The hash rate is still slightly below the historical peak, and although income has decreased, the continued investment by miners indicates a huge confidence in the Bitcoin network.

Authors: CryptoVizArt, UkuriaOC, Glassnode

Translation: Lawrence, Mars Finance

Abstract

- The hash rate is still slightly below the historical peak, and although income has decreased, the continued investment by miners indicates a huge confidence in the Bitcoin network.

- Interaction between investors and exchanges is decreasing, and the overall decline in trading volume indicates a weakening interest in investment and trading.

- Both Bitcoin and Ethereum ETFs have seen fund outflows, but investor interest in Bitcoin ETFs is still significantly larger in scale and quantity.

Miners

Miners are still the fundamental participants in the Bitcoin network and the primary source of new coins. Miners provide hash power to discover the next valid block, and the network automatically rewards them with newly issued coins and transaction fees.

This makes the mining industry extremely challenging, as miners cannot control the input cost of energy or the production cost of BTC.

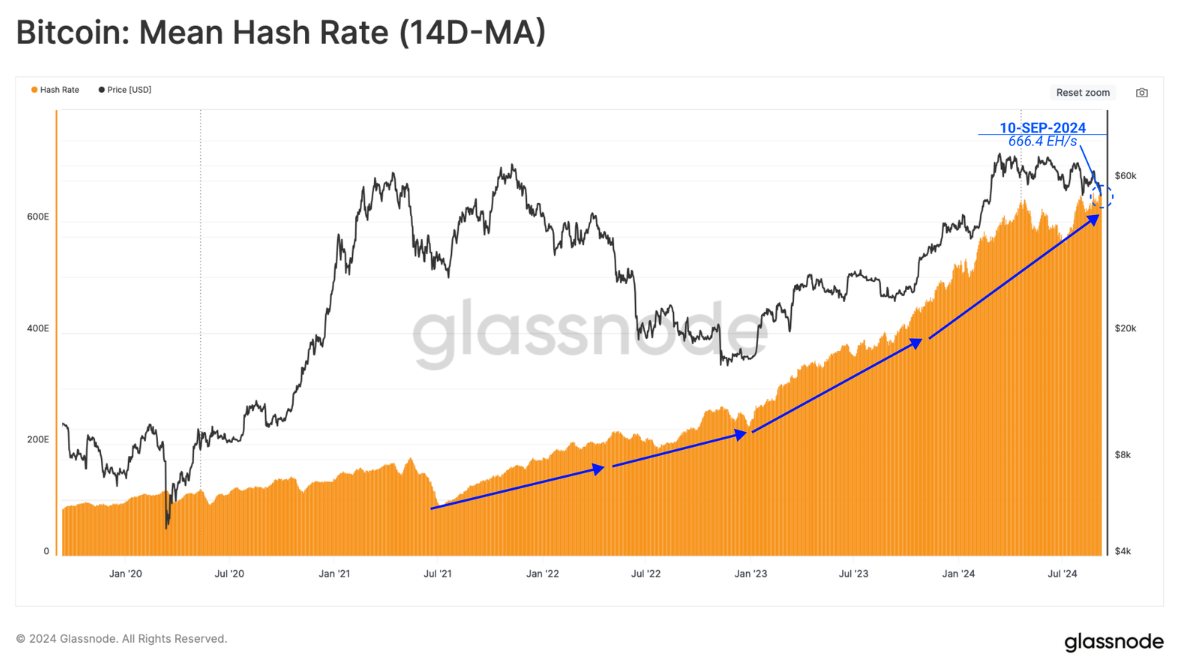

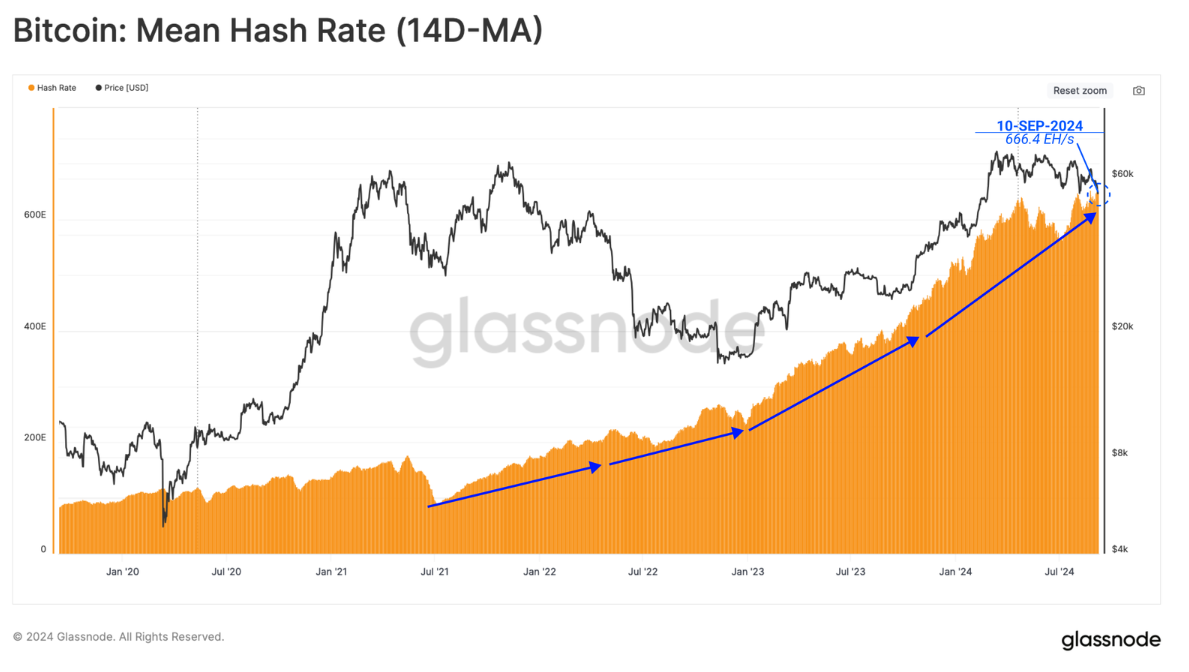

Despite fluctuating and uncertain market conditions, Bitcoin miners continue to install new ASIC hardware, driving up the overall hash rate (14D-MA) to 666.4EH/s, only 1% lower than the ATH.

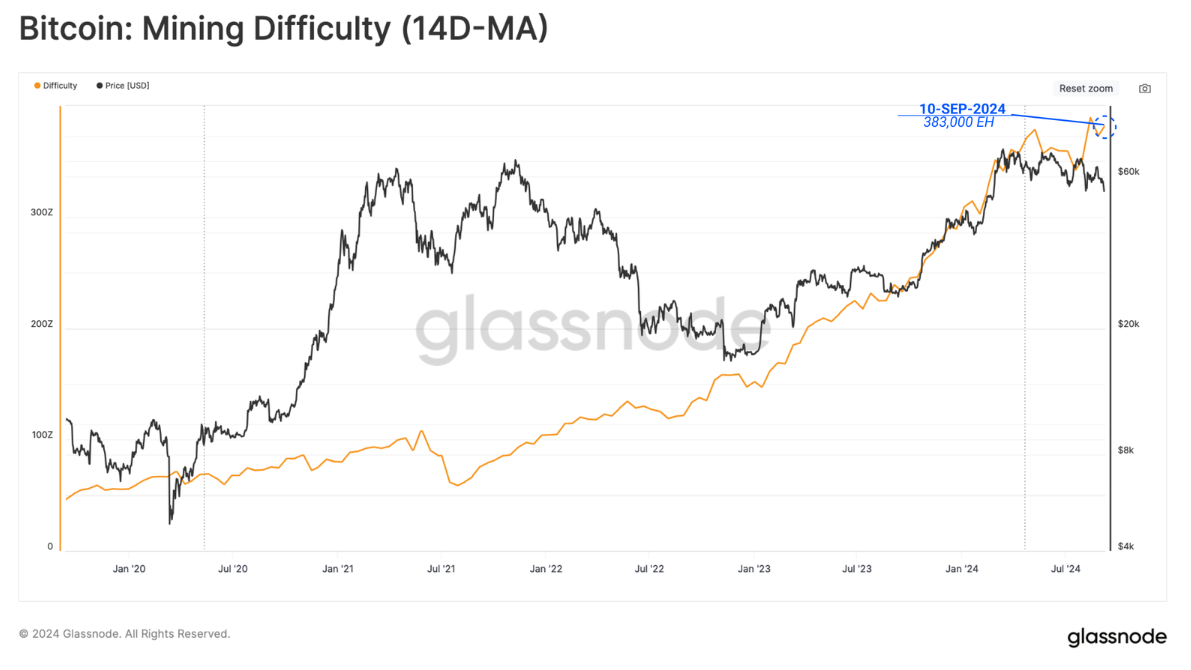

With the increase in hash rate, the target difficulty of successfully mining valid blocks will also increase. The Bitcoin protocol automatically adjusts the difficulty to accommodate the rise and fall of hash rate on the network.

Currently, the average hash value required to mine a block is 338k exahash. This is the second highest difficulty in Bitcoin's history, highlighting the increasingly fierce competition in the mining industry.

However, since the market price hit a new high in March, miner income has significantly decreased. A large part of the income decline can be attributed to the decrease in fee pressure, resulting from reduced demand for currency transfers and lower fees from rune and inscription-related transactions.

With the spot price exceeding $55,000, miner income related to block subsidies is still relatively high, but it is still about 22% lower than the previous peak level.

- Block subsidy income: $824 million

- Transaction fee income: $20 million

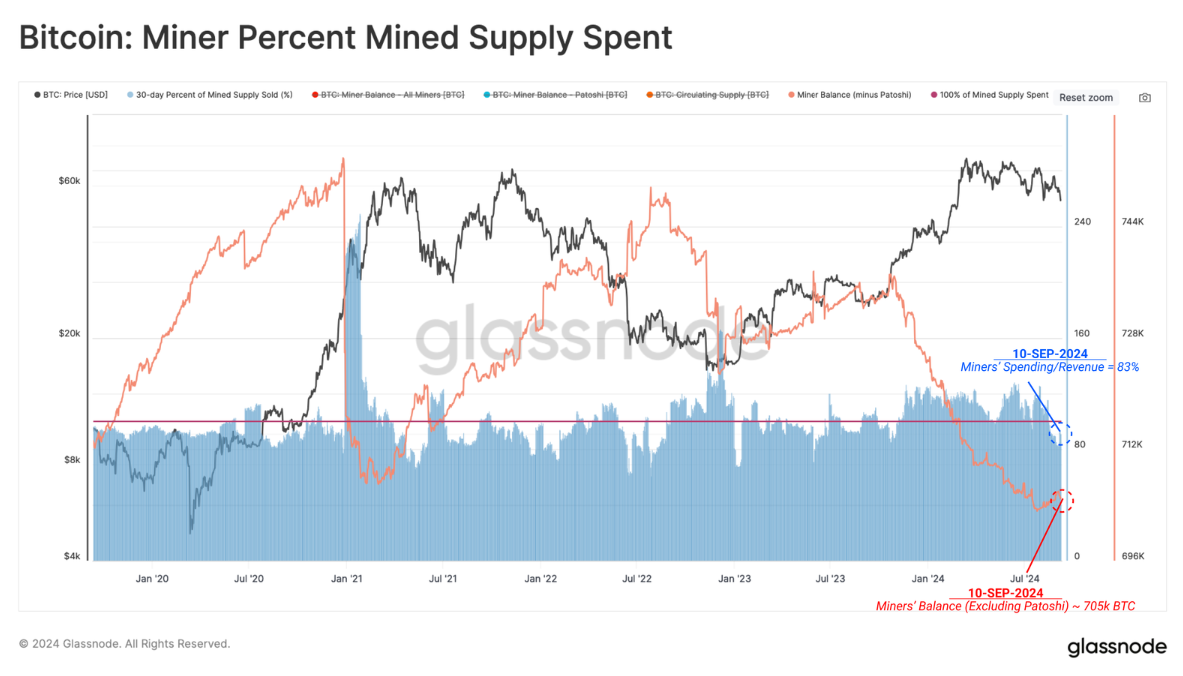

With the decrease in income, we can infer that a certain degree of income pressure may begin to emerge. We can estimate the percentage of mining supply spent by miners in 30 days to measure the situation.

Due to the competitive and capital-intensive nature of the mining industry, miners have historically needed to allocate most of the mined coins to pay for input costs. Interestingly, miners have shifted from net distribution of mined coins to now retaining a portion of the mined coins in their treasury reserves.

This highlights an interesting development, as miners tend to be pro-cyclical, being sellers during downturns and holders during upswings. The increase in hash rate and difficulty means that the production cost of BTC is increasing, which may have an adverse impact on miners' profitability in the near future.

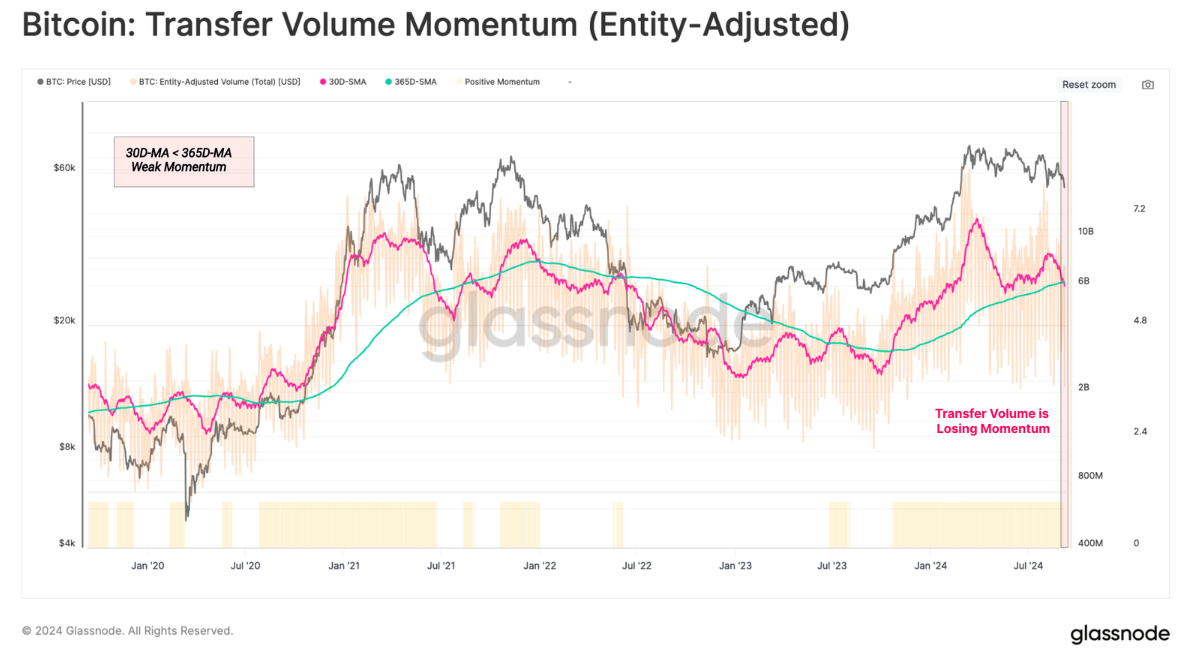

Settlement Slows

The size of on-chain settlement transaction volume can also reflect the level of adoption and the health of the network. When filtering the entity-adjusted transaction volume, the network currently processes and settles approximately $6.2 billion in transactions per day.

However, settlement volume has started to decline to the annual average level, indicating a significant decrease in network usage and throughput. Overall, this is a net negative observation.

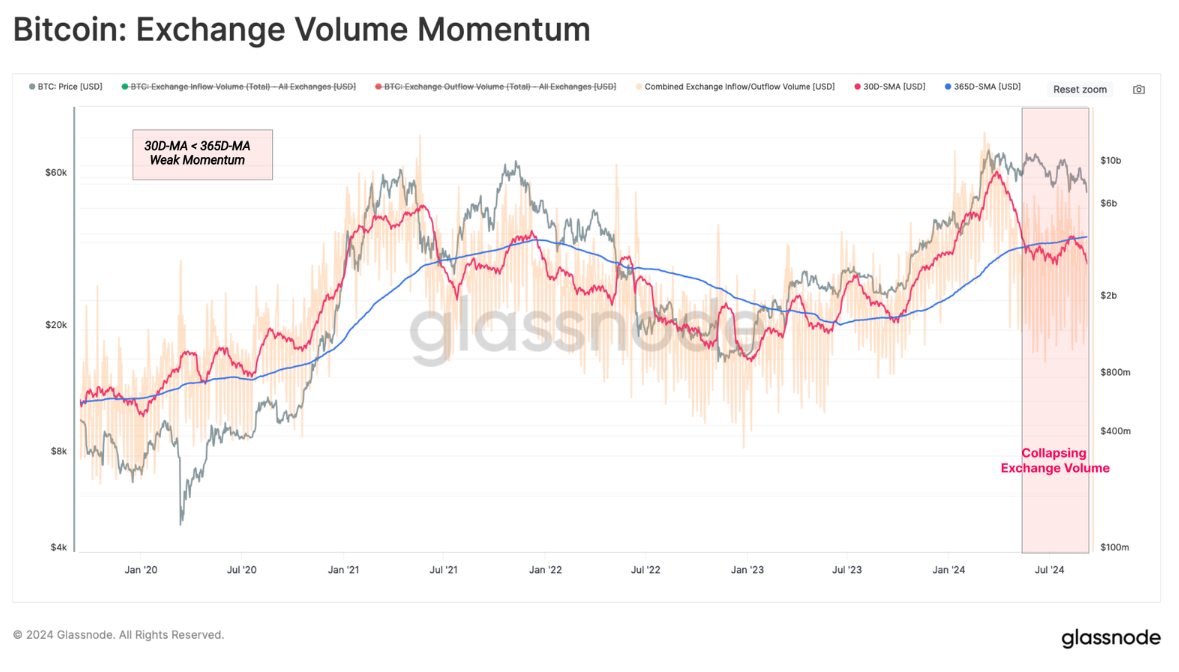

Declining Trading Interest

In the ever-changing market landscape, centralized exchanges have always been the central venues for speculative activities and price discovery. Therefore, we can assess the on-chain transaction volume of these venues as an indicator of investor activity and speculative interest.

By applying a similar 30-day/365-day momentum crossover to exchange-related inflows and outflows, we can see that the monthly average trading volume is significantly lower than the annual average trading volume. This highlights the decrease in investor demand and reduced speculative trading within the current price range.

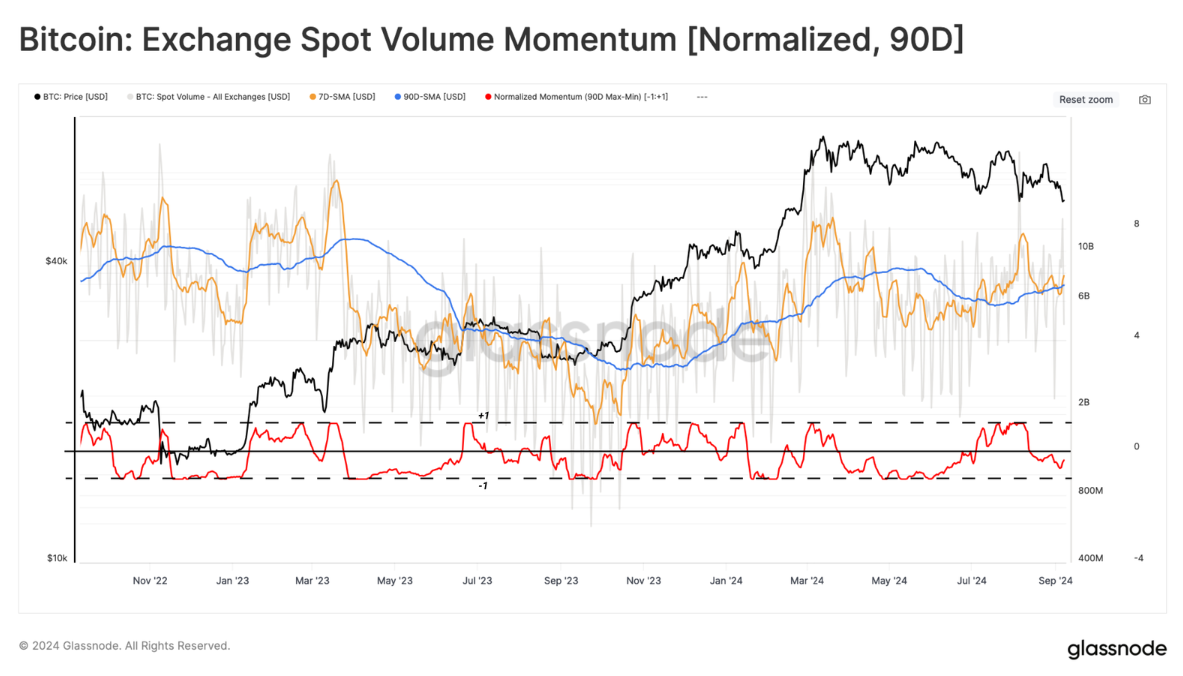

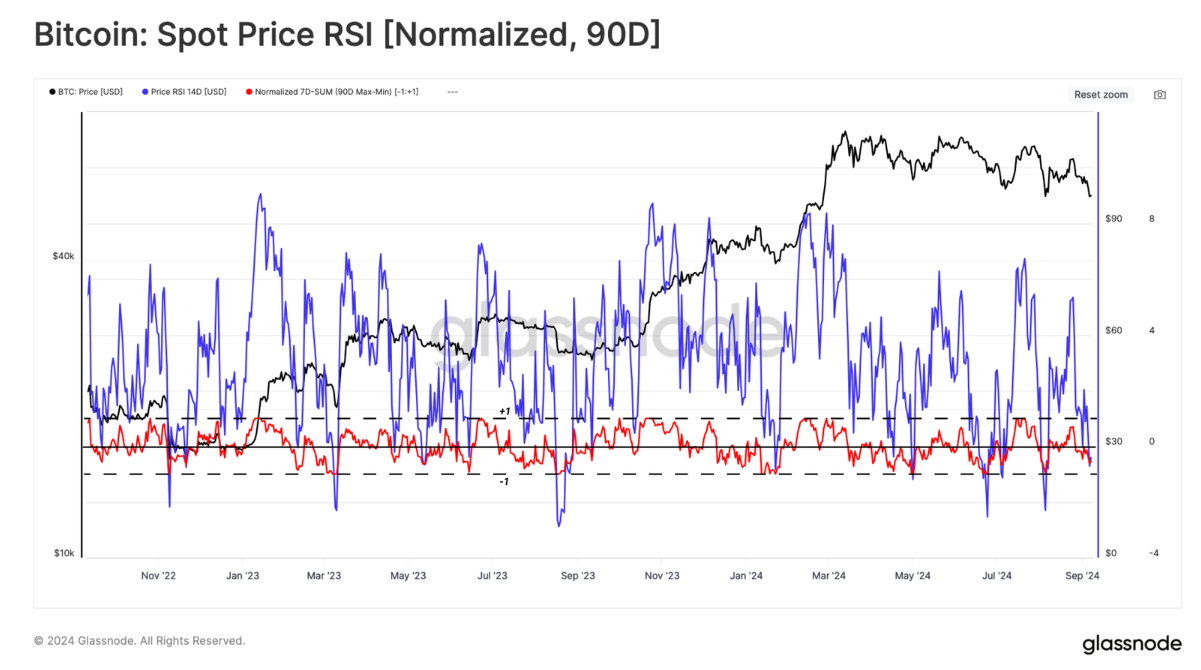

Next, we will look at spot trading volume on exchanges. Here, we apply a 90-day MinMax scalar, which normalizes values within the range of 1 to -1 relative to the maximum and minimum values for the selected period.

It can be seen that spot trading volume continues to weaken, similar to the previous observation. This further confirms the significant decline in trading activity in the previous quarter.

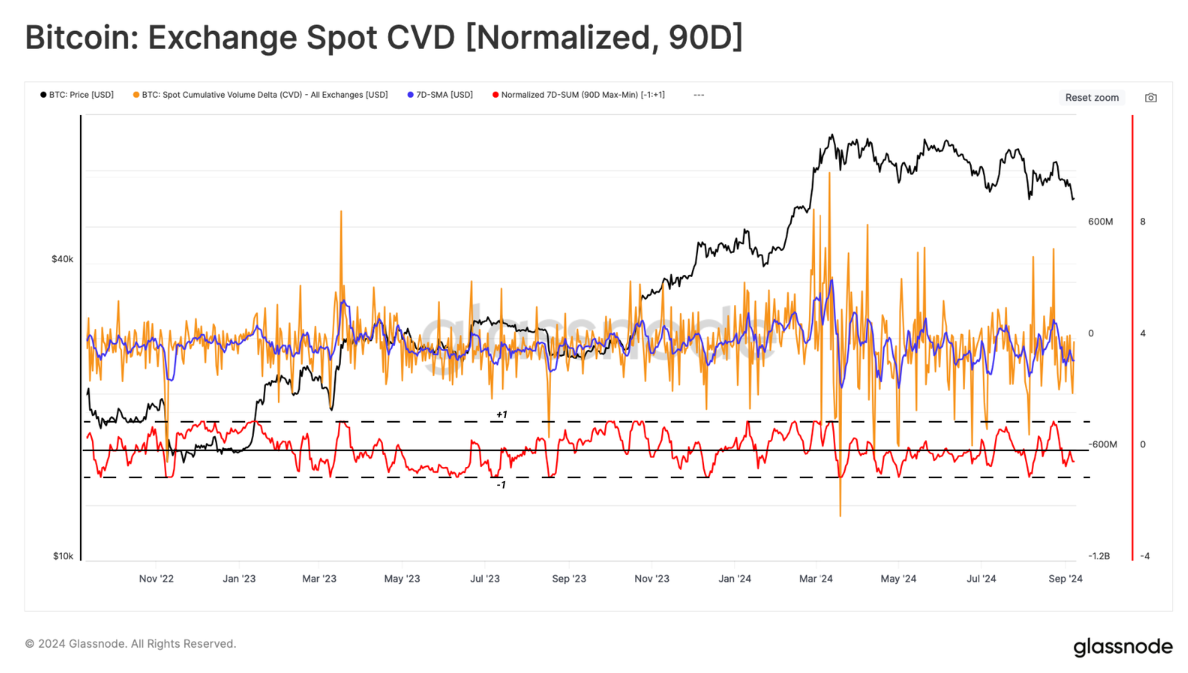

The CVD indicator can estimate the net balance of current buying and selling pressure in the spot market. Using the same method, we note that selling pressure from investors has been increasing over the past 90 days, leading to a downward bias in price trends.

Finally, we can assess the momentum of Bitcoin prices. Here, we can see a certain degree of indecision, with both positive and negative data points in August. This contrasts sharply with the two indicators previously emphasized, both of which were significantly negative during the same period.

By combining the MinMax transformations of trading volume, CVD, and price behavior, we can generate a sentiment heatmap with characteristic values between 1 and -1. We can consider this within the following framework:

🟢 A value of 1 indicates higher risk

🟡 0 indicates moderate risk

🔴 -1 indicates lower risk

All three indicators indicate that the market is entering a low-risk zone relative to the data points of the past 90 days. The fusion between the discussed spot indicators can be translated into a reduction (spot trading volume momentum) in selling pressure (CVD 0), while price action is slowly declining. This structure may be susceptible to external forces and could potentially break out on either side if the situation changes.

ETF

The Ethereum ETF has now followed the launch of the US Bitcoin ETF in August. These two events mark a "crossing the Rubicon" moment for the digital asset ecosystem, providing a convenient entry point for the US traditional market to access the leading two cryptocurrencies.

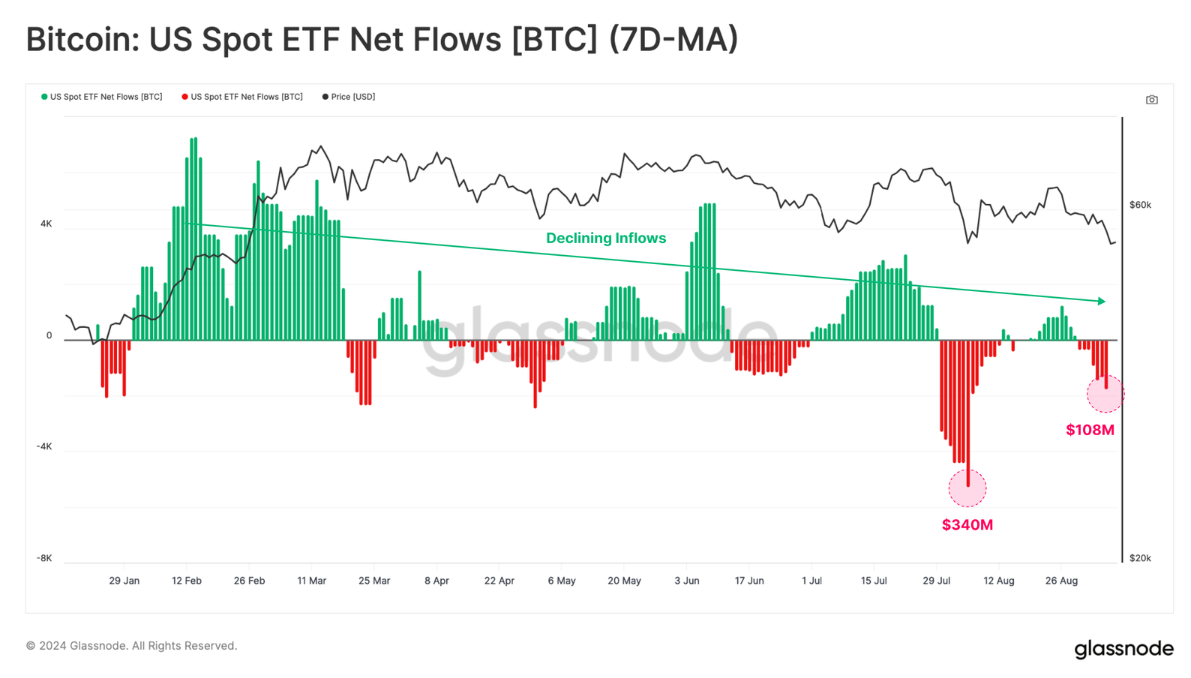

Starting with the Bitcoin ETF, we can see that net capital flows in USD have weakened since August 2024, with current weekly outflows at $107 million.

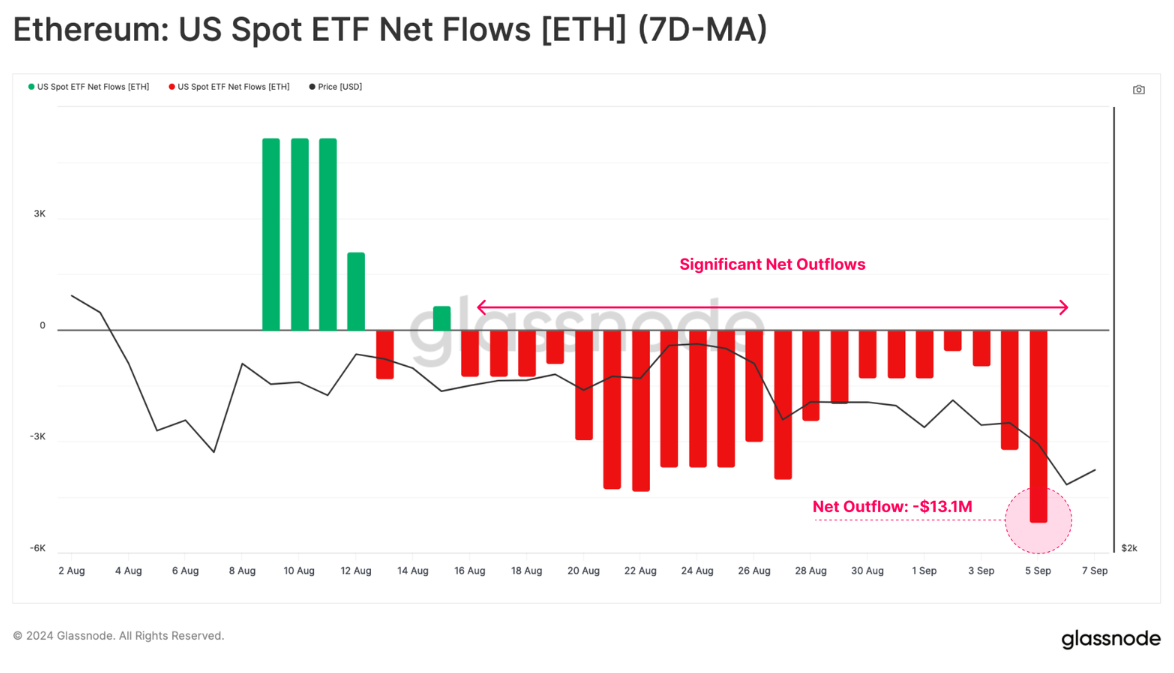

The recent demand for the Ethereum ETF has been relatively subdued, with net negative outflows. This is mainly due to redemptions of the Grayscale ETHE product, and the inflow demand from other instruments is not sufficient to offset this demand.

Overall, the total outflow of the Ethereum ETF is $13.1 million. This highlights the difference in demand scale between BTC and ETH, at least under current market conditions.

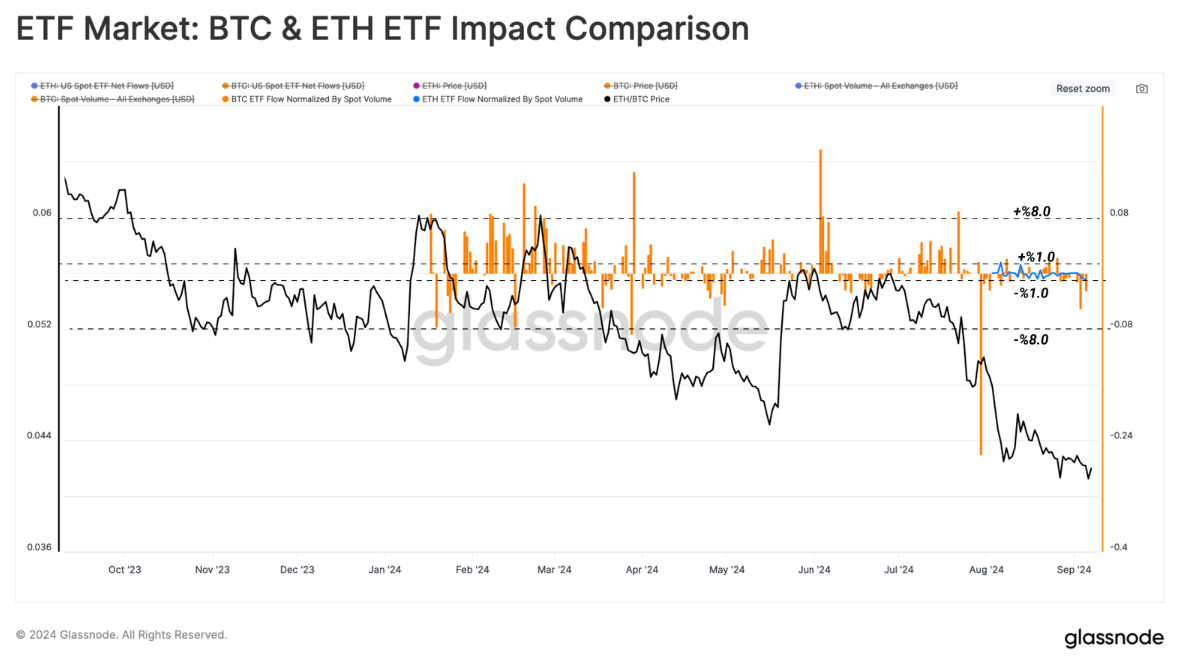

To approximate the impact of ETFs on the Bitcoin and Ethereum markets, we have standardized the net flow deviation of ETFs through the corresponding spot trading volume. This ratio allows us to directly compare the relative weight of each ETF in each market.

As shown in the chart below, the relative impact of the ETF on the Ethereum market is equivalent to ±1% of the spot trading volume, while the Bitcoin ETF is ±8%. This indicates that despite the normalization of the Bitcoin ETF, interest in the Bitcoin ETF is still an order of magnitude larger than the Ethereum ETF.

Summary

Miners continue to demonstrate great confidence in the Bitcoin network, despite a significant decrease in income, with the hash rate still slightly below the historical peak. However, as miners tend to be pro-cyclical, being sellers during downturns and holders during upswings, it can be expected that sellers will face some pressure if there is further decline.

At the same time, interaction between investors and exchanges continues to decline, with trading volume shrinking overall, indicating a waning interest in investment and trading. This is also evident among institutional investors, as both Bitcoin and Ethereum ETFs have seen net outflows.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。