In-depth analysis of two mainstream paradigms represented by xStocks (Backed Finance) and Robinhood, examining their structural barriers and exploring their potential development paths.

Author: Corgi Kokii

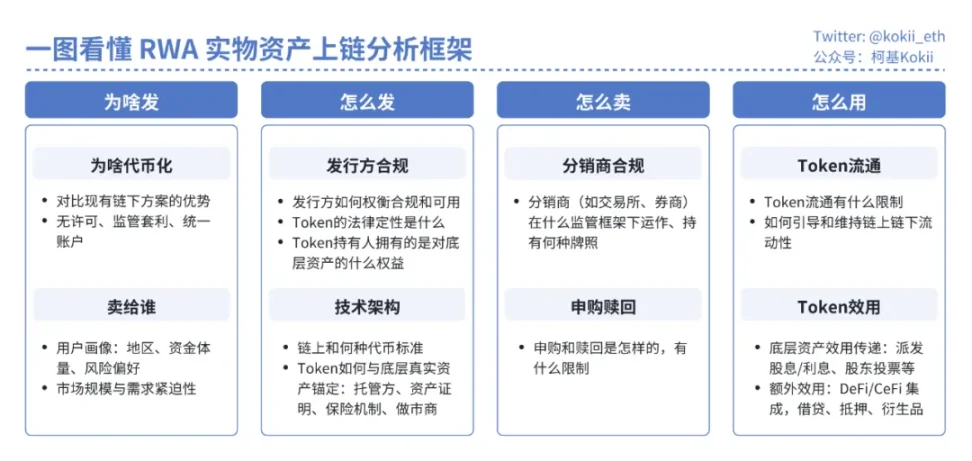

Why Stock Tokenization is Struggling

To understand the difficulties of stock tokenization, one must first recognize the key to successfully bringing RWA/real-world assets on-chain. Whether it is government bonds, funds, stocks, private credit, or even intellectual property, the essence is simply that physical assets are held offline, and a set of tokens is issued on-chain, which has no technical barriers, similar to issuing a memecoin.

However, all project teams must return to the core four questions: Why issue? How to issue? How to sell? How to use? If these questions are not well addressed, RWA can only end up like most memecoins, lacking actual demand and liquidity.

Taking the currently most successful category of RWA products, tokenized US Treasury bonds/money market funds as an example, government bonds, as a standardized debt instrument with simple rights and predictable cash flows, have undergone three steps in their tokenization process: identifying real demand, establishing a compliant issuance framework, and building token utility:

Why issue: Institutional investors [Crypto VC/Fund] have a lot of idle stablecoins on-chain and need risk-free income-generating scenarios.

How to issue: Fund - The fund manager structure, where tokens legally represent fund shares, the fund is responsible for issuing tokens and holding assets, and the fund manager is responsible for making investment decisions. Both the fund and the fund manager must comply with licensing requirements, and institutional-level services such as custodians, audits, and transparency reports are also needed.

How to sell: Only qualified investors after KYC/AML can buy, 24/7.

How to use: Token-derived utility, supported by mainstream DeFi, can be used as collateral to borrow stablecoins, and some centralized exchanges are starting to support it as collateral.

In contrast, stocks, as ownership certificates with complex rights (including governance rights) and uncertain cash flows, must overcome a series of significant operational and compliance barriers for tokenization.

Why Issue

Early RWA attempts often lacked clarity on the "why issue" aspect, focusing on alternative assets like private loans, private equity funds, and real estate, hoping that blockchain's efficient settlement would improve liquidity. However, the limited liquidity of these assets is not a technical issue but is constrained by deeper problems such as information asymmetry, lack of substitutability, pricing challenges, and issuers' resistance to secondary market liquidity. These issues exist off-chain and cannot be resolved simply by going on-chain.

The benefits of bringing physical assets on-chain have become clichés, summarized as follows:

Permissionless accessibility: Including [capital] lowering investment thresholds, [products] eliminating geographical and financial barriers such as bank accounts, compliance, foreign exchange controls, and [time] 24/7/365 trading with instant clearing and settlement; as well as regulatory arbitrage brought by permissionlessness, crypto-native platforms including wallets and exchanges can expand into traditional businesses without licensing.

DeFi composability: Utilizing DeFi protocols for trading, lending, and derivatives, applying DeFi's transparency and composability to traditional assets to gain additional yield opportunities.

Unified accounts: If the circulation of stablecoins increases, and the majority of economic activities are settled on-chain, bringing physical assets on-chain can allow a single account to manage various assets held by different brokers, enabling cross-collateralization.

The key is how to find the target user group. The story of financial democratization sounds grand, but one cannot expect unbanked individuals in Africa to buy US Treasury bonds or stocks. A well-functioning market requires a sufficient number of participants, which can come from political mandates from above, experienced high-net-worth retail investors, or institutional investors who have begun exploring blockchain.

Most likely, the target users of RWA projects are genuinely high-net-worth retail investors and institutional investors looking to invest, leading to the subsequent questions of how to issue and how to sell, and how to avoid the regulatory hammer falling.

Investors need to clearly understand the legal nature of the tokens they are buying, the issuing entity, risk control mechanisms, anchoring mechanisms, whether there is backing, redeemability, and whether it has legal validity. Previous attempts at US stock tokenization by DeFi's Mirror Protocol, Synthetix, and CeFi's Binance, FTX all failed due to regulatory pressure or awkward product design that could not find a market.

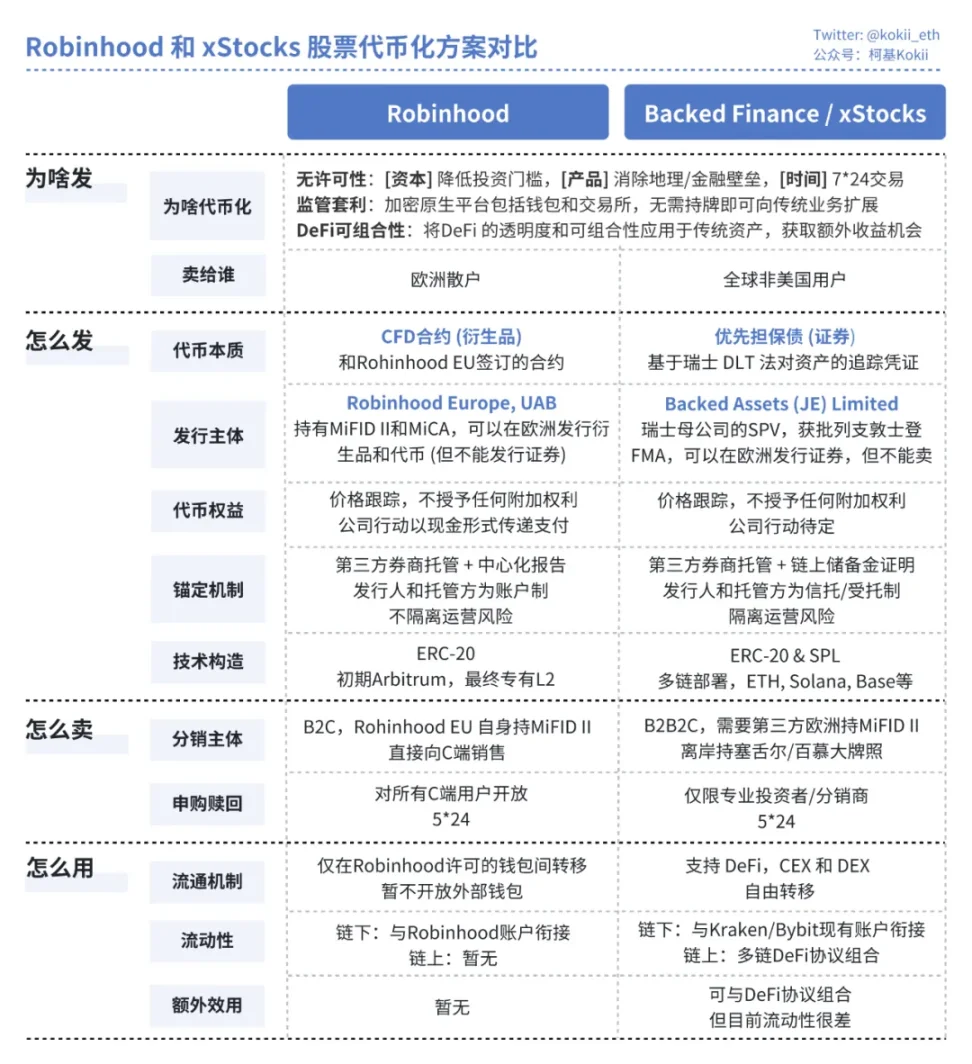

Recently, Robinhood and xStocks have designed a fully compliant, centralized securities registration token with a 1:1 mapping off-chain under relatively friendly existing legislation.

Current Solutions

a. Robinhood

How to issue: The legal core is under the EU MiFID II framework, issued by its licensed entity Robinhood Europe UAB in Lithuania as a financial derivative contract. The tokens held by users are merely digital certificates of this contract, with Robinhood itself as the counterparty. The actual stocks are held by Robinhood's US affiliate brokerage as a hedging position.

How to sell: A B2C model is adopted, with Robinhood Europe as the sole issuer and seller, directly targeting European retail users within its app. Liquidity is entirely provided internally on the platform, creating a closed loop.

How to use: The token's smart contract embeds a strict whitelist mechanism, preventing free circulation and lacking any external DeFi composability.

b. xStocks

How to issue: The legal core is under the Swiss DLT law framework, holding actual stocks through a bankruptcy-remote SPV established in Liechtenstein. The tokens held by users are legally a 1:1 asset-backed priority secured debt (tracking certificate), with its trust mechanism built on independent third-party custody and real-time verifiable Chainlink proof of reserves (PoR).

How to sell: A B2B2C model is adopted, with the issuer Backed Finance serving institutional-level primary market redemptions, and licensed exchanges like Kraken and Bybit acting as distributors for secondary market users. Liquidity is jointly provided by professional market makers from centralized exchanges and liquidity pools in decentralized protocols (such as Jupiter, Kamino on Solana).

How to use: Freely transferable and fully DeFi composable, can be used as collateral for lending.

Legally, the tokens only track prices and do not represent direct equity on-chain, while the handling of other rights associated with stocks (voting rights, dividend rights) and corporate actions (such as splits, mergers, delistings, liquidations) remains unresolved. Meanwhile, the additional utility brought by tokenization has yet to materialize: Robinhood's token can only circulate within its ecosystem, while xStocks, although composable with DeFi protocols, currently suffers from poor liquidity, essentially rendering it non-existent.

These two solutions resemble regulatory arbitrage by crypto-native platforms under the current more lenient regulatory conditions, aimed at attracting market attention to demand better pricing in capital markets. Regardless of the paradigm, the current stage of stock tokenization faces several structural barriers that are difficult to resolve in the short term:

Ambiguous demand: For its target non-US users, there are already many mature, low-cost, high-liquidity channels for trading US stocks in the market (such as online brokers like IBKR, CFDs, etc.), and stock tokenization does not offer significant advantages in user experience and fees.

Liquidity dilemma: Off-chain is the price discovery center. On-chain liquidity is too small and severely fragmented compared to traditional markets, leading to excessive slippage for large trades.

Market-making risk: During off-hours in the underlying stock market (such as weekends), market makers cannot hedge risks, forcing them to widen spreads or withdraw liquidity, resulting in low reliability and cost-effectiveness for 24/7 trading.

Incomplete rights: Both current models have made significant compromises on core shareholder rights. Holders only receive the economic benefits of stocks, while voting and other corporate governance rights are retained and handled by the issuer (SPV or Robinhood), limiting functionality compared to mature tools like ADRs.

Future Paths

Despite the harsh reality, the true significance of this "pilot" lies in exploring future possibilities. The future of tokenized stocks depends on their ultimate positioning within the entire financial ecosystem.

Path A: Mainstreaming and Infrastructure Development. If global mainstream regulatory frameworks mature and clarify, and stablecoins flow into households, major financial institutions will place a certain amount of assets on-chain, and issuing custodians will gradually evolve into traditional financial giants like JPMorgan and BNY Mellon. At that time, stock tokens will become a more powerful "composable super ADR." Blockchain will serve as a unified settlement layer for global equity markets, integrated into various DeFi protocols, with companies going public directly through STO issuance on-chain.

Path B: Offshoring and Emerging Asset Platforms. If mainstream regulation continues to tighten, the crypto world may evolve into an efficient offshore innovation center. At that time, tokenization will no longer seek to compete with NYSE for trading Apple stocks but will shift to becoming a "launch platform" for new or illiquid assets, such as private equity of pre-IPO companies, fractional transfers of VC fund shares, or even the securitization of future income streams like intellectual property.

The current immaturity of tokenized stocks is not a sign of failure but rather an early necessary stage in the construction of infrastructure. The measure of its success should not be whether it can provide a better trading experience for Apple stocks today, but rather what new markets and financial behaviors it creates for tomorrow. For all market participants, understanding this is key to seizing opportunities in the impending financial revolution.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。