Last year, Jane Street accounted for 14% of ETF trading in the U.S. and 20% in Europe.

Authors: Will Schmitt & Robin Wigglesworth

Compiled by: Deep Tide TechFlow

According to investor documents obtained by the Financial Times, Jane Street achieved over $10 billion in net trading revenue for the fourth consecutive year. According to Coalition Greenwich data, its total trading revenue of $21.9 billion is roughly one-seventh of the total trading revenue of the world's twelve largest investment banks in equities, bonds, currencies, and commodities last year.

“Their profits are almost astonishing. This is because they handle many financial instruments that others are unwilling to touch,” said Larry Tabb, a long-time analyst of the industry who currently works at Bloomberg Intelligence. “That’s where the biggest profits are, but also the biggest risks.”

There are currently no signs that Jane Street's growth will slow down. According to insiders, its net trading revenue in the first half of 2024 grew by 78% year-on-year to $8.4 billion. If this level can be maintained in the second half, Jane Street's annual trading revenue will exceed that of last year’s larger Goldman Sachs.

If it can maintain the 70% profit margin disclosed in the documents, Jane Street's revenue this year will easily surpass that of Blackstone or BlackRock, according to analyst forecasts collected by LSEG.

Jane Street has particularly excelled in the bond market, quickly penetrating this long bank-dominated field, which was previously considered difficult for independent trading firms to enter.

“You can think of Jane Street's development as a continuously automating process where we constantly challenge ourselves with more complex tasks and then automate them,” Matt Berger, head of Jane Street's fixed income department, told the Financial Times. “That’s the process of our business continually evolving.”

However, Jane Street also faces numerous internal and external challenges.

Jane Street Has Sparked an ETF Wave

This once low-profile trading firm has now become one of the most watched companies in the industry, making many Jane Street employees uncomfortable. The rapid growth is testing its originally flat, academic organizational structure. Competitors are trying to poach its top talent. Some investors worry that Jane Street's significant intermediary role in the rapidly expanding bond ETF market may render it systemically important.

Meanwhile, competitors are also fighting back, with banks trying to halt its expansion in the fixed income market, while Citadel Securities has set its sights on Jane Street's success in the corporate bond market.

“This is the classic innovator's dilemma,” said a former Jane Street employee. “When they were at a disadvantage, they acted quickly and innovated in ways that others couldn’t. Now that they are a giant, naturally, others will catch up.”

Jane Street was founded in 2000 by several traders from Susquehanna and a former IBM developer. In its first twenty years, it was content to develop quietly behind older, more established trading firms like Virtu Financial and Citadel Securities.

It initially traded American Depositary Receipts in a small, windowless office on the now-defunct American Stock Exchange. But it quickly expanded into options and ETFs, which were promoted by Amex a few years prior.

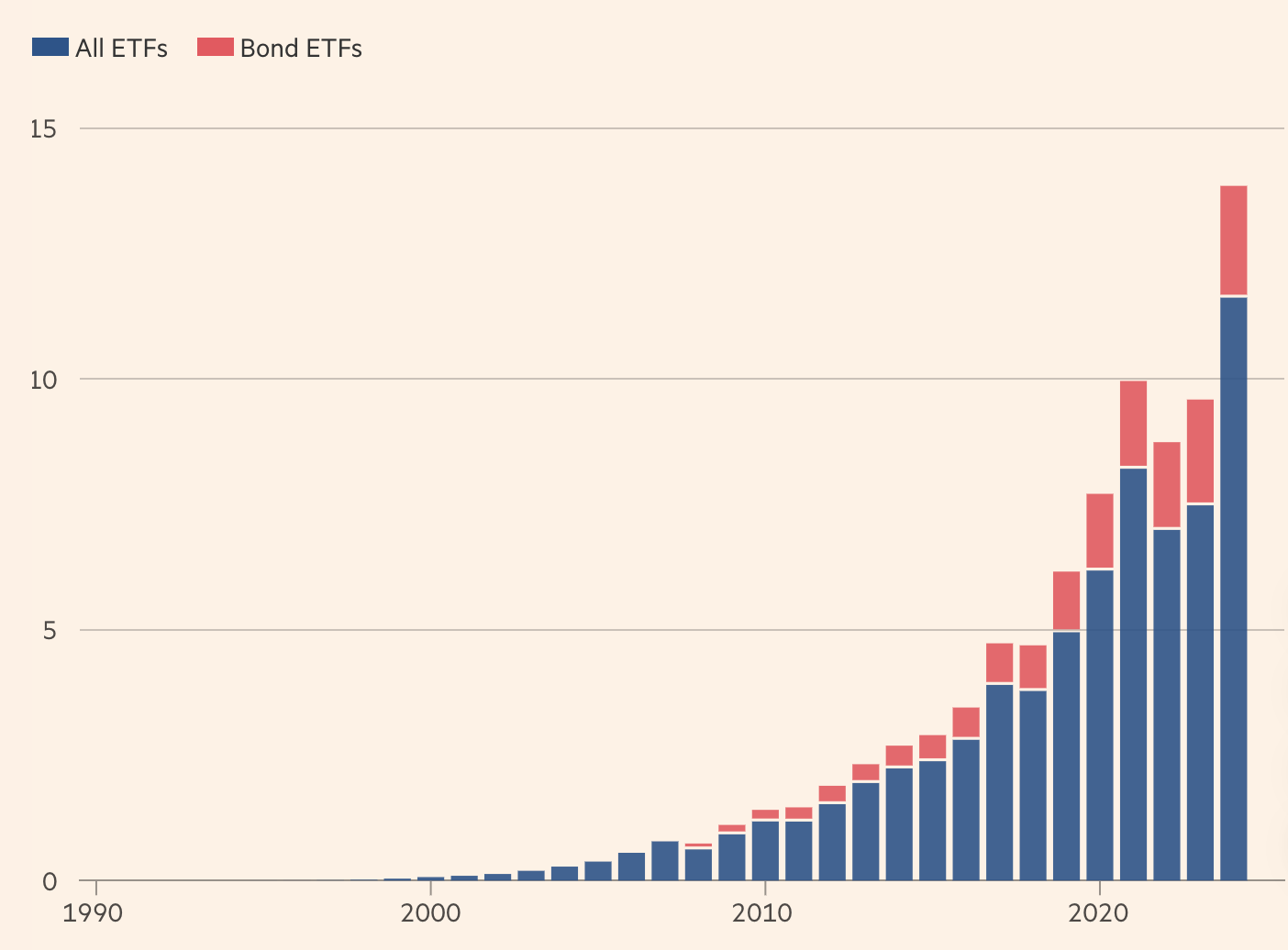

At that time, ETFs were still a niche market, with market assets of only about $70 billion when Jane Street began trading. However, ETFs quickly became its main business, and over time, it became an important “authorized participant,” acting as a market maker that can create and redeem ETF shares in addition to trading.

Jane Street has particularly excelled in the niche ETF space. Former and current executives say the company's love for puzzles—which is also part of its complex interview process—reflects its willingness to tackle more challenging trading problems, such as handling ETFs in less liquid markets (like corporate bonds, Chinese stocks, or exotic derivatives).

This means that, at Jane Street, speed is not as critical as it is at Jump Trading, Citadel Securities, Virtu, or Hudson River Trading, even though the company is often classified as a high-frequency trader.

According to insiders and competitors, Jane Street is positioned closer to the middle of the spectrum between intuitive traders from investment banks' “prop trading desks” before 2008 and pure tech firms like Citadel Securities or Jump Trading. The company sometimes holds positions for days or even weeks.

“It’s an interesting blend of technology and street smarts,” said Gregory Peters, co-chief investment officer of PGIM Fixed Income.

Investing in ETFs has proven to be a wise decision, as the industry has experienced a long-term boom. According to data provider ETGI, ETF assets are now approaching $14 trillion. Jane Street has gradually attracted smart talent looking to earn lucrative rewards—one of the reasons why young MIT graduate Sam Bankman-Fried joined the company in 2013.

However, even within its industry, it is known for its unique use of OCaml, a programming language used to build nearly all of its systems. To outsiders, it remains a mystery (fittingly, Jane Street has an original Enigma machine at its New York headquarters).

Its anonymity is so high that three of the four co-founders have quietly retired, with almost no one outside knowing, leaving the last one, Rob Granieri, referred to by insiders as the first among equals. But Jane Street has no CEO, and in loan documents shared with investors, the company describes itself as “a functional organizational structure composed of various management and risk committees.”

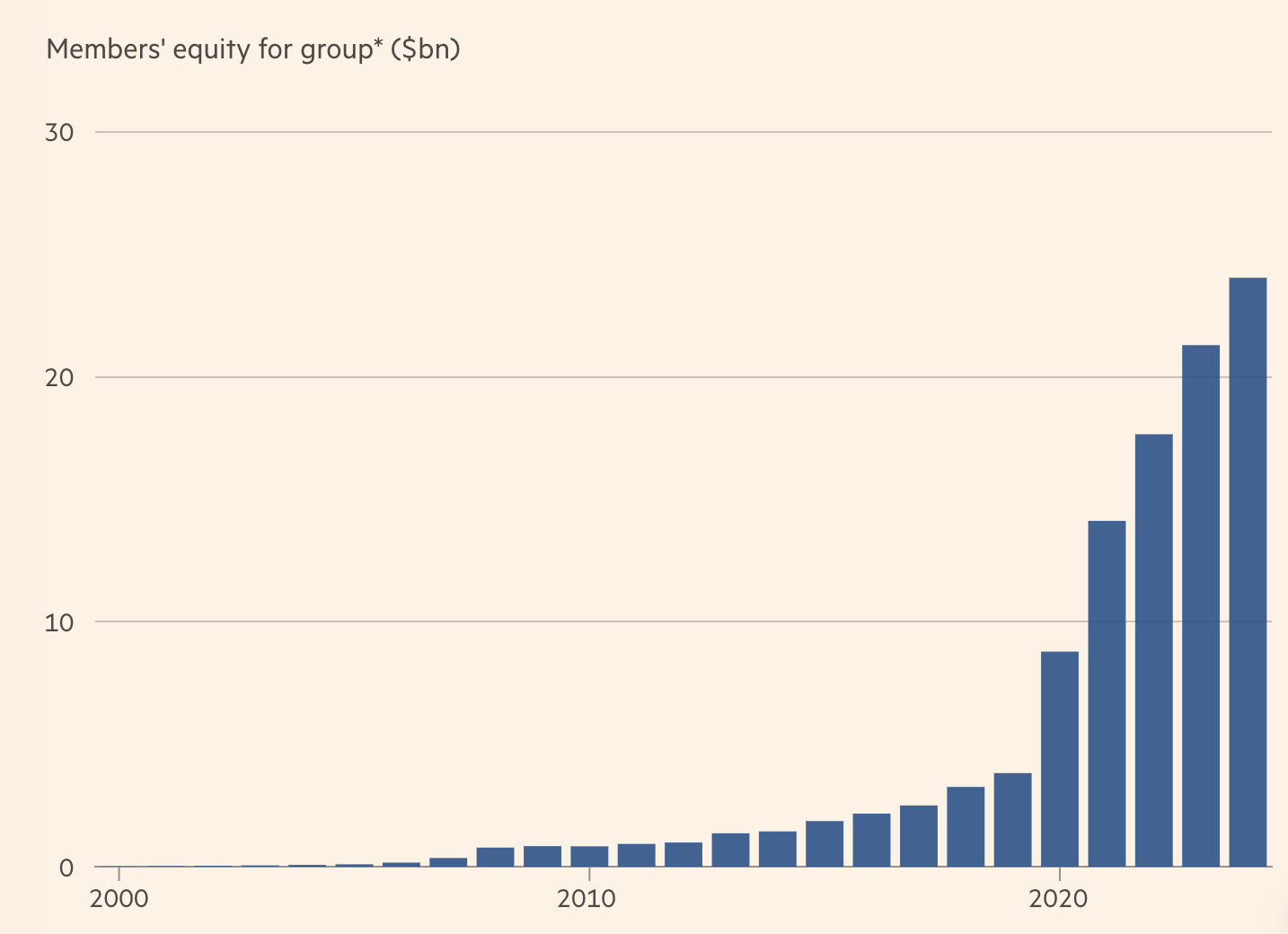

Each trading desk and business unit is overseen by one of 40 equity holders, who collectively own Jane Street, valued at $24 billion. Outsiders perceive Granieri more as a low-profile long-haired actor from Silicon Valley than a billionaire trading mogul, but Jane Street employees say that major decisions are made by a broader collective leadership group, a structure that fosters collaboration and reduces hierarchy.

This is reflected in its compensation structure—Jane Street does not tie compensation to individual trading profits, nor even to the profits of the trading desk an employee is on. The company has long avoided using formal titles, even though this may cause some confusion outside the company.

“In the early days, when you gathered these people in a room, they wouldn’t give you business cards, they all wore shorts and T-shirts, and you had no idea who you were talking to,” Tabb recalled from Bloomberg.

However, Jane Street's low-profile image began to change in 2020, as its massive profits during the tumultuous markets of the COVID-19 pandemic made headlines.

Its profits even surpassed those of Ken Griffin's Citadel Securities, drawing widespread attention, and rumors of huge paychecks sparked jealousy on Wall Street. Marking its debut on the biggest stage, in September 2020, the Federal Reserve added Jane Street to its list of acceptable trading counterparties for crisis response measures, alongside Wall Street stalwarts like JPMorgan.

Subsequently, Jane Street gained widespread attention because Bankman-Fried began his trading career there before founding the now-defunct cryptocurrency exchange FTX. This publicity made many at Jane Street uncomfortable, especially since Bankman-Fried's risky and non-compliant approach led to his imprisonment, which many insiders and outsiders viewed as starkly contrasting with Jane Street's extremely cautious style.

In addition to having a central risk center of 14 people that continuously monitors all its risk exposures, Jane Street also maintains an additional “liquidity buffer” of about 15% of its trading capital.

This reserve is kept outside its main brokers to ensure that even in chaotic markets, Jane Street can maintain its positions. Additionally, the company makes extensive use of derivatives to hedge against small idiosyncratic shocks that may affect individual trading desks and broad financial crises that could shake the entire company.

Earlier this year, Jane Street came back into the spotlight due to a lawsuit against two former traders who jumped to hedge fund Millennium Management in February. Jane Street noted in court documents that the company was losing over $10 million a day due to the alleged deterioration of an Indian options strategy taken by these traders. Since then, the two companies have been engaged in legal battles to determine who needs to provide which documents.

Nevertheless, these concerns have not affected Jane Street's pace of development. The rapid growth of its trading revenue demonstrates its expanding influence in the equities and options markets. According to Berger, the company plans to further expand its government bond and currency trading in the coming year, significantly enhancing the scope and objectives of its machine learning work in personnel, infrastructure, and computing power.

Jane Street's Profit Growth Enhances Company Value

However, Jane Street's core business remains ETFs. According to documents shared by the company with lenders, last year Jane Street accounted for 14% of ETF trading in the U.S. and 20% in Europe. In the bond ETF sector, Jane Street estimates it accounted for 41% of all creation and redemption transactions.

This market dominance allows Jane Street to enter the traditionally bank-dominated underlying bond market, which is a significant distinction from its peers.

“Technology-driven companies that can price in real-time and respond quickly will earn more profits,” said Alexander Morris, chief investment officer of F/m Investments, which uses Jane Street as its market maker for bond ETFs. “Because they are faster and provide fairer prices, their goal is to complete trades quickly and move on to the next one, rather than earning extra compensation by delaying trade execution.”

However, after several years of harvest, Jane Street seems to be facing greater pressure.

Many banks have been actively investing in technology and restructuring their trading teams to compete with companies like Jane Street, both in equities and bonds. These efforts have begun to pay off. “They have narrowed the gap significantly,” said Adam Gould, global head of equities at Tradeweb. At the same time, Citadel Securities—already a significant player in the government bond market—has also begun to venture into the corporate debt market. “Competition has indeed intensified, and I think this is beneficial for the overall market environment and investors,” Berger said.

However, the biggest challenge Jane Street may face could come from within. When all employees could work on one floor in New York, maintaining a collaborative, flat culture was relatively easy. But by the end of last year, the company had 2,631 full-time employees, with nearly half distributed across various branches from Singapore to Amsterdam.

This is also one of the reasons why the Millennium poaching incident has drawn attention. As the scale expands and cohesion weakens, Jane Street may lose more employees, and the risk of strategy leaks will also increase, posing a challenge for a company that has consistently performed well.

A former Jane Street employee pointed out, “Even in years of poor performance, Jane Street was still able to offer generous compensation to employees. But back then, the company only had 100-200 people. Now, the company needs to support nearly 3,000 employees.”

If Jane Street has a year of poor performance, it would have a significant impact on the company. If there is a year of mediocre performance, the company would find itself in a very difficult situation, putting it in an unstable position.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。