Written by: White55, Mars Finance

A procedural vote lasting nine hours with a four-vote margin, a late-night secret meeting at the White House, and the dramatic passage of three bills mark a watershed moment in the history of U.S. cryptocurrency regulation.

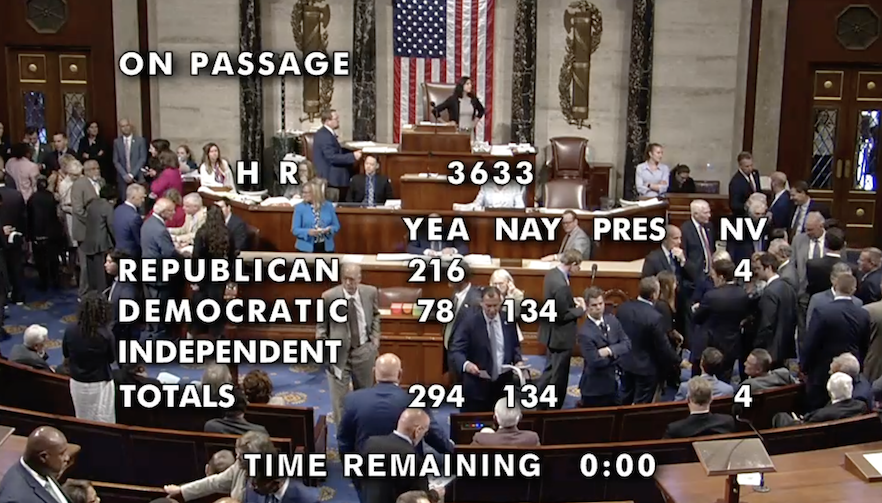

_ On Thursday, the House voted on the CLARITY Act. Source: _U.S. House of Representatives

On Thursday, the House voted on the CLARITY Act. Source: _U.S. House of Representatives

On the night of July 17, U.S. local time, the House of Representatives passed three key cryptocurrency bills through a marathon vote lasting over 8 hours, setting the record for the longest vote since the implementation of the electronic voting system.

This legislative battle, dubbed "Cryptocurrency Week," concluded with the GENIUS Act receiving 308 votes in favor and 122 against, and the CLARITY Act receiving 294 votes in favor and 134 against.

Just as the market was still digesting this significant news, the Financial Times reported another shocking policy development: the Trump administration is drafting an executive order to allow $9 trillion 401(k) retirement plans to invest in cryptocurrencies and other alternative assets.

Bill Passage: A Political Game of Four Votes

The drama of the legislative process exceeded market expectations.

On July 15, during a procedural vote in the House, over 10 Republican members cast opposing votes, blocking the bill's progress.

The deadlock continued until the evening of the 16th, when the House narrowly passed the procedural vote allowing the bill to enter debate with a vote of 217 to 212.

This was just the first hurdle.

On July 17, hardline Republicans in the House struck again, causing the vote to be temporarily shelved. The core of the deadlock was the conservatives' demand to ensure the passage of the Anti-CBDC Act, while members of the Financial Services Committee were concerned that additional provisions could lead to the simultaneous failure of both bills.

At a critical moment, Trump personally intervened to mediate.

Late Tuesday night, Trump held an emergency meeting in the Oval Office with about 12 conservative lawmakers. After the meeting, he claimed on social media, "They all agreed to vote in support of the rule." However, this promise did not yield immediate results.

On Wednesday, House Speaker Johnson engaged in over nine hours of closed-door negotiations with members of the Financial Services Committee, the Agriculture Committee, and conservative lawmakers. The compromise reached was to attach the Anti-CBDC Act to another "must-pass" bill, the National Defense Authorization Act. This political maneuver broke the deadlock and cleared the way for the final vote on the three bills.

Bill Analysis: A Historic Reconstruction of the Regulatory Framework

The three bills form the cornerstone of U.S. cryptocurrency regulation, each targeting different areas:

GENIUS Act: The Compliance Path for Stablecoins

This bill requires stablecoins (such as USDT, USDC) to be backed 100% by cash or short-term U.S. Treasury securities, and to publicly disclose asset statements monthly. Issuers with over $50 billion in circulation must also undergo annual additional audits. This means compliant stablecoin issuers like Circle will gain a significant advantage — its stock price surged 14% before the bill's passage.

More strategically, the bill mandates U.S. Treasury reserves, potentially making stablecoin issuers the third-largest buyers of U.S. Treasuries after the Federal Reserve and foreign governments. U.S. Treasury Secretary Yellen has predicted this could lead to up to $2 trillion in Treasury demand.

CLARITY Act: A Century Division of Regulatory Authority

This 236-page bill clearly defines the distinction between "digital asset securities" and "digital commodities" for the first time. Its core breakthrough is the introduction of the concept of "mature blockchain systems": tokens that meet the three standards of decentralized governance, open-source code, and automated operation can be regulated as commodities.

The bill also exempts four types of entities from compliance obligations: blockchain developers, node operators, front-end developers of DeFi protocols, and non-custodial wallet service providers. This means companies like Uniswap Labs, which only provide interfaces, no longer need to worry about accusations of being "unregistered exchanges."

Anti-CBDC Act: The Defense of Dollar Stablecoin Monopoly

The bill directly prohibits the Federal Reserve from issuing a central bank digital currency (CBDC) without congressional authorization, cutting off the competitive pathway between official digital currencies and stablecoins. Against the backdrop of over 98% of central banks globally developing CBDCs (including China's digital yuan), this bill aims to solidify the monopoly of dollar stablecoins worldwide.

Pension Revolution: A Breaking Moment for the $9 Trillion Market

As the cheers of legislative victory have not yet subsided, the Financial Times has reported another policy bombshell: the Trump administration is drafting an executive order requiring the Department of Labor and other agencies to remove regulatory barriers, allowing 401(k) and other retirement plans to invest in cryptocurrencies, gold, and private equity.

This policy has been in the works for some time. In May of this year, the Department of Labor rescinded guidance from the Biden administration that hindered 401(k) investments in cryptocurrencies, signaling "investment neutrality." Earlier, in 2022, Republican Congressman Peter Meyer proposed the Retirement Savings Modernization Act, attempting to incorporate digital assets into the retirement framework.

The strategic intent of the new policy is clear:

- Opening Asset Classes: Breaking the long-standing limitation of 401(k) plans to traditional stocks and bonds, incorporating cryptocurrencies, gold, and private equity into the investment scope.

- Reducing Legal Risks: Establishing a "safe harbor" mechanism for plan managers, protecting them from excessive litigation when offering high-risk assets.

- Reconstructing Capital Flows: Unlocking investment restrictions in the $9 trillion retirement market, bringing long-term capital to alternative assets!

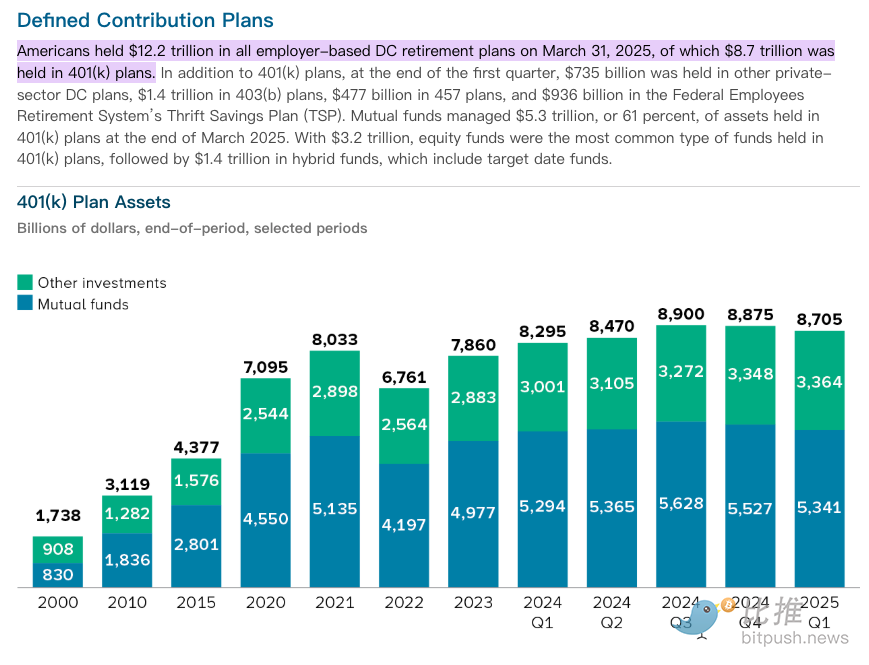

To understand the far-reaching impact of this policy, one must delve into the structure and scale of the U.S. pension market. As the world's top retirement reserve system, the total scale of the U.S. pension market has surpassed $9 trillion.

Specifically, as of the end of March 2025, the total assets of employer-sponsored defined contribution (DC) retirement plans in the U.S. reached $12.2 trillion. Among these, the core component, the 401(k) plan, accounts for $8.7 trillion, becoming the central vehicle for long-term wealth accumulation for American wage earners.

This massive funding source comes from the continuous contributions of tens of millions of workers.

The 401(k) plan, with its core advantages of pre-tax deductions, tax incentives, and employer matching, has become the cornerstone of asset allocation for most households.

Traditionally, pensions have been primarily allocated to publicly traded securities. As of the end of the first quarter of 2025, approximately 61% ($5.3 trillion) of 401(k) plan assets are managed by mutual funds, with equity funds ($3.2 trillion) dominating, followed closely by mixed products like target-date funds at $1.4 trillion. This allocation pattern, primarily focused on equity and fixed-income mutual funds, provides operational space for the current policy breakthrough in alternative assets.

Individual retirement accounts (IRAs) offer more flexibility for self-directed investments, and these retirement reserves accumulated by ordinary citizens constitute a long-term capital source supporting the U.S. economy and capital markets.

Comparing with China's pension system, both countries adopt a multi-layered design approach: the employer-funded nature of domestic enterprise/professional annuities is similar to that of 401(k) plans, while personal pension accounts align with the self-directed investment logic of IRAs.

Therefore, the expansion of the investment scope of U.S. pensions holds significant reference value for global asset allocation concepts.

And the keen-eyed Wall Street giants have already made early moves:

- Blackstone has partnered with Vanguard.

- Apollo Global Management and Partners Group are providing private equity products to retirement plan operators Empower.

- BlackRock has established a partnership with third-party management firm Great Gray Trust.

State governments have also begun to experiment. North Carolina has proposed allowing retirement funds to allocate 5% to cryptocurrencies; the Michigan and Wisconsin retirement systems have already invested in Bitcoin and Ethereum spot ETFs.

Conclusion: Challenges in the Era of Regulatory Clarity

On July 18, the GENIUS Act will be signed into effect by Trump; the executive order for the new 401(k) policy may be announced this week. Behind this policy combination is the ambition of the U.S. to seize the dominant position in cryptocurrency.

As the $9 trillion retirement funds connect with the cryptocurrency market, the boundaries between traditional finance and digital assets are beginning to blur. Institutions like BlackRock have started to include Bitcoin ETFs on their balance sheets, and JPMorgan plans to accept Bitcoin as collateral for loans.

The innovation dividends brought by regulatory clarity may propel the U.S. to regain blockchain dominance. However, the risks of this experiment cannot be ignored — the retirement money of ordinary Americans is being funneled into highly volatile new assets, while Wall Street private equity giants will become the biggest beneficiaries.

A watershed moment in the global cryptocurrency history has arrived; the "clarity" of regulation will ultimately forge the "freedom" of innovation, but how to balance freedom and risk remains a test of policymakers' wisdom.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。