1. Report Highlights

1.1 Core Investment Logic

Gelato has been deeply cultivating the developer services field for many years and has formed a relatively complete developer service suite. It is expected to achieve a breakthrough in its business by combining their RaaS service launched at the end of 2023.

The RaaS project has entered an intensive coin issuance period, with Altlayer, Dymension, and Saga all issuing coins recently. In addition, there are also well-funded competitors within the same field, such as Conduit and Caldera. The RaaS field is expected to continue to receive sustained market attention in the near future.

1.2 Main Risks

Difficulty in revenue generation. Gelato's two main business models, smart contract automation and RaaS, determine that its revenue generation is relatively difficult.

Strong competitors. Competitors such as Chainlink in the smart contract automation field, and Altlayer, Conduit, Caldera, and Dymension in the RaaS field, pose strong competition to Gelato. Gelato's competitive advantage is not strong enough.

Limited token use cases.

1.3 Valuation

Due to the unavailability of income data for Gelato's main business field, we are unable to make an accurate valuation.

From the perspective of circulating market value and total circulating market value, Gelato's current market value is relatively attractive compared to its competitors.

2. Project Overview

2.1 Project Business Scope

2.1.1 Automation

Mint Ventures once published a research report about Gelato in December 2021. Interested friends can go and check it out.

At that time, Gelato's main business was "automated execution of smart contracts," specifically "when condition A occurs, execute operation B in the smart contract." The products/features it launched include:

AMM limit orders (A=token price reaches a certain value, B=transaction). Gelato's limit order service was once launched as a separate product called Sobert Finance, and was also directly integrated into the official pages of PancakeSwap, QuickSwap (the largest DEX on Polygon), and SpookySwap (the largest DEX on Fantom), demonstrating the partners' recognition of Gelato's products.

Liquidation-free borrowing (A=loan-to-value ratio reaches a certain value, B=retrieve collateral, swap collateral for debt, repay debt). Gelato's feature was once launched as a product for end users called Cono Finance, and it received grants from Aave for this feature and was integrated by Instadapp.

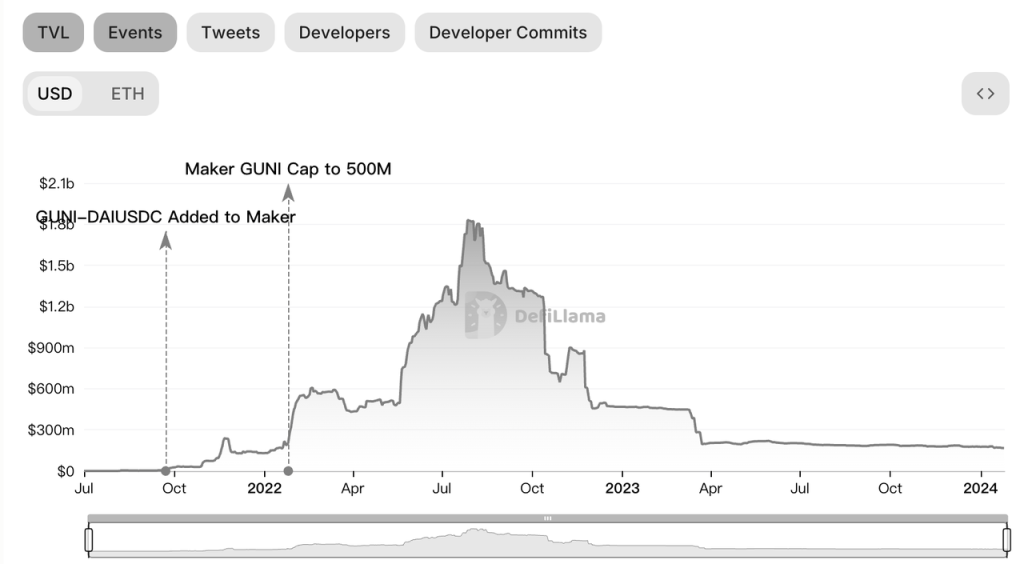

Position management tool for Uniswap V3, G-UNI (A=token price reaches a certain value, B=adjust LP market range). In September 2021, MakerDAO added GUNI's USDC-DAI LP as collateral that can generate DAI, and GUNI's TVL once rose to nearly $2 billion. In 2022, Gelato spun off GUNI as Arrakis Finance and prepared to issue its own coin. However, as MakerDAO's business focus shifted to RWA in 2022, Arrakis's TVL significantly decreased.

* Arrakis TVL Changes Source: Defillama

* Arrakis TVL Changes Source: Defillama

In addition to the above three typical functions, Gelato's Automate has many other use cases, which have also been used by many DeFi projects, such as automatically earning yields for Yield Framing protocols, updating oracles, and more.

Source: Gelato Official Website

Overall, Gelato's automation business provides many useful products for crypto developers and users, bringing a lot of convenience.

Gelato plans to upgrade its automation service to "Web3 Function" in June 2024, which will support more trigger conditions, allowing developers to execute on-chain transactions based on any off-chain data (API/graph, etc.). These trigger conditions will be stored on IPFS and ultimately submitted to Gelato for execution.

2.1.2 Rollup as a Service

Gelato officially launched its Rollup as a Service (RaaS) at the end of 2023. RaaS can help developers choose the right technology stack to easily deploy a Rollup. With the rapid development of ETH L2, leading L2 projects have all launched their own open-source frameworks (Optimism launched the OP stack, Arbitrum launched Arbitrum Orbit, and Polygon launched Polygon CDK) to help developers quickly deploy a Rollup. As a result, a large number of third-party service providers like Gelato have emerged to assist developers with "blockchain-related needs."

Although RaaS is a nascent field, the current competition is fierce. We will provide a detailed analysis in section 3.1 on industry space and competitive landscape.

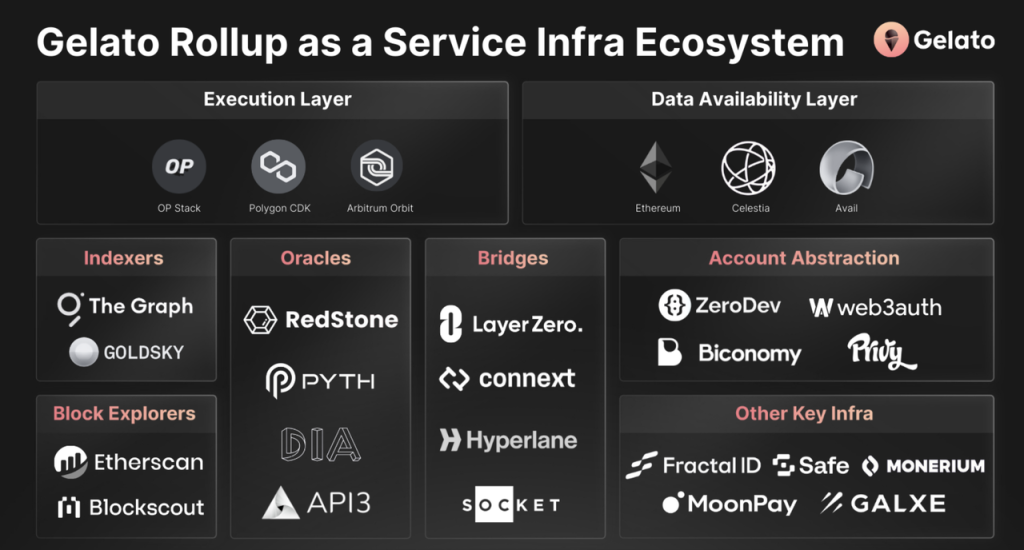

Gelato's RaaS service has already integrated with many infrastructure service providers:

Integrated OP stack, Polygon CDK, and Arbitrum Orbit at the execution layer

Integrated Ethereum, Celestia, and Avail at the DA layer

Integrated Layerzero and Connext for cross-chain purposes

Integrated Redstone, Pyth, and API3 for oracles

Integrated The Graph and Goldsky for indexing

Integrated Moonpay and Monerium for fiat payments, Fractal ID for KYC services, and Safe for wallet services, among others

In general, apart from some businesses competing with Gelato, such as Chainlink, Gelato has integrated with the vast majority of infrastructure service providers, providing developers with a relatively comprehensive suite.

Gelato's RaaS currently has 2 users: Astar Network ($ASTR) and Lisk ($LSK). Astar Network completed a $22 million financing round led by Polychain in January 2022 and is a well-known public chain in Japan. They plan to use Gelato's RaaS service to launch a zk Rollup based on Polygon CDK. Lisk is a well-established application chain project that recently announced its transition to become ETH's L2.

Another upcoming user is Ape, and Gelato has proposed to become a RaaS service provider for ApeChain on ApeDAO's governance forum. This is currently in the discussion phase on the governance forum.

2.1.3 Relay

In 2021, Gelato launched the Relay service. The Relay service allows protocols to pay gas fees on behalf of users, thereby lowering the barrier for users to enter the Web3 world.

Some typical use cases include:

Helping users of NFT protocols to mint NFTs without gas fees. The NFT creation and collection protocol Zora has used Gelato's Relay functionality.

Assisting users of cross-chain bridge protocols to perform cross-chain transactions without gas fees. Specific users include Connext Network and Kinetex.

Source: Gelato Official Website

According to information provided by IOSG, nearly half of Gelato's business volume from 2022 to 2023 came from Relay, and the income from the Relay network became a key source for the team to survive the bear market. However, Gelato's team has not publicly disclosed the income from the Relay service.

2.1.4 Other Infrastructure Services

Gelato also provides many other infrastructure services, such as:

Verifiable Random Function (VRF), which provides verifiable random number services for the crypto world and can be applied to games, NFTs, and other projects.

Account Abstraction, an intelligent wallet established based on the ERC-4337 standard.

Multi-chain payment service 1Balance, which helps developers easily handle various payment issues and supports the payment for all of Gelato's businesses.

The above infrastructure services have also been integrated into Gelato's RaaS components. With years of deep cultivation in the web3 developer services industry, Gelato may have a significant advantage over other RaaS competitors due to its rich development toolkit.

2.2 Team Overview

Gelato's two co-founders, Hilmar Orth (X:@hilmarxo) and Luis Schliesske (X:@gitpusha), are both developers, and the core features of Gelato's products were initially developed by them. They have been close friends since university and have been working together ever since. Before Gelato, they co-founded a startup focused on helping large European companies explore new business models using smart contracts. They also participated in a series of hackathons, including ETHParis, ETHBerlin, ETHCapetetown, and Kyber Defi Hackathon, where they achieved good results and influence. It was through these experiences that they were able to secure grants from Gnosis and MetaCartel and establish Gelato Network.

According to LinkedIn, the Gelato team consists of 29 people, making it a medium-sized crypto team. Based on the recruitment situation on the official website, the team continues to show a strong willingness to expand in business development and marketing.

Looking at Gelato's past development, they have been able to provide useful products, but their investment in business development has not been substantial. According to a post on the governance forum, their total budget for marketing and business development in 2022 was only $103,600.

The importance of investment in business development and marketing for infrastructure projects is evident from the development journeys of Chainlink and Polygon. Whether Gelato can effectively increase its investment in business development and marketing may be a key point for its future development.

2.3 Financing and Key Partnerships

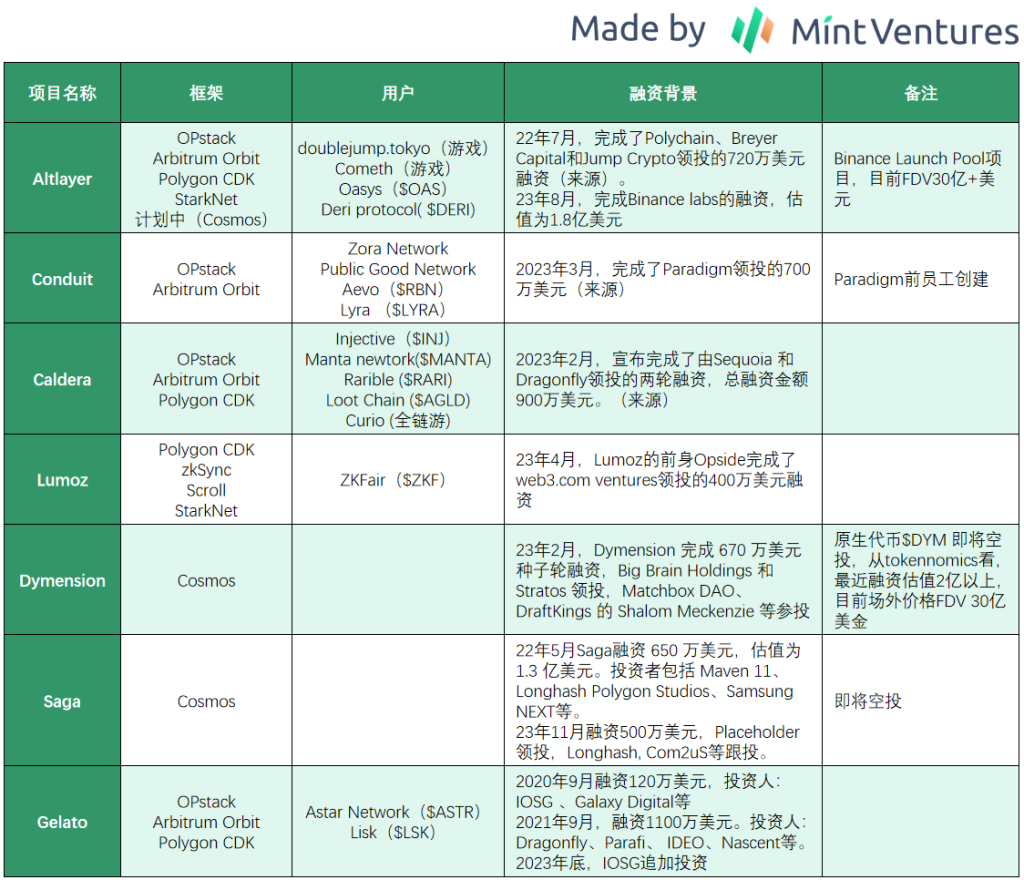

Gelato has had a total of 4 fundraising rounds, including 3 private rounds and 1 public round, as follows:

The seed round took place in September 2020, raising $1.2 million from investors including IOSG, Galaxy Digital, D1 VC, The LAO, Ming Ng, and MetaCartel. The cost of $GEL in this round was $0.019.

In September 2021, Gelato announced a $11 million fundraising round with investors including Dragonfly, Parafi, IDEO, Nascent, and Stani Kulechov (founder of Aave). The cost of $GEL in this round was $0.2971.

The public round also took place in September 2021, raising $5 million. The cost of $GEL in this round was also $0.2971.

In December 2023, Gelato completed an expansion round of financing led by IOSG, but the amount and method of financing were not disclosed.

In addition, at the inception of the project, they received grants from Gnosis and MetaCartel.

Partnerships-wise, Gelato has numerous partners due to its position in the developer services industry and its provision of RaaS services to external parties, as we have already listed in the previous sections.

In addition, Gelato was the winner of BNB Chain's Most Valuable Builders iii in 2021.

3. Business Analysis

3.1 Industry Space and Competitive Landscape

We will mainly analyze the smart contract automation services and RaaS market.

3.1.1 Smart Contract Automation Services

Regarding the market space and competitive landscape of smart contract automation services, we have already provided a comprehensive analysis in a previous article, and our viewpoint has not changed. Here are the core points:

There is a wide range of scenarios in the Web3 world that require the automatic execution of smart contracts, such as regular reinvestment of earnings, regular salary payments, and liquidity rebalancing. For developers, designing and executing a complete set of monitoring, calculation, and execution programs on their own requires a significant amount of manpower and time. Automation service providers can help developers avoid "reinventing the wheel." For service providers like Gelato, the marginal cost of providing services to new users is low, as there is no difference between Uniswap's limit orders and Quickswap's limit orders. Therefore, cooperation between the two parties is more "economical" for both sides, and the business logic is solid.

However, the issue may be that because the services provided by Gelato have a relatively low barrier to entry, developers are willing to pay limited fees. In practice, they may encounter difficulties similar to those faced by web2 automation service provider IFTTT: "They can provide useful products, but there are not many people willing to pay for them."

In the field of smart contract automation, the two main players that are currently widely used are Chainlink and Gelato. Although Andre Cronje's Keeper network ($KP3R) also targeted this market at one point, over time, Keeper network has largely exited this field, and the main use case for the KP3R token has become generating income from the Fixed Forex protocol.

According to disclosures from IOSG, Gelato currently holds an 80% market share in the smart contract automation market, which is quite remarkable in the sub-market where the Web3 infrastructure leader Chainlink is involved. However, unfortunately, a high market share has not brought stable income, and the product is currently in a state of "good reputation but low sales," making commercialization somewhat challenging.

In terms of competition, although Gelato entered this market earlier than Chainlink and currently holds a leading position in the market, in the medium to long term, Chainlink has a stronger brand, more effective developer outreach channels, a more abundant team fund reserve, and can cross-sell with other proprietary services. Therefore, it will not be easy for Gelato to maintain a leading position in competition with Chainlink.

3.1.2 RaaS

RaaS has been a relatively hot sub-track in the infrastructure field since 2023, and it has attracted considerable market attention recently with Altlayer launching on Binance's Launch Pool.

With the rapid development of ETH L2, the scalability issues that ETH once faced seem to have been largely resolved through Rollups. Especially after the upcoming Dencun upgrade, the cost of Rollups will once again be significantly reduced by an order of magnitude, laying a solid foundation for the large-scale commercial promotion of Rollups.

The Ethereum ecosystem currently has the most complete infrastructure in the web3 field (including wallets, browsers, oracles, indexes, etc.), and the user experience within the EVM system is widely accepted among current web3 users. For application developers, becoming an ETH Rollup, allowing them to focus on the application itself rather than dealing with many "miscellaneous matters" related to running a chain, is a good choice.

On one hand, we see teams such as Coinbase, Consensys, Mantle, and Blur, which have achieved very good results in other areas of web3, choosing L2 when building a chain in 2023 (correspondingly, in 2020, Binance and OKX both built L1).

On the other hand, we also see more and more L1 projects deciding to transition to Rollups, including:

Celo, a stablecoin project somewhat similar to Luna, proposed in July 2023 to transition to ETH L2.

Lisk, established in 2016, announced in December 2023 that it will use Gelato's services to transition to ETH L2.

We expect this trend to continue in the future. While developers are building Rollups, there are still a series of issues and trade-offs that developers need to consider, such as how to choose a Rollup that suits their characteristics, how to build and operate a Sequencer, how to solve MEV issues, and how to choose oracle and index solutions. RaaS service providers, as "integrated service providers" directly targeting developers, clearly have relatively stable demand in this context.

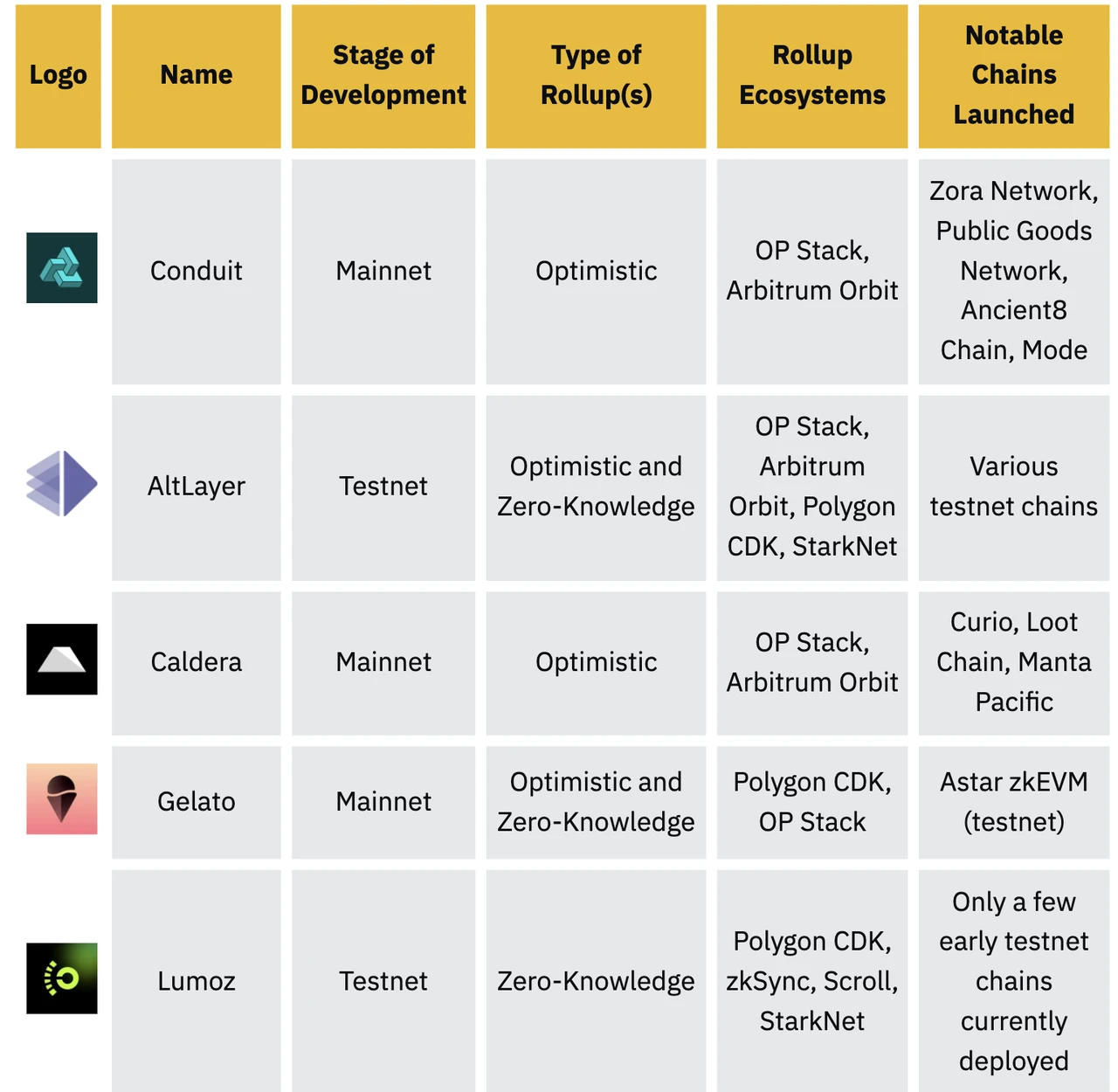

In November 2023, Binance released a research report on the RaaS sub-track, which mainly mentioned Conduit, Altlayer, Caldera, Gelato, and Lumoz as the 5 projects. The other four projects can be said to directly compete with Gelato.

Source: Binance RaaS research

The above protocols can be seen as part of the Ethereum ecosystem. In fact, for developers, their goal is to create an application chain that better meets their needs, and whether this chain is a Rollup or a Cosmos IBC chain is not particularly important to them. Although the infrastructure of the Ethereum system is relatively complete, the Ethereum system is not the only choice.

For these reasons, we consider "one-click chain deployment" service providers in the Cosmos ecosystem to be competitors of Gelato. Competitors of Gelato in the RaaS or AppChain as a service field include:

(In fact, there are also participants in the RaaS field such as Astria, Gateway.fm, Karnot, Snapchain, Vistara, Zeeve, etc., but due to space limitations, we will not provide detailed introductions.)

From the above project information, we can see that although the RaaS track is an emerging track, there are already many players in the field, and top VCs have already participated in RaaS projects, making the competition intense. Since the second half of 2023, more and more protocols have been using RaaS to deploy Rollups. Apart from Altlayer, there are also Cosmos-based projects like Dymension and Saga nearing their launch, indicating a small peak in the entire track.

Looking at the currently operational RaaS Rollups, it seems that RaaS service providers do not charge for providing RaaS services. Several RaaS service providers hope to capture more value from derivative services in the future.

To explore how the RaaS track can generate revenue, let's take Optimism as an example to understand the revenue and cost structure of Rollups:

The gas paid by Rollup users is generally allocated to the following three layers:

Execution layer: This layer directly faces users, collects gas fees paid by users, and pays fees to the DA and settlement layer.

DA layer: The DA layer ensures the data availability of the Rollup, and this is the main destination of user-paid gas and the major cost of L2 projects. Apart from Ethereum, other providers of DA include the recently popular Celestia, Polygon's independent Avail, and Eigenlayer.

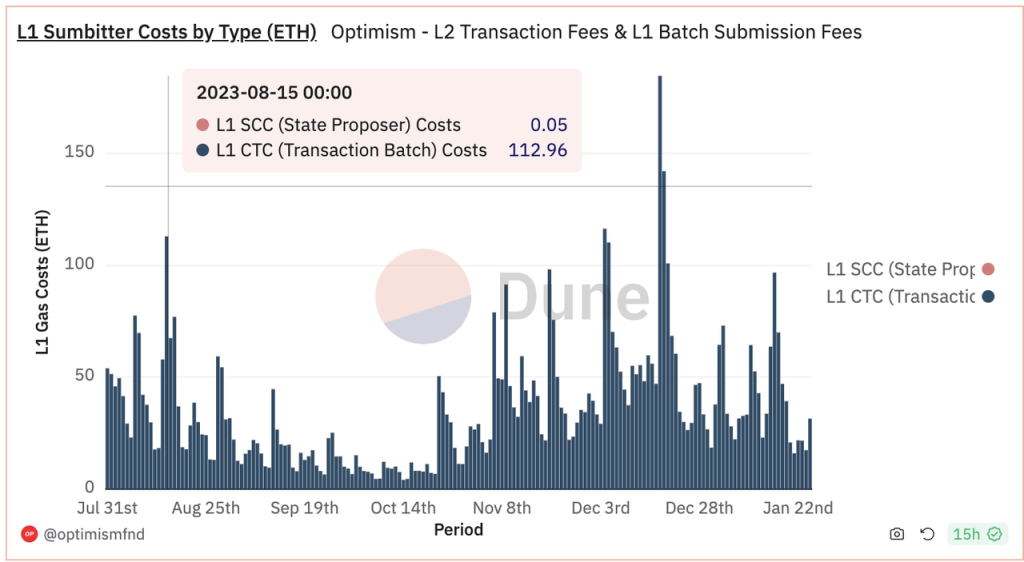

Settlement layer: The issue with the settlement layer is that it captures relatively little fees. Currently, Optimism pays Ethereum only about 0.05 ETH per day for settlement fees (source).

For Optimism and any other Rollup, its revenue = execution layer revenue, expenses = DA expenses + settlement layer expenses, and gross profit = execution layer revenue - DA expenses - settlement layer expenses.

- First, looking at the cost, the settlement layer expenses are very low, with Optimism currently paying Ethereum only about 0.05 ETH per day for settlement fees.

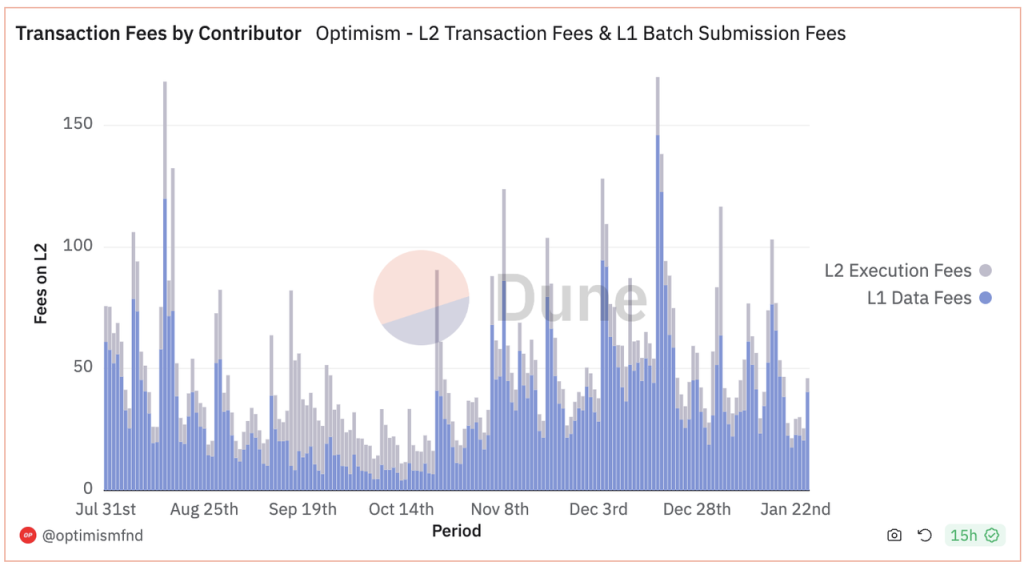

Fees paid by Optimism to the DA layer (dark blue) and settlement layer (barely visible orange) (source)

- Then, in terms of total revenue, due to the high DA costs, Optimism's "gross profit" margin is not very large.

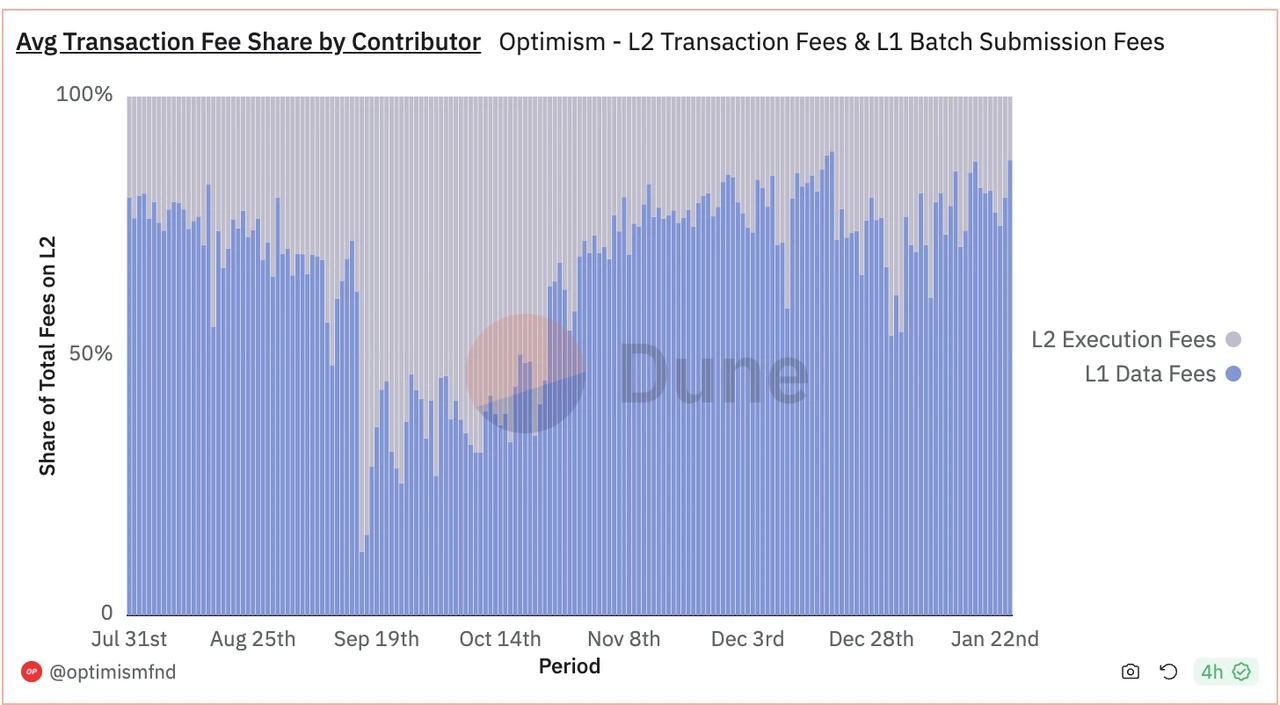

Optimism's execution layer gross profit (gray) and absolute value of DA layer expenses (blue) (source same as above)

Optimism's execution layer gross profit (gray) and DA layer expenses (blue) as a percentage (source same as above)

We can see that in the entire Rollup ecosystem, the DA layer captures the most profit. As RaaS service providers, they need to extract a portion of the "gross profit" from Optimism (= execution layer revenue - DA costs - settlement layer costs) to generate revenue, which is generally quite challenging.

Based on the comprehensive information available, potential ways for RaaS to generate revenue/capture value include:

Generating more revenue through hosting sequencers, MEV, and other services at the execution layer, which is the most reasonable and likely source of revenue.

Generating revenue by becoming the settlement layer for Rollups/Appchains (e.g., Dymension).

Charging fees not through user transactions, but through integrating wallets, browsers, and other infrastructure, or other technical consulting services.

Subscription fees similar to traditional SaaS.

Of course, there is also the recent collaboration between Altlayer and Eigenlayer to achieve Restaked rollup, where $ALT is used more as an economic bandwidth, capturing value for tokens through the combination with Restking. However, this value capture is not directly related to the RaaS services they provide.

Overall, since there are relatively few operational RaaS projects, the ways to generate revenue are not yet set in stone. However, based on the analysis of the revenue and cost structure of Rollups, it appears that generating revenue through RaaS is quite challenging.

In terms of competition, since the users of RaaS service providers are developers/project teams, attracting developers/project teams is the main focus for RaaS service providers. Although different RaaS service providers have different technical characteristics, the services they can provide are largely determined by the underlying framework. Therefore, we believe that the services provided by RaaS service providers generally exhibit significant homogeneity.

Under relatively homogeneous service content, the project's own influence may be a determining factor.

For projects that have not yet launched tokens, the main focus is on lead investors. On one hand, the endorsement of lead investors can significantly reduce the psychological barriers for developers/project teams to use the service and increase the likelihood of their use. On the other hand, lead investors have rich developer/project team resources in the industry, which can naturally bring a customer base to RaaS service providers. We can see that Conduit's users exhibit clear characteristics of the Paradigm system.

For RaaS projects that have already launched tokens, the project's market value is a simple quantifiable indicator of its influence.

For RaaS projects with good influence, the team's own business development (BD) capabilities will be the key factor in determining the ceiling for RaaS projects in the long term.

In a market like RaaS, which seems like a blue ocean but may actually be approaching a red ocean, Gelato does not have an advantage in terms of influence and BD capabilities compared to its competitors. Its advantage lies more in the team's years of focus on developer services, allowing it to provide a more comprehensive suite of development tools.

3.2 Token Model Analysis

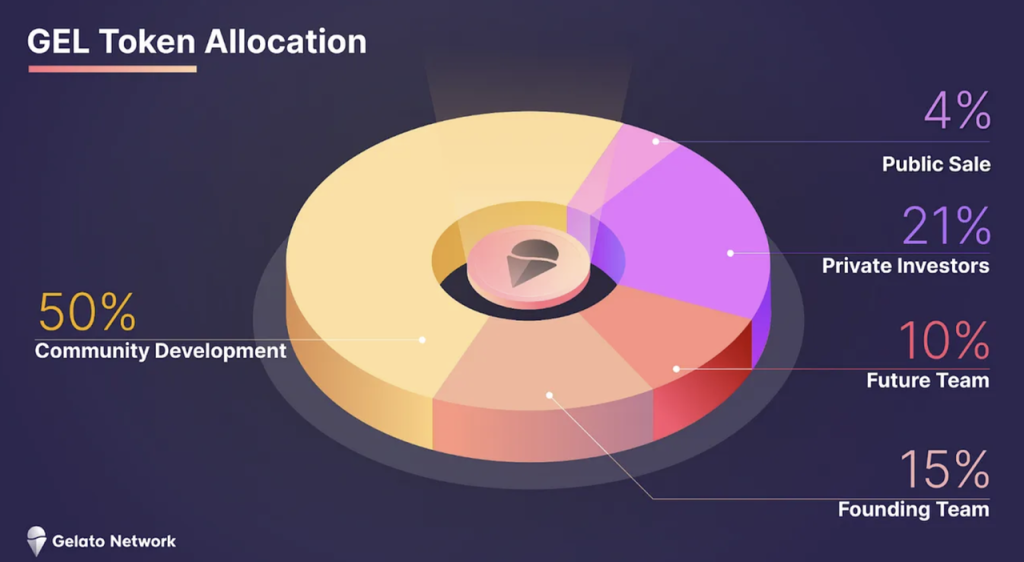

Gelato Network's governance token $GEL has a total supply of 420,690,000, and its distribution is as follows:

- 50% allocated to community development (later, after a governance vote in March last year, 20% was set aside for further financing)

- 4% allocated to the public sale in September 21

- 21% allocated to private investors, with half of the investors' tokens released in September 2022 and the other half in September 2023 (later, after a governance vote, the tokens originally scheduled for release in September 23 were released in February 23).

- 25% allocated to the team, with 15% allocated to the current team and 10% allocated to the future team. Team tokens are locked for 1 year, with 25% released after the lock-up period, and the remaining portion released linearly over three years.

According to the lock-up terms, the portions of tokens for public and private sale investors are already in circulation, 27% of the community tokens are locked, and 15% of the team's tokens are still in a locked state, resulting in an overall circulation ratio of 58%.

Through analysis of on-chain data, it was found that four addresses belonging to private investors, including IOSG and Dragonfly, have not sold their $GEL tokens, collectively holding 12.4% of $GEL.

Currently, the circulating market cap of GEL is $164 million, and the fully diluted market cap is $282 million.

According to official documentation, the use case for $GEL is governance and staking. However, since its launch, Gelato has had few governance matters to address, with only 10 votes on Snapshot. $GEL also does not have a real staking function (except for staking $GEL in 2022 to receive governance tokens from Arrakis).

Overall, the use case for $GEL tokens is relatively limited.

3.3 Risks

Gelato faces the following risks:

- Difficulty in revenue generation: Whether it's smart contract automation or RaaS business, the business model determines that revenue generation is quite challenging.

- Strong competitors: In the field of smart contract automation, Chainlink, and in the RaaS field, Altlayer, Conduit, Caldera, and Dymension, all pose as competitors to Gelato. Compared to these competitors, Gelato's competitive advantage is not strong enough.

4. Valuation Level

Whether it's smart contract automation or RaaS, we currently do not have accurate revenue data for projects in the track, so we cannot accurately perform valuation. Here, we mainly list the circulating market cap and fully diluted market cap of several projects that compete with Gelato for reference.

5. References and Acknowledgments

- https://www.neelsomani.com/blog/rollups-as-a-service-are-going-to-zero.php

- https://twitter.com/_RayXiao/status/1742869034222182890

- https://mirror.xyz/hismrti.eth/I-aOI7SfOItFb51prXpX3hhy-3_9EYu-jaMdIsQExXc

- https://mirror.xyz/hismrti.eth/SOq1l9dU-rWOd_pUoUZZAHIJDf_SuBudRZO8ux-3XNw

- https://www.neelsomani.com/blog/rollups-as-a-service-are-going-to-zero.php

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。