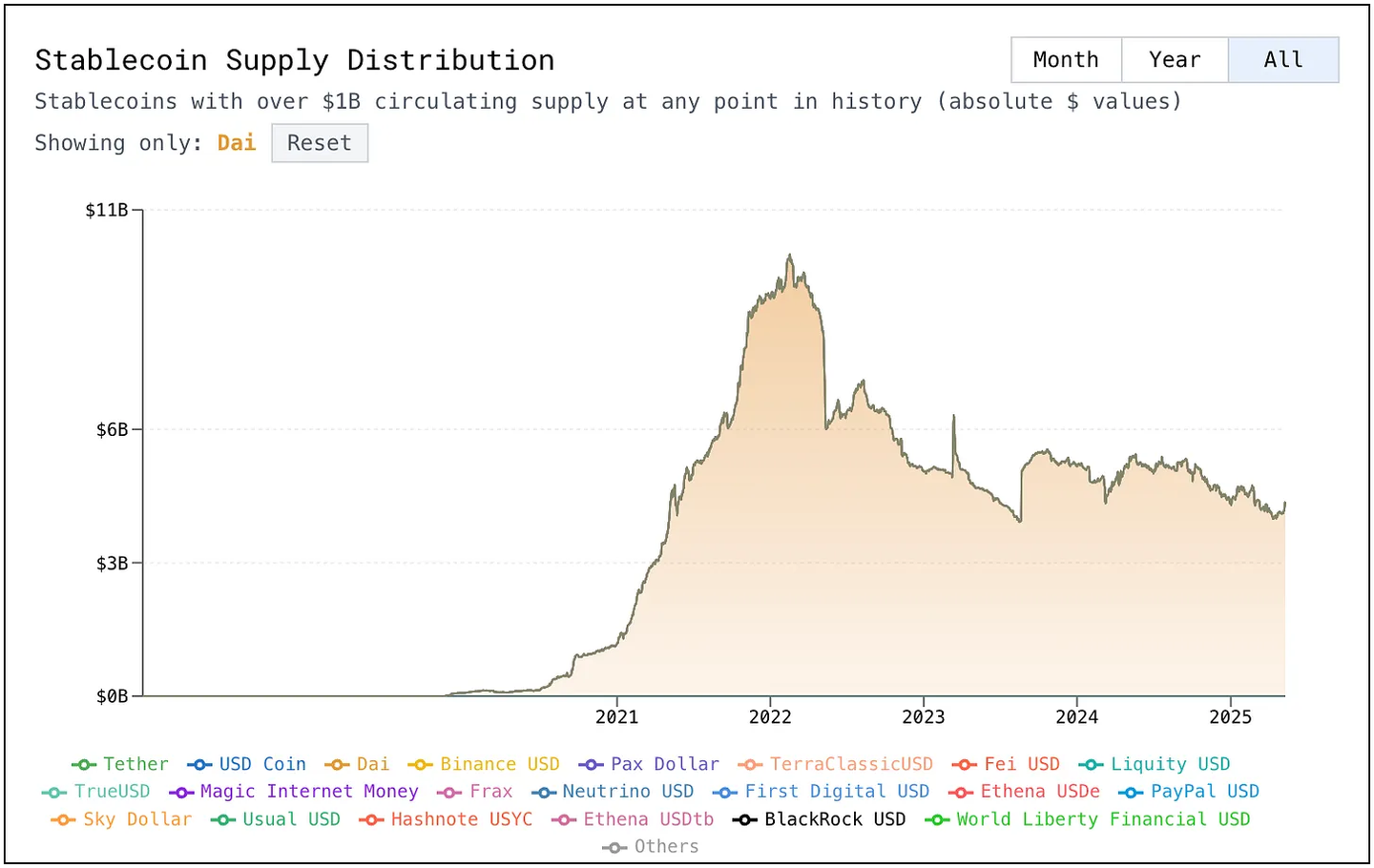

Maker/Sky Protocol has issued the largest decentralized cryptocurrency-backed stablecoins (DAI and USDS) in the space, continuing since the launch of the single-collateral DAI in 2017. Users mint DAI by depositing accepted collateral (such as ETH, wBTC, stETH, rETH, USDC, GUSD, and other crypto assets, as well as tokenized real-world assets including US Treasuries, real estate-backed tokens, and loans) into Vaults (formerly CDPs). Each type of collateral must meet a minimum collateralization ratio (for example, 150% for ETH), and if the value of the Vault falls below this threshold, it will face liquidation to maintain system solvency. The process is as follows:

A user deposits 1 wBTC worth $100,000 into a Maker Vault as collateral. The wBTC Vault type requires a 150% collateralization ratio (66.67% LTV).

The user can mint up to 66,666 DAI ($100,000 * 66.67%).

If the user mints 50,000 DAI, leaving a buffer above the minimum ratio, the Vault will hold 1 wBTC as collateral against the 50,000 DAI debt, resulting in a collateralization ratio of 200% or 50% LTV.

If the value of wBTC drops below $75,000, the Vault's collateralization ratio will fall below 150%, and the Vault will become under-collateralized.

At this point, the Vault will face liquidation: part of the wBTC will be auctioned/sold to cover the DAI debt, plus liquidation penalties.

If the user wishes to unlock the collateral at any time, they must repay 50,000 DAI (plus accumulated stability fees) before they can withdraw the wBTC.

This is very similar to how banks create new money through loans, but using liquid on-chain collateral, with each stablecoin resembling different banknotes from the free banking era, where holders must assess stablecoin risks based on the following non-exhaustive factors:

The quality, liquidity, and volatility of the on-chain loan-backed collateral.

The protocol's ability to secure under-collateralized loans.

The security of the smart contracts and mechanism design.

For example, during the market crash in March 2020, ETH dropped 53% in two days, exposing a significant weakness in the DAI model that relied solely on ETH collateral. The sharp price drop triggered massive liquidations, leading to congestion on the Ethereum network and delayed oracle price feedback. As a result, DAI lost its peg, trading between $0.96 and $1.13 on March 13. This instability highlighted the risks of relying solely on ETH as collateral, prompting the DAI community to propose adding USDC on March 16, 2020, to diversify risk and improve peg stability. Since 2021, DAI has maintained relative stability.

Algorithmic Stablecoins

Unlike fiat-backed and cryptocurrency-backed stablecoins, algorithmic stablecoins are not always backed by hard assets but use a combination of algorithms and smart contracts to maintain their peg. According to Kraken's analysis, we can further categorize algorithmic stablecoins into several models:

Seigniorage or Dual-Token Algorithmic Stablecoins

Seigniorage or dual-token algorithmic stablecoins use a dual-token system to maintain stable value. The first token is the stablecoin itself; the second is a bond or utility token, managed through incentive mechanisms and smart contracts to regulate supply and demand dynamics.

When the stablecoin trades above $1, indicating excess demand, the protocol mints new stablecoins and distributes them, typically to governance or bond token holders. This increase in supply aims to exert downward pressure on the price, guiding it back to the $1 target.

Conversely, if the stablecoin price falls below $1, the protocol contracts supply by allowing users to purchase bond tokens at a discount (e.g., $0.75). These bonds can be redeemed for $1 once the peg is restored. This mechanism incentivizes buyers and reduces the circulating supply of stablecoins, theoretically helping the price return to par.

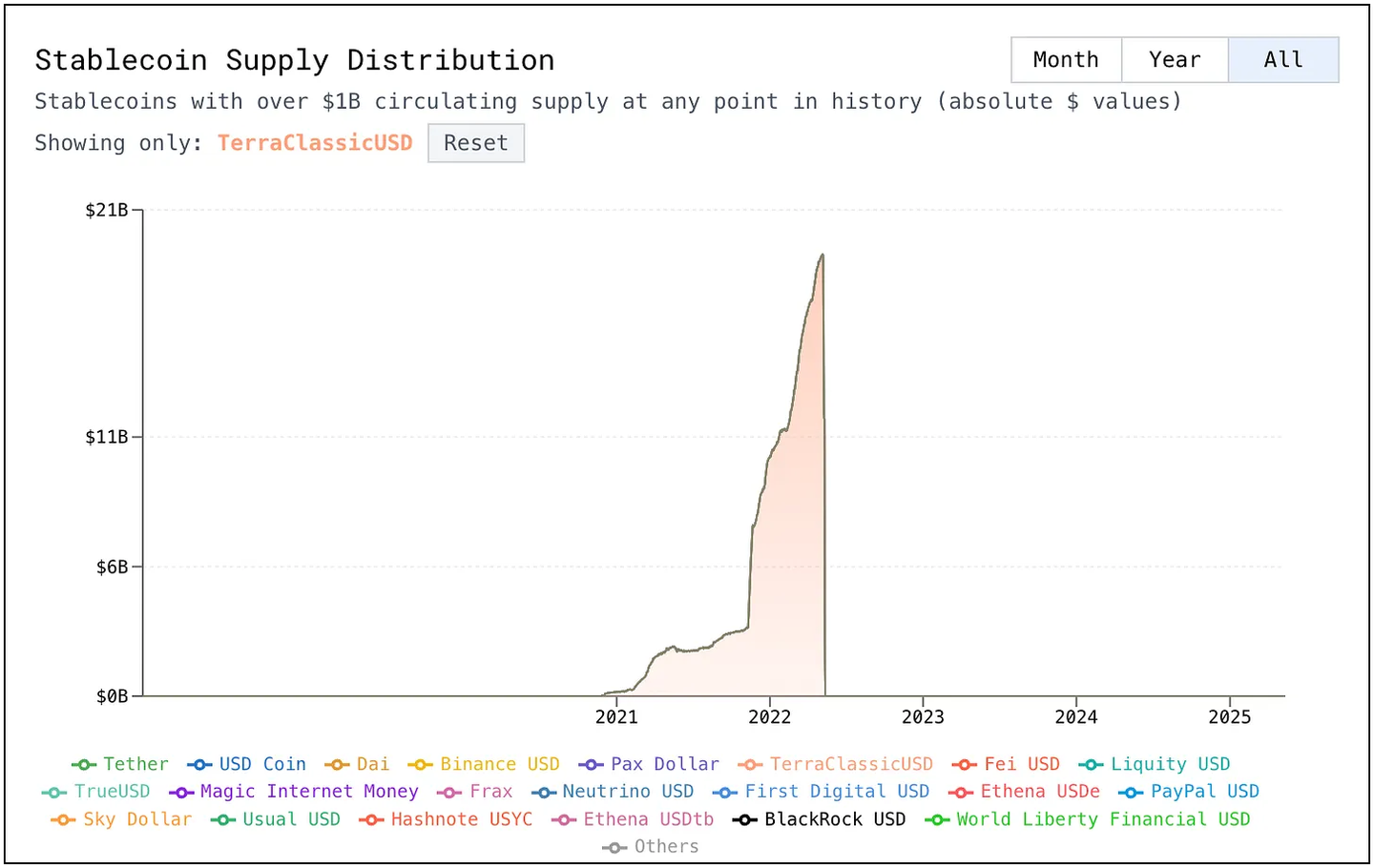

Terra Luna and the UST stablecoin followed this model, with LUNA tokens being burned/minted to restore UST value to $1 during price fluctuations. However, in early 2022, UST lost its $1 peg due to a loss of trust in the system and hyperinflation of LUNA supply, leading to the protocol's collapse. Within days, UST's market cap evaporated by about $18 billion, and the price fell below $0.10.

The other two categories of algorithmic stablecoins include:

Rebalancing Stablecoins: Rebalancing stablecoins maintain a $1 peg by directly adjusting the supply in users' wallets. When the price is above $1, the token balance increases proportionally; when the price is below $1, the balance decreases. This elastic supply model does not rely on minting or redemption mechanisms. Ampleforth (AMPL) is the most well-known example.

Partially Algorithmic Stablecoins: These stablecoins combine partial collateral support with algorithmic supply control. A portion is backed by assets like USDC or ETH, while the remainder relies on programmatic adjustments. The early FRAX adopted this model, maintaining a collateralization ratio below 100%, such as 90% backed by USDC.

Since the collapse of Terra Luna and UST, experiments with algorithmic stablecoins have sharply declined, with many projects (such as Frax Finance and Near Protocol) abandoning the model. This retreat is partly due to regulatory resistance: proposed legislation in the U.S. suggests a two-year ban on new algorithmic stablecoins, while the EU's Markets in Crypto-Assets Regulation (MiCAR) has outright banned such stablecoins, specifically targeting "endogenously collateralized" stablecoins. Although the appeal of decentralization and capital efficiency may drive some experiments to continue, we anticipate that algorithmic models will remain niche. The risks of de-pegging and an increasingly stringent regulatory environment may limit their role in the future growth of the stablecoin market.

Strategy-Backed Stablecoins

A new category of "stablecoins" has recently emerged—these tokens maintain a $1 valuation while embedding yield-generating investment strategies. These tools are more akin to dollar-denominated open-ended hedge fund shares than traditional stablecoins. This concept was proposed in March 2023 by BitMEX founder and perpetual futures contract pioneer Arthur Hayes, who introduced a hypothetical stablecoin, NUSD, structured as: 1 NUSD = 1 dollar of Bitcoin + shorting 1 BTC/USD inverse perpetual swap. Inspired by this, Guy Yang founded Ethena, whose strategy-backed stablecoin USDe has become a leading project in this emerging category.

Each USDe is minted by depositing an equivalent amount of dollars in crypto assets (such as ETH, BTC, or liquid staking tokens) while shorting an equivalent notional value through perpetual swaps or futures. This creates a "long + short" neutral basis trade, where the price fluctuations of the underlying asset are offset by the short position, keeping the net portfolio value around $1. This structure allows USDe to maintain a 1:1 full collateralization without the typical over-collateralization buffer seen in traditional cryptocurrency-backed stablecoins.

USDe also has yield-generating characteristics. The short position earns financing payments when the perpetual swap financing rate is positive. In this sense, Ethena effectively provides/funds leverage to the market, as the demand for leverage in the crypto market tends to be cyclical but high. Users can stake USDe to receive sUSDe (yield-bearing tokens) to capture this yield, with sUSDe functioning similarly to a savings tool, accumulating returns from financing rates, liquid staking rewards, and other protocol revenues, while the underlying USDe remains an interest-free stablecoin if idle. In 2024, the average annualized yield for sUSDe was around 19%, reflecting strong demand in the crypto market for leverage and staking rewards.

The launch of Ethena and USDe has sparked many other strategy-backed stablecoins, such as Resolv USD and the recent Neutrl, which tokenizes OTC arbitrage trades (long discounted OTC rounds, short perpetuals).

We refer to these strategy-backed stablecoins as dollar products or synthetic dollar products, but it is important to note that their risk characteristics differ from what many consider traditional stablecoins (i.e., those based on Treasuries or short-term government debt instruments).

Alright, I will continue the translation from the previous document you provided, starting from the "The Case for Stablecoins" section, maintaining the same style as before, ensuring accurate conveyance of the original content while keeping the language fluent and professional. If you have specific requests (such as translating to a certain section, providing a summary, or adjusting the depth of translation), please feel free to let me know. Here is the translation of the "The Case for Stablecoins" section, and I will continue to translate the subsequent content in order.

Use Cases for Stablecoins

Store of Value

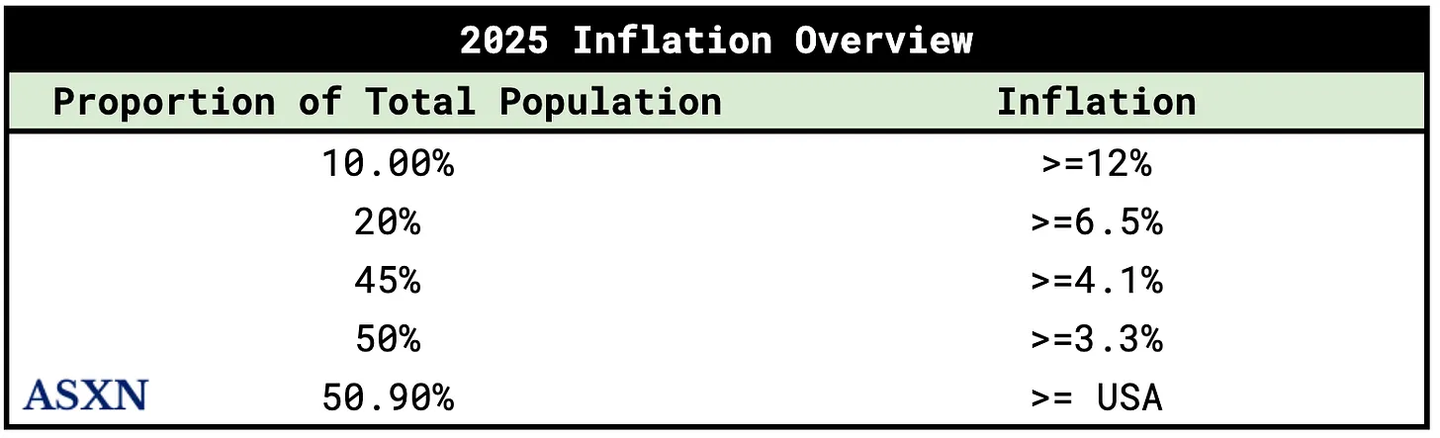

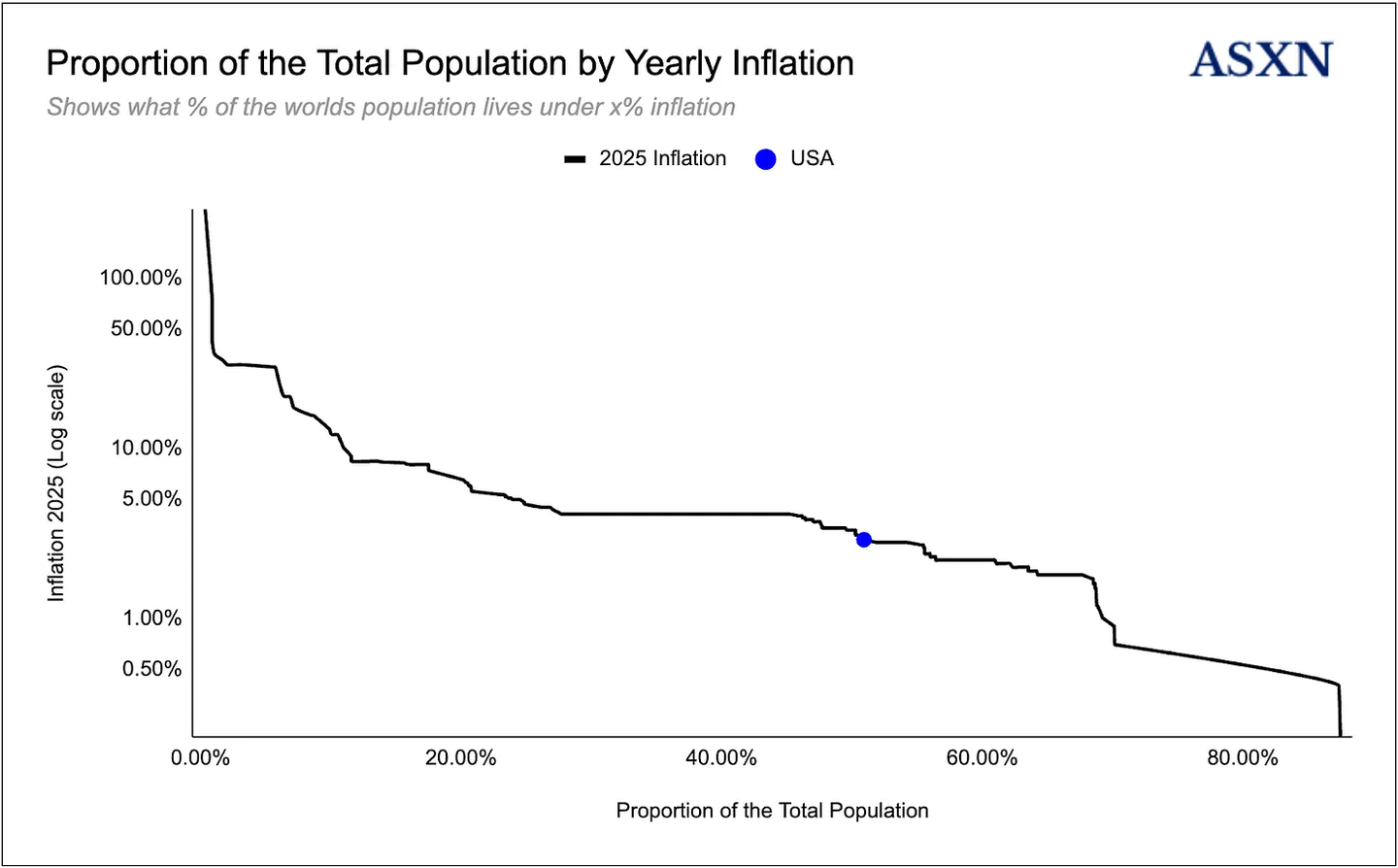

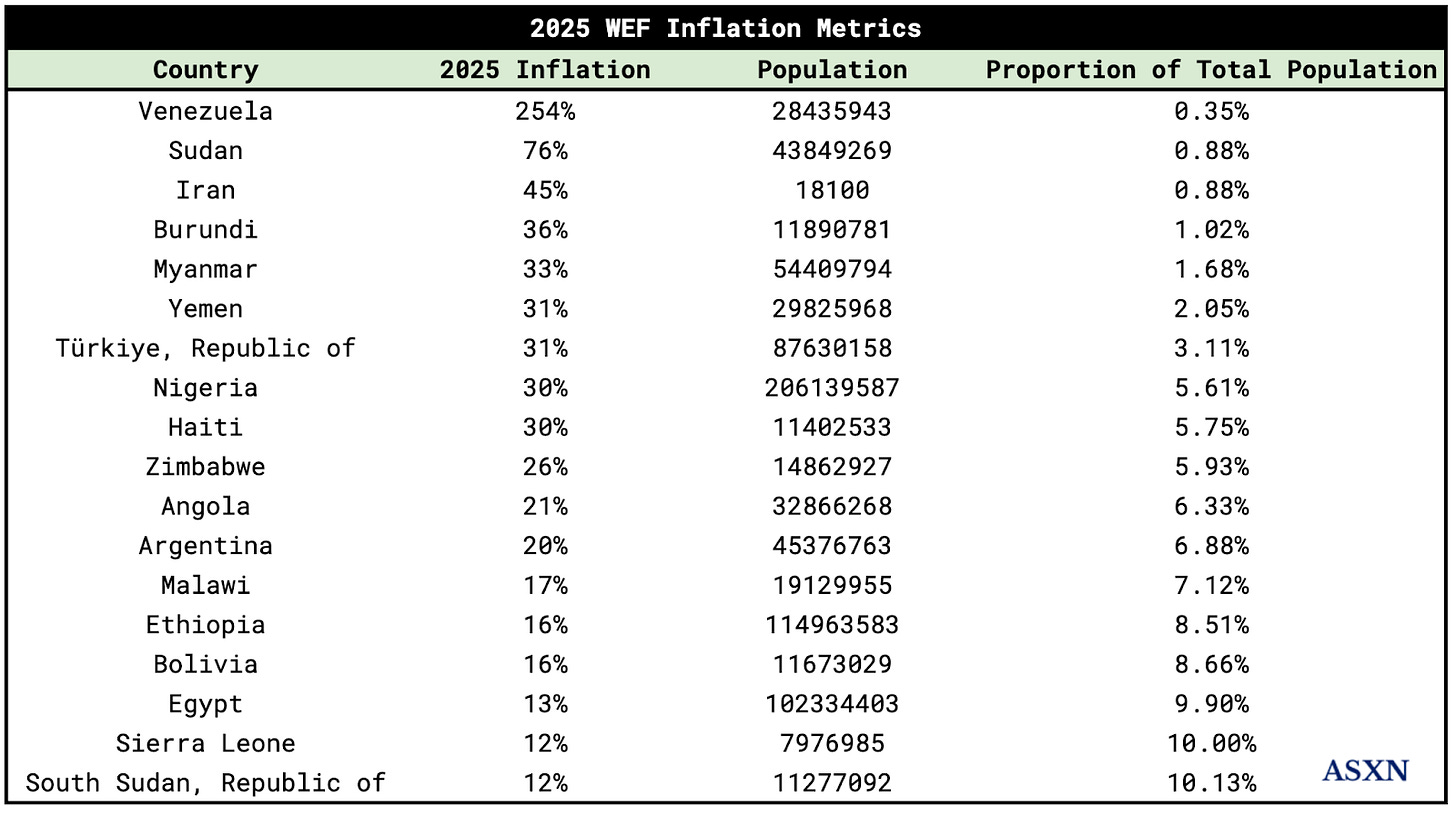

While most investors, especially Bitcoin investors, recognize that the dollar is slowly losing purchasing power due to ongoing inflation and currency devaluation, as Ray Dalio aptly described, "the dollar is still the least dirty shirt in the laundry basket." In fact, over 20% of the global population lives under regimes with inflation rates of 6.5% or higher, and over 51% of the population faces worse inflation than the U.S. (2025 data). In countries suffering from hyperinflation, currency devaluation, or strict capital controls, citizens and businesses are initiating a grassroots financial transformation: increasingly turning to dollar-pegged stablecoins as a means of storing value. In economies such as Argentina, Turkey, Lebanon, Venezuela, and Nigeria, people choose to hold digital dollars (like USDT, USDC, or DAI) instead of rapidly depreciating local currencies. In these environments, stablecoins serve more as digital savings accounts rather than payment channels, providing a more stable purchasing power protection solution.

The effectiveness of currency as a store of value depends on several core economic fundamentals. When these fundamentals deteriorate, confidence in the currency gradually weakens. Key drivers include:

Inflation: Low and stable inflation is crucial for maintaining the value of currency. High inflation can quickly erode purchasing power.

Monetary Policy: If the market perceives a lack of discipline or independence from the central bank—such as financing deficits through money printing or implementing unorthodox policies—the value of the currency may plummet. Turkey is an example: despite an average inflation rate exceeding 40%, the central bank lowered interest rates in 2022-2023, undermining credibility and leading to a 300% decline in the value of the lira from 2020 to 2023.

Fiscal Discipline: Unsustainable fiscal policies can lead to currency devaluation. If a government runs deficits for an extended period and accumulates debt that investors doubt it can repay, it may resort to monetizing the debt (i.e., printing money). This expands the money supply, triggers inflation, and damages the currency's value. For instance, Lebanon's government debt default and deficit monetization in the late 2010s led to a currency collapse and triple-digit inflation.

Money Supply: The rate of money supply expansion relative to actual economic growth affects long-term value. If the money supply grows far faster than economic growth (common when central banks fund government spending or bail out banks), it typically leads to inflation and devaluation. For example, during hyperinflation in Venezuela, the money supply surged, leading to the collapse of the bolívar as a store of value.

Capital Controls and Convertibility: The attractiveness of currency as a store of value also depends on the ability to freely convert or transfer value. When governments implement capital controls—restricting access to foreign exchange, cross-border transfers, or fixing unrealistic exchange rates—the currency becomes "trapped," often overvalued domestically. This undermines confidence, as people worry about their inability to exit to stable assets when needed.

Political and Institutional Stability: Broader political risk factors also play a role. Regime instability, threats of expropriation or bank freezes, and a lack of rule of law can diminish confidence in local currency and banks. Lebanon's banking crisis is a typical example: from 2019 to 2020, banks implemented informal capital controls and froze deposits, destroying trust in holding wealth in local institutions.

For many countries and the majority of the global population, the dollar has a relative advantage in the following key dimensions: lower inflation, fewer capital controls, and greater political stability. Additionally, the dollar provides access to the world's most liquid financial markets, supported by a (mostly) disciplined Federal Reserve that sets clear targets around core economic indicators.

We can gain deeper insights into how citizens in emerging economies use stablecoins to protect their wealth through some case studies:

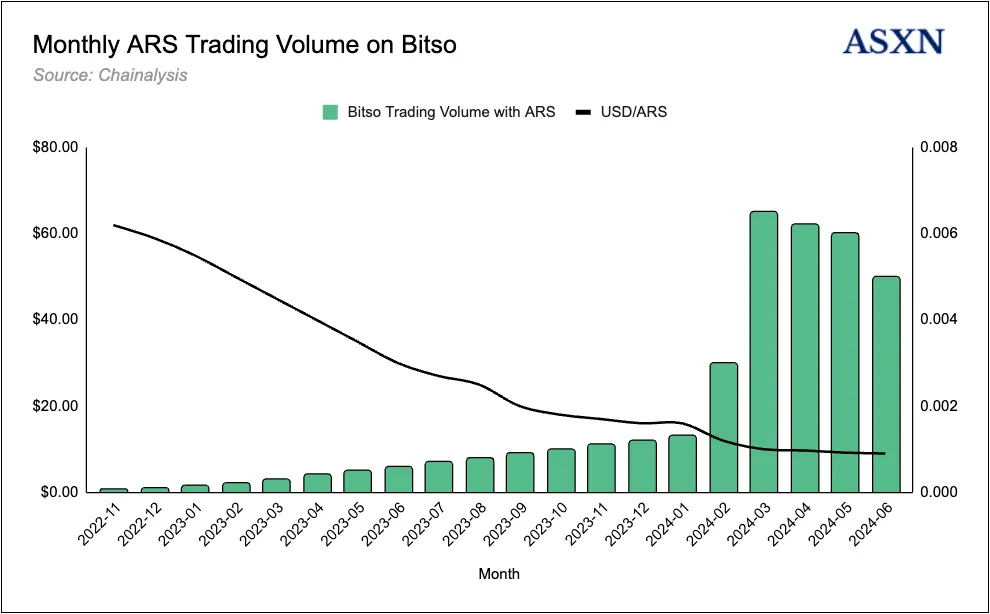

Argentina

Argentina is a typical case of capital fleeing to stable value through cryptocurrency. Decades of chronic inflation and repeated currency crises have eroded public trust in the peso. While the current inflation rate is around 20%, Argentina experienced inflation rates as high as 143% in 2023, pushing about 40% of Argentinians into poverty. In December 2023, newly elected President Javier Milei devalued the peso by 50%, calling it "shock therapy."

"To cope with this economic crisis, some Argentinians have turned to the black market for foreign currency, most commonly the dollar. This 'blue dollar' is traded at parallel, informal exchange rates, typically purchased through secret exchange houses known as 'cuevas' across the country. Others have explored dollar-pegged stablecoins, as reflected in our data.

We analyzed the monthly stablecoin trading volume against the Argentine peso (ARS) on Bitso, a leading trading platform in Latin America, and found that the persistent decline in the peso's value consistently triggered spikes in stablecoin trading. For example, when the ARS fell below $0.004 in July 2023, the following month's stablecoin trading value surged to over $1 million. Similarly, when the ARS dropped below $0.002 in December 2023 (when President Milei announced the devaluation), the next month's stablecoin trading value exceeded $10 million." — Chainalysis

USDT is widely used in certain circles for everyday transactions, effectively becoming a parallel currency. Even the Argentine tax authorities have taken notice—Mendoza province began accepting stablecoin payments for taxes in 2022, legitimizing their actual role as currency. For ordinary Argentinians, stablecoins are a lifeline: a way to hold a "dollar" that won't rapidly devalue without special permissions.

Lebanon

Lebanon's financial collapse that began in 2019 illustrates why ordinary citizens turn to stablecoins when traditional financial systems fail. The Lebanese pound (LBP) lost over 98% of its value during the crisis, personal savings were destroyed, and by 2023, inflation exceeded 200%. Meanwhile, banks froze dollar accounts and imposed arbitrary withdrawal limits, effectively implementing capital controls that cut off depositors' access to their funds. In this financial paralysis, many Lebanese turned to crypto assets, particularly stablecoins, as a practical alternative to the dollar.

Tether USDT rapidly gained popularity in Lebanon, becoming the actual quoting currency for local currency exchangers and traders, forming a crypto-based parallel exchange market. One report described USDT as "the preferred cryptocurrency for bypassing bank restrictions." Its peer-to-peer transferability allows users to circumvent the frozen banking system and the official currency peg, trading USDT for pounds or other cryptocurrencies through Telegram groups or local brokers. Once holding USDT, users possess a stable store of value insulated from hyperinflation, enabling online purchases or cross-border transfers—functions that are typically blocked under capital controls.

Lebanon also highlights the trust advantage of stablecoins, especially when paired with self-custody wallets. Domestic banks are widely viewed as bankrupt and untrustworthy, and storing funds in personal crypto wallets provides users with a sense of control and security. Many Lebanese view stablecoins as digital savings accounts, holding USDT or USDC for weeks or months, only converting to LBP when needed for consumption.

Summary of Stablecoins as a Store of Value

For brevity, we have only listed a few case studies, but Chainalysis provides a good overview of similar trends in Latin America. Overall, dollar-pegged stablecoins (like USDT, USDC, DAI) have strong appeal in high-inflation, capital-restricted economies. The following factors make them an attractive means of storing value:

Purchasing Power Protection: For people in Argentina or Nigeria, shifting from currencies that lose 20-100% of their value annually to dollar-pegged stablecoins can immediately achieve dollarization, halting the erosion of purchasing power. Even with U.S. inflation around 3-4%, the comparison remains significant. Stablecoins inherit the relative stability and credibility of the dollar, making them an attractive alternative in countries where trust in local currency has collapsed.

Self-Custody: Users self-custody their crypto keys, meaning their assets are not subject to the solvency of local banks or government freeze orders. This is a powerful feature in places where banks may be bailed out or withdrawals arbitrarily restricted (like Lebanon, Nigeria). With stablecoins, users can store $100 or $100,000 in a secure hardware wallet or even a paper backup, without the risk of local authorities devaluing or seizing their funds, unless the global crypto network is compromised.

Liquidity: Holding stablecoins is not just for passive savings; they also have high liquidity in transactions. This makes them functional in daily life. Traditional ways of exposure to dollars (like offshore accounts or physical cash) cannot match this liquidity.

Censorship Resistance: Traditional dollar channels (banks or remittance services) are susceptible to monitoring, censorship, or political interference. Stablecoins, especially when traded on peer-to-peer or decentralized platforms, can offer greater privacy and censorship resistance.

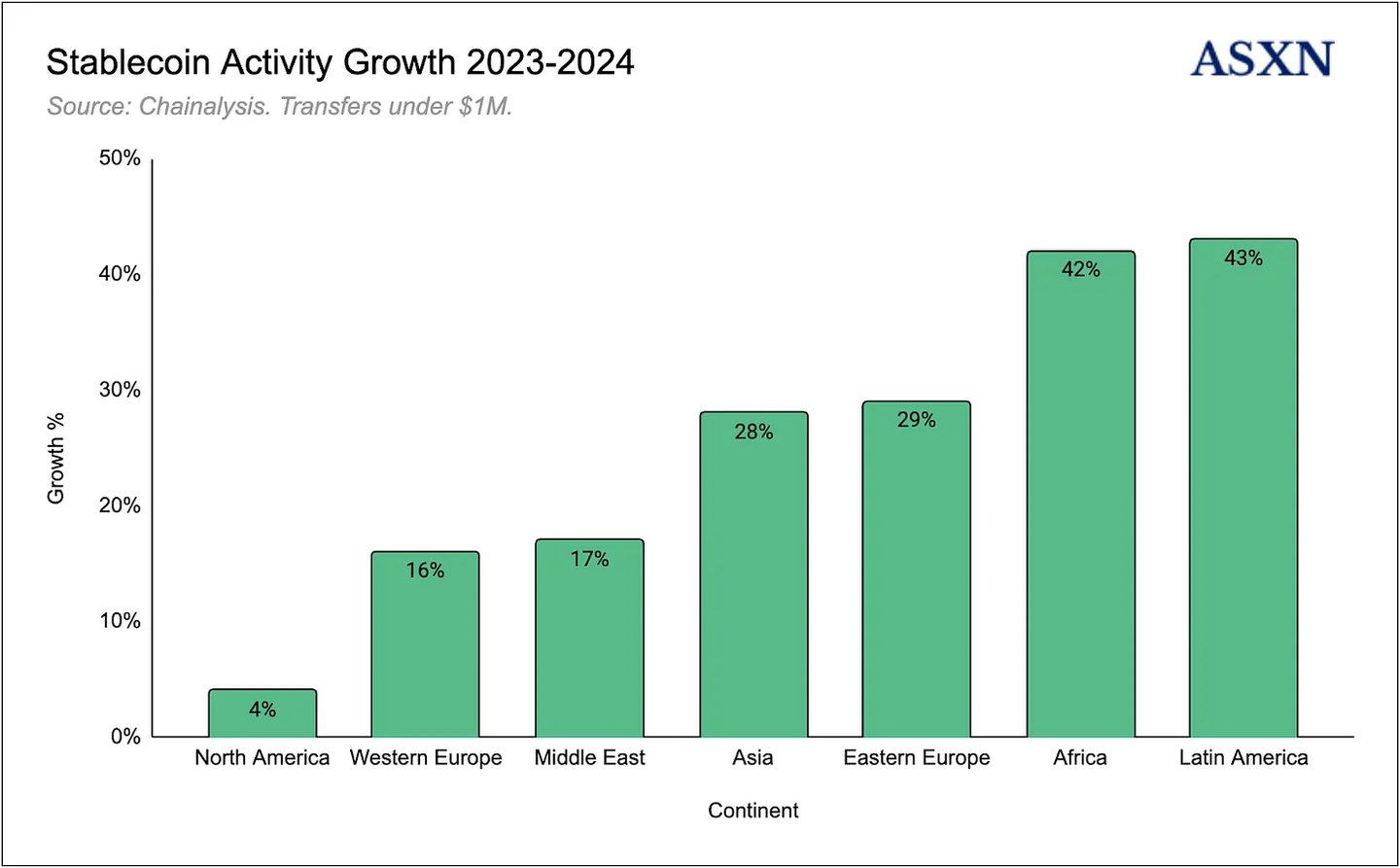

For these reasons, stablecoin activity is rapidly growing in Latin American and African countries. According to Chainalysis's de-anonymization software, transfers under $1 million have increased by over 40%.

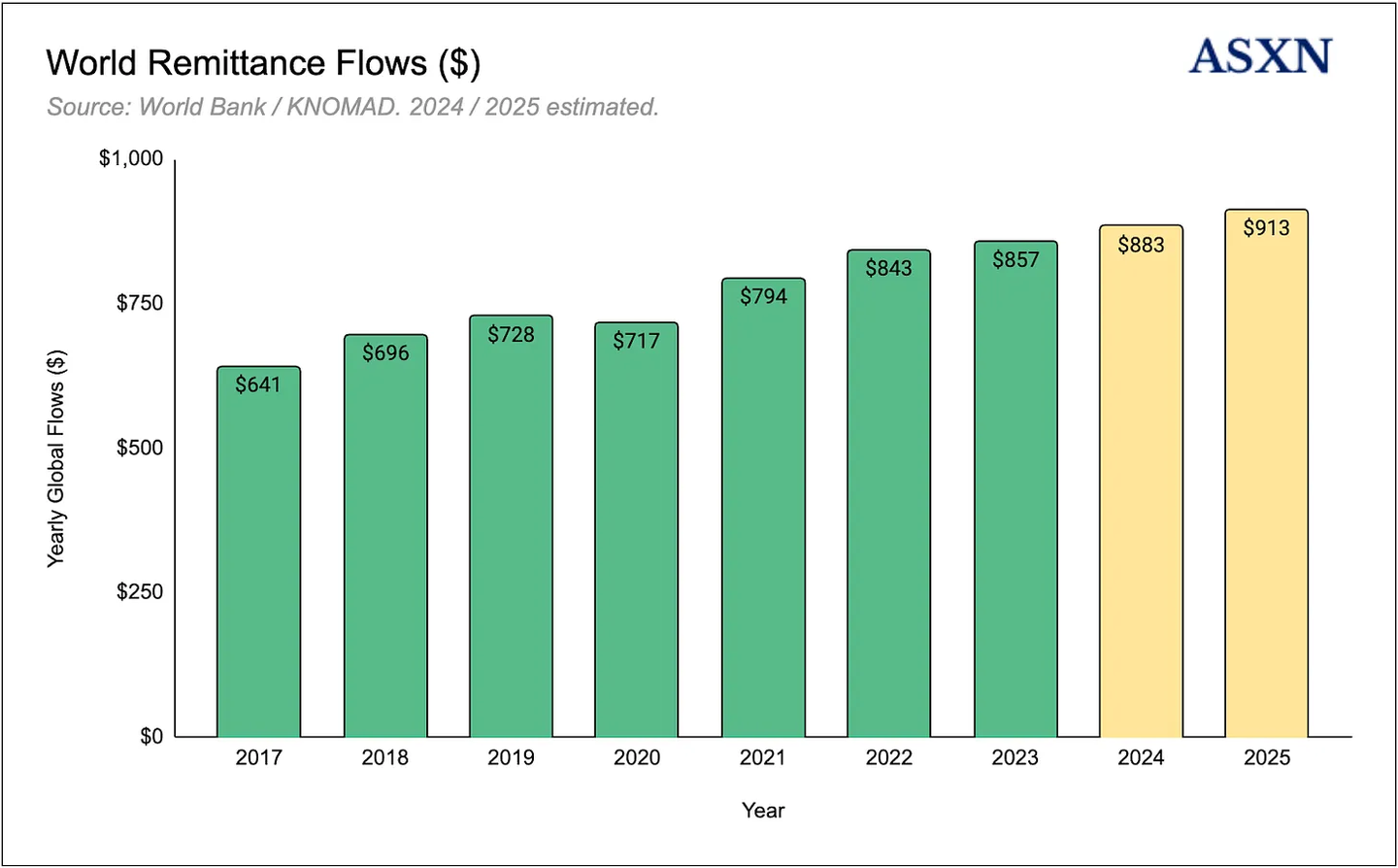

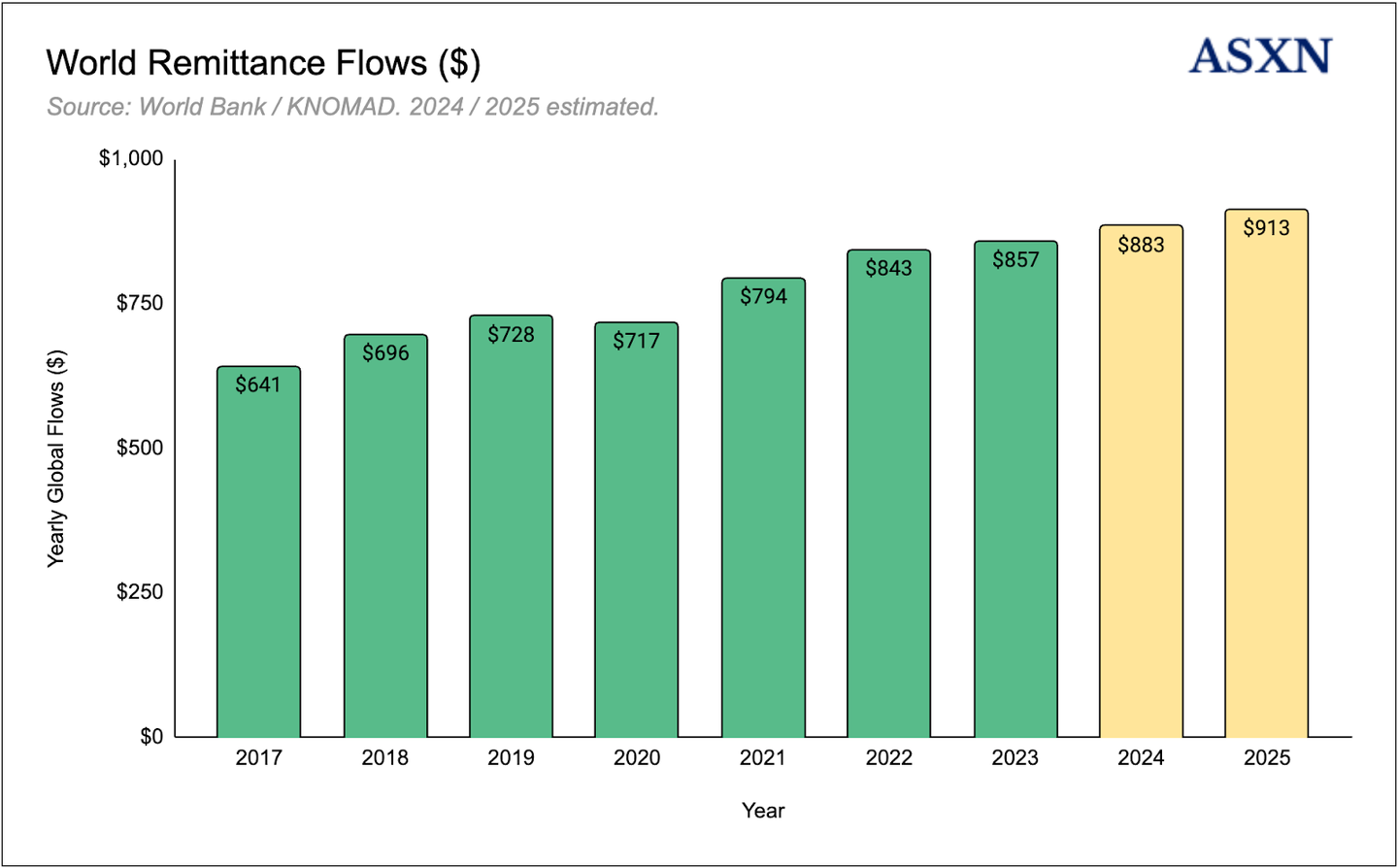

Remittances

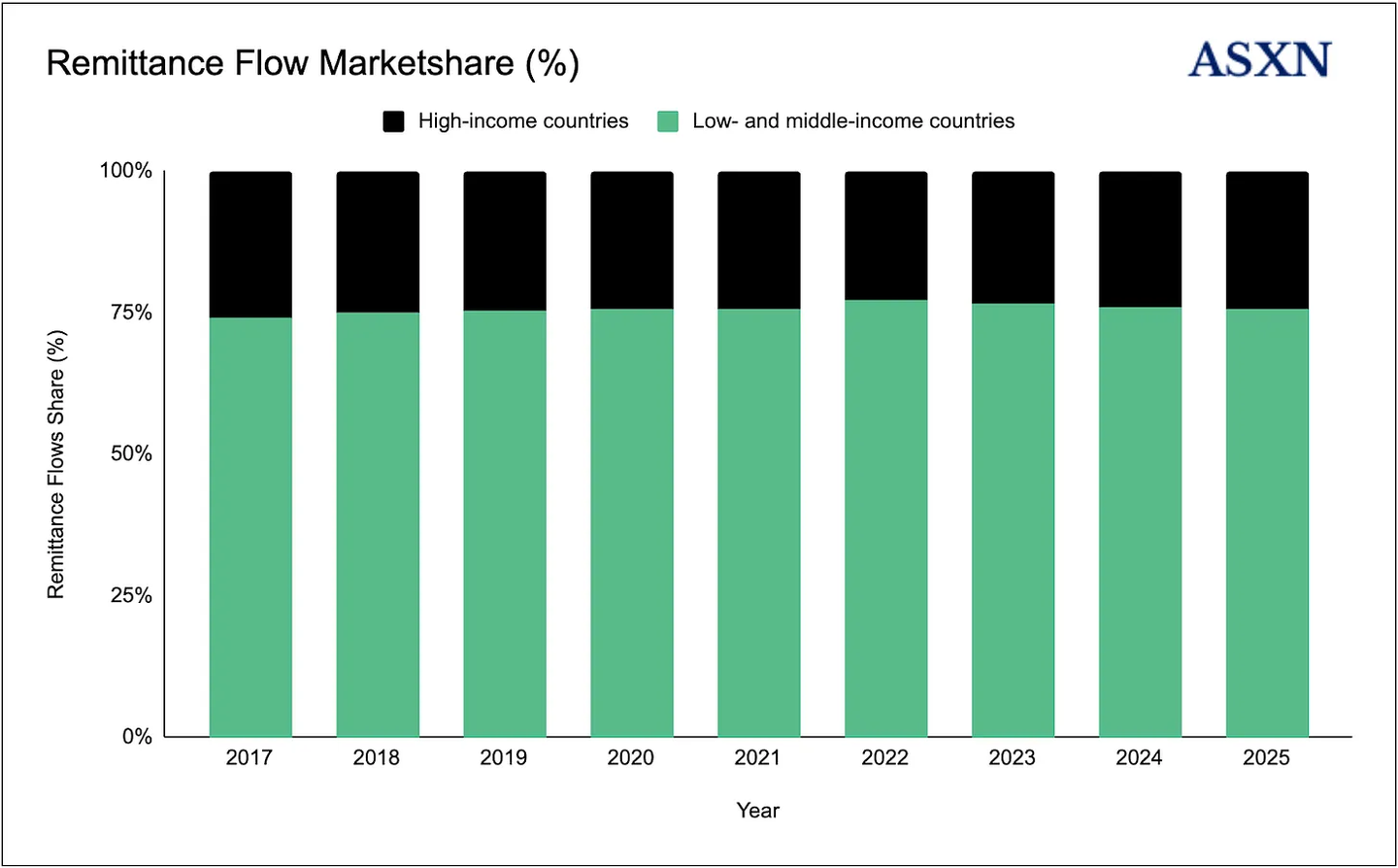

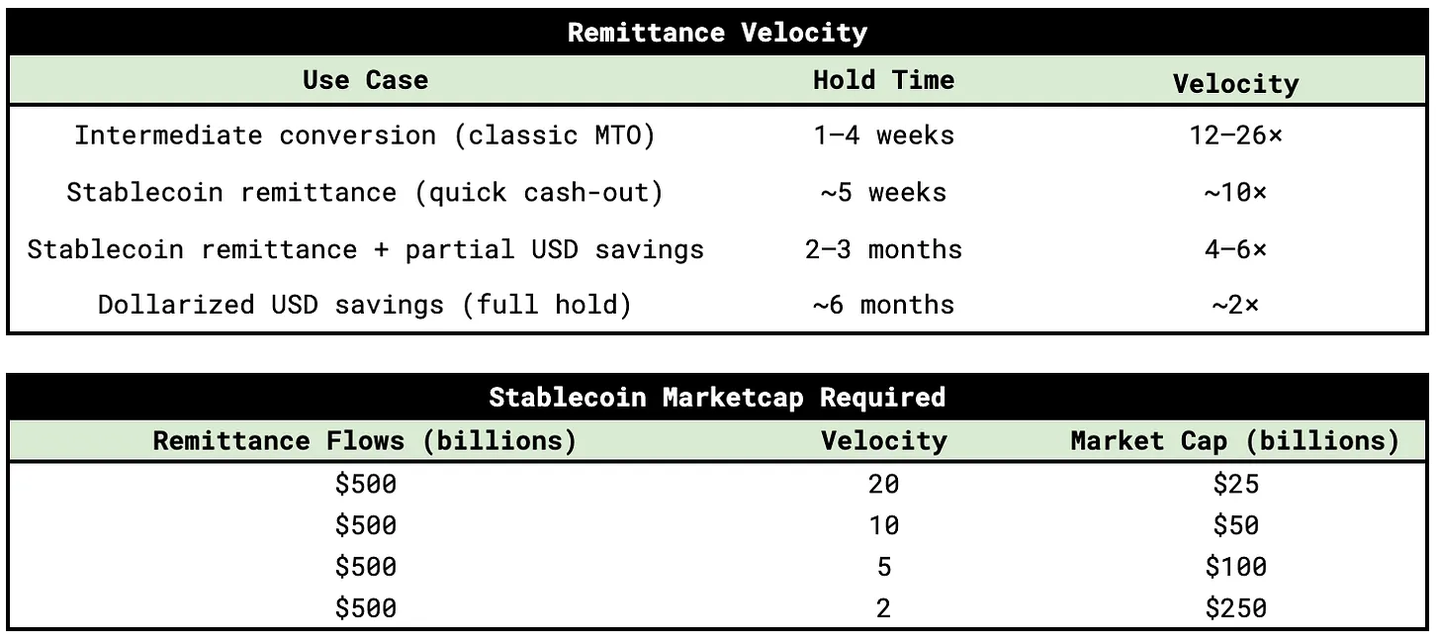

Remittances are one of the primary use cases for stablecoins. Every year, tens of millions of workers send part of their wages back home, supporting over 200 million beneficiaries globally. In 2024, global remittance flows reached approximately $905 billion, equivalent to the GDP of a medium-developed economy. This is expected to continue growing in 2025. About 76% (approximately $685 billion) flows to low- and middle-income countries (LMICs), where remittances often serve as a lifeline for household economies, covering basic needs such as food, education, and healthcare.

Remittances are highly concentrated in LMICs, which often face the value storage challenges we mentioned earlier, including weak local currencies, capital controls, and political instability. This makes cross-border inflows particularly susceptible to value erosion—providing a strong rationale for the adoption of stablecoins as a more resilient and efficient alternative.

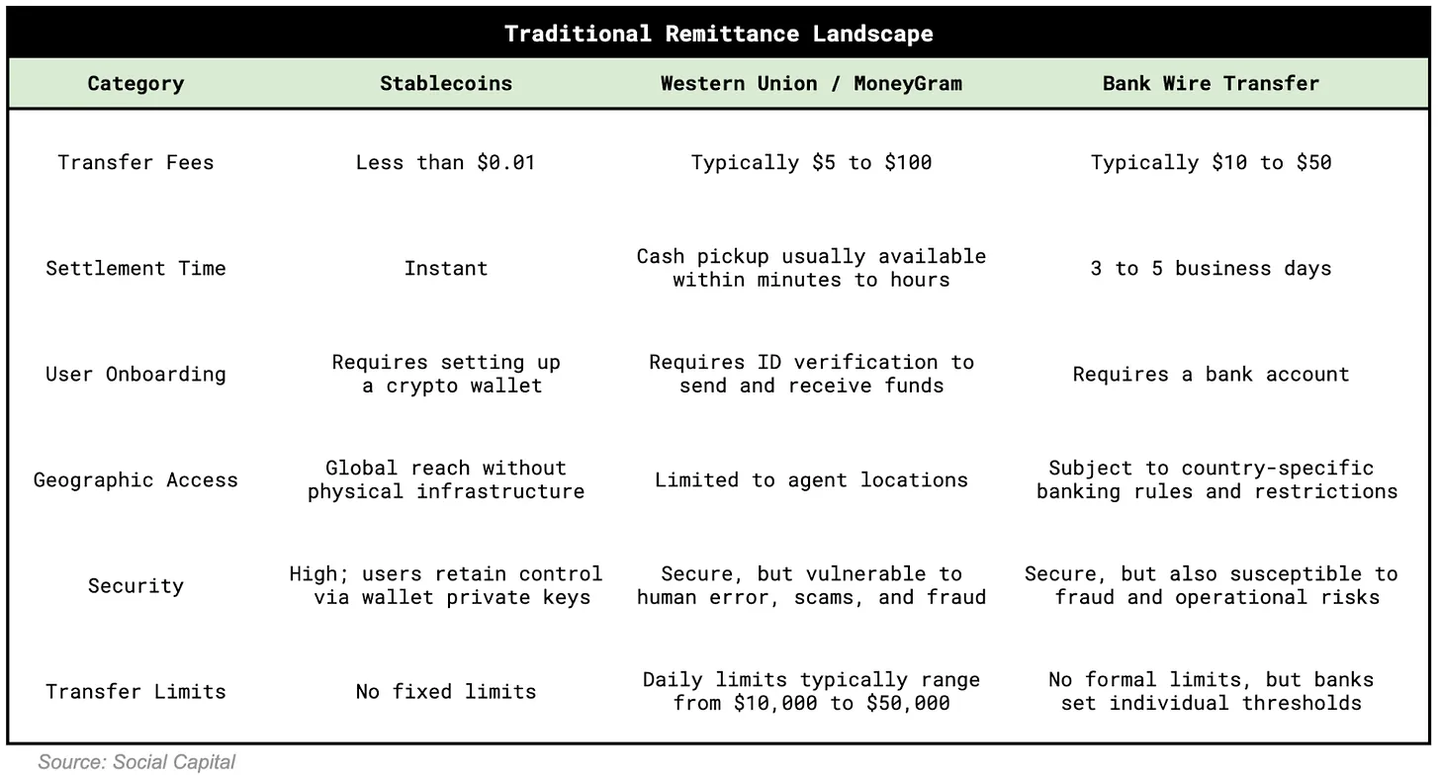

Stablecoins are well-suited for remittances, not only because they provide a more stable store of value (especially dollar-pegged stablecoins) but also because they offer faster, cheaper, and safer cross-border transfers. Currently, most remittances are sent through traditional banks, money transfer operators like Western Union and MoneyGram, or mobile money platforms like M-Pesa in certain regions. Although these channels are widely used, they often involve high fees and delayed settlements. In the fourth quarter of 2023, the global average cost of sending $200 was about 6.4%. In some channels, this figure exceeded 10%. For budget-constrained individuals, losing such a large percentage in remittance costs is a significant burden. These costs resemble a regressive tax on the world's poorest workers, and although the 2030 Sustainable Development Goals aim to reduce global remittance costs to 3%, fees still grow at an annual rate of 3.2%.

In the major remittance channels, banks remain the most expensive, with an average cost of 12% in the fourth quarter of 2023. Post offices follow at 7.7%, money transfer operators average 5.5%, and mobile money services are the lowest at 4.4%. Despite mobile operators having the lowest costs, their share of total remittance volume is less than 1%. In addition to high costs, traditional remittance methods often involve delays. Recipients may have to wait 2-5 business days for funds to clear, as payments must go through multiple intermediary banks. Along the way, hidden fees and unfavorable exchange rate markups further reduce the final amount received.

Stablecoins for Remittances

Stablecoins and their operating cryptocurrency rails provide an internet-native alternative that optimizes speed, transparency, and low cost. Just as the internet revolutionized global instant information transfer, stablecoins have achieved a similar transformation for value transfer. Because they operate on public blockchains, transactions settle in seconds and are available 24/7.

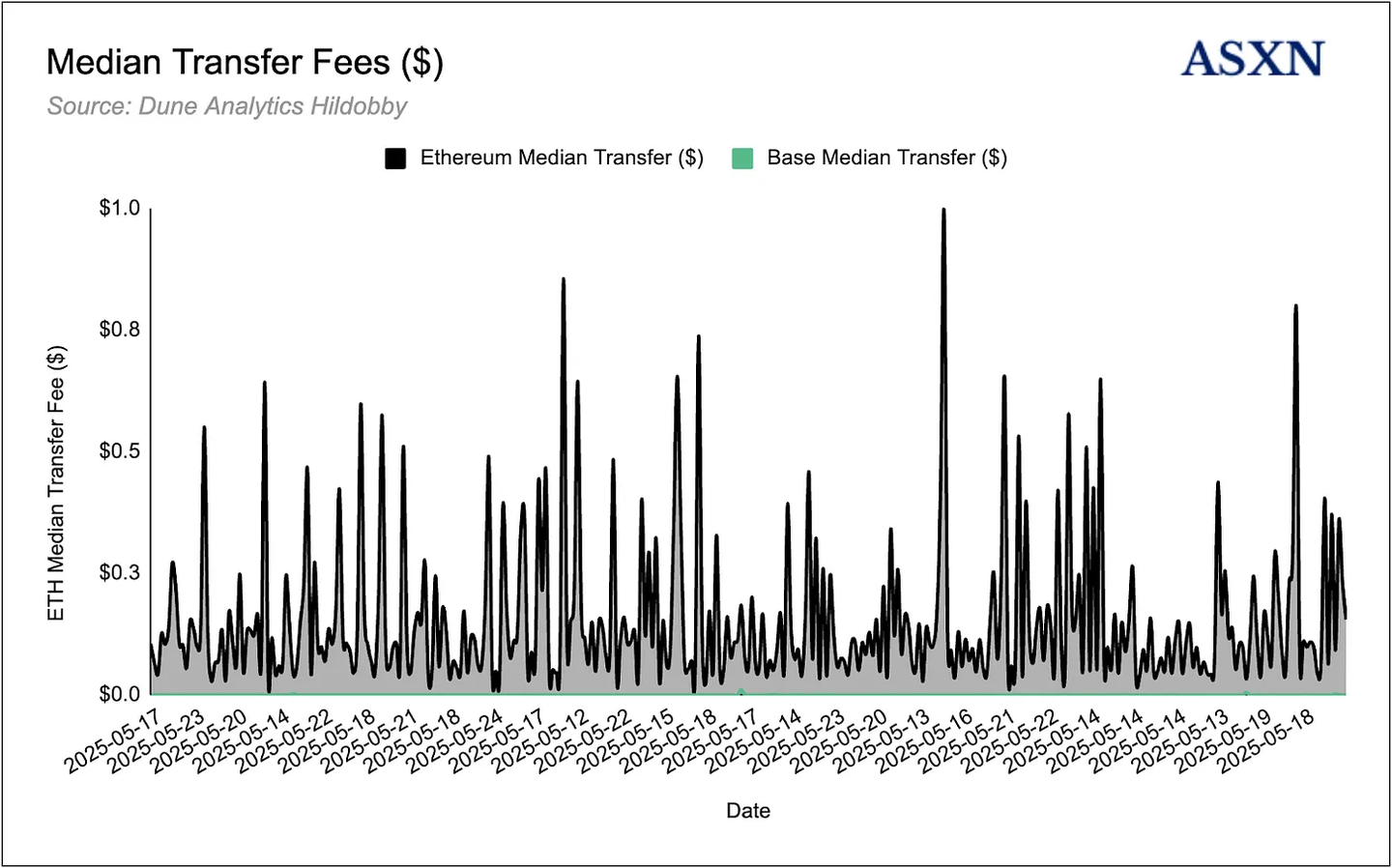

While the global average remittance fee is 6.4%, on-chain transaction costs are often calculated in cents or even fractions of a cent, thanks to recent advancements in blockchain scalability. For example, the average transfer fee on Base over the past two weeks was only $0.00024, while Ethereum's was $0.155. High-throughput blockchains like Solana and the upcoming Plasma are expected to further reduce costs, with Plasma aiming for zero fees on USDT transactions.

Moreover, the entire payment path is visible on the blockchain. There is no need for banking relationships or pre-existing accounts: anyone with an internet connection and a digital wallet can send or receive stablecoins, providing access to regions with limited or underdeveloped banking infrastructure. Senders can fund USDC or USDT through debit cards or bank transfers, almost instantly transferring these tokens across borders and exchanging them for local currency through local partner networks. Even accounting for withdrawal fees (which can be as low as 0-2% in competitive channels), total costs are typically below 2% of the transaction. This reduction in time and cost represents a significant improvement for families relying on remittances for their livelihoods.

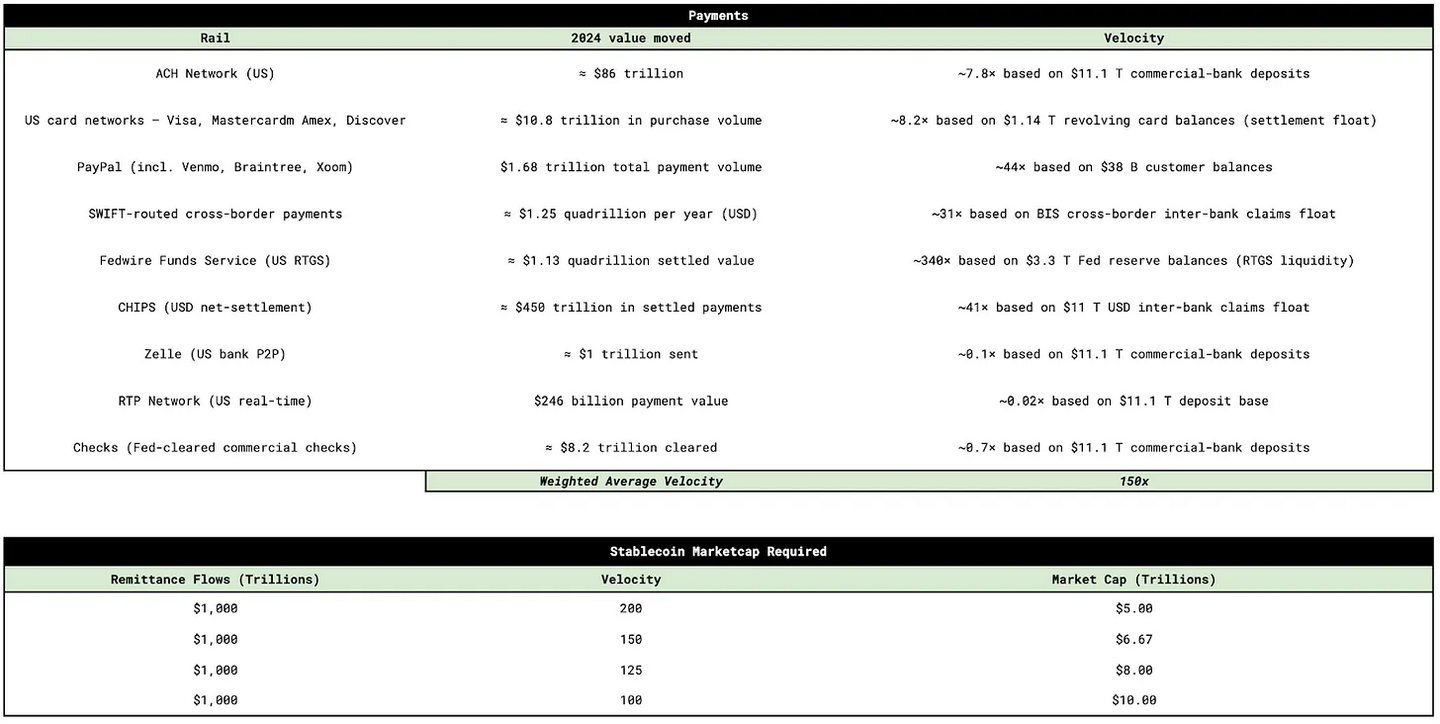

Payments

While remittances are a unique subfield, the broader global payment ecosystem—which encompasses consumer transactions, business-to-business cash flows, public sector and social spending, and emerging embedded rails—continues to struggle with the limitations of traditional infrastructure. Core limitations include high costs, slow settlement times, low transparency, and poor interoperability. Despite these structural inefficiencies, the global payments industry remains one of the largest in the world, processing 3.4 trillion transactions in 2023, involving $180 trillion in value and generating $2.4 trillion in revenue.

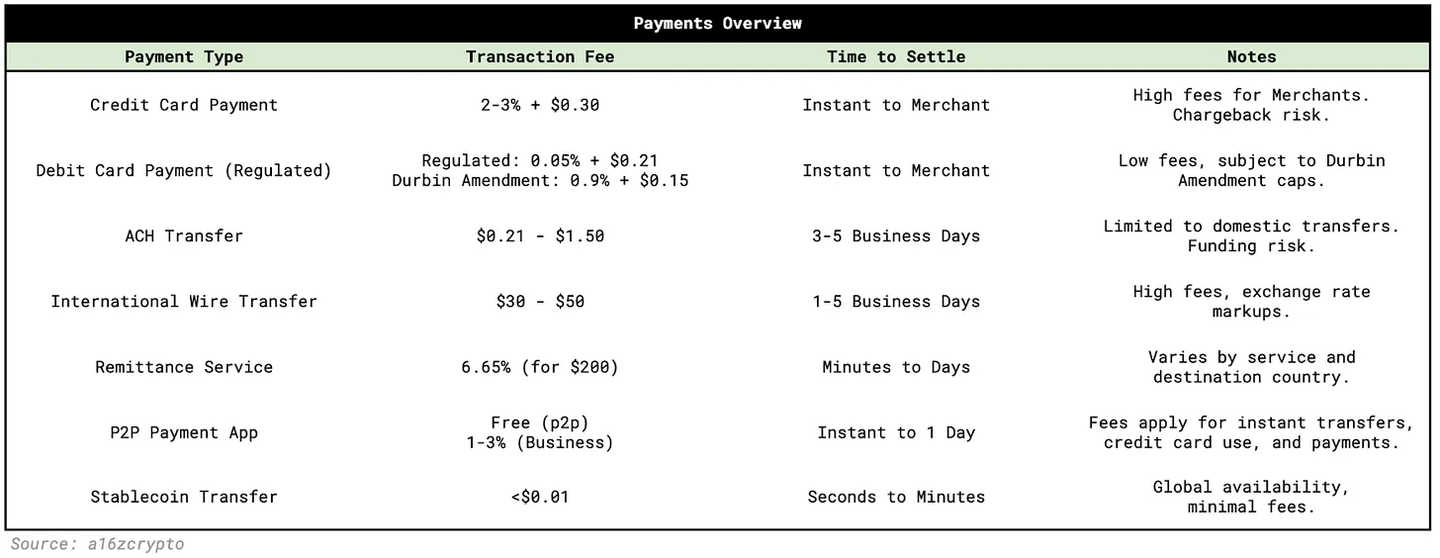

Let’s briefly look at the most commonly used payment rails today to understand how stablecoins and crypto rails can reduce fees and settlement times, thereby improving the profitability and operational efficiency of global businesses:

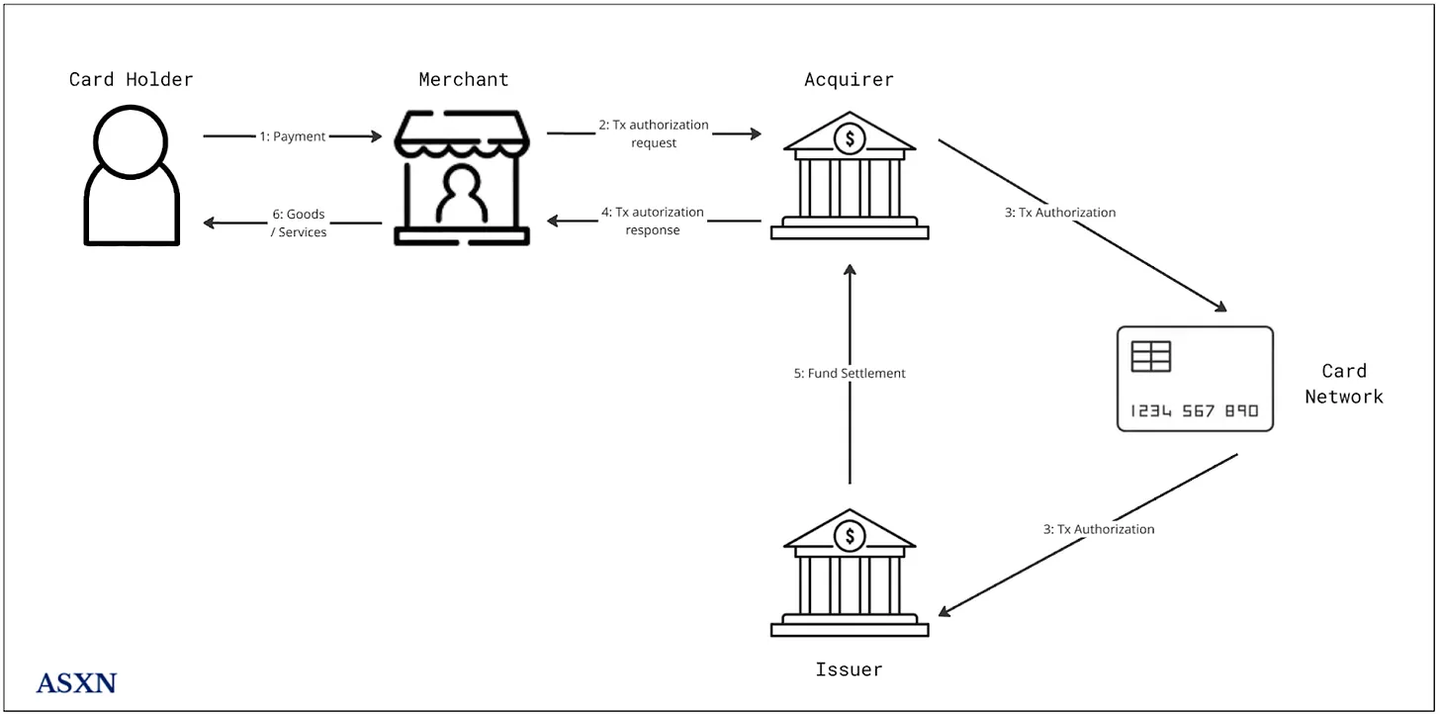

- Card Networks: Card networks and payment cards originated with the launch of the Diners Club credit card in 1950 and have since expanded to process over $40 trillion in transactions globally each year. Card payment systems are a multi-party network connecting four core participants: cardholders, merchants, issuing banks (which provide and authorize cards), and acquiring banks (which settle funds on behalf of merchants). These participants interact through open-loop schemes (Visa, Mastercard) or closed-loop networks (American Express). When consumers make a payment, data flows from the merchant's gateway (encrypting and routing information) to the payment processor, then through the card network to the issuing bank for authorization. Once approved, funds are captured and ultimately settled in bulk cycles. The fee structure—interchange fees charged by issuing banks, scheme fees charged by networks, and settlement fees charged by acquiring banks—is set by the card networks and varies by region and card type, typically ranging from 2-3% of the transaction plus a fixed fee (around $0.30). Modern payment service providers (PayFacs) and orchestration platforms simplify merchant access and optimize routing, improving acceptance rates and reducing costs.

ACH (Automated Clearing House): ACH is the foundational payment network in the U.S., moving trillions of dollars annually between over 10,000 financial institutions. Originally developed in the 1970s to replace paper checks, ACH gained nationwide adoption when the federal government used it for social security payments. Today, it supports everything from direct deposits and utility bill payments to business vendor payments. The system processes credit ("push") and debit ("pull") transfers, operating in batches rather than in real-time. Each transaction involves the originator, their bank (ODFI), the operator (such as the Federal Reserve or a clearinghouse), and the receiving bank (RDFI). The originating bank assumes responsibility for the legitimacy of the transaction, especially in debit scenarios—hence the 60-day consumer dispute window. Same-day ACH, launched in 2015, allows for faster processing but still faces transaction limits and a lack of international coverage. Despite its age, ACH remains deeply embedded in the U.S. financial infrastructure due to its reliability, ubiquity, and relatively low cost compared to card networks ($0.21-$1.50).

Wire Transfers: Wire transfers are the backbone of high-value, time-sensitive payments in the U.S., primarily facilitated through the Fedwire and CHIPS systems. Fedwire, operated by the Federal Reserve, uses real-time gross settlement (RTGS) to process transactions instantaneously, crucial for securities settlements and large corporate transactions. CHIPS, owned by major U.S. banks and operated by a clearinghouse, serves fewer institutions and reduces liquidity needs through net settlement, with most transfers settling the same day. Once sent, wire transfers are typically irreversible, making them a reliable rail for final settlement. For international wire transfers, banks often rely on SWIFT, a secure global messaging network used by over 11,000 financial institutions to transmit instructions rather than direct funds. SWIFT-supported cross-border payments typically settle within one business day, but this depends on the chain of intermediary banks. Together, they move trillions of dollars daily, supporting the global payment infrastructure.

Payment Apps: Peer-to-peer payment apps like Venmo and PayPal allow individuals to digitally send and receive funds within a closed network, requiring users to create accounts and log in to transact. These platforms provide a seamless, low-friction user experience in developed markets, often allowing free personal transfers via linked bank accounts or balances, with settlement times being instant or less than a day. However, cross-border payments are more complex, involving additional fees, currency conversion, and regulatory friction. While peer-to-peer transfers may be free, business-related transactions typically incur fees of around 3%, which is attractive for personal use but can be costly for merchants or business transactions.

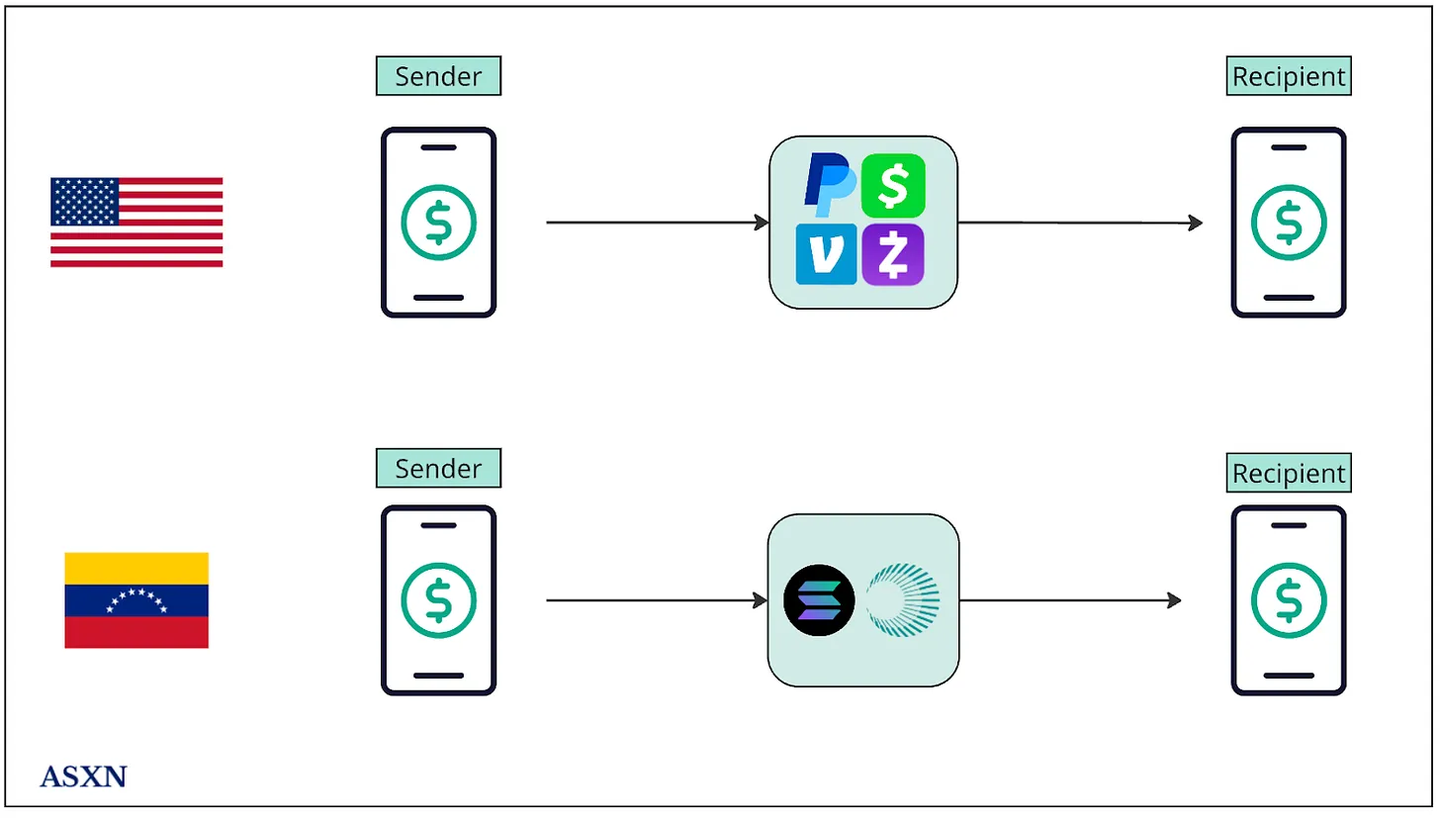

While the banking experience in the U.S. is seamless, stablecoins provide users in countries with high inflation and low trust in the banking system, like Venezuela, a secure way to transfer value.

A16Z provides a comprehensive overview of traditional payment methods, detailing associated costs, settlement times, and operational details. Compared to crypto rails, these traditional systems appear outdated—characterized by high transaction costs, slow settlements, return risks, closed networks, and limited accessibility.

Merchants and Enterprises

In our view, stablecoin-based payments will have the most direct impact on U.S. businesses, particularly those targeting the U.S. as the world's largest consumer market. This is primarily due to the high credit card usage rate in the U.S. and its associated processing fees.

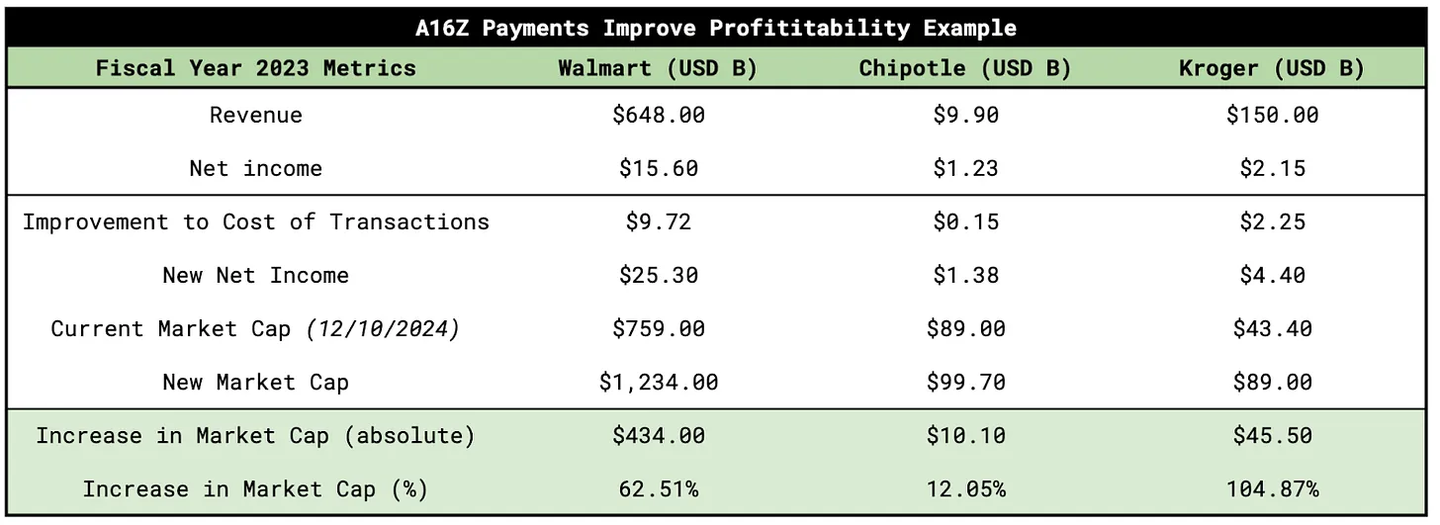

A16Z provides a compelling case study highlighting the profit potential of integrating stablecoin payment infrastructure into large U.S. enterprises. By reducing payment processing fees to 0.1%, the improvement in profitability is significant:

Walmart: Reporting revenue of $648 billion for fiscal year 2024, it may pay around $10 billion in credit card fees, while net income is $15.5 billion. Eliminating these fees could boost profits by over 60%, significantly enhancing valuation.

Chipotle: With revenue of $9.8 billion and net income of $1.2 billion, credit card fees are approximately $148 million. Reducing these fees could increase profits by 12%—no other line item on the income statement can match this increase.

Kroger: Operating on a profit margin of less than 2%, the potential card fees are comparable to its net income. For low-margin retailers like Kroger, stablecoin payments could double profitability.

In short, for large U.S. enterprises facing significant burdens from payment processing costs, crypto-native rails—especially stablecoins—offer an underutilized opportunity to unlock margins and enhance enterprise value. According to a recent report by The Wall Street Journal, Walmart and Amazon are exploring issuing their own stablecoins.

Cross-Border Business Payments

Cross-border B2B transactions remain a significant bottleneck in global commerce. Even routine payments—such as a Kenyan distributor paying a Malaysian supplier—can pass through multiple banks and foreign exchange providers, each adding fees, delays, and settlement risks. What should be simple transfers often turn into multi-day processes, hampered by traditional infrastructure. Banks continue to dominate this space, handling about 92% of global B2B cross-border payment flows.

Payment service providers face similar challenges. Platforms like Stripe may take up to a week to complete international merchant payments, with funds tied up due to managing returns, currency risks, and settlement uncertainties. Shortening this cycle would free up substantial working capital and reduce systemic friction in the value chain.

This means that even a 1-2% reduction in transaction fees can significantly impact corporate profitability, as shown in previous case studies. Speed is equally critical: reducing settlement times from days or weeks to hours can greatly enhance working capital efficiency and improve overall cash flow management. You can learn more about B2B payments, cross-border vendor payments, accounts receivable, and foreign aid spending in Archetype's crypto rails report.

New Payment Use Cases

Stablecoin-based payments also open up entirely new use cases for internet-native payment infrastructure: