What's the upside for L2 tokens?

Fee sharing?

Even if they turned on fee sharing, it's not much:

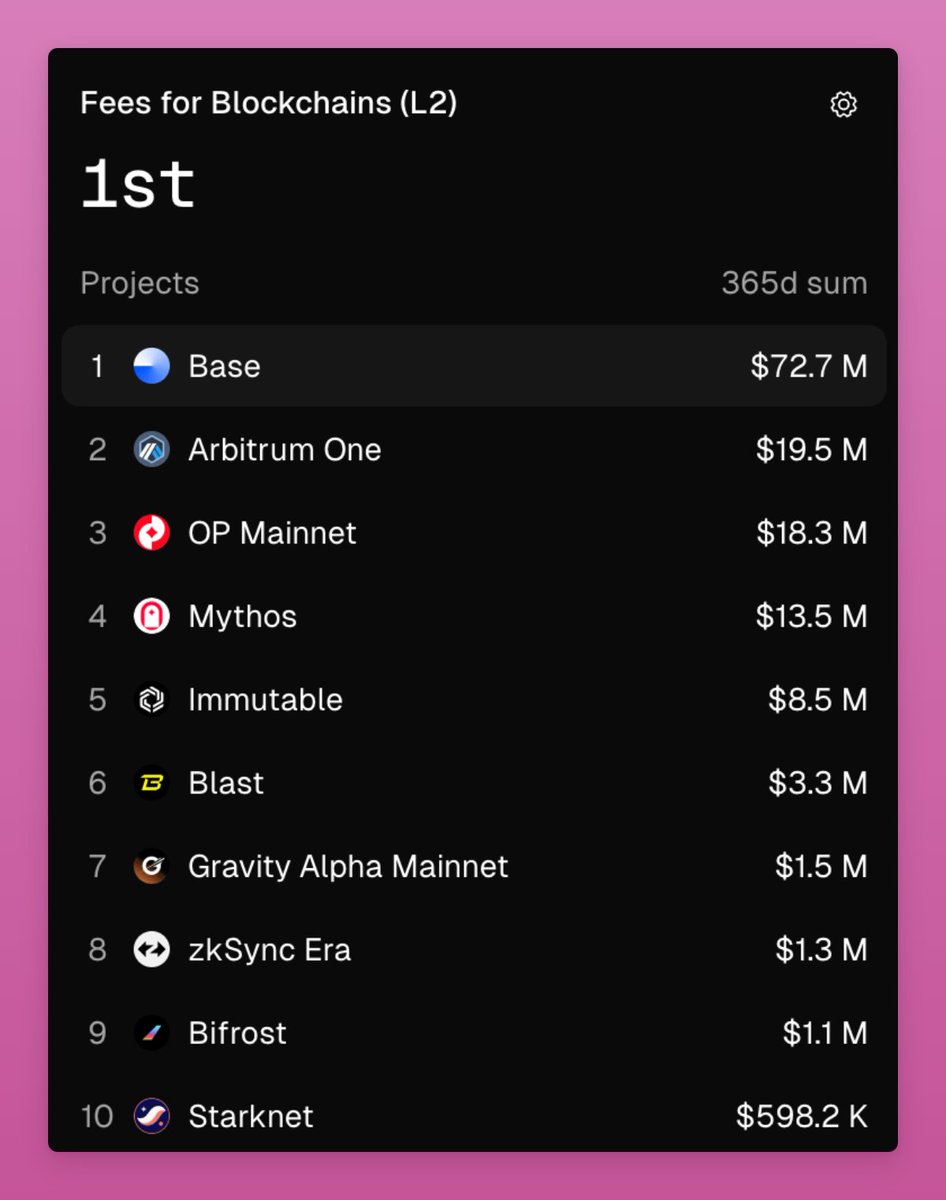

Arbitrum made $19.5m in fees in a year. Optimism $18.3m.

zkSync just $1.3m and Starknet $600k.

This Price(FDV)-to-Fees ratio puts Arbitrum at 137.8x, and Optimism at 205.7x

Starknet - 4204x

In context, TSLA trades at 187x P/E ratio so Arbitrum might even look cheap.

But Tesla is an exception. S&P500 trades at ~ 29x the earnings.

This makes L2 tokens overvalued by a lot. Unless we expect their adoption and fees to pick up massively.

Maybe governance?

Hoarding tokens gives voting power to direct incentives.

But projects like @lobbyfinance make bribing cheap. Recently one user paid 5 ETH (~$10k) on Lobby to buy 19.3M ARB (~$6.5m) voting power.

I believe that most projects issue tokens for two main reasons:

- To raise capital

- To bootstrap adoption

L2s are bootstrapping adoption, like the Arbitrum DRIP proposal, which allocates 80M $ARB.

The goal is to attract sticky liquidity, outlive, and outcompete other L2s.

If we apply the Pareto principle, 80% of the liquidity will eventually concentrate in 20% of the L2s.

So, perhaps we need to wait until the L2 winners become clear and then invest in them.

This implies waiting for most L2s to naturally phase out.

Yet as more L2s launch with new tokens, the timeline for clear winners to emerge is extended.

(Except for Base... Which doesn't have a token (just a stock)).

$INK is about to launch a token with liquidity mining to inflict even more pain on the remaining L2s.

A cursed sector to invest.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。