Unlike the previous cycle, this time it will be built on business fundamentals rather than token mechanisms.

Author: Thejaswini M A

Article compiled by: Block unicorn

Introduction

I used to get excited about every funding announcement in cryptocurrency.

Every seed round financing felt like major news. “Anonymous team raises $5 million for revolutionary DeFi protocol!”

I would frantically research the founders, dive into their Discord, trying to understand what was special about the project.

Fast forward to 2025. Another round of financing appears in my news headlines. Series A funding. $36 million. Stablecoin payment infrastructure.

I categorize it under “enterprise blockchain solutions” and then move on to other things.

When did I become so… pragmatic?

Since 2020, late-stage deals in cryptocurrency venture capital have outpaced early-stage deals for the first time.

65% to 35%.

Read that again.

The industry used to be built on seed round pre-financing, with anonymous teams innovating DeFi protocols in garages.

Now? Series A and beyond financing is driving the flow of funds.

What has changed?

Everything has changed. And yet, it seems like nothing has changed.

Crypto Venture Capital

Suit-wearing VCs. Due diligence has gone from minutes to months.

Regulatory compliance. Institutional adoption.

Professional project pitches instead of anonymous Discord messages.

KYC processes. Legal teams. Real revenue models.

Companies like Conduit raised $36 million for “unified on-chain payments.” Beam raised $7 million for “stablecoin-based payment services.”

These are infrastructure projects. B2B solutions. Enterprise-grade platforms.

Boring, profitable, scalable businesses.

Headlines in cryptocurrency venture capital always love to exaggerate the numbers, so let’s start with the facts:

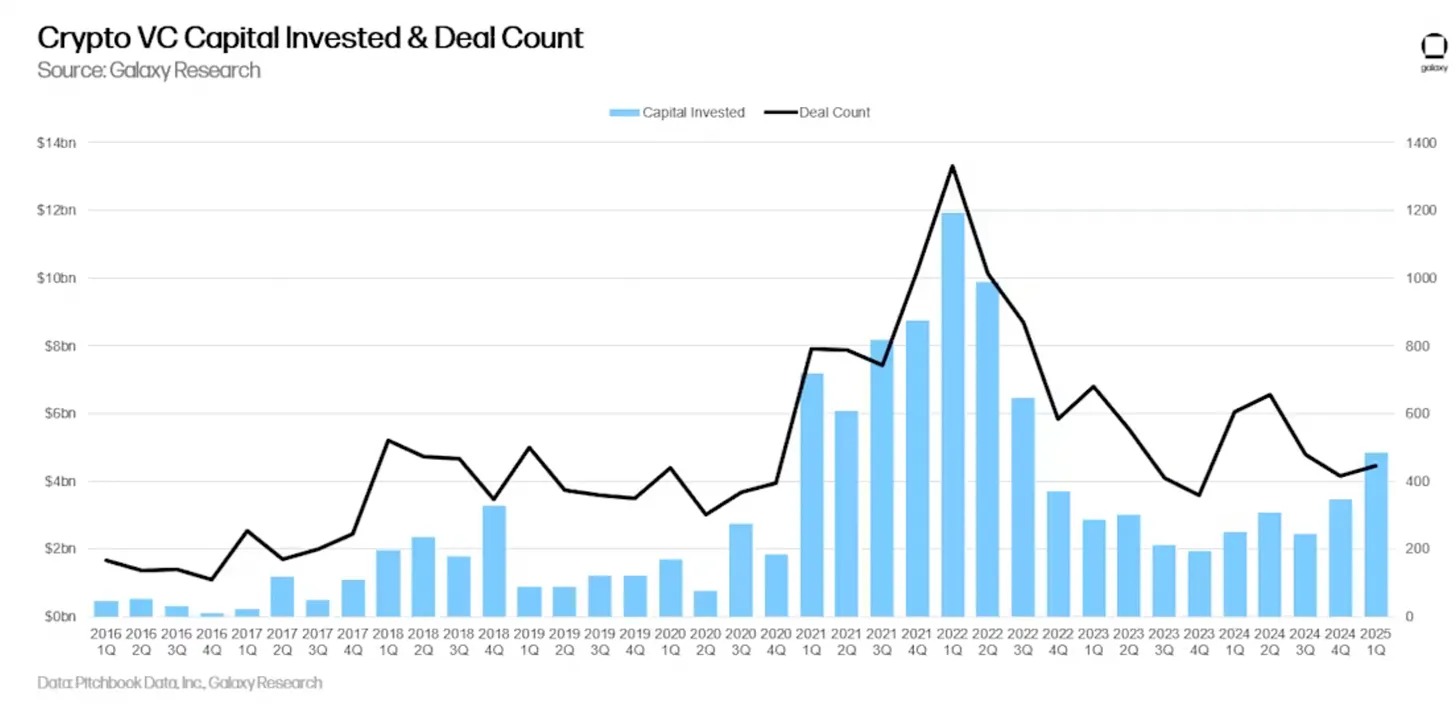

Q1 2025: 446 deals totaling $4.9 billion (up 40% quarter-over-quarter).

Year-to-date: A total of $7.7 billion raised, with 2025 expected to reach $18 billion.

And the issue is: MGX (Abu Dhabi sovereign fund) wrote a $2 billion check to Binance.

This perfectly reflects the current venture capital environment: a few large deals distort the data while the overall ecosystem remains sluggish.

According to Galaxy Research, the correlation between Bitcoin prices and venture capital activity—reliable for years—broke in 2023 and has yet to recover.

Bitcoin hit new highs while venture capital activity remained sluggish. It turns out that when institutions can buy Bitcoin ETFs, they don’t need to fund risky startups to gain exposure to cryptocurrency.

Reality Check for Venture Capital

Cryptocurrency venture capital has dropped 70% from its peak of $23 billion in 2022 to just $6 billion in 2024.

The number of deals plummeted from 941 in Q1 2022 to 182 in Q1 2025.

But this should terrify every founder claiming “the next big event”—only 17% of the 7,650 companies that raised seed rounds since 2017 have made it to Series A.

And only 1% have reached Series C.

This is the maturation process of cryptocurrency venture capital, and it will be painful for those who thought the feast would last forever.

Category Rotation

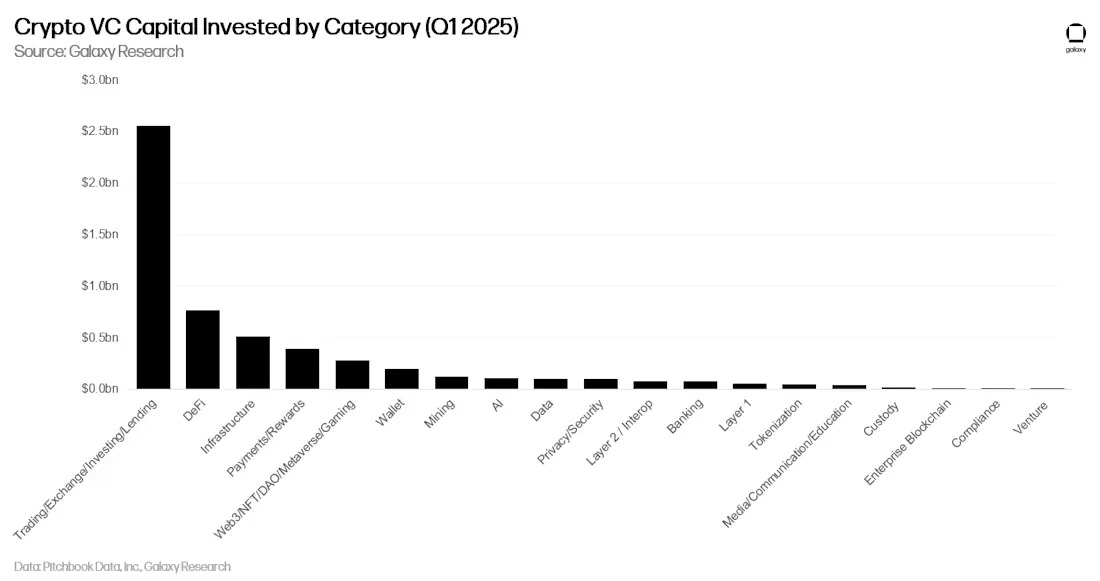

The hot narratives of 2021-2022—gaming, NFTs, DAOs—have almost disappeared from venture capital interest.

In Q1 2025, companies building deals and infrastructure attracted most of the venture capital. DeFi protocols raised $763 million. Meanwhile, the categories that once dominated deal numbers—Web3/NFT/DAO/gaming—have slipped to fourth place in capital allocation.

This shows that venture capital is finally placing revenue-generating businesses above narrative-driven speculation.

Infrastructure that truly drives cryptocurrency transactions is getting funded.

Applications that people actually use are getting funded.

Protocols that generate real fees are getting funded.

And everything else will increasingly lack capital.

Artificial intelligence has also become a major competitor for venture capital.

Why bet on crypto gaming when you can bet on AI applications with clearer revenue paths? The opportunity cost for crypto-native applications has significantly shifted against projects that cannot demonstrate immediate utility.

Graduation Crisis

Let’s dig into the most thought-provoking statistic from the data: the graduation rate from seed round to Series A in cryptocurrency is 17%.

This means that for every six companies that raise a seed round, five will never receive meaningful follow-on funding.

In contrast, about 25-30% of seed round companies in the traditional tech industry reach Series A, and you start to understand the severity of the problem.

The success metrics for cryptocurrency have always had fundamental flaws.

Why? Because for years, the script for cryptocurrency has been simple: raise venture capital, build something that looks innovative, launch a token, and let retail investors provide exit liquidity. VCs didn’t need companies to truly graduate through funding rounds because the public market would provide them with a lifeline.

That safety net has disappeared. Most tokens issued in 2024 are trading at only a fraction of their initial valuations. EigenLayer’s EIGEN was issued at a fully diluted valuation of $6.5 billion and has since dropped 80%. Projects with monthly revenues exceeding $1 million are few and far between.

As the path to token listing comes to an end, the true graduation rates are gradually becoming apparent. And the results are not optimistic. What’s the outcome? The questions venture capitalists are now asking are the same ones traditional investors have been asking for decades: “How do you make money?” and “When will you be profitable?” This is clearly a revolutionary concept in the cryptocurrency space.

Centralization Takeover

While the number of deals has significantly decreased, the deal sizes have undergone an interesting change. Since 2022, the median seed round has significantly increased, even though the overall number of companies raising funds has decreased.

This indicates that an industry is consolidating around fewer, larger bets. The “spray and pray” seed investment era is over.

The message to founders is clear: if you’re not in the core circle, you may not get funding. If you haven’t secured financing from top funds, your chances of obtaining follow-on funding will significantly decrease.

This centralization is not limited to funding.

Data shows that 44% of the companies in the A16z portfolio have A16z participating in their follow-on rounds.

For Blockchain Capital, this figure is 25%. The best funds are not only picking winners but actively ensuring that their portfolio companies continue to receive funding.

Our Perspective

We have all witnessed the shift from “revolutionary DeFi protocols” to “enterprise blockchain solutions.”

Honestly? I’m conflicted.

Part of me misses that chaos. The wild volatility. Those anonymous teams with Discord nicknames raising millions for ideas that sounded like fever dreams.

There was a purity in that madness. Just builders and believers betting on a future that traditional finance couldn’t even imagine.

But another part of me—the part that has witnessed too many promising projects fail due to lack of fundamentals—knows that this adjustment is inevitable.

For years, cryptocurrency venture capital has operated in a fundamentally flawed manner. Startups could raise funds solely based on white papers, launch tokens to retail investors for liquidity, and then call it a success regardless of whether they built what users truly wanted.

What’s the result? An ecosystem optimized for hype cycles rather than value creation.

Now, the industry is undergoing a long-overdue shift from speculation to substance.

The market is finally beginning to apply the performance standards that should have existed from the start. When only 17% of seed round companies make it to Series A funding—this means market efficiency has finally caught up with an industry that was once artificially supported by excessive narrative.

This brings both challenges and opportunities. For founders accustomed to raising funds based on token potential rather than business fundamentals, the new reality is harsh. You need users, revenue, and a clear path to profitability.

But for those building solutions to real problems and genuine businesses, the environment has never been better. Competition for funding has decreased, investors are more focused, and success metrics are clearer.

“Tourist capital” has left, leaving behind the substantial funding that true startups need. The remaining institutional investors are not looking for the next “meme coin” or speculative infrastructure investment.

Founders and investors who survive this transformation will build the infrastructure for the next chapter of cryptocurrency. Unlike the previous cycle, this time it will be built on business fundamentals rather than token mechanisms.

The gold rush is over. The mining operation has just begun.

Although I said I missed that chaos? This is exactly what cryptocurrency needs.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。