Author: sui14

Compiled by: Ladyfinger, BlockBeats

Editor's note:

This article provides an in-depth analysis of the impact of the Dencun upgrade on the Ethereum L2 network, revealing the positive results of the upgrade in reducing transaction costs, increasing user activity, and asset inflows on L2 networks, while also pointing out the negative effects such as network congestion and high rollback rates caused by MEV activities. The article calls for community attention and joint development of MEV solutions adapted to L2 characteristics to promote the healthy development of the Ethereum ecosystem.

Introduction

In this article, we aim to provide a data overview of the current L2 status. We monitored the importance of the Dencun upgrade in March for the reduction of gas fees on L2, studied how activities on these networks have evolved, and emphasized the emerging challenges driven by MEV activities. In addition, we discussed potential barriers to developing MEV tools and solutions for L2.

Positive aspects: Adoption of L2 after the Dencun upgrade

Gas costs reduced by 10 times

The gas fees on Ethereum L2 consist of two parts: the cost of executing transactions on L2 and the cost of submitting batch transactions to Ethereum L1. Different L2 gas fee structures and sorting rules vary due to their development stages and design choices. For example, Arbitrum operates on a first-come, first-served (FCFS) basis, processing transactions in the order they are received. In contrast, Optimism (OP Mainnet) and Base, as part of the OP Stack, use a priority gas auction (PGA) model, which combines L2 base fees and priority fees. Users can choose to pay higher priority fees to be included faster and appear earlier in the block. Understanding the fee structure is crucial for understanding the growth of the ecosystem and MEV dynamics.

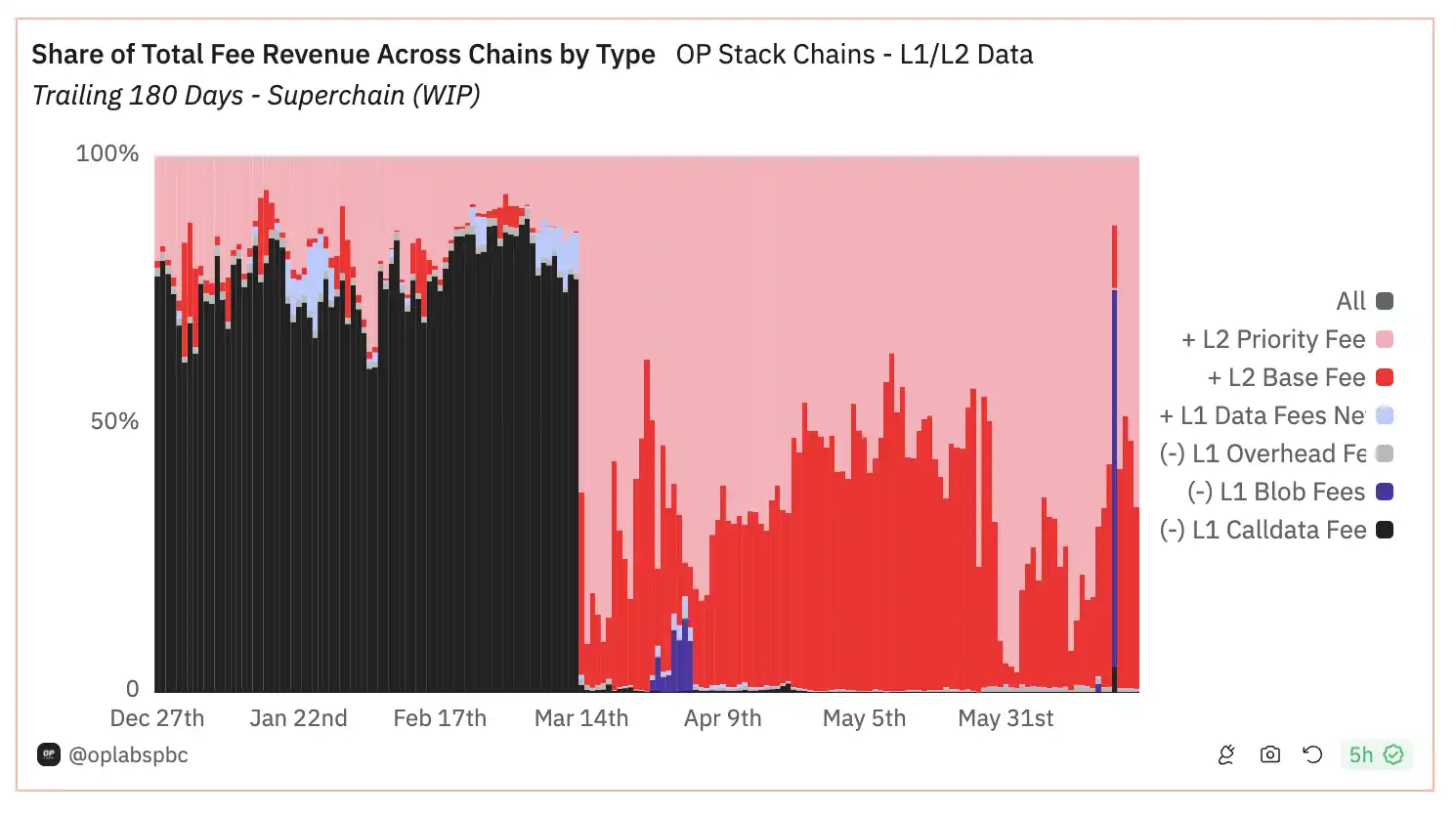

Historically, the fees on Ethereum L1 have constituted the majority of the total fees users need to pay when trading on L2, accounting for over 80% of the costs, as shown by the black bars in the graph below. However, after the Dencun upgrade on March 14, L2 transitioned from using calldata to a more economical method, known as "blobs 1," for submitting batches to L1. This temporary storage includes its own gas auction, composed of blob base fees and priority fees.

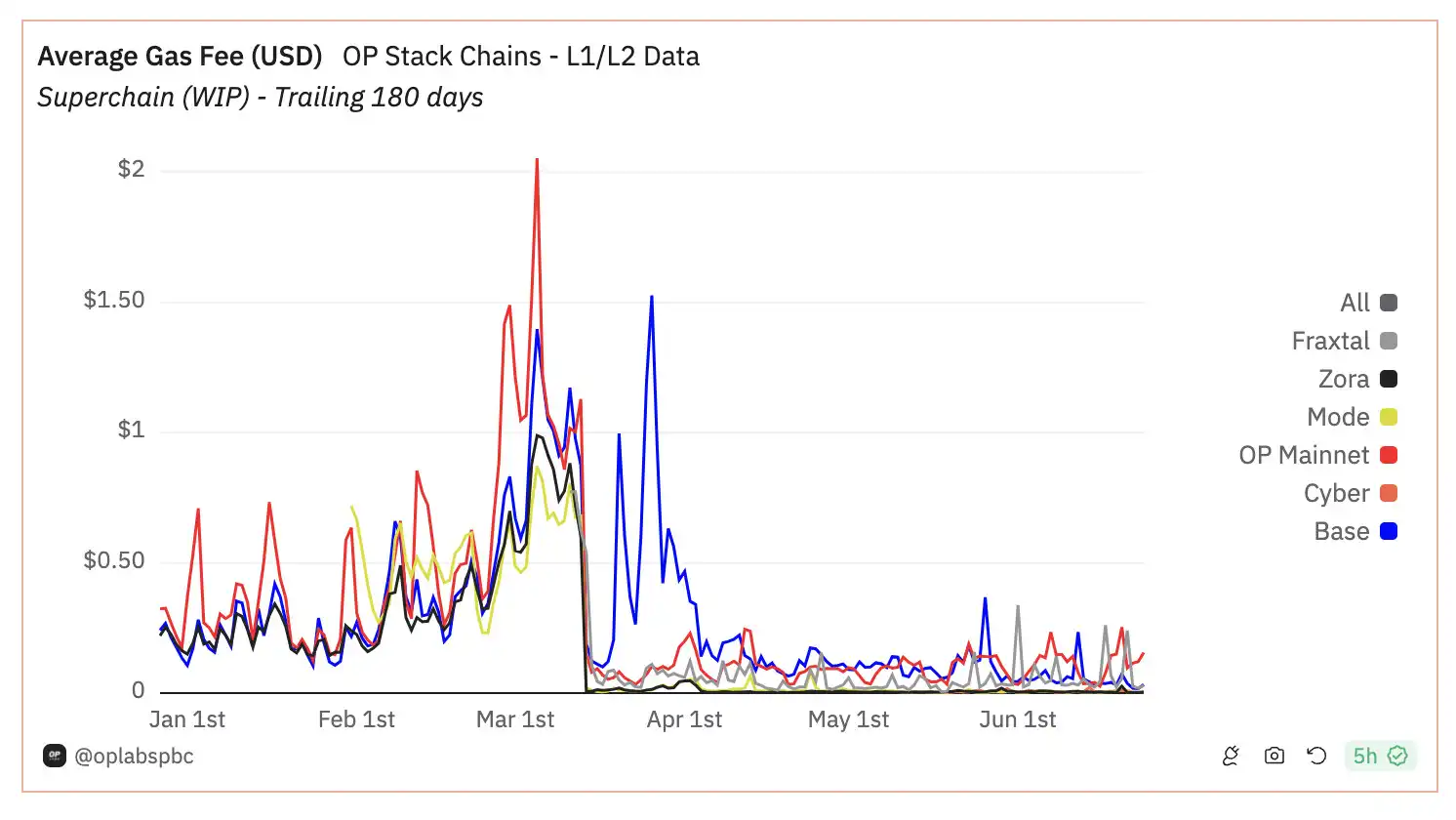

Since Dencun, the fees paid by L2 to L1 have significantly decreased— the chart shows a significant change in the gas cost breakdown of the OP Stack chain, with L1 costs plummeting from over 90% to just 1%, while L2 costs now account for 99% of the total costs. This shift has led to an overall approximate tenfold decrease in the average total gas fees on L2, for example, the average gas fee on OP Mainnet dropping from about $0.5 per transaction to $0.05.

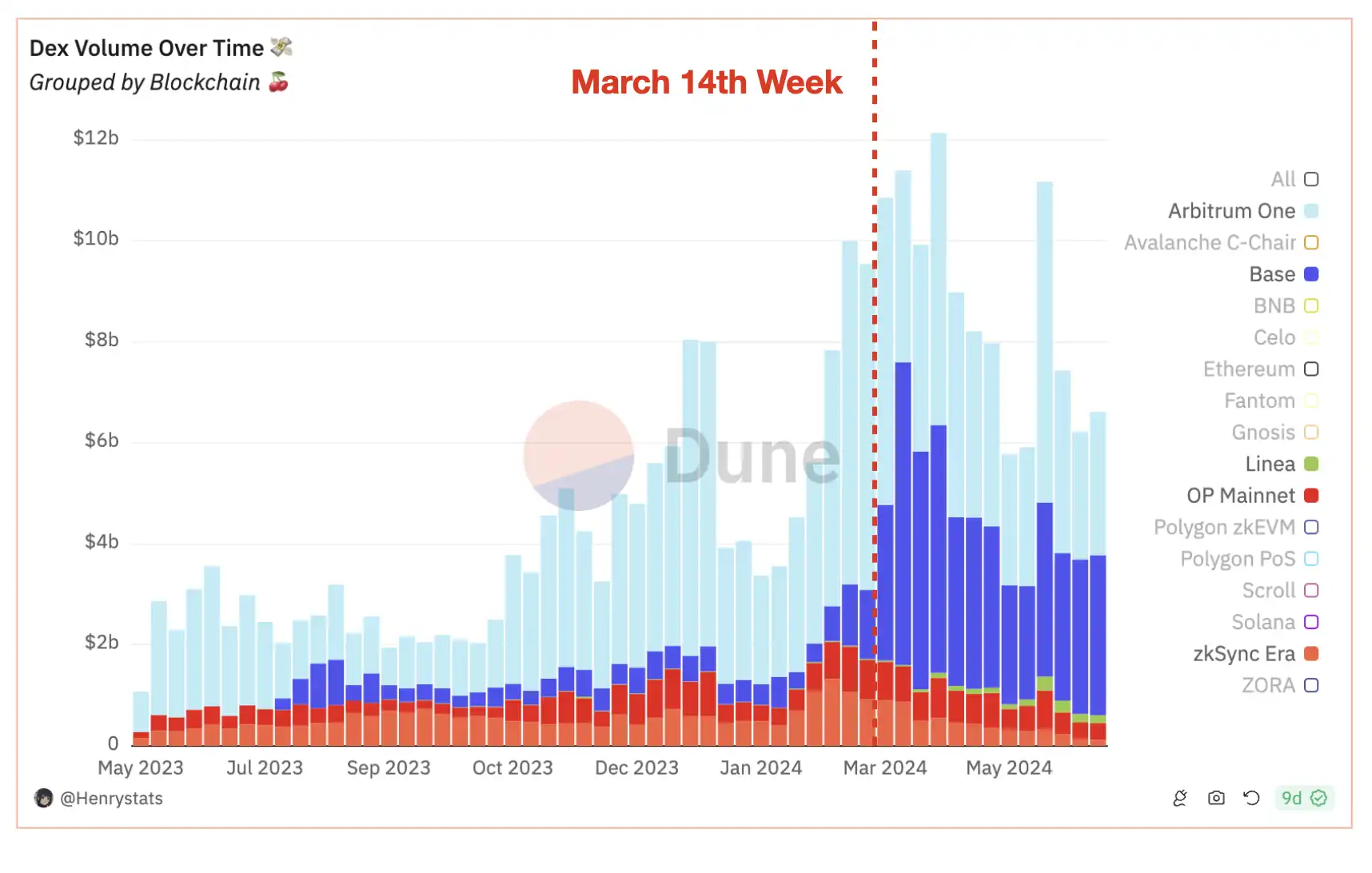

Surge in activity on L2

After the cost reduction, there has been a significant increase in activity and usage on L2, as evidenced by the surge in L2 gas fees in the graph above. It is worth noting that on March 26, the average gas fee on Base exceeded the pre-upgrade peak. To accommodate more transactions and reduce network congestion, Base began raising its gas target from March 26 and made several adjustments thereafter.

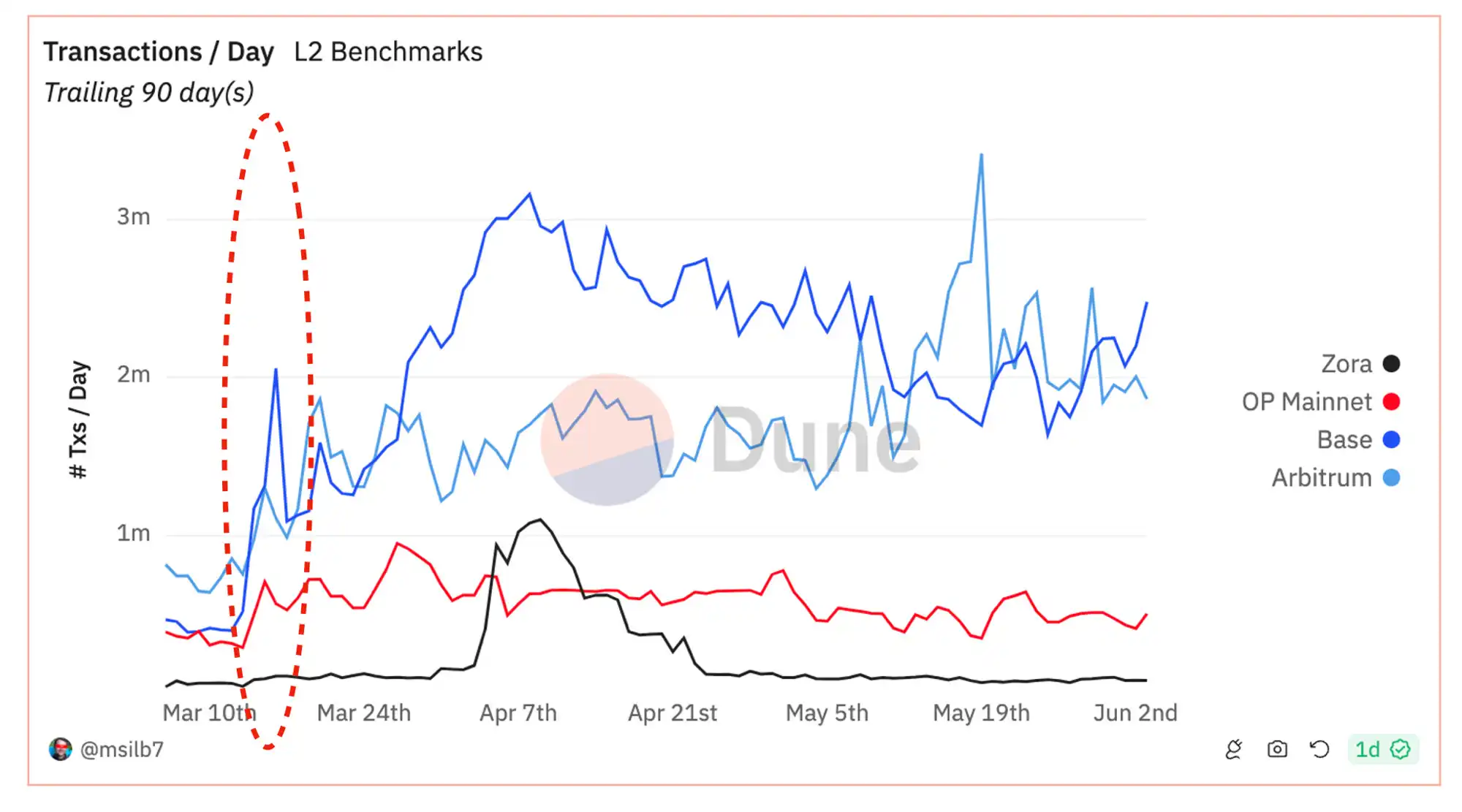

The chart below highlights the daily transaction volume on L2, showing significant growth on networks such as Arbitrum, Base, and OP Mainnet. In particular, the daily transaction volume on Base has quadrupled, now processing approximately 2 million transactions per day.

Although it is difficult to determine whether this is the result of organic participation or influenced by incentive programs and Sybil activities, since the end of last year, with improved market conditions and the arrival of the memecoin season triggered by WIF on Solana, all major active addresses and DEX trading volumes on L2 have significantly increased after the EIP-4844 upgrade, especially on Base and Arbitrum.

Inflow of assets to L2

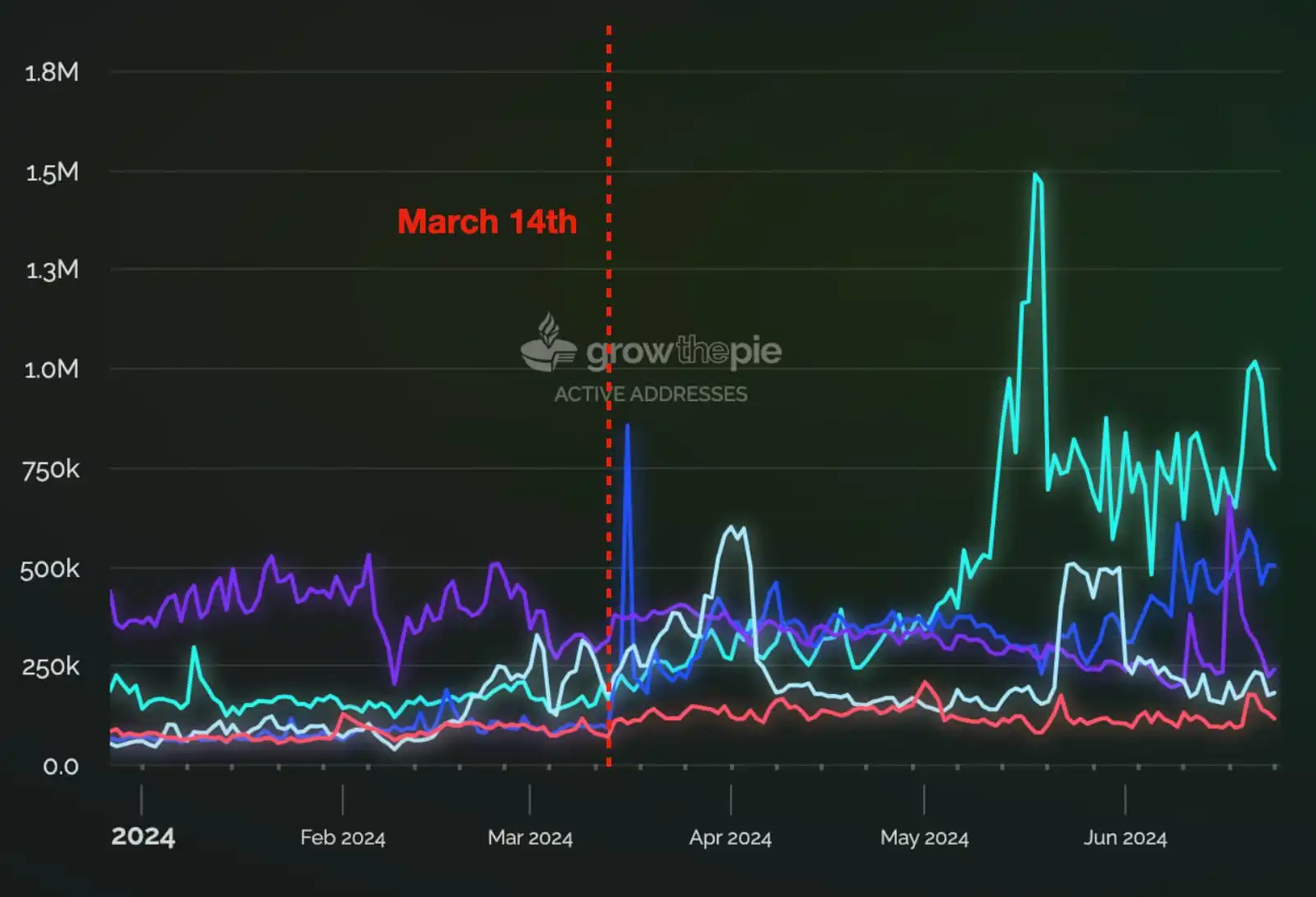

With improved market conditions and the arrival of the memecoin season triggered by WIF on Solana, the total value locked (TVL) on L2 has been steadily increasing since the end of last year. It is noteworthy that Base has become the fastest-growing chain, with its recent total TVL surpassing that of OP Mainnet.

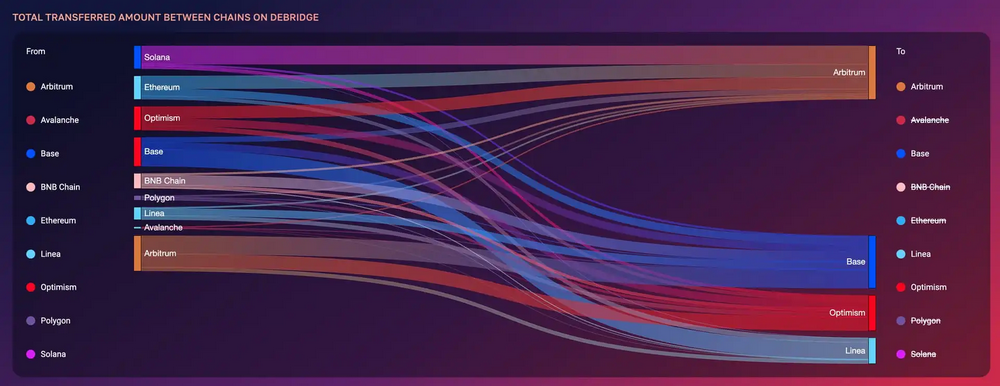

Since early March, Base has seen an inflow of approximately $1.5 billion USDC, some of which was transferred by Coinbase from customer and corporate funds to Base. According to data from Artemis on 11 major bridges since January 2024, there has been an outflow of $14 billion from Ethereum to major L2s. Arbitrum leads with approximately $7 billion, followed by zkSync, Base, and OP Mainnet. Further data from Debridge Finance confirms that this is a widely used cross-chain bridge in EVM chains and Solana, and it confirms that Arbitrum and Base are the top recipients of all fund outflows.

Negative aspects: As gas fees decrease, hidden MEV activities gradually increase

When we further examined the transactions, we noticed that bot trading activity is increasing gas fees and rollback rates on L2. In the next section, we will use statistical data from Base to conduct a case study and discuss in more detail the impact of cheaper gas on L2 after the Dencun upgrade.

L2 after the Dencun upgrade: Similar to Ethereum without Flashbots, but lacking transaction pools

Network congestion

Challenges began to emerge on March 26, when the average daily gas fees on the Base network briefly surged, exceeding the levels before the Dencun upgrade. However, on June 3, Base raised its gas target to 7.5M gas/second, compared to 2.5M gas/second during the Dencun upgrade, which reduced the average gas cost to approximately 5 cents.

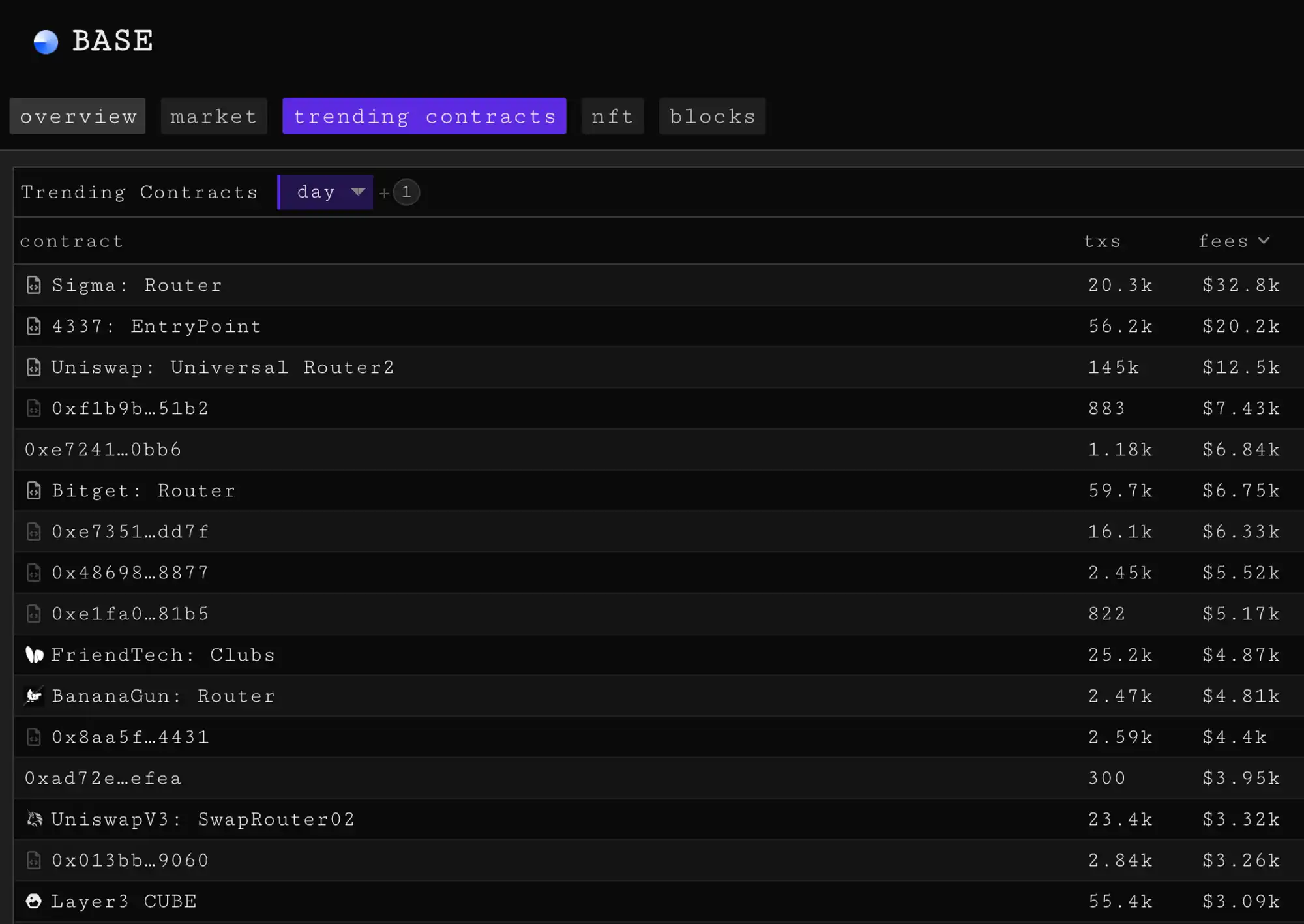

On the Base network, the contracts that consume the most gas include Telegram trading bots like BotSigma and Banana Gun, as well as digital wallets and DEXs such as Bitget and Uniswap. Additionally, many unmarked contracts are involved in activities such as token minting, meme coin trading, and atomic arbitrage. These contracts are ranked based on gas fees on the Base network.

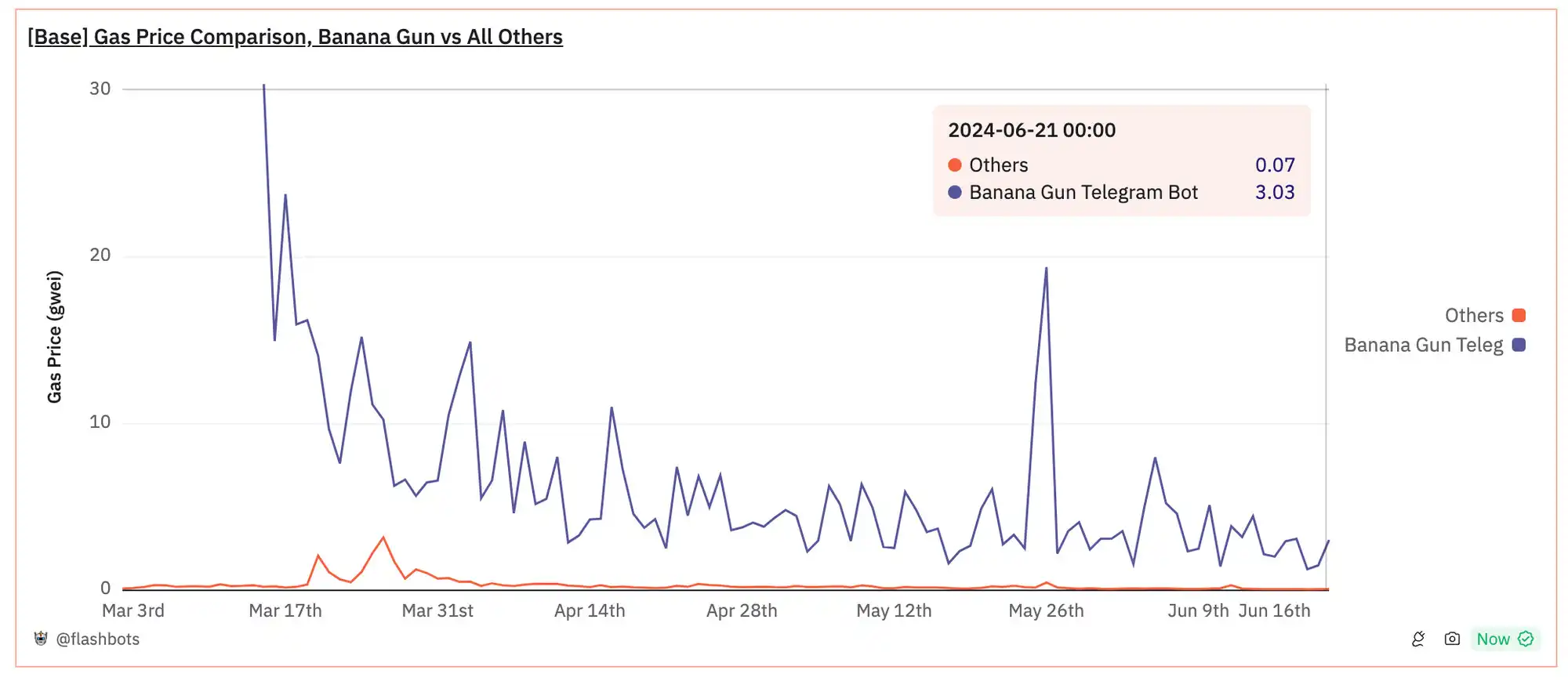

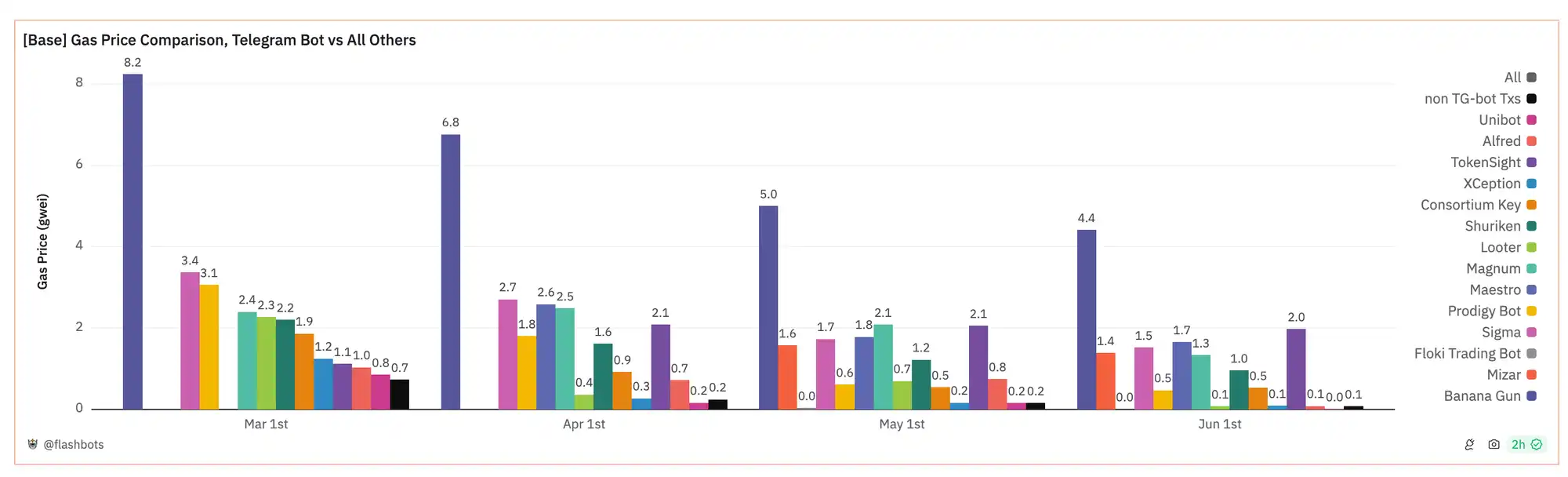

By comparing the behavior of popular Telegram bots like BananaGun, it is evident that the transactions they conduct result in significantly higher gas fees than regular transactions. After the Dencun upgrade, users executing transactions on the Base network using the BananaGun Telegram bot experienced peak gas prices of 30 Gwei. Although this rate later stabilized at around 3 Gwei, it was still 43 times higher than the gas fees for other transactions.

Daily gas prices on Base, comparison of Banana Gun transactions with other transactions

When analyzing the average monthly gas prices paid by mainstream DEX trading bots on Base and comparing them with non-Telegram bot transactions (represented by black bars), it is clear that users using trading bots incur significantly higher gas costs. The following is a comparison of monthly gas prices on the Base network, showing the differences between all Telegram bots and other transactions.

Surge in high rollback rates

The rollback rate of transactions on a blockchain network is an important indicator of its health. We noticed that after the Dencun upgrade, especially on L2 networks like Base, Arbitrum, and OP Mainnet, the rollback rates have increased. Currently, the rollback rate on the Ethereum mainnet is approximately 2%, while on Binance Smart Chain and Polygon, it ranges between 5-6%. Before the Dencun upgrade, Base maintained a rollback rate of about 2%, but it sharply rose to approximately 15% after the upgrade, reaching a peak of 30% on April 4. Meanwhile, Arbitrum and OP Mainnet also experienced periodic spikes in transaction failure rates, fluctuating between 10% and 20%.

Cross-chain transaction rollback rates

Upon further analysis, we found that the high rollback rates on L2 networks do not always represent the actual experience of regular users. Instead, these rollbacks are likely caused by MEV bots. By using the following heuristic approach (Query 2), we identified a set of router contracts exhibiting behavior similar to that of bots—showing high rollback rates when executing MEV extraction transactions:

Since the Dencun upgrade,

- Active routers: The contract processed over 1000 transactions.

- Limited interaction EOAs: Less than 10 external owned accounts (EOAs) wallets interacted as transaction senders.

- Sender distribution: Less than 50% of transaction senders only sent one transaction, indicating that the user group did not exhibit a long-tail distribution. This suggests that routers are unlikely to be used by retail users.

- Behavior pattern: Transaction history precisely covers 24 hours or shows multiple transactions in one block, indicating non-human behavior.

- Exchange concentration: Over 75% of successful transactions involve exchanges.

- Detected MEV transactions: Over 10% of successful transactions use atomic MEV strategies, as detected by hildobby's heuristic approach.

Using these criteria, we detected 51 routers on Base, likely representing a conservative lower bound estimate of bot activity on Base.

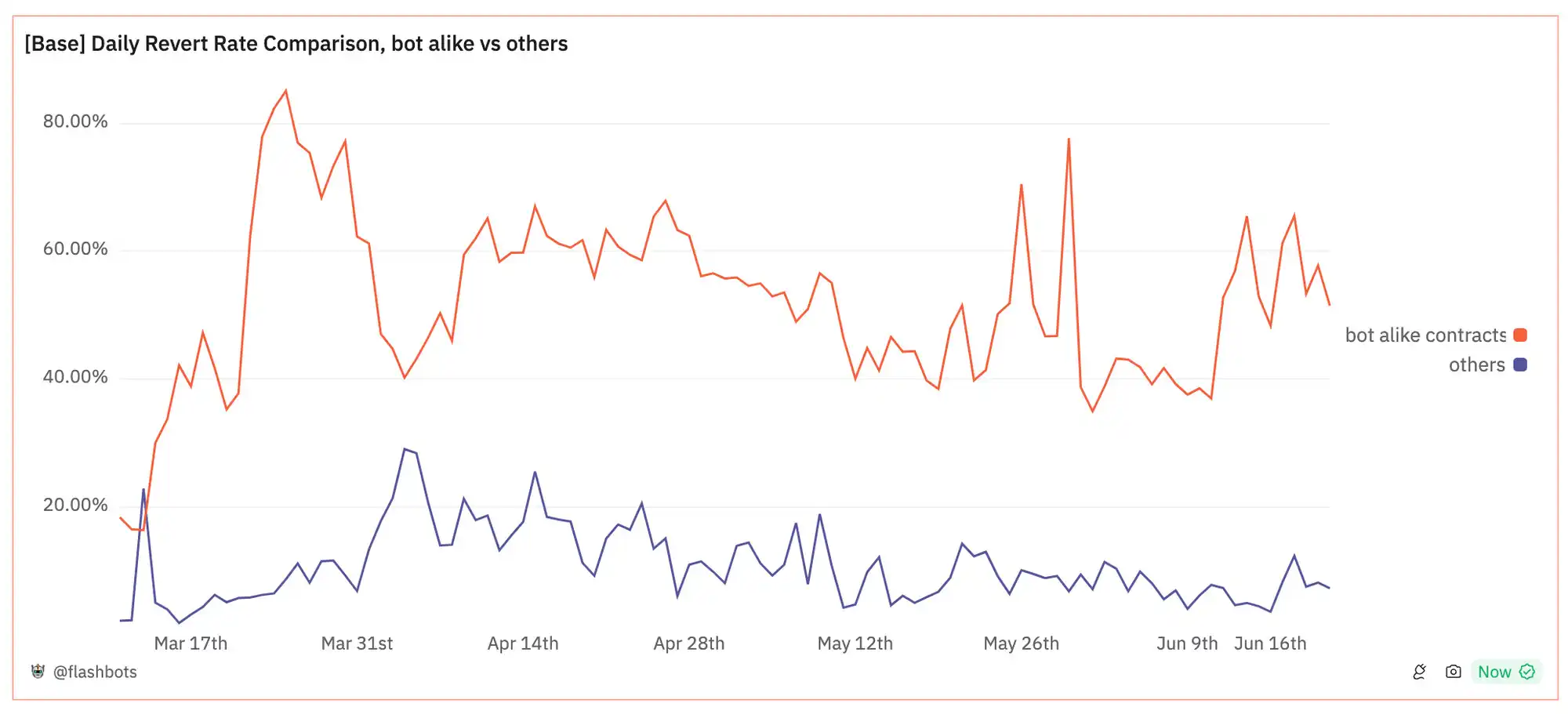

We divided all transactions processed by routers on the Base network into two groups and conducted a comparative analysis. The results showed a significant difference in rollback rates between similar bot-like routers and other transactions: the average rollback rate of bot-like contracts reached 60%, which is six times higher than the approximately 10% observed for other transactions.

Daily rollback rates on Base, comparison of bot-like contracts with other transactions

Based on the data above, we can infer that automated trading activities such as MEV bots and Telegram bots are likely a major contributing factor to the high gas fees and high rollback rates on the Base network.

The single sequencer architecture on L2, combined with the lack of a public transaction pool, has fostered a large amount of MEV strategies utilizing sequencers, which have become the main cause of network congestion. This congestion is particularly evident on L2 networks using the priority gas auction (PGA) mechanism, such as OP Mainnet and Base. The result is not only network congestion but also a significant waste of block space and gas fees due to rolled-back transactions and MEV searcher activity. This situation is similar to the state of Ethereum before the emergence of Flashbots, with the difference being the absence of sandwich MEV due to the lack of transaction pools on L2.

How Large is the Scale of MEV on L2?

Understanding MEV activity on L2 networks is crucial for assessing its impact. However, there is currently no widely accepted figure for L2 MEV data that has been verified through multiple sources and reliable methods. Additionally, compared to the Ethereum mainnet, L2 lacks real-time monitoring data provided by tools such as mev-inspect, libmev, and eigenphi, which are crucial for measuring the total amount of MEV and miner profits.

Some of the L2 MEV datasets and research papers published to date include:

An open-source dataset built by hildobby on Dune Analytics (heuristic links: sandwich, sandwiches, atomic arbitrage)

The research paper "Quantifying MEV On Layer 2 Networks" by Arthur Bagourd and Luca Georges Francois, which quantifies MEV on Polygon, OP Mainnet, and Arbitrum using mev-inspect. The research was sponsored by Flashbots.

The research paper "Rolling in the Shadows: Analyzing the Extraction of MEV Across Layer-2 Rollups" by Christof Ferreira Torres, Albin Mamuti, Ben Weintraub, Cristina Nita-Rotaru, and Shweta Shinde, which quantifies activity and discusses new MEV strategies on L2, leveraging the role of sequencers and batch confirmation delays.

In addition to the above resources, Sorella Labs will soon release their MEV data indexer tool Brontes, an open-source repository for Ethereum mainnet and L2. Flashbots and Uniswap Foundation are seeking funding to expand L2 MEV classification and quantification. If you are working in this area or interested in collaboration, please contact the Flashbots Market Research Team.

Although further validation is needed, the dataset published by hildobby on Dune Analytics provides a valuable preliminary reference standard.

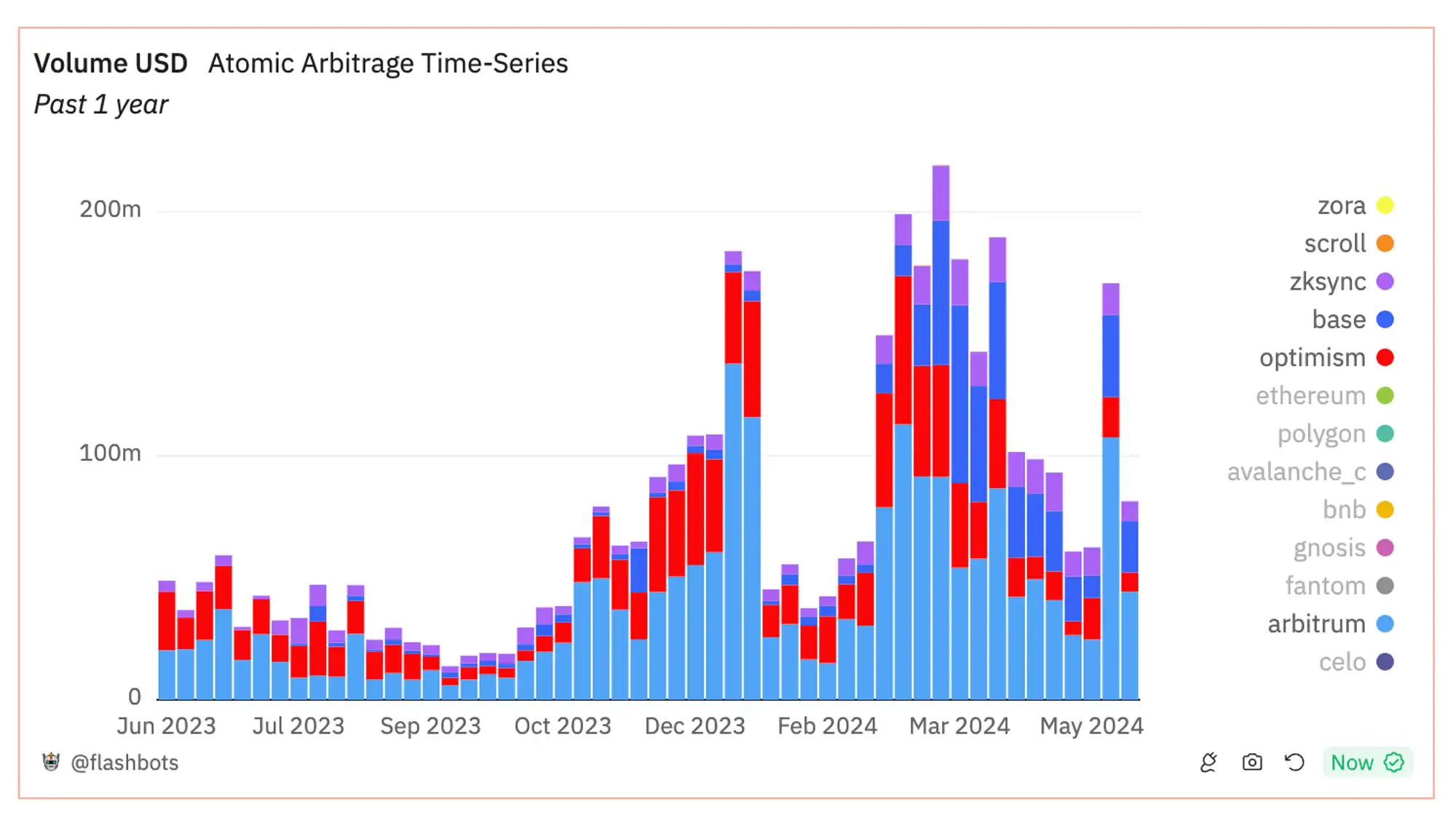

Atomic arbitrage volume on L2 using hildobby's dataset

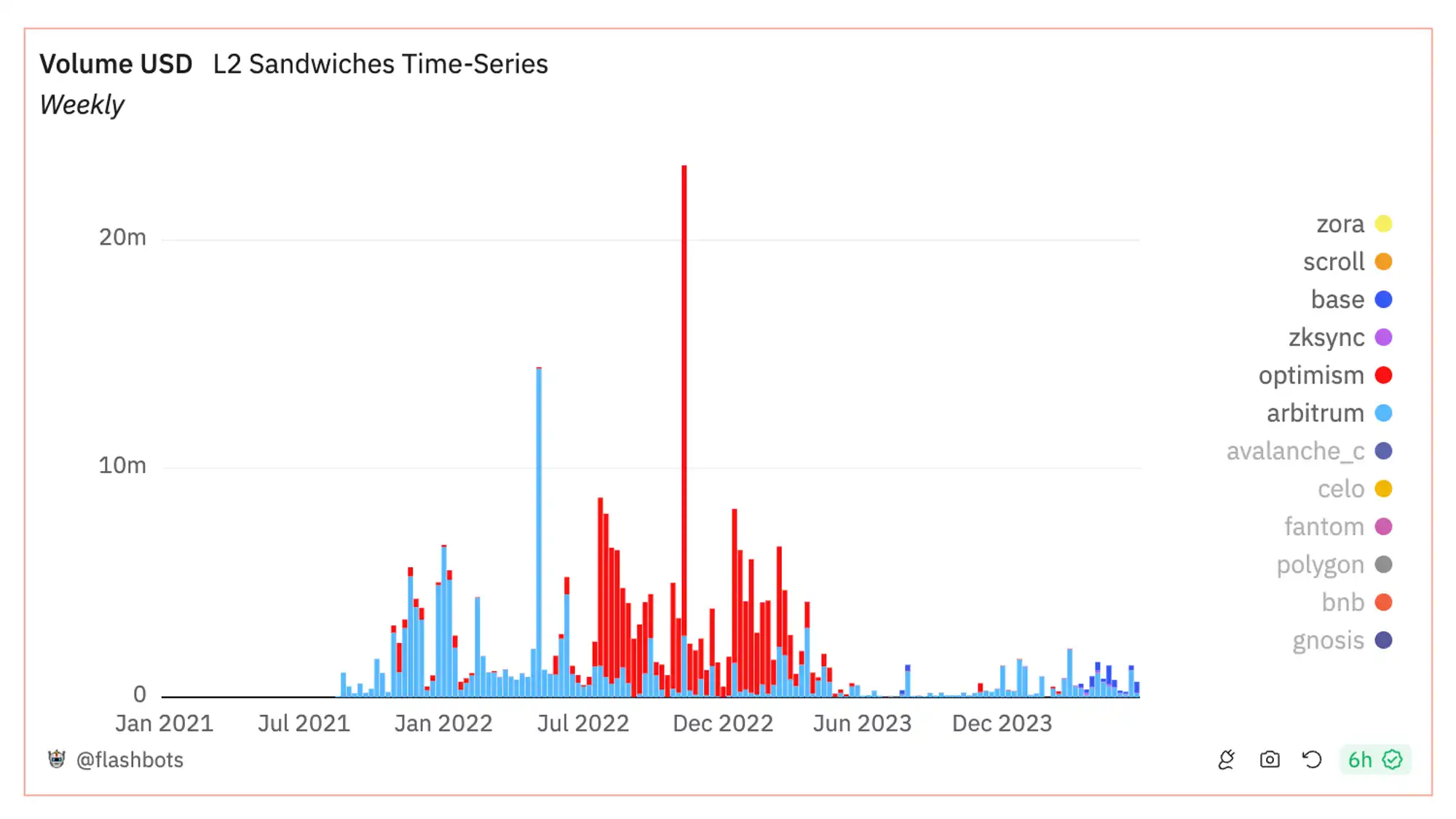

In the past year, the volume of atomic arbitrage MEV transactions on six major L2 networks, including Arbitrum, OP Mainnet, Base, Zora, Scroll, and zkSync, has exceeded $36 billion, accounting for 1% to 6% of the total decentralized exchange (DEX) trading volume on each chain. Initially, this MEV transaction volume was mainly concentrated on Arbitrum and OP Mainnet, but it has gradually shifted towards Base and zkSync.

Compared to atomic arbitrage volume, the volume of sandwich attack transactions on L2 networks is significantly lower, in stark contrast to Ethereum, where the volume of sandwich attacks is four times that of atomic arbitrage. This difference is mainly due to the single sequencer setup on L2 networks, which lacks a transaction pool, limiting the ability of searchers to execute sandwich MEV using user transactions in the transaction pool, unless there is a data leak from the transaction pool or a sandwich attack initiated by a single sequencer. Therefore, on L2, atomic arbitrage, flashbots, statistical arbitrage, and liquidations have become more feasible strategies for searchers.

Ethereum MEV Decomposition

How much remaining MEV income is there in the MEV market on L2?

While it is difficult to precisely quantify the MEV market, we can examine the numbers in other ecosystems with MEV solutions for size comparison:

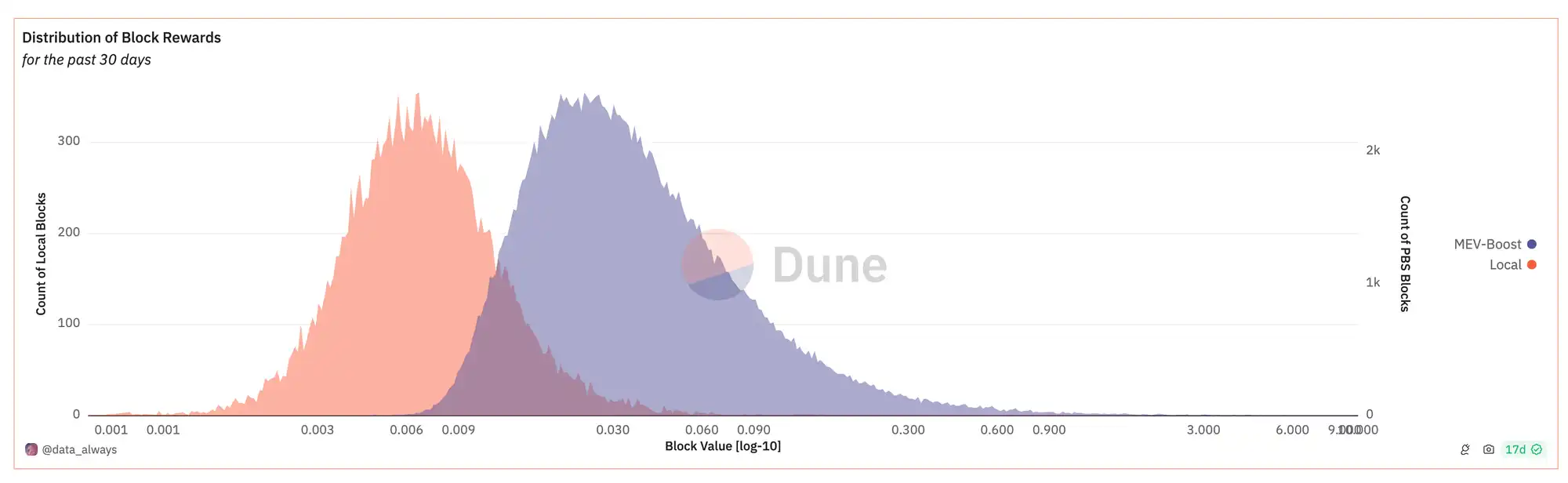

- On Ethereum L1, the annual validator income from MEV-boost blocks is approximately $96.8 million (based on an estimated price of $3500/ETH); the median value of MEV-boost blocks is four times the value of regular validator blocks.

Block reward distribution between regular blocks and MEV-boost blocks

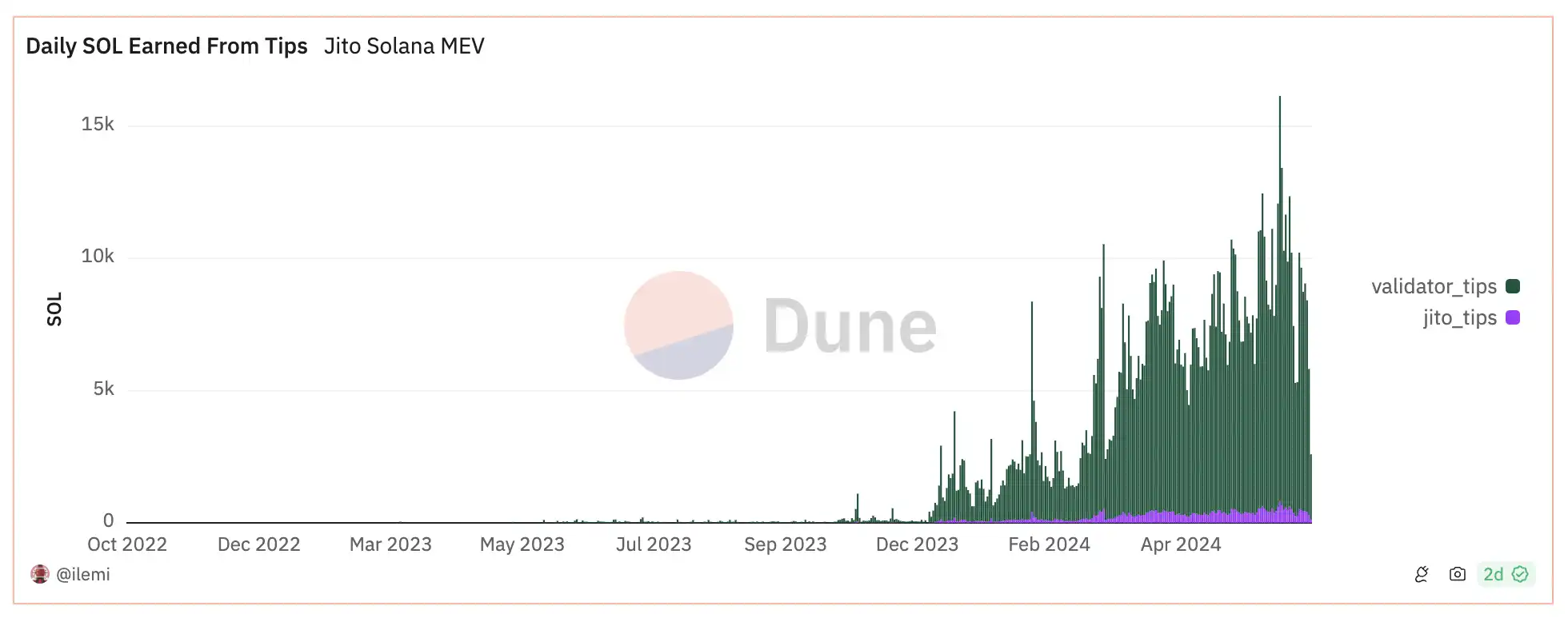

- On Solana, validators collect additional MEV income from validator tips through Jito's bundling service, based on a weekly 50,000 SOL, estimated to be approximately $338 million (based on a price of $130/SOL).

Daily tips earned through Jito's bundling service, per validator with Jito Labs

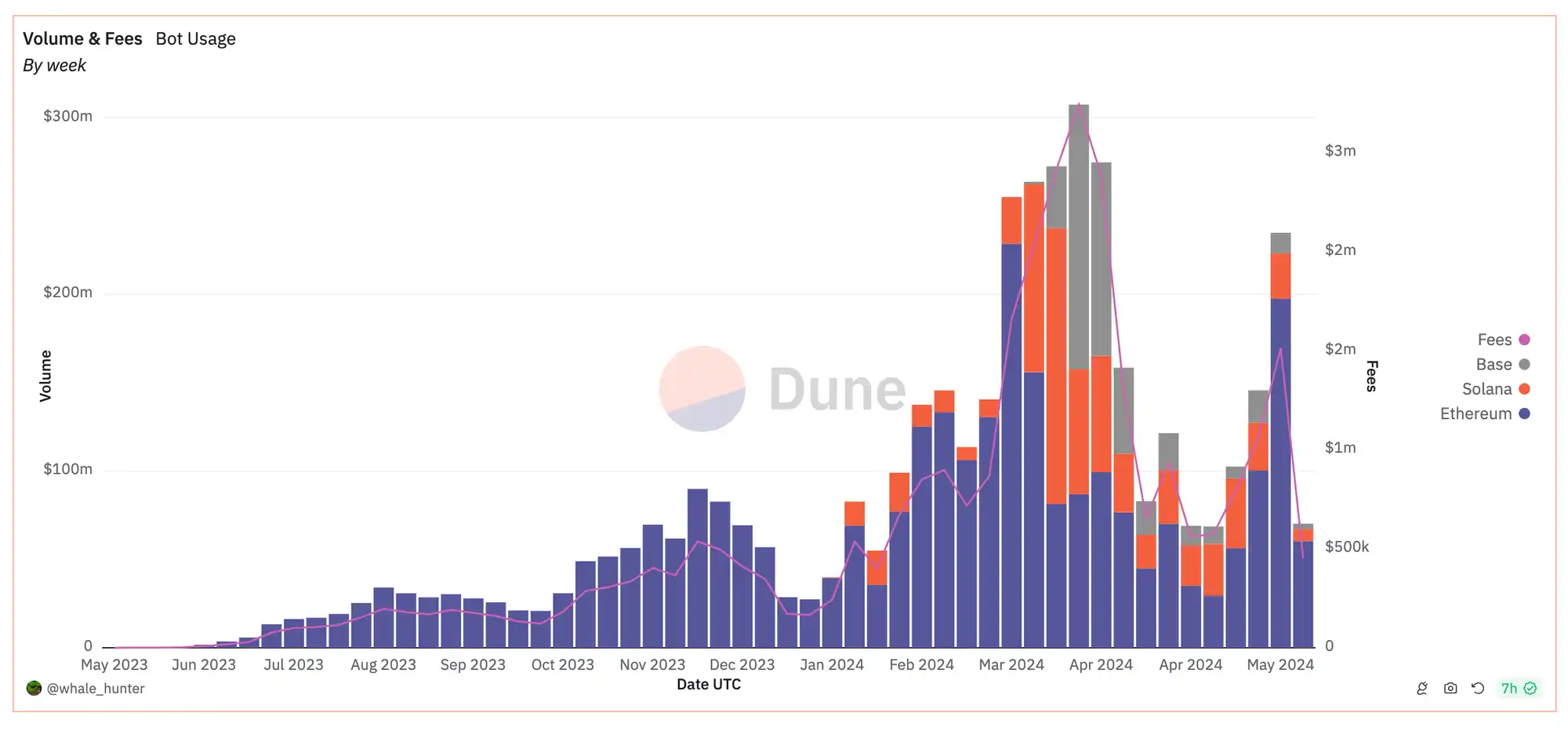

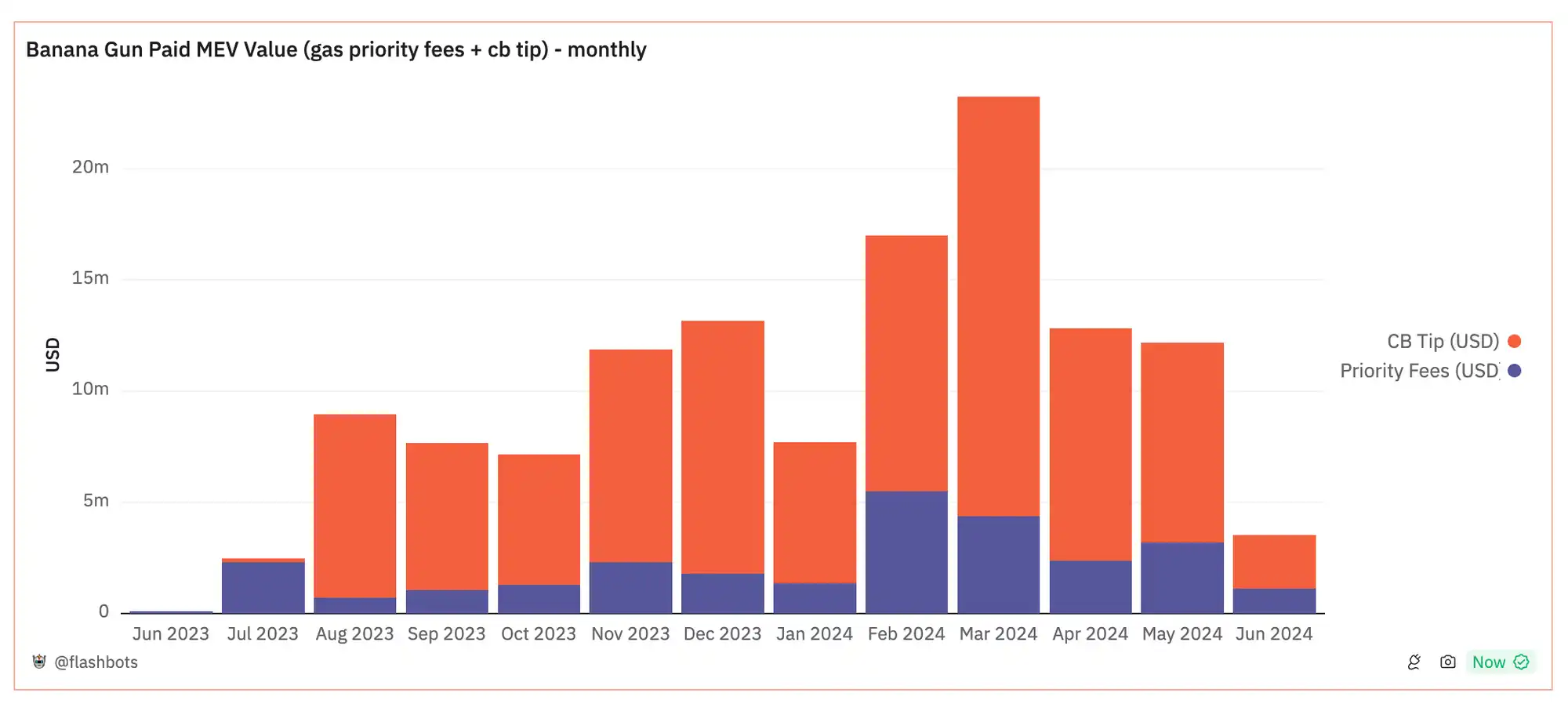

While the exact total MEV volume on the Base network has not been disclosed, we can estimate the market size by observing the income of the Banana Gun Telegram Bot, one of the most active participants in the market. Banana Gun has roughly the same trading volume on Base's L2 network and Solana, generating over $1 million in daily trading volume on each chain, equivalent to over $10,000 in transaction fees per chain per day.

Cross-chain volume and fees for Banana Gun Telegram Bot

It's important to note that the market share of Banana Gun Bot on Solana may significantly differ from that on Base. For example, there are several other major Telegram Bots on the Solana platform, such as Sol Trading Bot and BonkBot, while Base may support fewer Telegram Bots. Therefore, the proportion of trading volume and MEV income for Banana Gun on Solana cannot be directly used to estimate the total MEV income on Base.

However, using another predictive method, we can see different results: in March, Banana Gun Telegram Bot paid over $23 million to Ethereum's block producers and validators. Specifically, during the week of March 26 to April 1, the trading volume of Banana Gun on Base actually exceeded that on Ethereum, as indicated by the peak in the chart, implying a huge potential for MEV income on the Base network. This comparison of cross-chain trading volume reveals the growth prospects of Base in terms of MEV.

Of course, there are significant differences between Base and Ethereum in the MEV ecosystem. Compared to Ethereum, MEV competition on Base may not be as intense, which could lead to lower fees required by Bots when bidding to validators. Nevertheless, meme coin trading Bots that rely heavily on sandwich attacks and arbitrage mechanisms remain viable under Base's sequencer architecture.

MEV income paid by Banana Gun Telegram Bot to validators

Focus on MEV Issues in L2 Networks

Ethereum has developed a mature MEV ecosystem, equipped with infrastructure tools to serve participants at various levels of the supply chain. At the protocol level, MEV-boost allows validators to outsource block construction tasks through auction. For searchers, bundling services provided by Ethereum block producers—similar to Jito Labs on Solana and FastLanes on Polygon—enable them to implement MEV strategies with rollback protection. These services ensure that block producers simulate transactions and only execute those that are guaranteed not to be rolled back. Additionally, private RPC services like Flashbots Protect provide ordinary users with a way to bypass public transaction pools and their potential risks. However, there is still significant room for improvement in developing MEV infrastructure comparable to this in current L2 networks.

Why Focus on MEV Strategies and Solutions in L2 Networks?

The phenomenon of MEV still exists in environments lacking transaction pools and plays a crucial role in maintaining market efficiency, particularly through the execution of statistical arbitrage, atomic arbitrage, and liquidation strategies in outdated AMMs and lending markets.

However, the lack of mature MEV infrastructure, such as bundling services, may lead to some negative consequences. Without transaction pools, many MEV strategies may degrade into spam strategies, leading to:

- Increased network rollback rates;

- Aggravated network congestion.

By implementing bundling services, the focus of MEV competition can be shifted from the main chain to the auxiliary chain, effectively alleviating the high gas fee burden faced by users due to MEV bot competition. At the same time, searchers can enjoy higher profits due to rollback protection, reducing the risk cost of failure.

For L2 networks using shared sequencers, current mainstream solutions often require users to submit transactions to public transaction pools, which may lead to a resurgence of sandwich attacks. In this case, MEV protection tools like Flashbots Protect are particularly important, as they not only protect users from the threat of sandwich attacks but may also provide refunds for MEV or priority fees, ensuring users receive better transaction execution and more favorable prices.

The development of complex MEV infrastructure faces some unresolved challenges. Firstly, as more value flows to sequencers, the profit model for searchers will change over time, and marginal profits may decrease. This change may raise questions about the sustainability of long-term highly competitive search strategies. We expect market mechanisms to regulate this phenomenon, resulting in common search strategies paying a larger but not full proportion of the value to sequencers, while less common strategies pay less.

Furthermore, existing MEV infrastructure, such as Ethereum's block construction market, has rapidly evolving order flow dynamics. Currently, these factors have been major drivers of centralization trends in the block construction market and the rise of private transaction pools on Ethereum L1. Ensuring the competitiveness and fairness of the block construction market remains an issue that needs to be addressed.

Finally, MEV solutions for L2 networks may need to be different from current mechanisms on Ethereum, mainly due to the unique characteristics of L2: such as shorter block generation times, lower-cost block space, and relatively centralized governance structures. For example, Arbitrum has a block time of only 250 milliseconds, and it is currently unknown whether such a fast block generation rate is compatible with existing MEV infrastructure. Additionally, the ample and economical block space provided by L2 has greatly changed the landscape of transaction search, making the spam problem more severe and in need of new solution strategies. Furthermore, compared to other environments like Ethereum L1, governance in L2 is more centralized, which may allow for additional requirements to be imposed on MEV service providers, such as requiring block producers to avoid sandwich attacks on users to ensure market fairness.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。