Unless Eclipse provides a unique product, the token will temporarily inflate.

Author: Pine Analytics

Compiled by: Deep Tide TechFlow

Summary

Eclipse Labs has raised $65 million from top investors to build a Layer-2 based on the Solana Virtual Machine (SVM) on Ethereum. Eclipse has garnered support from companies like Polychain, Placeholder, and Hack VC, positioning itself as a high-performance, cross-chain Rollup platform with ambitious architectural plans.

However, despite its ample funding and good reputation, the on-chain reality is starkly different. Activity is shallow and short-lived, primarily driven by airdrop mining rather than natural demand. Gas fees, deposit amounts, and total locked value (TVL) have been declining. The current application ecosystem lacks a product of unique value—most offerings are merely weaker copies of others.

Due to the lack of outstanding applications and declining usage, Eclipse enters the token issuance cycle with an overvaluation. Although its network fundamentals are insufficient to support this valuation, its fully diluted valuation is expected to exceed $300 million.

The likely outcome is that after a brief short squeeze, sustained selling pressure will follow, as insiders and market makers profit from retail interest before exiting.

Unless Eclipse provides products that can only exist within its stack, the token will temporarily inflate the ecosystem—then gravity will pull it back to the ground.

Funding

Since its inception, Eclipse Labs has raised $65 million through multiple funding rounds, making it one of the most well-funded Ethereum Layer-2 projects.

Funding Round Breakdown

- Pre-Seed ($6 million) – August 2022

This round was led by Polychain Capital, with follow-on investments from Tribe Capital, Tabiya, Accel, Polygon Ventures, and others. This early funding positioned Eclipse as an ambitious attempt to bring Solana's high-performance virtual machine (SVM) to Ethereum. The estimated valuation for this round was $30 million to $40 million, which was common for strong infrastructure development projects at the time (e.g., pre-product).

- Seed Round ($9 million) – September 2022

Co-led by Tribe Capital and Tabiya, with follow-on investments from CoinList, Infinity Ventures Crypto, Soma Capital, and Struck Crypto. Although Eclipse has yet to launch a formal network or protocol, this round pushed Eclipse's valuation into nine figures (post-funding valuation of $100 million to $120 million). The funds were used to expand the engineering team and accelerate infrastructure development.

- Series A ($50 million) – March 2024

Co-led by Hack VC and Placeholder, with participation from Delphi Digital, Polychain (returning investor), OKX Ventures, GSR, Flow Traders, Distributed Capital, Maven 11, and DBA. This round aims to launch the Eclipse mainnet and build the Eclipse ecosystem. Although Eclipse's valuation has not been officially disclosed, insiders estimate it to be between $300 million and $500 million, indicating that Eclipse will become a top competitor in Ethereum Layer-2.

Strategic Positioning

Eclipse's funding is not only unique in scale but also in its promised strategic cross-chain appeal:

Support from Ethereum and Solana investors (e.g., Anatoly Yakovenko, Solana Foundation, Ethereum Foundation researchers).

An architecture that merges Ethereum's security with Solana's execution layer and Celestia's modular data availability.

This allows Eclipse to present itself as the future of cross-chain performance—a "best-in-class" rollup stack.

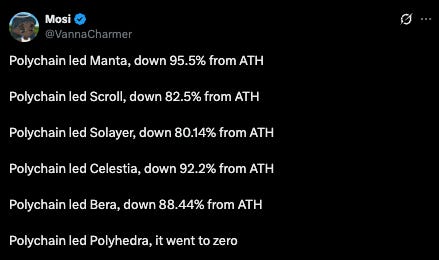

Polychain's Reputation

Polychain Capital led the pre-seed funding for Eclipse and participated in subsequent rounds—but their recent behavior in other investments has raised serious red flags. In projects like Celestia, they aggressively sold off tokens post-launch, reportedly dumping over $240 million of $TIA, leading to a 90% price drop. A similar pattern has emerged in other Polychain-backed tokens, such as Manta, Scroll, and Solayer, all of which have fallen 80% to 95% from their peak prices.

There is no reason to expect Eclipse to be any different. Polychain has consistently shown a willingness to maximize returns, regardless of its impact on the ecosystem. Their early position in Eclipse indicates that they are prepared to rotate out when liquidity appears—rather than build a long-term partnership.

On-Chain Activity and Usage

Despite raising $65 million and positioning itself as Ethereum's fastest L2 platform using Solana's virtual machine, Eclipse's on-chain activity still exhibits a fleeting, airdrop-driven usage pattern with almost no sustained demand. The following data visualizations illustrate the rise and rapid decline of key metrics such as gas payments, user deposits, TVL (Total Value Locked), and application attractiveness.

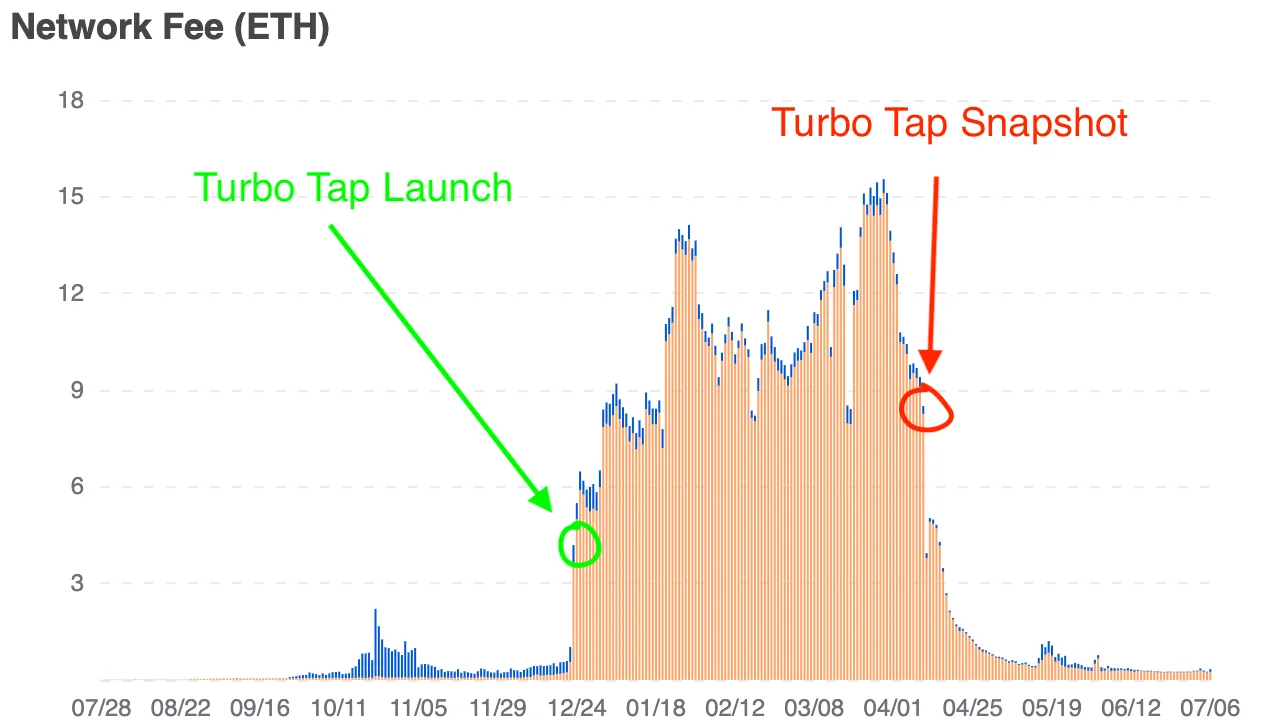

Network Fees Reveal Airdrop-Driven Speculation

This chart shows the total daily network fees paid on the Eclipse platform (in ETH). After the launch of Turbo Tap (an application specifically for airdrop mining), its activity immediately surged. The sharp decline following the Turbo Tap snapshot further confirms the correlation between usage and reward expectations.

By June 2025, network fees had fallen below 1 ETH per day (approximately $750), reflecting both a decline in user transaction volume and the disappearance of incentive-driven behavior. This trend reinforces the notion that there is no other natural trading demand on the network aside from airdrop mining.

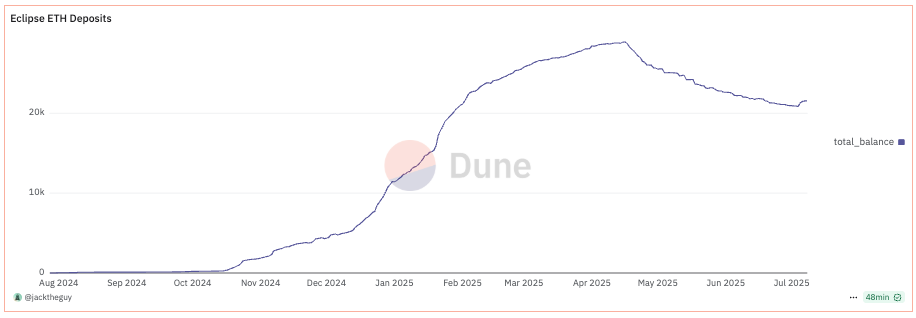

Chain Deposits Steadily Decline

The curves of ETH and Hyperlane deposits into Eclipse closely correlate with the surge in gas usage—both saw rapid growth from December 2024 to March 2025, driven by incentive-driven activity. Starting in Q2 2025, deposit amounts began to steadily decline as users withdrew funds and possibly reallocated them to more liquid or active ecosystems.

Hyperlane-based deposits peaked at $25 million to $27 million in Q1 2025 but have since fallen below $17 million. This downward trend is also consistent among bridged assets like USDC, SOL, and WIF. Importantly, this is not a reallocation of asset composition but an outflow of funds from the entire ecosystem. As the reward incentive mechanisms gradually weaken, user participation also declines, exposing the fragility and temporariness of Eclipse's liquidity base.

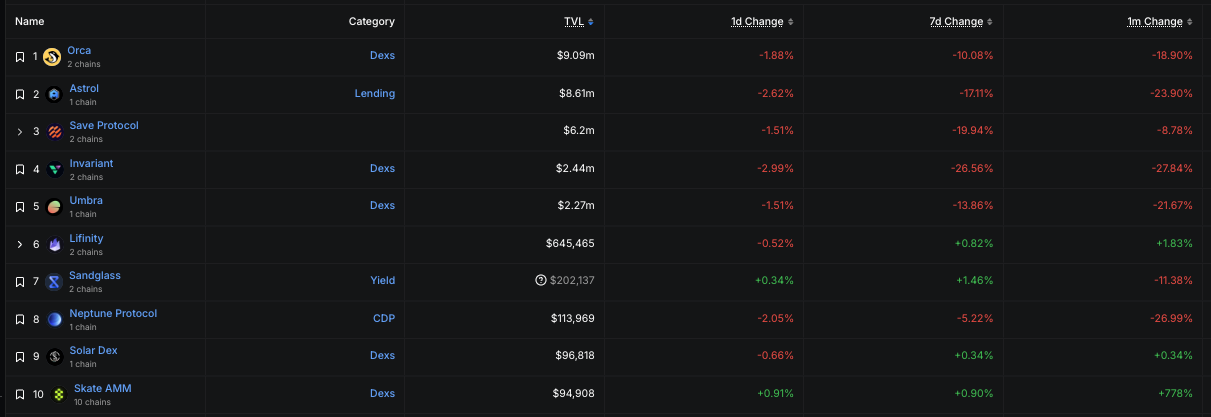

DeFi Application Ecosystem is Small, Illiquid, and Heavily Losing

Among the top 10 Eclipse applications, TVL remains very low:

Only 3 applications have a TVL exceeding $2 million (Orca, Astrol, Save).

Most others have TVLs below $500,000, with some even below $100,000.

The one-month change column shows that almost all major protocols have experienced significant double-digit declines (Astrol -24%, Invariant -28%, Neptune -27%).

This situation indicates that developers have not found sticky traction, and users have not found compelling or profitable reasons to stay.

Lack of Focus

As it stands, Eclipse's application ecosystem lacks any unique and valuable products. The existing application portfolio—DEXs, lending markets, stablecoins, NFT markets—structurally resembles applications already available on Solana, Ethereum, or other Layer-2s. In most cases, they offer fewer features, poorer liquidity, and lack competitive advantages.

For a blockchain to maintain long-term usage and justify its block space, it needs a clear value proposition—an application or experience that cannot be found elsewhere. So far, Eclipse has not achieved this.

Instead, the network's short-term activity is almost entirely driven by airdrop mining. While the upcoming token issuance may temporarily spark user interest, it is unlikely to capture attention without a core reason for retention. Token incentives can generate user momentum, but they cannot replace a genuine product-market fit.

Without outstanding native applications from Eclipse, the ecosystem may quickly unravel after the TGE. Builders will leave in search of more liquid platforms. Users will turn to chains where their tokens have exit opportunities. And this network—despite its strong funding and engineering capabilities—may become irrelevant, not due to technical failure, but because there is nothing truly significant within it.

If Eclipse wants to have a future, it needs to incubate or attract an application that can only be realized on its architecture—an application that leverages SVM in a way that cannot be replicated by any EVM chain. Otherwise, the token will only temporarily inflate the ecosystem, and then gravity will pull it back to the ground.

Expected Token Issuance Dynamics

Based on similar projects and the current state of the Eclipse ecosystem, the most likely outcome is a valuation mismatch at TGE. Despite the chain's declining usage and lack of sticky applications, Eclipse's fully diluted valuation (FDV) is expected to be higher than its most recent private funding round—potentially exceeding $300 million. This would immediately place it among the highest-valued L2 platforms, despite lacking corresponding fundamentals.

Perpetual contract markets may launch shortly after, and traders will begin to short the token, attempting to drive its price down to where it should be. In response, market makers and early supporters will short squeeze these positions, temporarily pushing prices higher until the short positions are brought down to manageable levels. Once liquidity dries up, stakeholders holding unlocked or liquid tokens will begin to gradually sell off, leading to sustained selling pressure and triggering what is typically a prolonged and severe downtrend.

This pattern—overpriced issuance, initial market short squeeze, followed by long-term distribution—is common in overhyped, low-utilization ecosystems. Without a catalyst for natural demand or unique applications to attract attention, Eclipse's token is likely to follow a similar trajectory.

Final Thoughts

Eclipse has raised significant funds, built an impressive tech stack, and attracted the attention of top investors. However, none of this has translated into sustained user demand, product-market fit, or provided the blockchain with a reason for existence beyond short-term speculation.

The current reality is clear: Eclipse lacks a killer application, a sticky user base, and any unique reasons for developers or capital to remain post-token issuance. The token issuance is likely to follow the pattern of many previous token launches—after a brief wave of hype, sustained selling pressure will ensue due to insider rotations and a lack of natural demand.

Eclipse may still find its footing, but this path requires more than just funding and clever architecture. It needs to provide something that only Eclipse can offer—not just technically, but economically and experientially. Until then, the project's valuation will not align with its utility, and the pricing of its token will be more narrative-driven than based on actual usage.

In such a market, downward gravity will ultimately prevail.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。