This is an era of strategic exits.

Written by: Saurabh Deshpande

Translated by: Luffy, Foresight News

Coinbase has acquired Deribit for $2.9 billion, marking the largest merger and acquisition event in cryptocurrency history.

The same is true in the tech sector. To date, Google has acquired 261 companies. These acquisitions have given rise to products such as Google Maps, Google AdSense, and Google Analytics. Perhaps the most significant was Google's acquisition of YouTube for $1.65 billion in 2020. In the first quarter of 2025, YouTube generated $8.9 billion in revenue, accounting for 10% of Alphabet's (Google's parent company) total revenue. Similarly, Meta has conducted 101 acquisitions to date, with Instagram, WhatsApp, and Oculus being prominent examples. Instagram generated over $65 billion in annual revenue in 2024, accounting for over 40% of Meta's total business revenue.

To buy off-the-shelf or to build it yourself?

The cryptocurrency industry is no longer a new sector. It is estimated that the number of cryptocurrency users has reached 659 million, with Coinbase having over 105 million users, while the global internet user base is about 5.5 billion. Therefore, the number of cryptocurrency users has reached 10% of the total number of internet users. These numbers are significant as they help us identify the sources of growth for the next phase.

The increase in user numbers is an obvious way to grow. Currently, we have only developed use cases for cryptocurrency in the financial sector. If other applications use blockchain technology as infrastructure, the entire market size will expand significantly. Acquiring existing users, cross-selling, and increasing revenue per user are some ways for existing companies to achieve growth.

When the pendulum swings towards acquisition

Acquisitions address three key issues that pure financing cannot solve. First, in a highly specialized field where experienced developers are scarce, acquisitions help with talent acquisition. Second, in an environment where the cost of natural growth is increasingly high, acquisitions assist in user acquisition. Third, acquisitions can facilitate technology integration, allowing protocols to transcend their original use cases. These issues will be further explored in conjunction with industry cases later.

We are in a new wave of mergers and acquisitions in the cryptocurrency space. Coinbase has acquired Deribit for a record $2.9 billion; Kraken has acquired the retail futures trading platform NinjaTrader, regulated by the U.S. Commodity Futures Trading Commission (CFTC), for $1.5 billion; Ripple has acquired multi-asset prime broker Hidden Road for $1.25 billion and had previously bid to acquire Circle but was rejected.

These transactions reflect the changing priorities in the field. Ripple seeks distribution and regulatory channels, Coinbase pursues options trading volume, and Kraken is filling product gaps. These acquisitions stem from strategic, survival, and competitive positioning.

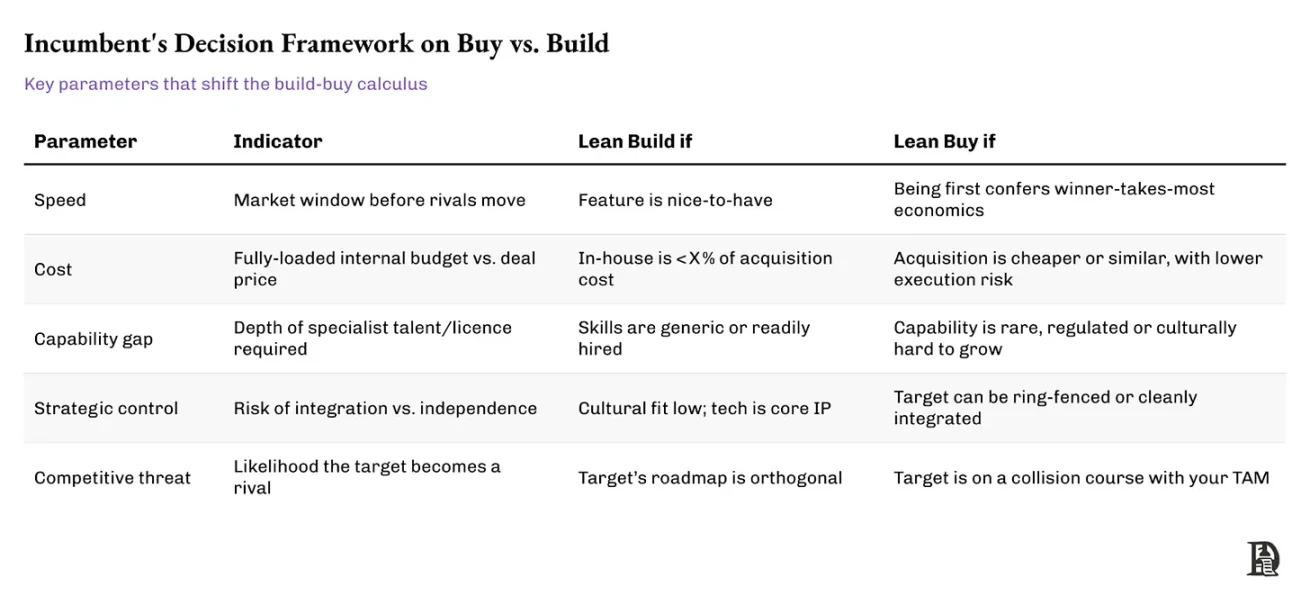

The table below can help you understand the considerations existing companies have when deciding whether to build or acquire.

While the table summarizes the key trade-offs in the build versus buy decision, existing companies often rely on unique signals when taking decisive action. A good example is Stripe's acquisition of Nigeria's Paystack in 2020. Building infrastructure in Africa means facing steep learning curves regarding regulatory details, local integration, and merchant onboarding.

Stripe chose to acquire. Paystack had already addressed local compliance issues, built a merchant base, and proven its distribution capabilities. Stripe's acquisition met multiple criteria, such as speed (gaining first-mover advantage in a growing market), capability gaps (local expertise), and competitive threats (Paystack becoming a regional competitor). This move accelerated Stripe's global expansion without diverting attention from its core business.

Before we delve into the reasons behind these transactions, two questions are worth considering: first, why should founders consider being acquired; and second, why is now an important time to consider this issue?

Successful acquisitions can be a booster

Why is the current macro environment favorable for acquisitions?

For some, it is about liquidity at the time of exit. For others, it is about accessing more sustainable distribution channels, ensuring long-term growth, or becoming part of a platform that can amplify influence. For many, it is a way to avoid the increasingly narrow path of venture capital, which is now scarcer than ever, with higher investor expectations and more urgency.

A rising tide does not lift all boats

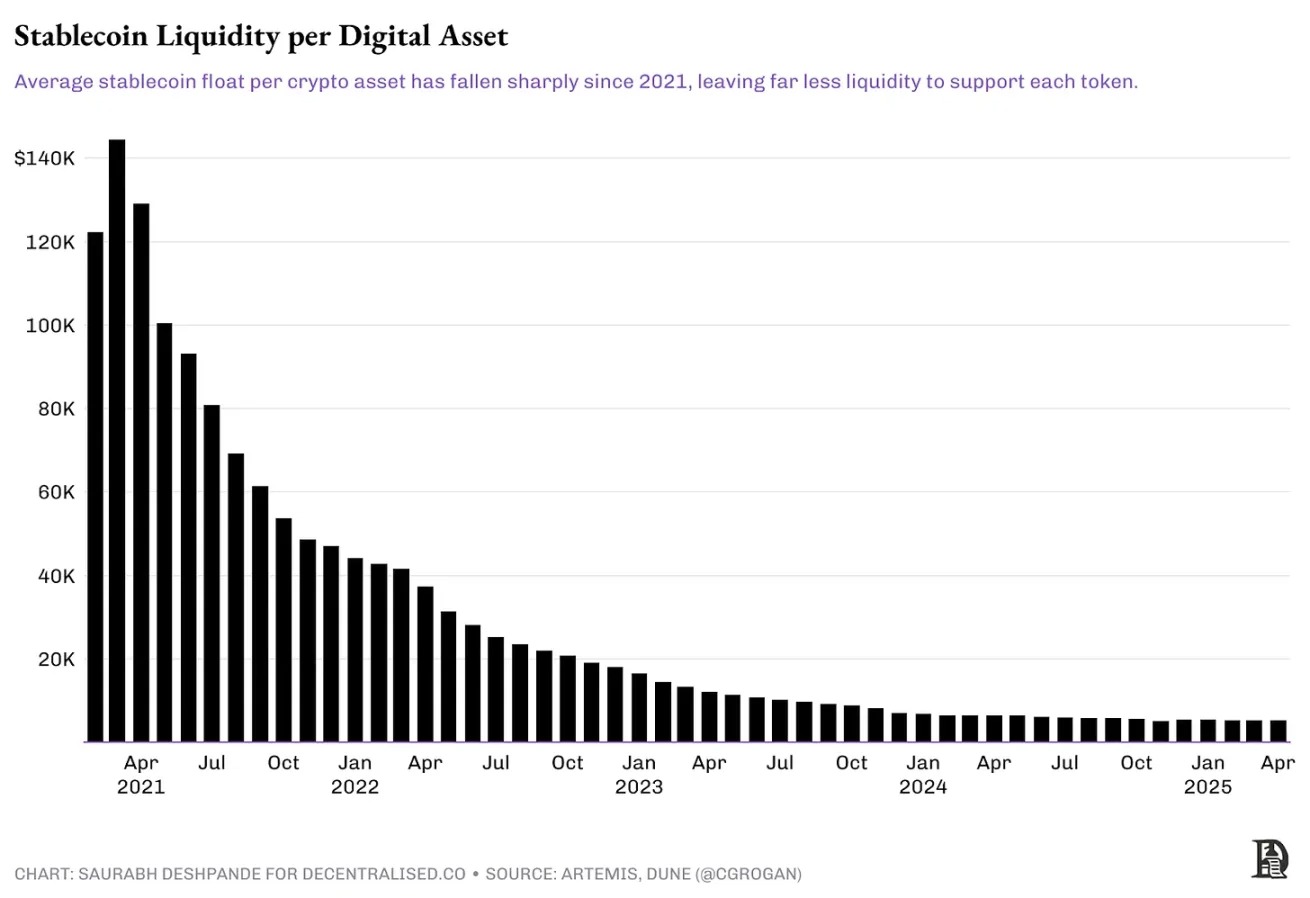

The venture capital market lags behind the liquidity market by several quarters. Typically, whenever Bitcoin prices peak, venture capital activity takes months or quarters to cool down. Venture capital in the cryptocurrency space has declined by over 70% since its peak in 2021, with median valuations returning to levels seen in 2019-2020. I believe this is not a temporary pullback.

Let me explain why. In short, venture capital returns have declined while the cost of capital has risen. As a result, with higher opportunity costs, the amount of venture capital chasing deals has decreased. However, from the unique perspective of the cryptocurrency space, the market structure has been affected by a significant increase in the number of assets. I have been keeping an eye on this chart, and most token businesses should be aware of it. Just because creating new tokens is easy does not mean it is wise to issue them. Capital on the internet is limited. With each new asset issued, the liquidity chasing it decreases, as shown in the chart below.

Every venture-backed token launched with a high fully diluted valuation (FDV) requires substantial liquidity to reach a multi-billion dollar market cap. For example, EigenLayer's EIGEN token launched at $3.9, with a fully diluted valuation of $6.5 billion. The circulating supply at launch was about 11%, with a market cap of approximately $720 million. The current circulating supply is about 15%, with a fully diluted valuation of around $1.4 billion. After multiple rounds of unlocking, 4% of the supply has entered circulation since the token's initial issuance. Since its launch, the token's price has dropped by about 80%. To return to its issuance valuation, the price would need to increase by 400% with the increase in supply.

Unless the token can genuinely accumulate value, market participants have no reason to chase these tokens, especially in a market with many investment options. Most of these tokens are unlikely to ever reach their initial valuations again. I checked the 30-day revenue data for all projects on Token Terminal, and only three projects (Tether, Tron, and Circle) had monthly revenues exceeding $1 million. Only 14 projects had monthly revenues exceeding $100,000. Among these 14 projects, 8 have tokens, meaning they have investment value.

This means individual investors are either unable to exit or must exit at a discount. The overall poor performance of the secondary market puts pressure on venture capital investment returns. This will lead to more cautious investment strategies. Therefore, products must either find product-market fit (PMF) or be something we have not yet tried to attract investors and achieve valuation premiums. A product with only a minimum viable product (MVP) and no users will struggle to find investors. So, if you are building another "blockchain scaling layer," your chances of attracting top investors are very low.

We have seen this situation unfold. As mentioned in our article on the Venture Funding Tracker, monthly venture capital inflows into the cryptocurrency space have dropped from a peak of $23 billion in 2022 to $6 billion in 2024. The total number of funding rounds has decreased from 941 in Q1 2022 to 182 in Q1 2025, indicating a cautious attitude towards venture capital funding.

Why now?

So what happens next? Acquisitions may make more sense than a new round of financing. Protocols or businesses that already have some revenue will pursue niche markets that can fill their blind spots. The current environment is prompting teams to move towards consolidation. Higher interest rates make capital expensive; user adoption rates are stabilizing, making natural growth more difficult; the effects of token incentives are not as strong as before; meanwhile, regulation is forcing teams to specialize more quickly. All these factors are driving the cryptocurrency space to view acquisitions as a means of growth. This time, mergers and acquisitions in the cryptocurrency space seem to be more thoughtful and concentrated than in previous cycles. We will explore the reasons for this later.

M&A Cycle

Historically, the traditional financial sector has experienced five to six major waves of mergers and acquisitions, triggered by factors such as deregulation, economic expansion, cheap capital, or technological change. The early waves were driven by vertical integration and monopoly ambitions; later waves emphasized synergies, diversification, or global influence. We do not need to delve into a century-long history of mergers and acquisitions; simply put: when growth slows and capital is abundant, consolidation accelerates.

Source: Harvard Law School Forum on Corporate Governance

How can we explain the different stages of mergers and acquisitions in the cryptocurrency space? It resembles what we have seen in traditional markets over decades. The growth of emerging industries is often wave-like rather than linear. Each wave of mergers and acquisitions reflects different demands along the industry maturity curve: from building products, to finding product-market fit, to acquiring users, and locking in distribution channels, compliance, or defensive capabilities.

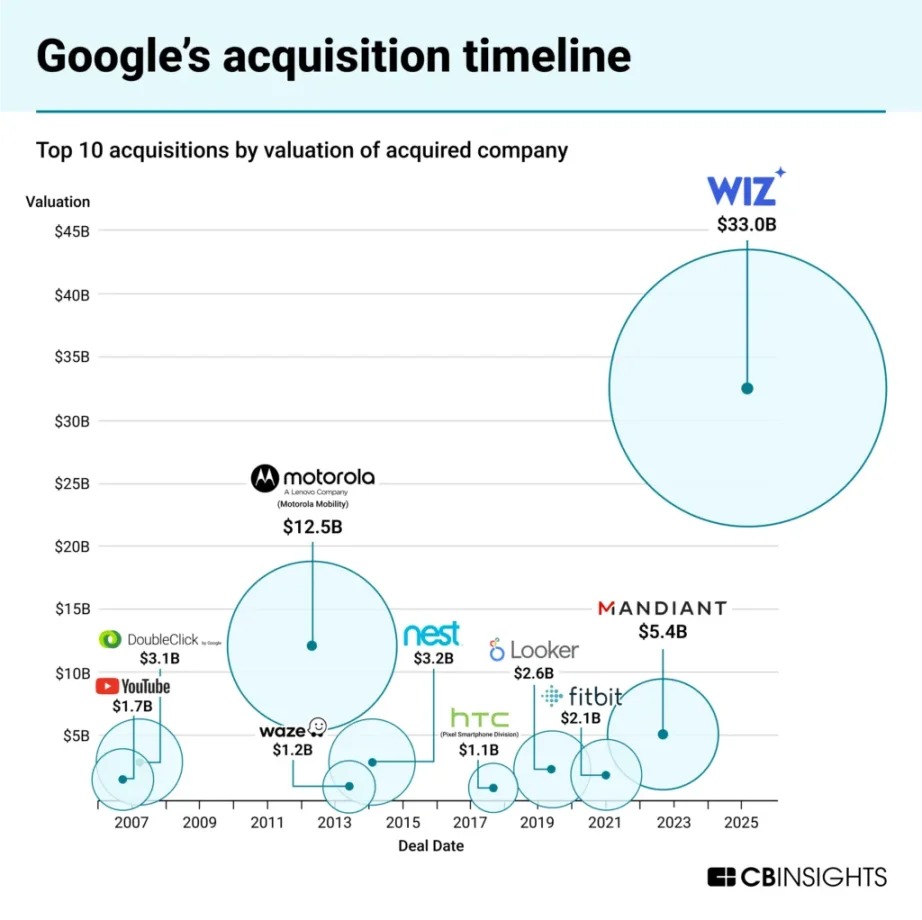

Source: CBInsights

We have seen this situation in both the early internet era and the mobile internet era. Recall that in mid-2005, Google acquired the Android operating system. This was a strategic bet that mobile devices would become the dominant computing platform. According to "Androids: The Team That Built the Android Operating System" by Chet Haase, a veteran engineer at Google:

In 2004, global personal computer shipments were 178 million units. During the same period, mobile phone shipments were 675 million units, nearly four times the number of personal computers, but their processor and memory performance was comparable to that of personal computers from 1998.

The mobile operating system market was once fragmented and constrained. Microsoft charged licensing fees for Windows Mobile, the Symbian system was primarily used on Nokia devices, and BlackBerry's operating system only ran on its own devices. This created strategic opportunities for the development of open platforms.

Google seized this opportunity by acquiring a free open-source operating system that manufacturers could adopt without paying expensive licensing fees or building their own operating systems from scratch. This democratization allowed hardware manufacturers to focus on their strengths while accessing a complex platform that could compete with Apple's tightly controlled iOS ecosystem. Google could have built an operating system from scratch, but acquiring Android allowed it to gain a first-mover advantage and helped counter Apple's growing dominance. Twenty years later, 63% of web traffic comes from mobile devices, with 70% of mobile web traffic generated by the Android system. Google foresaw the shift from personal computers to mobile devices, and acquiring Android also helped Google dominate the mobile search space.

The 2010s were dominated by cloud infrastructure-related deals. Microsoft acquired LinkedIn for $26 billion in 2016, aiming to integrate identity information and professional data across Office, Azure, and Dynamics. Amazon acquired Annapurna Labs in 2015 to build its own custom chips and provide edge computing capabilities for AWS, indicating that vertical integration of infrastructure was becoming crucial.

The emergence of these cycles is due to the different limiting factors that each stage of industry development brings. Initially, the key was the speed of product launches. Later, the focus shifted to user acquisition. Ultimately, clarity in regulation, scalability, and durability became critical. Acquisitions are a way for industry winners to compress time; they buy licenses instead of applying for them, acquire teams instead of hiring, and purchase infrastructure instead of building from scratch.

Thus, the pace of mergers and acquisitions in the cryptocurrency space mirrors that of traditional markets. The technology may differ, but the common sense remains the same.

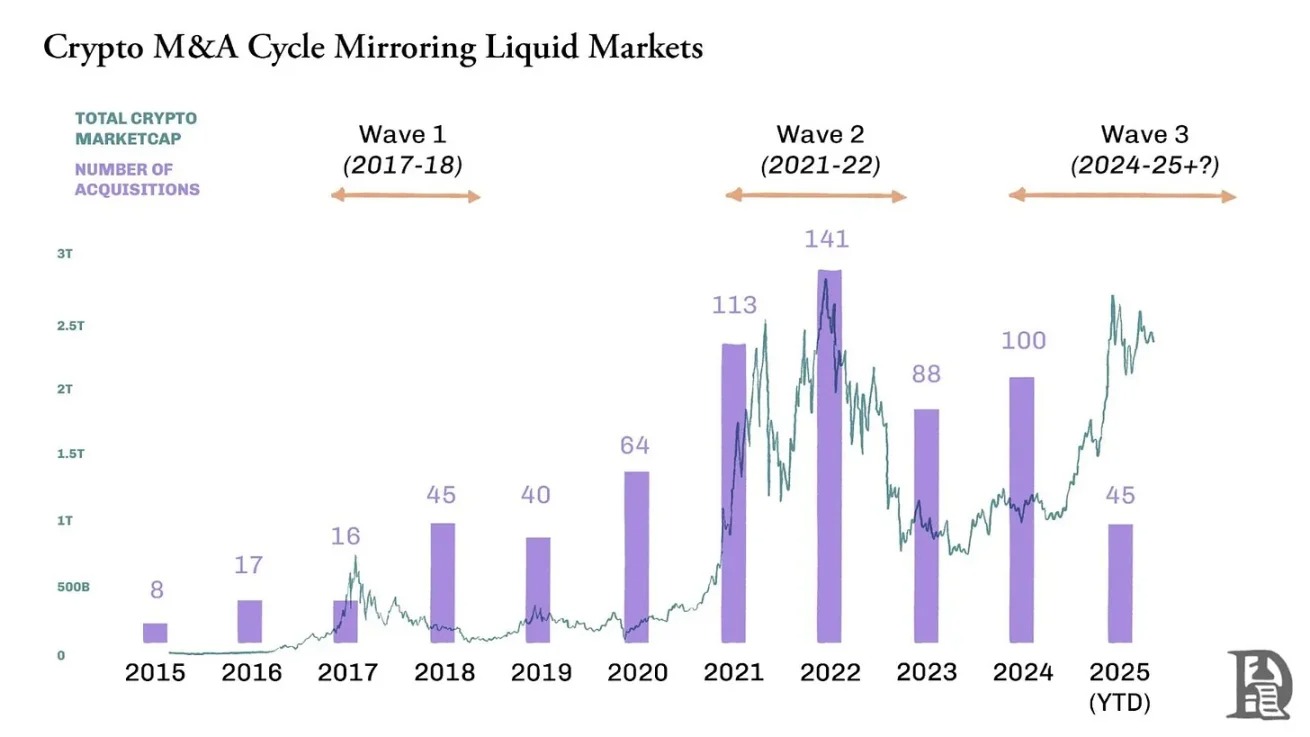

Three Waves of Mergers and Acquisitions in Cryptocurrency

Upon reflection, the mergers and acquisitions in the cryptocurrency space have gone through three distinct phases. Each phase is determined by the market demands and technological conditions of the time.

First Wave (2017-2018) — The ICO Boom: Smart contract platforms were just emerging, and there was no decentralized finance (DeFi) yet; people only hoped to build on-chain applications that could attract users. Exchanges and wallets acquired smaller front-end platforms to attract new token holders. Notable deals from this era include Binance's acquisition of Trust Wallet and Coinbase's acquisition of Earn.com.

Second Wave (2020-2022) — Fund-Driven Acquisitions: Protocols like Uniswap, Matic (now Polygon), and Yearn Finance, as well as companies like Binance, FTX, and Coinbase, had found product-market fit (PMF). During the bull market of 2021, their market capitalizations soared, and the valuations of the tokens they held were inflated, providing them with spending power. Decentralized autonomous organizations (DAOs) of protocols used governance tokens to acquire relevant teams and technologies. Yearn's acquisition spree, OpenSea's acquisition of Dharma, and the frenzied acquisitions by FTX before its collapse (such as LedgerX and Liquid) defined this era. Polygon also undertook ambitious acquisitions, acquiring teams like Hermez (a zero-knowledge proof scaling solution) and Mir (zero-knowledge technology) to establish its leadership in the zero-knowledge scaling space.

Third Wave (2024 to Present) — Compliance and Scalability Phase: In an environment of tightening venture capital and clearer regulations, well-funded companies are acquiring teams that can bring regulated venues, payment infrastructure, zero-knowledge technology talent, and account abstraction primitives. Recent examples include Coinbase's acquisition of BRD Wallet to strengthen its mobile wallet strategy and user onboarding, as well as its acquisition of FairX to accelerate its push into the derivatives space.

Robinhood's acquisition of Bitstamp aims to expand its business into other regions. Bitstamp holds over 50 valid licenses and registrations globally, which will bring Robinhood customers from the EU, UK, US, and Asia. Stripe acquired OpenNode to deepen its cryptocurrency payment infrastructure.

Why Do Acquirers Acquire?

Some startups are acquired for strategic reasons. When an acquirer initiates a deal, they typically hope to accelerate their own roadmap, eliminate competitive threats, or expand into new user groups, technological areas, or regions.

For founders, becoming an acquisition target is not just about obtaining returns; more importantly, it is about achieving scale expansion and business continuity. A well-planned acquisition can provide teams with greater distribution channels, long-term resource support, and the ability to integrate products into the broader ecosystem they are trying to improve. Rather than struggling for the next round of financing or pivoting to catch the next wave, becoming an acquisition target may be the most effective way to realize the original mission of the startup.

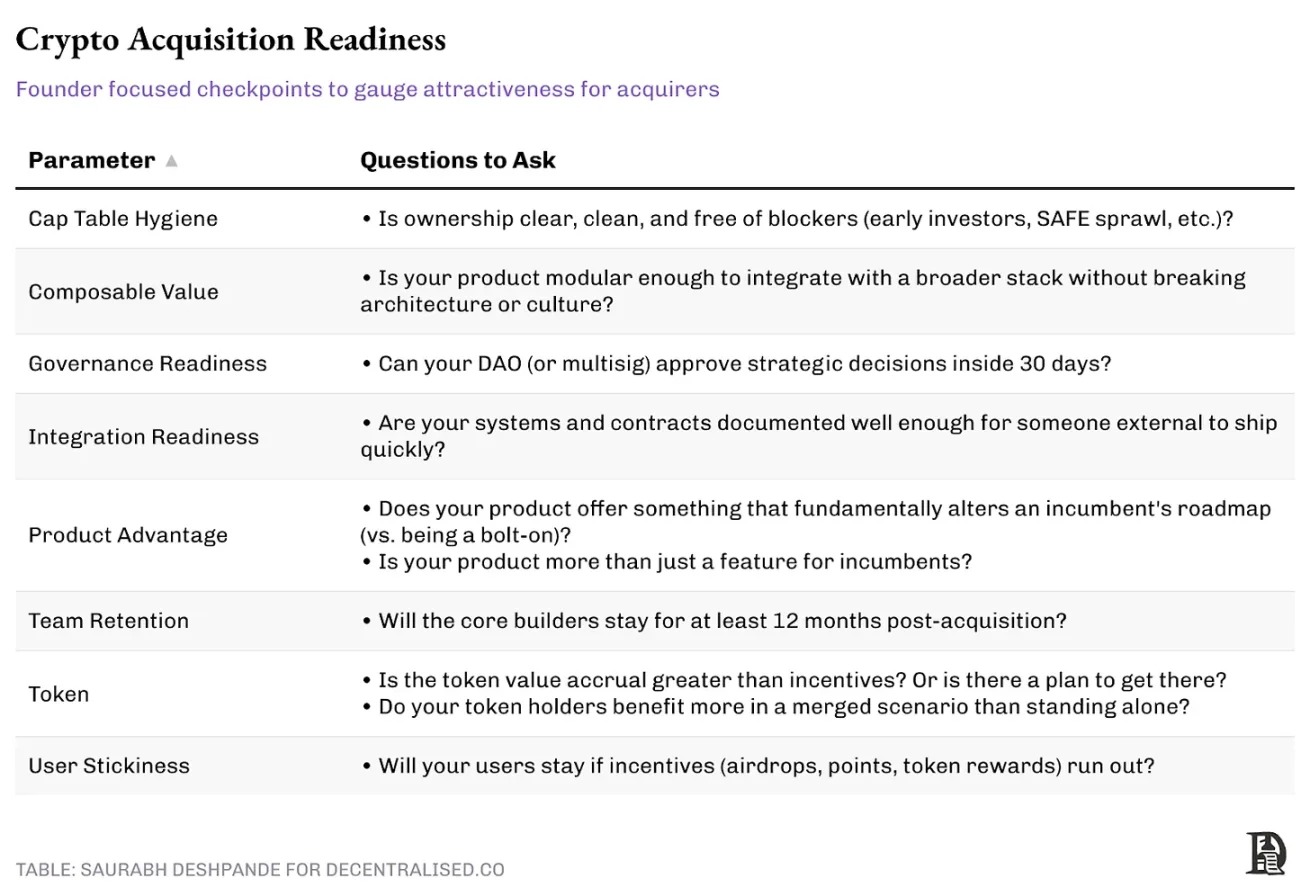

Here is a framework to help you assess how far your startup is from becoming the "right acquisition target." Whether you are actively considering an acquisition path or just keeping the possibility of being acquired in mind while building your business, excelling in these parameters will significantly increase your chances of being noticed by the right acquirer.

Four Models of Cryptocurrency Acquisitions

In studying significant transactions over the past few years, we have identified some clear patterns in the structure and execution of these acquisitions. Each model represents a different strategic focus:

1. Talent Acquisition

Vibe coding has emerged, but teams need skilled coders who can build products without relying on artificial intelligence. We have not yet reached a point where AI can write code and be trusted with millions of dollars in funding. Therefore, acquiring small startups for talent before they become a threat is indeed a reasonable reason for existing companies to acquire startups.

But from an economic perspective, why is talent acquisition reasonable? First, acquirers often gain relevant intellectual property, ongoing product lines, and existing user bases and distribution channels. For example, when ConsenSys acquired Truffle Suite in 2020, it not only absorbed a developer tool team but also acquired key intellectual property, such as Truffle's development tool suite, including Truffle Boxes, Ganache, and Drizzle.

Second, talent acquisition allows existing companies to quickly integrate specialized teams, and the costs are often lower than building a team from scratch in a competitive talent market. As far as I know, there were only about 500 engineers in 2021 who truly understood zero-knowledge technology. This is why Polygon's acquisition of Mir Protocol for $400 million and Hermez Network for $250 million makes sense. Assuming these talents could be acquired, hiring these zero-knowledge cryptographers individually could take years.

In contrast, these acquisitions brought elite zero-knowledge researchers and engineers into Polygon's team overnight, significantly simplifying the hiring and onboarding process. Compared to the total costs of hiring, training, and personnel growth time, this acquisition is economically efficient, especially when the acquired team is already launching products.

When Coinbase acquired Agara for $40-50 million at the end of 2021, the deal was more about acquiring engineering talent than customer service automation. The team in India had deep expertise in artificial intelligence and natural language processing. After the acquisition, many of these engineers were integrated into Coinbase's product and machine learning teams to support its broader AI initiatives.

While these acquisitions were framed around technology, the real asset was the talent: engineers, cryptographers, and protocol designers who could realize Polygon's vision for a zero-knowledge future. Although the full integration and productization of these teams took longer than expected, these acquisitions provided Polygon with a deep reservoir of zero-knowledge technical talent, a resource advantage that continues to shape its competitive strategy.

2. Capability / Ecosystem Expansion

Some strategic acquisitions focus on expanding ecosystem coverage or internal capabilities. The positioning and market visibility of the acquiring company often help achieve this goal.

Coinbase is a great example of expanding capabilities through acquisitions. It acquired Xapo in 2019 to expand its custody business. This laid the foundation for Coinbase Custody, providing secure and compliant storage solutions for digital assets. The acquisition of Tagomi in 2020 led to the launch of Coinbase Prime, a comprehensive suite of institutional trading and custody services. The acquisition of FairX in 2022 and Deribit in 2025 further helped Coinbase solidify its position in the U.S. and global derivatives markets.

For example, Jupiter's acquisition of Drip Haus in early 2025. Jupiter is a leading decentralized trading aggregator on Solana, aiming to expand from the decentralized finance (DeFi) space into the non-fungible token (NFT) space. Drip Haus established a highly engaged on-chain audience by providing free NFT collectible distribution services for creators on Solana.

Because Jupiter is closely connected to Solana's infrastructure and developer ecosystem, it has unique insights into which cultural products are gaining attention. It views Drip Haus as a key attention hub, especially within the creator community.

By acquiring Drip Haus, Jupiter has gained a foothold in the creator economy and community-driven NFT distribution. This move enables it to extend NFT functionalities to a broader audience and offer NFTs as incentives to traders and liquidity providers. It is not just about collectibles; it involves controlling the NFT channels that capture Solana's native attention. This expansion of the ecosystem marks Jupiter's first foray into the cultural and content space, an area where it previously had no business. This is very similar to how Coinbase systematically built its custody, prime brokerage, derivatives, and asset management capabilities through acquisitions.

Source: Bloomberg

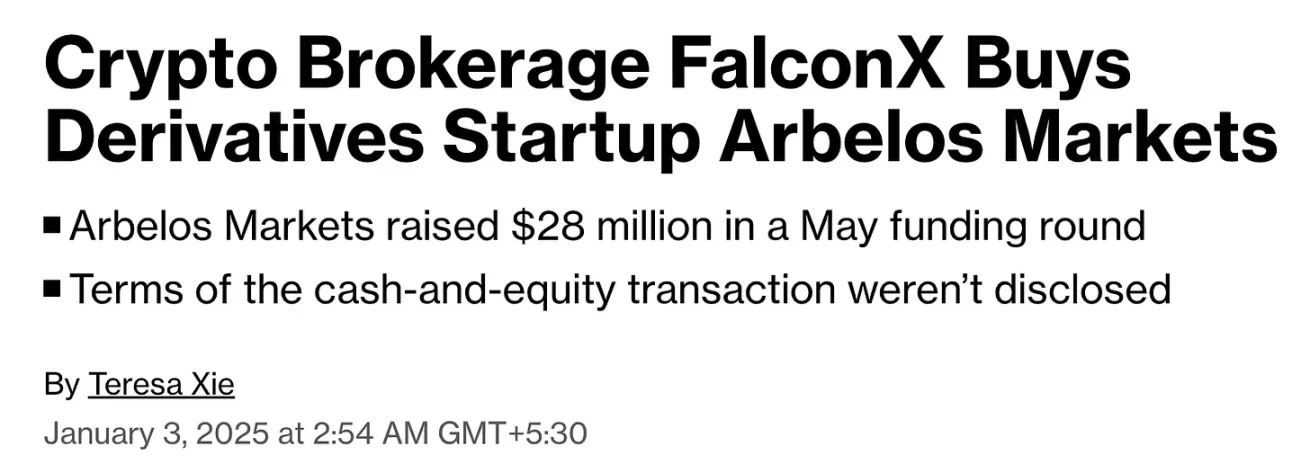

Another example is FalconX's acquisition of Arbelos Markets in April 2025. Arbelos is a specialized trading firm known for its expertise in structured derivatives and risk warehousing. These capabilities are crucial for serving institutional clients. As a leading broker for institutional cryptocurrency funds, FalconX understands the derivative trading volume through Arbelos. This may have led it to believe that Arbelos was a high-value acquisition target.

By incorporating Arbelos, FalconX enhanced its ability to price, hedge, and manage risks associated with complex crypto instruments. This acquisition will help them upgrade their core infrastructure to attract and retain mature institutional capital flows.

3. Infrastructure Distribution

In addition to talent, ecosystems, or users, some acquisitions revolve around infrastructure distribution. They embed a product into a broader stack to enhance defensibility and market coverage. A clear example is ConsenSys's acquisition of MyCrypto in 2021. While MetaMask was already a leading Ethereum wallet, MyCrypto brought user experience experiments, security tools, and a different user base focused on advanced users and long-tail assets.

This acquisition was not a comprehensive rebranding or merger; the two teams continued to develop in parallel. Ultimately, they integrated MyCrypto's feature set into MetaMask's codebase. This strengthened MetaMask's market position and helped fend off competition from more agile wallets by directly absorbing innovative outcomes.

These infrastructure-driven acquisitions aim to lock in users at critical levels by improving tool stacks and protecting distribution channels.

4. User Base Acquisition

Finally, there is the most straightforward strategy: buying users. This is particularly evident in the competitive NFT market, where the race for collectors has become very intense.

OpenSea acquired Gem in April 2022. At that time, Gem had about 15,000 active wallets per week. For OpenSea, this deal was a preemptive defensive measure: locking in a high-value "professional" user base and accelerating the development of an advanced aggregator interface, which was later launched as OpenSea Pro. In a competitive market, acquisitions are more cost-effective when speed is crucial. The lifetime value (LTV) of these users, especially the "professional" users in the NFT space who often spend large sums, likely justifies the acquisition cost.

Acquisitions make sense only when they are economically rational. According to industry benchmarks, the average revenue per NFT user in 2024 is $162. However, Gem's core user base—"professional" users—could contribute value several orders of magnitude higher. If we conservatively estimate the lifetime value of each user at $10,000, the value of these users would amount to $150 million. If OpenSea acquired Gem for less than $150 million, then from a user economics perspective, this acquisition may have already paid for itself, not to mention the development time saved.

Although user-centric acquisitions may not be as flashy as talent or technology-driven deals, they remain one of the fastest ways to solidify network effects.

What Do These Data Indicate?

Here is a macro perspective on the evolution of cryptocurrency acquisitions over the past decade—categorized by transaction volume, acquirer, and target type.

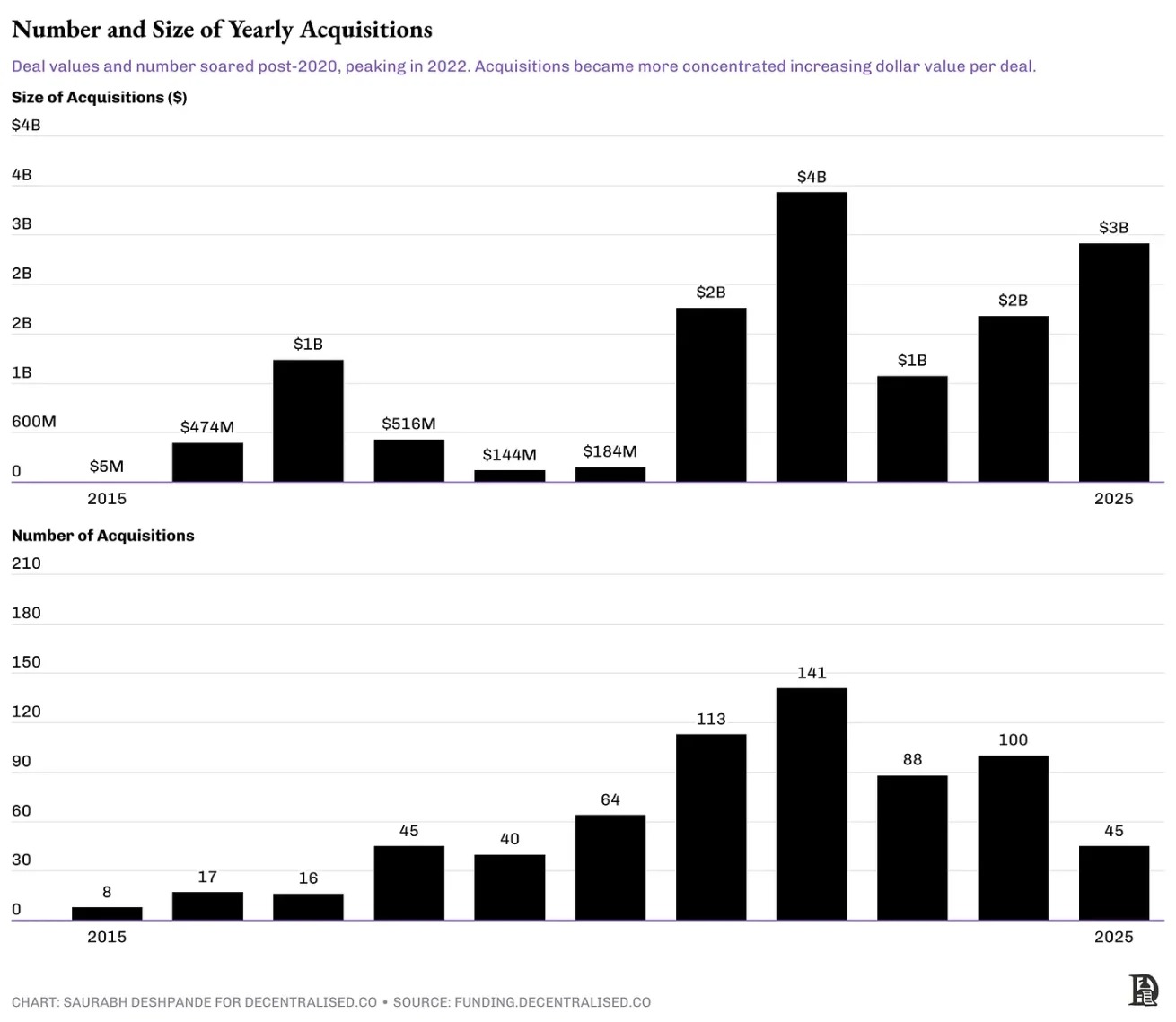

As mentioned earlier, the number of transactions does not completely synchronize with the price trends in the public market. In the 2017 cycle, Bitcoin peaked in December, but the wave of mergers and acquisitions continued into 2018. A similar lag occurred this time as well. Bitcoin peaked in November 2021, but mergers and acquisitions in the cryptocurrency space did not reach their peak until 2022. The private market reacts more slowly than the liquidity market, often delaying the digestion of market trends.

After 2020, merger and acquisition activity surged, peaking in 2022 in both quantity and cumulative value. However, transaction volume does not tell the whole story. While M&A activity cooled in 2023, the scale and nature of acquisitions changed. The broad wave of defensive acquisitions has passed, replaced by more cautious category investments. Interestingly, despite the decline in the number of acquisitions after 2022, the total transaction value in 2025 rebounded. This indicates that the market is not shrinking, but rather that mature acquirers are making fewer, larger, and more targeted deals. The average deal size increased from $25 million in 2022 to $64 million in 2025.

Coinbase's transaction with Deribit is not included in this chart.

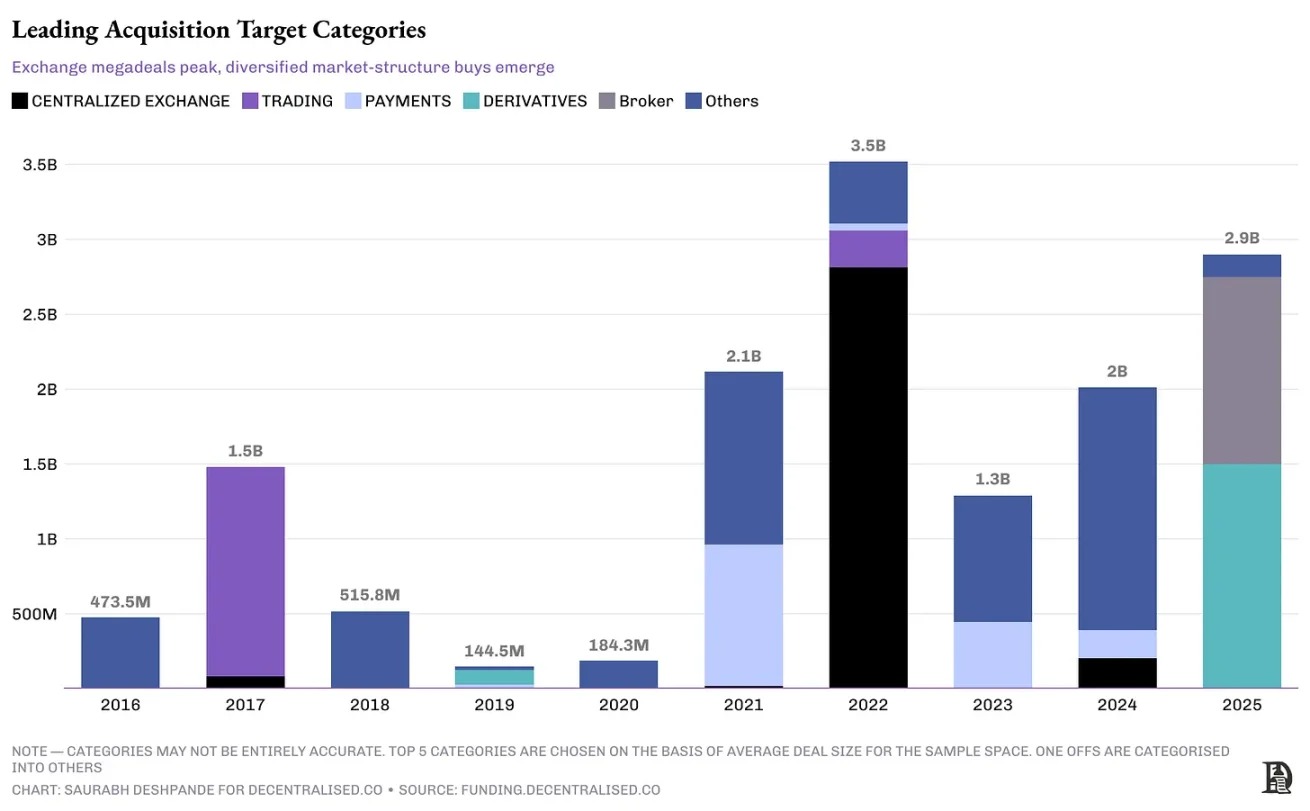

From the perspective of target categories, early acquisition targets were relatively dispersed. Market platforms acquired gaming assets, Rollup infrastructure, and a range of ecosystem investments covering early gaming, Layer 2 infrastructure, and wallet integrations. However, over time, target categories have become more concentrated. During the peak of M&A activity in 2022, transactions focused on acquiring trading infrastructure, such as matching engines, custody systems, and front-end interfaces needed to enhance trading platforms. Recently, acquisitions have concentrated in the derivatives and user-facing brokerage channel sectors.

Coinbase's transaction with Deribit is not included in this chart.

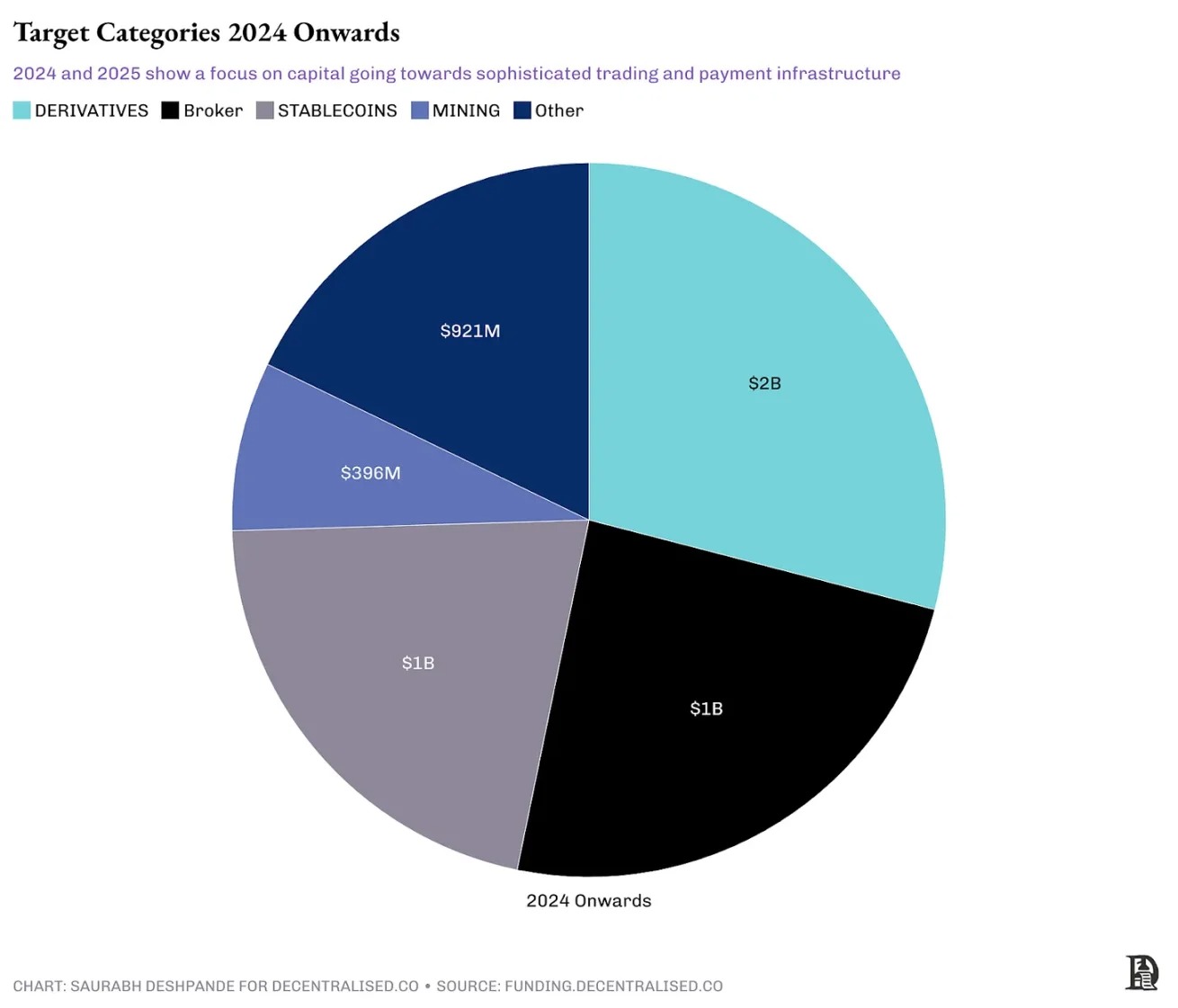

A deeper dive into transactions from 2024-2025 reveals an increasing concentration of acquisitions. Derivatives trading venues, brokerage channels, and stablecoin issuers absorbed over 75% of disclosed transaction value. The U.S. Commodity Futures Trading Commission (CFTC) has clarified rules for cryptocurrency futures, MiCA has provided a pass for stablecoins, and Basel guidelines on reserve assets have reduced risks in these areas. Giants like Coinbase are responding by purchasing regulatory footholds rather than building them themselves. NinjaTrader provides Kraken with the necessary licenses and 2 million customers in the U.S. Bitstamp offers trading coverage compliant with MiCA regulations, while OpenNode connects USD stablecoin channels directly to Stripe's merchant network.

Coinbase's transaction with Deribit is not included in this chart.

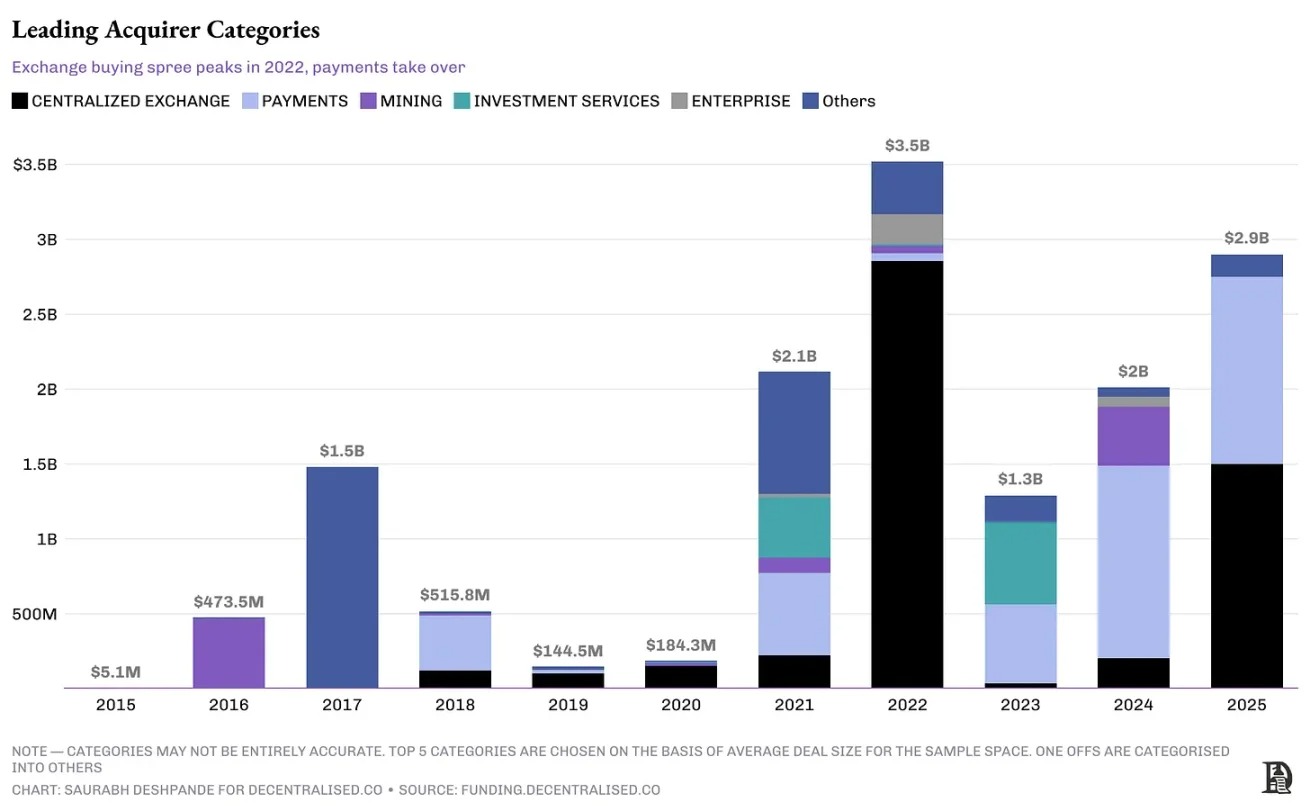

Acquirers are also evolving. In 2021-2022, exchanges led the M&A wave by acquiring infrastructure, wallets, and liquidity layers to defend their market share. By 2023-2024, the baton has passed to payment companies and financial tool platforms, targeting downstream products such as NFT channels, brokers, and structured product infrastructure. However, with regulatory changes and under-served derivatives markets, exchanges like Coinbase and Robinhood have re-emerged as acquirers, purchasing derivatives and brokerage infrastructure.

A common characteristic of these acquirers is ample funding. By the end of 2024, Coinbase had over $9 billion in cash and cash equivalents. Kraken achieved $454 million in operating profit in 2024. Stripe had over $2 billion in free cash flow in 2024. By transaction value, most acquirers are profitable companies. Kraken's acquisition of NinjaTrader to control the entire futures trading stack from user interface to settlement is an example of vertical acquisition aimed at controlling more of the value chain. In contrast, horizontal acquisitions aim to expand market coverage at the same level, as seen in Robinhood's acquisition of Bitstamp to broaden geographic reach. Stripe's acquisition of OpenNode combines vertical integration and horizontal expansion.

Coinbase's transaction with Deribit is not included in this chart.

Remember the story of Google's acquisition of the Android system? Google did not focus on short-term revenue but prioritized two things that simplified the entire mobile experience for hardware manufacturers and software creators. First, providing a unified system for hardware manufacturers to adopt. This would eliminate the fragmentation issues that plagued the mobile ecosystem. Second, offering a consistent software programming model so developers could create applications that run on all Android devices.

In the cryptocurrency space, you can see similar patterns. Well-funded existing companies are not just filling business gaps; they aim to strengthen their market positions. When you delve into the latest acquisition cases, you will see a gradual strategic shift in both the targets and acquirers. The key is that we are witnessing signs of the entire industry maturing. Exchanges are solidifying their moats, payment companies are racing to control channels, miners are strengthening their positions ahead of halving events, and vertically driven sectors like gaming have quietly disappeared from M&A records. The industry is beginning to understand which integrations will actually create compound effects and which will merely consume capital.

The gaming sector is a good example. In 2021-2022, investors poured billions of dollars into supporting gaming-related startups. However, since then, the pace of investment has significantly slowed. As Arthur mentioned in our podcast, investors have lost interest in the gaming sector unless there is a clear product-market fit.

Source: funding.decentralised.co

This context makes it easier to understand why so many mergers and acquisitions, despite strategic intentions, fail to achieve the expected results. It is not just about what is acquired, but also about the quality of integration. While cryptocurrency is unique in many ways, it cannot escape these issues.

Why Mergers and Acquisitions Often Fail

In the book "The M&A Trap," Baruch Lev and Feng Gu studied 40,000 global M&A cases and concluded that 70%-75% of mergers and acquisitions end in failure. They attribute these failures to factors such as the target company's size being too large, overvaluation of the target, acquisitions unrelated to core business, weak operations of the target company, and inconsistent executive incentives.

The cryptocurrency space has also seen some failed acquisitions, and the aforementioned factors apply here as well. Take FTX's acquisition of the portfolio tracking app Blockfolio for $150 million in 2020 as an example. At the time, this deal was touted as a strategic move aimed at converting Blockfolio's 6 million retail users into FTX trading users. Although the app was rebranded as the FTX App and briefly gained some attention, it failed to significantly boost retail trading volume.

Worse still, when FTX collapsed at the end of 2022, its partnership with Blockfolio nearly vanished. Years of accumulated brand equity evaporated. This serves as a reminder that even acquisitions with a strong user base can become worthless due to the overall failure of the platform.

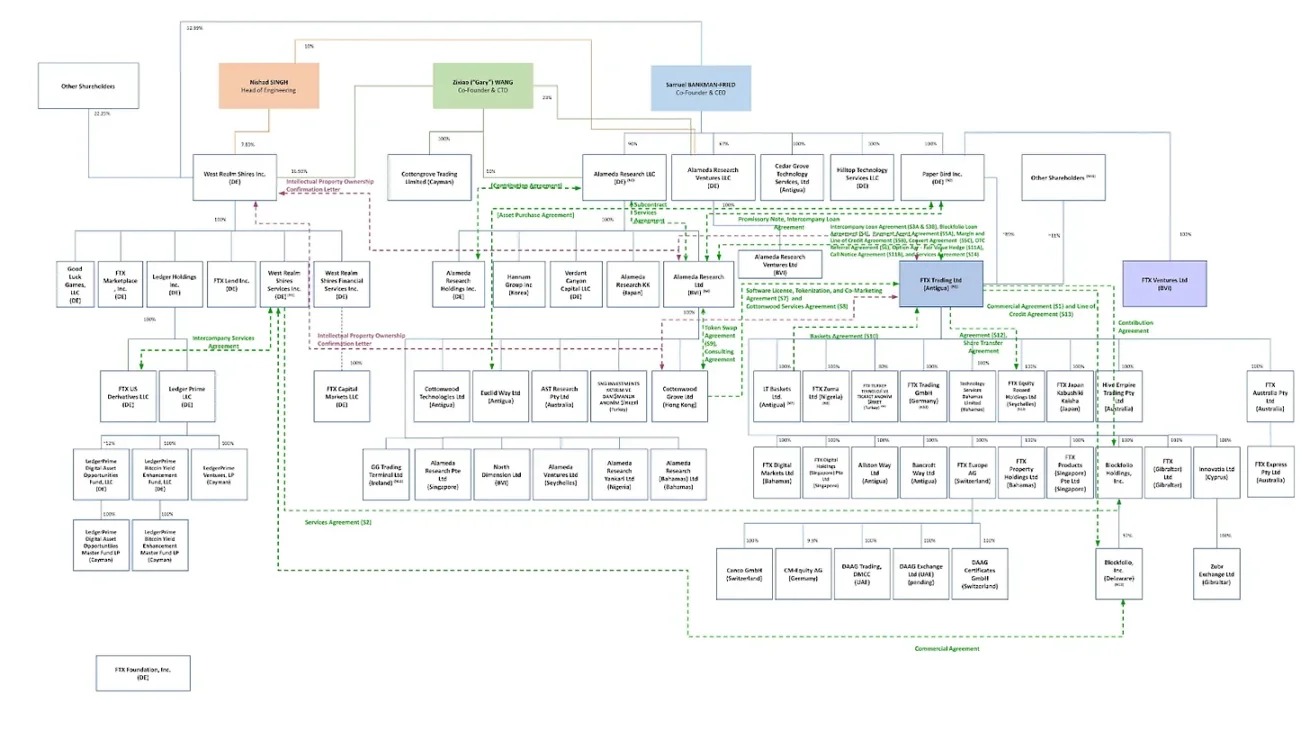

Many companies act too quickly during acquisitions, making mistakes. The image below shows how fast FTX moved during its acquisition, perhaps unnecessarily so. It obtained licenses through acquisitions, and the following image depicts its post-acquisition company structure.

Source: Financial Times

Polygon is a notable example of the risks associated with aggressive acquisition strategies. Between 2021 and 2022, it spent nearly $1 billion acquiring projects related to zero-knowledge proofs, such as Hermez and Mir Protocol. At the time, these moves were hailed as visionary. However, two years later, these investments have not translated into meaningful user adoption or market dominance. One of its key zero-knowledge proof projects, Miden, ultimately spun off into an independent company in 2024. Polygon, once at the center of cryptocurrency discussions, has significantly declined in strategic relevance. Of course, these things often take time, but as of now, there is no substantial evidence indicating a return on investment from these acquisitions. Polygon's acquisition spree reminds us that even with ample funding, talent-driven acquisitions can fail without the right timing, integration, and clear downstream use cases.

There are also failed acquisition cases in the on-chain native DeFi space. In 2021, the merger of Fei Protocol and Rari Capital, along with a token swap, led to joint governance under the newly formed Tribe DAO. Theoretically, this merger promised deeper liquidity, lending integration, and cooperation between DAOs. However, the merged entity quickly fell into governance disputes and faced costly vulnerabilities in the Fuse market, ultimately leading the DAO to vote to return funds to token holders.

Despite this, the cryptocurrency space has advantages in successful acquisitions compared to traditional industries for three reasons:

The open-source foundation means that technical integration is often easier. When most of your code is already public, due diligence becomes more straightforward, and there are fewer issues with merging codebases compared to proprietary systems.

Token economics can create incentive alignment mechanisms that traditional equity cannot match, provided that the tokens have real utility and value capture capabilities. When the teams of both acquirers hold tokens of the merged entity, their incentives remain aligned long after the deal is completed.

Community governance introduces accountability mechanisms that are rare in traditional mergers and acquisitions. When significant changes must be approved by token holders, it becomes more difficult to push through deals based solely on executive arrogance.

So, where do we go from here?

Built for Acquisition

Today's funding environment requires a pragmatic approach. If you are a founder, your pitch should not only be "Why should we raise funds?" but also "Why might someone want to acquire us?" Here are three major drivers in the current cryptocurrency M&A landscape.

First, venture capital will be more precise.

The funding environment has changed. Venture capital has plummeted over 70% since its peak in 2021. Monad's $225 million Series A funding and Babylon's $7 million seed round are exceptions and do not indicate a market rebound. Most venture capital firms are focusing on companies with growth momentum and clear business models. As interest rates increase capital costs and most tokens fail to demonstrate sustainable value accumulation mechanisms, investors have become highly selective. For founders, this means that while considering an increasingly difficult funding path, they must also contemplate acquisition offers.

Second, strategic leverage.

Well-funded existing companies are buying time, distribution channels, and defensive capabilities. With increased regulatory clarity, licensed entities have become obvious acquisition targets. But this acquisition appetite goes beyond that. Companies like Coinbase, Robinhood, Kraken, and Stripe are making acquisitions to enter new markets faster, secure stable user bases, or compress years of infrastructure development into a single deal. If what you build can reduce legal risks, accelerate compliance processes, or provide clearer paths to profitability or reputation enhancement for acquirers, then you are on their radar.

Third, distribution and interfaces.

The missing link in infrastructure is delivering products quickly and reliably to users. The key is to acquire those that can unlock distribution channels, simplify complexity, and shorten time to market fit. Stripe acquired OpenNode to streamline cryptocurrency payment processes. Jupiter acquired DRiP Haus to add NFT distribution capabilities to its liquidity stack. FalconX acquired Arbelos to add institutional-grade structured products, potentially making it easier to serve different customer segments. These are all infrastructure strategies aimed at expanding coverage and reducing operational friction. If what you build enables other companies to grow faster, cover more ground, or serve better, then you are on the acquirer's shortlist.

This is an era of strategic exits. As you build your company, consider that your future depends on whether others want to own what you create.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。