Break down the yield-bearing stablecoin project to the finest granularity and see how each party plays the game with capital, users, and the market.

Written by: Zuo Ye

Continuing from the previous article, the logic of yield-bearing stablecoins (YBS) is to mimic the banking industry; this is just the surface. It also needs to address numerous issues such as where user returns come from, how they are distributed, and how to maintain the long-term operation of the project. The collapse of DeFi projects is a routine occurrence in the financial industry, as evidenced by SBF going to prison. However, the situation with Silicon Valley Bank is a budding systemic risk that requires immediate action from the Federal Reserve.

The Era of Excessive Leverage

The pursuit of profit is a product mindset, and the financialization of this is speculation. Significant price differences are the source of arbitrage, and long-term volatility requires risk hedging.

The reverse is the movement of the Dao. After the introduction of computer technology, the financial industry has gone through three stages of quantitative speculation:

• Portfolio insurance: Diversifying investment targets to preserve value, quantifying risk levels, and pricing them;

• Leverage (LTCM): Accumulating small profits through borrowing to amplify returns;

• Credit default swaps: CDS is not a demon; the risk control of derivatives fails and devolves into pure gambling;

In the current financial world, significant spatial price differences have disappeared. Normalization, small-scale, and decentralization are now the norms. On-chain MEV and off-chain CEX are Web3's imitation of TradFi.

Long-term preservation of value is no longer mainstream; leverage, extremism, and speculation are the goals. Hedging itself has become the objective, and future risks will never bring about a future.

In this context, YBS project teams generally face a paradox: if the APY/APR is not high enough, it is difficult to attract funds to increase TVL; but if they promise too high, they will inevitably head towards a Ponzi scheme, ultimately leading to a blow-up at any stage of TGE, financing, rug pulls, score manipulation, VC, or exchanges.

Hedging is essentially arbitrage, and momentum cannot be avoided.

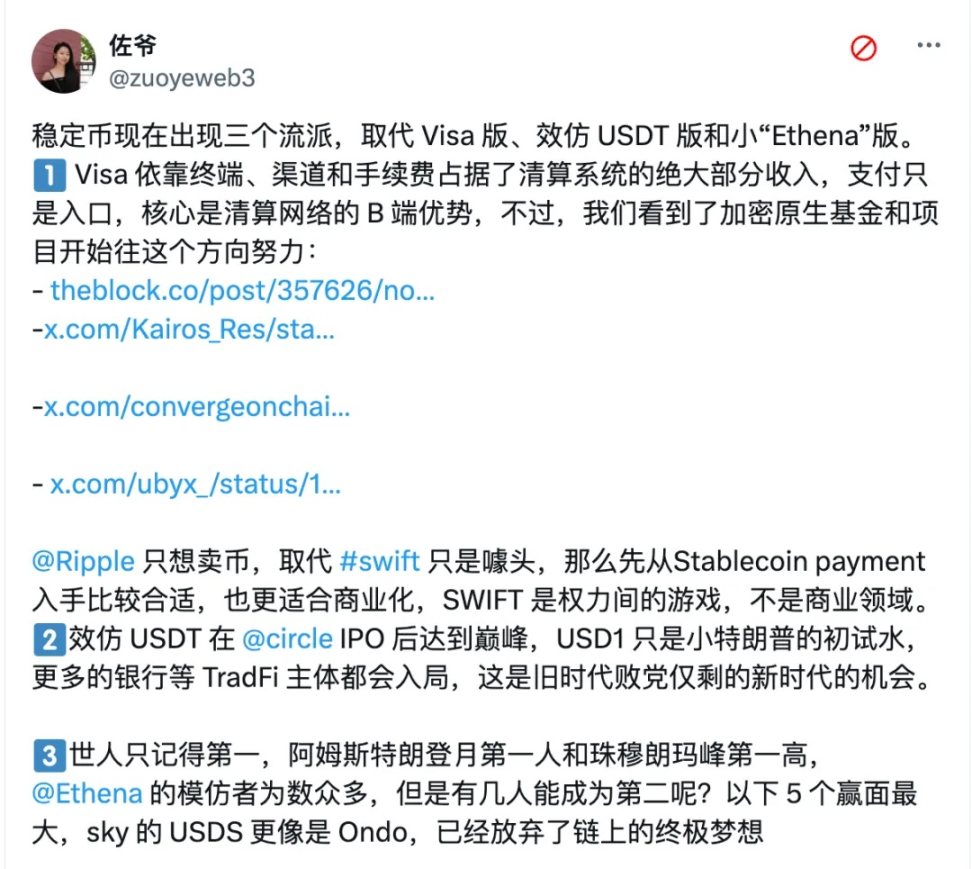

Image description: Stablecoin factions

Image source: https://x.com/zuoyeweb3/status/1935242935634903275

First, let's extract YBS from the stablecoin market. Currently, stablecoins exist in three branches:

• The first is for institutional use, primarily as a clearing network for cross-border, cross-industry, and cross-entity transactions, aiming to supplement and replace existing products like Visa and SWIFT, such as JD.com or JP Morgan;

• The second is products similar to USDT promoted by TradFi, which can be divided into dollar-pegged and non-dollar-pegged stablecoins, as well as alternative attempts by large financial institutions, such as USD1;

• The third is competitors to Ethena, such as Resolv, which is also the main focus of this article.

The market always has a kind of "impulse," surging when it can rise and continuing to dive when it expects a bottom, referred to as momentum. YBS fits this perfectly, as many projects will compete with Ethena, pulling APY to the highest, then the market clears, leaving the king of this track. Hedging will ultimately converge with arbitrage, making them indistinguishable.

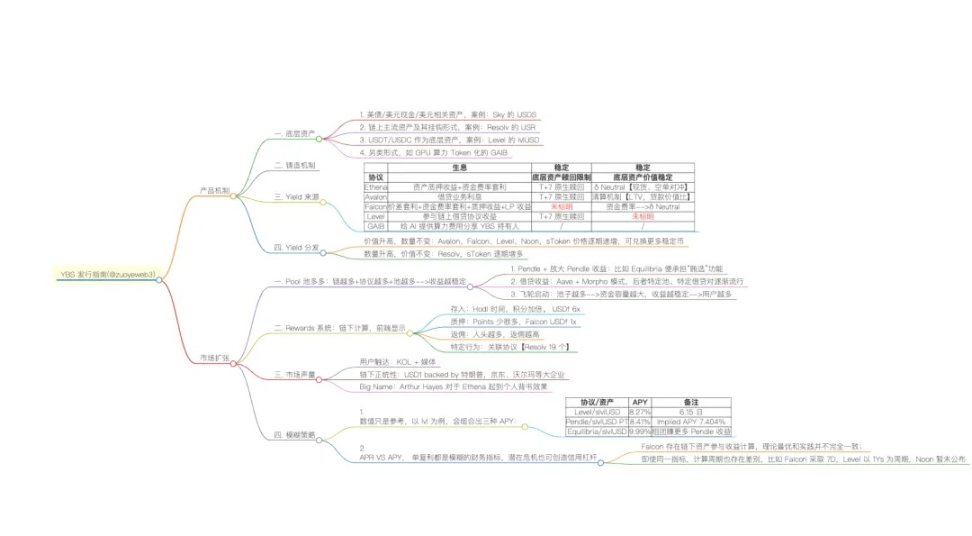

Image description: YBS issuance guide

Image source: @zuoyeweb3

Still the familiar formula. After analyzing over 100 YBS projects frame by frame, we extracted the issuance guidelines for yield-bearing stablecoin projects, roughly divided into product mechanisms and market expansion. The product mechanism consists of four parts: underlying assets, minting mechanisms, sources of income, and distribution. This is the universal formula for YBS project teams, with differences only in ratios and web packaging.

Next is the market. In an era of homogenized formulas, the market is essentially a handicraft, testing the aesthetics of project teams. It can only roughly outline four aspects: Pool strategies, rewards design, market volume, and vague strategies.

Let's start with the product. After Delta Neutral, it is merely a modified version of Ethena.

Products Without Distinction, Large Dividends on US Debt

Yield-bearing stablecoins differ from USDT's "historical stability." Year after year, FUD has instead created resilience. YBS requires a strong asset reserve, and the cycle of credit leverage models is difficult to cold start, so let’s explain briefly.

In the early stablecoin market, project teams could "claim" to have assets equivalent to 1 dollar, thus issuing a 1 dollar stablecoin, which would then be staked and circulated off-chain, leading to infinite cycles.

After the collapse of UST and FTX, the difficulty of such operations has increased significantly. Although there are still disconnections between on-chain and off-chain, in the context of increasingly mature real-name entrepreneurship and regulation, it can be assumed that most YBS project teams have relatively sufficient reserves.

YBS project teams prefer to use the credit leverage model of banks, i.e., a reserve system to cope with regulation, insufficient liquid funds to handle withdrawals, and the remainder is used for lending to earn interest. This is the fundamental reason why dollar / US debt has become the mainstream choice for YBS; only dollar / US debt can circulate seamlessly in Web2 and Web3, maximizing profit from yield combinations.

The GENIUS Act is not the beginning of regulation but a summary of past practices.

1. Underlying Assets

In terms of underlying asset selection, dollar / US debt is the mainstream choice. However, directly adopting MakerDAO/Sky's fundraising to buy US debt seems a bit crude. The market space left here is to help Web3's YBS project teams purchase real assets and assist Web2 financial giants in issuing compliant YBS.

For example, Compound's founder's new project SuperState not only helps DeFi's old money manage assets but also has one important business: USTB, compliant tokenization of US debt, with Resolv as its client.

Another example is Ondo, which has become closer to Wall Street since bringing in Kaite Wheeler, who previously worked at BlackRock and Circle. Wheeler was responsible for fixed income products for institutional clients at BlackRock, and at Ondo, he is in charge of institutional partnerships.

If we categorize the forms of using dollar / US debt, they can be divided into the following four types:

• US debt / dollar cash / dollar-related assets, case: Sky's USDS

• On-chain mainstream assets and their pegged forms, case: Resolv's USR

• USDT/USDC as underlying assets, case: Level's lvlUSD

• Alternative forms, such as GPU computing power tokenization GAIB

Among them, Resolv's BTC/ETH reserves represent a hypothetical state. Currently, it is still more closely related to USDC and US debt, just as Ethena initially envisioned using BTC but ultimately chose ETH; compromise is the norm.

On-chain mainstream assets, especially BTC/ETH/SOL, have made insufficient progress in YBS reserve monetization. It is important to note that Ethena's ETH hedging is a stability mechanism and does not completely align with reserves.

I believe that on-chain mainstream assets need to be more widely accepted by traditional financial markets to be directly used as reserves for YBS. We can observe from three angles: ETFs, national reserves, and (micro) strategies. On-chain stablecoins need to first gain off-chain recognition, which is quite darkly humorous.

The most interesting new forms like GAIB do not use a certain asset as reserves but rather a certain "utility." The essence of currency is a general equivalent, and the computing power in the AI era indeed has this characteristic, hoping to achieve some gains.

2. Minting Mechanism

In the previous text, the minting and yield process of YBS were conflated. However, the minting of YBS should specifically refer to the "issuance of stablecoins based on underlying assets," which should not involve subsequent yield mechanisms, redemptions, or other reverse operations.

Drawing on the CDP (Collateralized Debt Position) mechanism of lending products, we include all YBS under this scale, allowing for both positive and negative to accommodate YBS types with insufficient reserves.

Theoretically, unlike MakerDAO (DAI), Aave (GHO), and Curve (crvUSD), which commonly adopt an over-collateralization model, the new era of YBS generally adopts a 1:1 full collateralization, at least in terms of mechanism design. However, the reality of the situation is not for outsiders to know, which is also what YBSBarker hopes to penetrate.

Additionally, a few non-fully collateralized products generally adopt credit or guarantee mechanisms, making it difficult to become the mainstream choice in this cycle, so they will not be introduced.

3. Yield Sources

Based on underlying assets and minting mechanisms, we consider two dimensions of yield sources: yield mechanisms and stability, thus forming a complete process of minting, yielding, and redeeming yield-bearing stablecoins.

Taking Ethena as an example, the Delta mechanism consists of ETH spot and short positions for hedging. The hedging itself is the mechanism that ensures USDe is pegged 1:1 to the dollar, while the funding rate arbitrage from opening short positions is the source of yield, used to pay the returns to sUSDe holders.

Image description: Sources of yield

Image source: @zuoyeweb3

Ethena also chooses stETH and other ETH versions with built-in staking yields to enhance yield capture capability. The above describes the minting process of sUSDe and USDe, and we also need to consider the redemption process.

sUSDe reverts to USDe (unstaking) requires a 7-day cooling-off period before entering the withdrawal process, or it can be directly exchanged in real-time on DEX;

USDe reverts to ETH, with a T+7 restriction. Of course, USDe itself is a stablecoin and can be directly exchanged for any asset on CEX or DEX, but this is not the official asset redemption function provided.

Apart from Ethena, the remaining YBS projects are merely more diverse in yield scenarios and have improved asset value stabilization mechanisms. Slightly different is Avalon’s liquidation mechanism, which resembles traditional lending products more closely, used to control the price stability of stablecoins.

4. Yield Distribution

There are only two types of distribution mechanisms: one where value remains unchanged while quantity increases, and another where value increases while quantity remains unchanged:

• Value increases, quantity remains unchanged: Avalon, Falcon, Level, Noon, where sToken prices increase over time, allowing for the exchange of more stablecoins.

• Quantity increases, value remains unchanged: Resolv, where sToken quantities increase over time, but the price of sToken remains pegged 1:1 to its stablecoin.

Looking at the entire product mechanism design of YBS, there are two main difficulties. The first is the establishment of reserves. Other DeFi projects, such as DEX, operate under the AMM mechanism where adding liquidity is a user behavior. The DEX itself mainly focuses on technical development, product design, and market promotion, making it hard to say that self-funding is necessary to create a successful product.

YBS is inherently linked to "currency" as an asset or equivalent form. Insufficient capital reserves cannot gain user trust. In other words, people prefer to use YBS issued by wealthy individuals. In this regard, YBS naturally excludes ordinary entrepreneurs but is particularly suitable for large VCs to heavily invest in cultivating a second Ethena, a second Circle IPO, or a second USDT printing machine.

The second challenge is the source of yield. Referring to the history of quantitative finance, only those who are ahead of their peers can earn α returns. After that, one either learns to keep the secret of the grand prize like Simmons or competes in hardware and software resources, ultimately leading to the "law of large numbers," where capital scale overwhelms opponents, triggering systemic crises in a cyclical manner until the end of the world.

Yield Competition, High Volume and Intensity

Now that you have assembled an excellent YBS team, completed the project naming, front-end, back-end, and AI outsourcing for smart contracts, and successfully secured substantial funding from Big Name VCs, the next step is to attract large and retail investors to deposit funds and get the yield rates and scales running.

Then a major problem arises: yield rates and yield scales seem unable to coexist.

1. Pool Strategies

The most effective way for YBS to acquire customers is to offer high yield rates. However, as the capital scale increases, the stable high return rate will decrease. From A16Z's investment returns to BlackRock's asset management returns, the myth of Aave creating a thousand-fold return is merely a thing of the past.

YBS must find its own flywheel: providing users with more yield options. In simpler terms, it needs to seek out all possible yield-generating chains, protocols, and pools.

Three perspectives form around the yield of YBS:

• Coin-centric: The issuance data of stablecoins and sTokens themselves;

• Pool-centric: The usage and yield data of stablecoins and sTokens;

• Protocol-centric: The overall governance structure of stablecoins and sTokens.

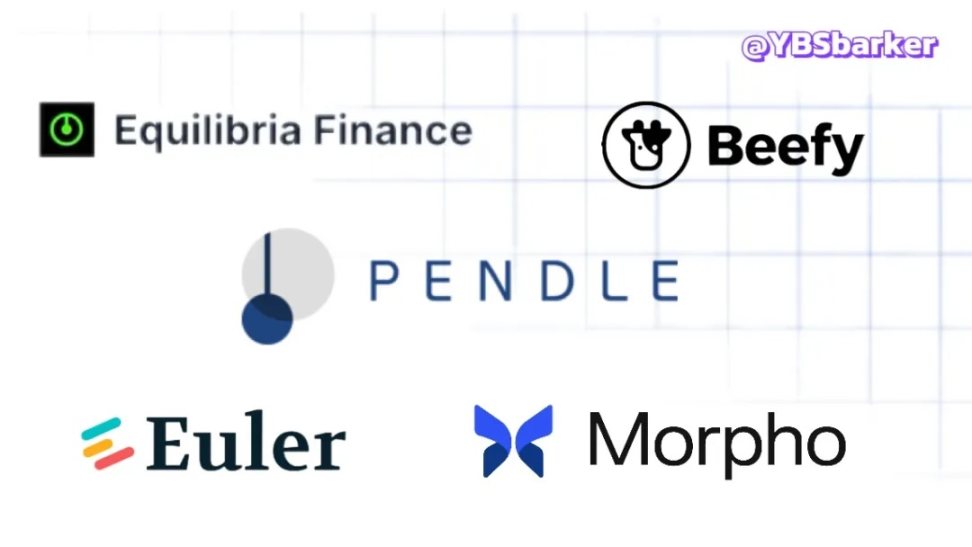

The levels of abstraction and complexity increase sequentially. The simplest perspective involves the issuance volume, staking volume, and holding addresses of USDe and sUSDe, which is coin-centric. Their trading pools in Pendle and Curve represent the pool-centric view, while the involvement of USDe, sUSDe, ENA, sENA, and protocol income, distribution mechanisms, and historical data is protocol-centric.

The coin-centric view is very intuitive, while the complexity of the pool-centric view lies in the accumulation of cross-chain, multi-protocol, and multi-pool interactions.

Image description: Protocols involved in YBS

Image source: @zuoyeweb3

Among them, Equilibria serves as Pendle's "bribery platform," allowing users to achieve the effect of collective staking ETH through Lido, reducing investment costs and increasing final gains.

Following this line of thought, the pool strategies exhibit three characteristics:

• Pendle and Amplifying Pendle's Yields: Pendle and Equilibria, similar to Curve and Convex;

• Aave and Morpho's lending mechanisms amplify yields, with specific pools and lending pairs of the Morpho model gradually gaining popularity;

• Replacing the old with the new: Pendle/Morpho/Euler are replacing the importance of older DeFi protocols like Curve and Uniswap for YBS.

Most importantly, Pendle has become the infrastructure of the YBS industry. Only by landing on Pendle can YBS take root on-chain, achieving a similar effect to USDC binding with Coinbase.

Flywheel Activation: More pools --> Larger capital capacity, more stable yields --> More users

2. Rewards System

The rewards system can be summarized simply, but it is exceptionally complex to implement. How to evaluate user behavior while balancing between anti-witchcraft and genuine customer acquisition is a challenge. Onekey and Infini have successively abandoned U card services, stemming from the uncontrollable profit model for C-end users.

The rewards in the YBS field are more like a Points battle. Some users want to earn investment returns, while others seek expected airdrops, trying to align their behaviors with reality.

• Deposit: Hodl time doubles points. USDf 6x

• Staking: Points are significantly fewer, Falcon USDf 1x

• Commission: The more people involved, the higher the commission

• Specific behaviors: Associated protocols, such as Resolv with 19 connections

However, the points system is not synonymous with airdrops and tokens. Under the usual "off-chain calculation, front-end display" model, whether one can receive Farm rewards as expected is left to fate.

3. Market Volume

The success of Ethena certainly stems from its excellent design, but it cannot be separated from the support of Arthur Hayes himself. Referring to past successful cases, three models can be summarized:

• User outreach: KOL + media, whose effectiveness is diminishing, becoming closer to routine actions.

• Off-chain legitimacy: USD1 backed by Trump, large enterprises like JD.com and Walmart.

• Big Name: Arthur Hayes serves as a personal endorsement for Ethena.

Regarding market volume, I feel my understanding is not quite adequate. If any readers have thoughts, feel free to share in the comments.

### 4. Vague Strategies

APR vs. APY, both simple and compound interest are vague financial indicators, and potential crises can also create credit leverage.

• Falcon has off-chain assets participating in yield calculations, where theoretical optimality and practice do not fully align;

• Even for the same indicator, there are differences in calculation periods. For example, Falcon uses a 7-day period, Level uses a 1-year period, and Noon has not yet announced its period.

Even if the calculation methods are the same, the off-chain components of each YBS will also participate in the calculations, such as CEX's opening order data or foundations, audits, etc., which are all black boxes that cannot be tracked in real-time. There is significant operational space in these details.

The YBS market remains a battleground for yield data, and the specific strategies employed require proactive discovery by users to amplify yield rates and participate in this gold rush.

Conclusion

The less demand there is, the closer it is to divinity.

The surface of YBS is incredibly simple, with a 1:1 peg to the dollar providing lasting security, but the underlying complexities are immense.

For the general public, involving savings and lending has always been a social and political event, as is the case in both the East and the West. Based on this, we delve into the internal workings of YBS, explaining the basic characteristics of a healthy project from the perspective of project teams. Entrepreneurship is challenging; how many of the 100 YBS projects will survive?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。