Title: In-depth Exploration of On-chain Derivative DEX Token Economics

Introduction

In our previous article, we discussed the continuous evolution of decentralized derivative exchanges (referred to as derivative DEX) and the evolution and potential development of existing derivative DEX. This article will delve into the current token economics of decentralized derivative exchanges, analyze the different mechanisms adopted by various protocols, and discuss potential future development directions.

Why is Token Economics Important?

Token economics is crucial for the growth and stability of protocols. After experiencing the "DeFi Summer," liquidity mining successfully provided initial funding for protocols in the early stages. However, in the long run, this mechanism is ultimately unsustainable. This mechanism attracted profit-driven capital, leading to a vicious cycle of "mining and dumping," where investors providing funds continuously seek the next protocol offering higher returns, while abandoned protocols suffer damage.

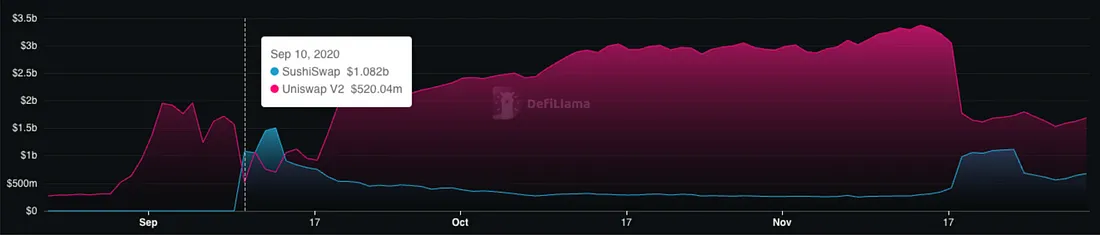

One example is Sushiswap's vampire attack on Uniswap, which initially attracted a large TVL but ultimately proved unsustainable. Meanwhile, protocols such as Aave and Uniswap, with a focus on product priority, successfully attracted and retained users. Sustainable token economics also helped solidify their position as market leaders, which they still maintain to this day.

While product-oriented growth is essential, token economics is also a factor in distinguishing derivative DEX in a competitive market. Tokens represent users' value judgments of the protocol based on their activities, similar to stocks reflecting company performance forecasts. Unlike traditional markets, token prices often precede widespread recognition and growth of crypto projects.

Therefore, having token economics that can accumulate value from protocol growth is crucial. Ensuring a sustainable token economy and providing sufficient incentives for new user participation are also important. Overall, sound token economics is key to achieving long-term growth and retaining protocol value.

Current State of Derivative DEX

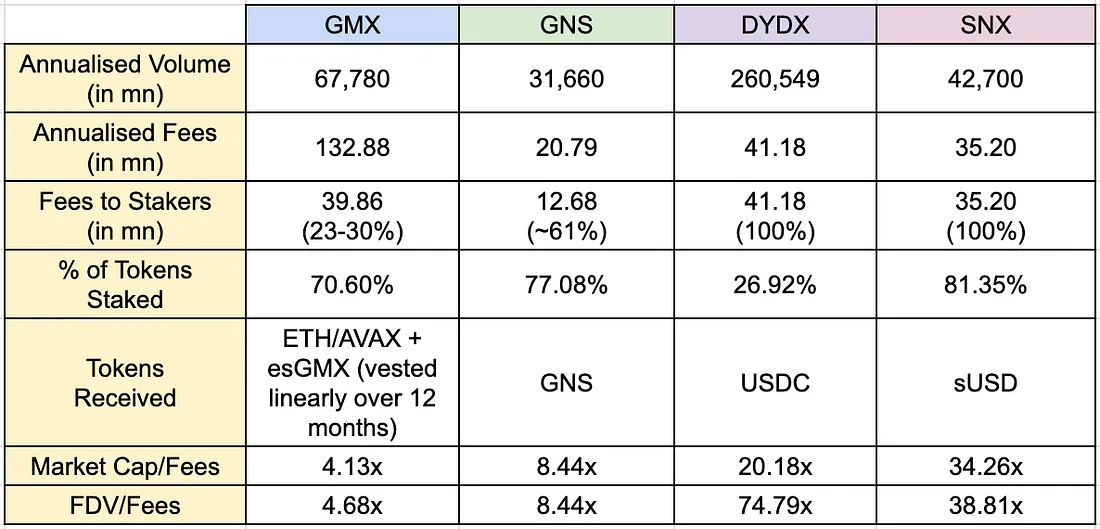

In our previous Hindsight Series articles, we extensively introduced the evolution and mechanisms of derivative DEX. Now, we delve into the token economics of these protocols. dYdX was one of the first projects to launch perpetual contracts on-chain in 2020 and introduced its token in September 2021. Apart from providing a trading fee discount, the token does not offer much utility to its holders and is generally considered highly inflationary due to releases from staking, liquidity providers (LP), and trading rewards.

GMX entered the market in September 2021, aiming to address the unsustainability of emissions. GMX is one of the first companies to introduce the Peer-to-Pool model and user fee-sharing mechanism, which generates revenue from trading fees in the form of major cryptocurrencies and native project tokens. Its success has also led to the creation of more Peer-to-Pool model systems, such as Gains Network. It differs in staking mode and income sharing parameters, posing lower risks to users but also generating lower returns.

Synthetix is another DeFi protocol in this field, supporting multiple front-end perpetual contract exchanges and options exchanges, such as Kwenta, Polynomial, Lyra, and dHEDGE. It adopts a synthetic model where users must stake their SNX tokens as collateral and borrow sUSD for trading, earning sUSD fees from all front-end trades.

Comparison of Derivative DEX Token Economics

The table below shows a comparison of the token economics of different protocols:

Factors to Consider in Well-Designed Token Economics

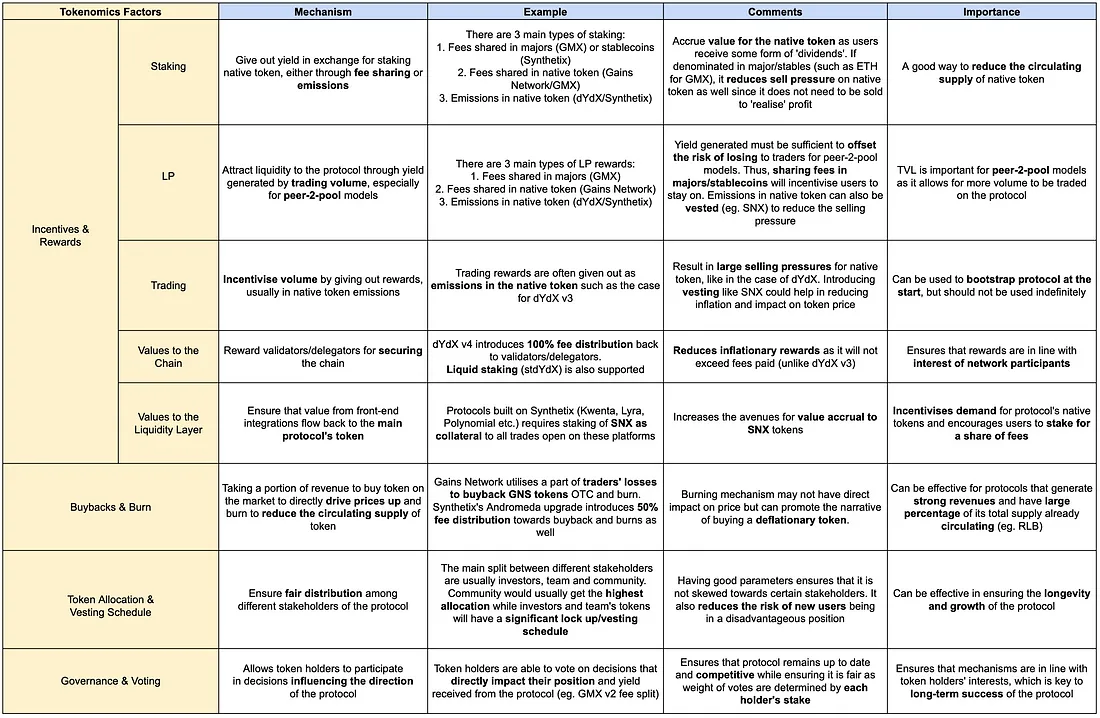

Well-designed token economics requires careful consideration of various factors to create a system that aligns participants' incentives and ensures the long-term sustainability of the token. Based on the current landscape of derivative DEX token economics, we discuss the various factors below.

1. Incentives and Rewards

Incentives and rewards play a crucial role in encouraging user behavior. This includes mechanisms for staking, trading, or other contributions to the protocol.

Staking

Staking is a mechanism where native tokens are deposited into the protocol in exchange for returns. The returns received by users are either obtained through sharing fees (which may be major cryptocurrencies or stablecoins in the market) or through the release of native tokens. Among the protocols analyzed, there are three main types of staking:

- Sharing fees in major cryptocurrencies or stablecoins

- Sharing fees in native tokens

- Receiving inflationary releases of native tokens

As shown in the table, fee sharing has proven to be effective in incentivizing users to stake their tokens. The table reflects recent changes in token economics for dYdX and Synthetix, including the introduction of 100% fee sharing for dYdX v4 and the elimination of inflationary releases for SNX.

Previously, dYdX v3 had a security and liquidity staking pool that released inflationary DYDX rewards, as these pools did not directly benefit from platform trading volume. Following community votes in September/November 2022, these two pools were abandoned as they did not truly serve their purpose and were not efficient for the DYDX token. With v4, trading fee generated returns are returned to stakers, incentivizing users to stake for returns.

GMX utilizes two types of staking to allocate its rewards, distributing fees in major tokens (ETH/AVAX) and its native token. The staking rates for GMX, Gains Network, and Synthetix are very high, indicating that the rewards are sufficient to incentivize users to provide initial capital and maintain their stakes within the protocol. It is challenging to determine the ideal incentive mechanism, but so far, the partial payment of fees in major tokens/stablecoins and the introduction of inflationary release rewards for native tokens have proven effective.

In summary, staking has the following benefits:

(1) Reducing the circulating supply of tokens (and selling pressure)

This method is effective only when the generated returns are not purely distributed to ensure sustainability

If the returns are in major tokens or stablecoins, it reduces selling pressure as users do not need to sell tokens to realize their returns

(2) Increasing the value of staked tokens

As the protocol develops and the fees generated per token increase, the value of the tokens can indirectly grow

Providing stable returns for tokens can attract non-traders to participate solely for earning returns

However, several factors need to be considered when implementing staking based on the protocol's objectives:

(1) Persistence and type of rewards

Having stable returns is crucial, considering that risk-averse users do not need to sell tokens to "realize" returns

The release rate is also important to ensure that the returns received by users are not too unstable and can be sustained over time

(2) Targeting the right users for rewards

- Lower entry barriers and ease of obtaining rewards (no upfront capital, no need for cashing out, etc.) are likely to attract mercenary-like users, diluting rewards for active users (traders, long-term holders, etc.)

Our Thoughts: In most protocols, staking is a common way to reduce token circulating supply. This is a good way to align with user interests, especially if the native token is required as collateral (e.g., SNX), which reduces the volatility of user positions through returns. If rewards are distributed based on partial fees and major tokens/stablecoins, the effect of staking will be more positive and long-term, which may be more suitable for most derivative DEX with decent trading volume.

Liquidity Providers (LP)

Liquidity providers (LP) are particularly important for derivative DEX, especially for the Peer-to-Pool model, as it allows them to support more platform trading volume. In the Peer-to-Pool model, LP becomes the counterparty to traders on the platform. Therefore, the fee-sharing revenue must be sufficient to offset the risk given to traders.

For order book models like dYdX, LP is a way for users to earn rewards. However, most TVL still comes from market makers, and the rewards issued by DYDX are purely inflationary. Therefore, the LP module was abandoned in October 2022. Synthetix is an exception, as stakers on platforms integrated with it (such as Kwenta, Polynomial, dHEDGE, etc.) are actually LP and earn fees from trading volume.

Both GMX and Gains Network adopt the Peer-2-Pool model, which requires LP to act as the counterparty for trades executed on the platform. Comparing these two protocols:

GLP's TVL is significantly higher than gDAI, possibly due to higher returns.

gDAI users face lower risk as traders' profits are supported by GNS minting, while GMX pays funds to users from GLP.

More risk-averse users may be attracted by the higher returns of GLP, while less risk-averse users can deposit gDAI, despite lower returns.

Gains Network's mechanism is similar to Gambit Financial, the predecessor of GMX on BNB. Gambit generated significant trading volume and TVL after its launch. Although Gambit and GMX share similar features in the Peer-to-Pool model and revenue-sharing mechanism, their parameters differ.

While Gambit gained traction, GMX saw a surge in trading volume and user numbers on Arbitrum after modifying its token economics and structure. Key changes observed include:

Allocating the majority of returns to stakers/LP.

Gambit only allocated 40% of the revenue share (20% to USDG + 20% to Gambit stakers) to holders/stakers, while GMX v1 allocated 100% of the revenue share (70% to GLP + 30% to GMX stakers).

Increasing the amount of returns allocated to stakers/LP, creating a compelling narrative to attract a broader audience, not just pure traders.

Transferring risk to LP, who bear the brunt of traders' profits or losses.

From the case studies of Gains Network, Gambit, and GMX, it is evident that increasing LP returns can incentivize more liquidity, especially for the Peer-to-Pool model. In GMX v2, there were subtle changes in token economics, reducing the fee share for stakers and GLP holders by 10%. Details of this adjustment:

GMX V1: 30% allocated to GMX stakers, 70% to GLP providers.

GMX V2: 27% allocated to GMX stakers, 63% to GLP providers, 8.2% to the protocol treasury, 1.2% to Chainlink, approved by community vote.

Community members largely supported the vote and the continued growth of GMX v2's TVL, indicating positive changes for the protocol.

Rewarding LP has many benefits, especially for the Peer-to-Pool model, as it enhances loyalty to the protocol through stable returns:

Reducing the risk of LP losing initial capital.

Combining stable returns reduces the inertia to adjust positions, as they do not need to sell tokens to realize returns.

For dYdX v3, this mechanism is not applicable as the volatility of its native token would generate at issuance.

Accumulating value for the native token.

Factors to consider:

Adjusting LP risk for the protocol.

Recently, SNX stakers lost $2 million due to a market manipulation event on TRB, as the OI cap was set in TRB token quantity rather than USD amount.

In the past, most GLP holders benefited from traders' losses, but questions have been raised about the sustainability of this mechanism. With changes in token economics, any significant trader wins could receive support from the protocol treasury.

Our Thoughts: This mechanism is crucial for the Peer-to-Pool model, as growth requires incentivizing user liquidity. Over time, GMX effectively achieved this through high revenue sharing and increased trader losses. While trader wins pose risks for LP, we believe that the returns for mid-sized protocols can significantly offset this risk. Therefore, we consider adequately incentivizing LP crucial for building a strong user base.

Trading

Trading rewards are primarily used to incentivize trading volume and are usually distributed in the protocol's native token. Rewards are typically calculated as a percentage of the total reward for a specific period's trading volume/fees.

For dYdX v3, the total supply allocated for trading rewards is 25%, which was the primary issuance source in the first two years. Therefore, the amount of trading rewards often exceeds the amount of fees paid by traders, indicating highly inflationary token issuance. As there is almost no holding incentive (mainly for trading fee discounts), over time, this has led to significant selling pressure on DYDX. This situation changed for dYdX v4, which will be discussed below.

Kwenta also provides trading rewards for platform traders, limited to 5% of the total supply. It requires users to stake KWENTA and conduct trades on the platform to be eligible. The reward is determined by multiplying the percentage of staked KWENTA and paid trading fees, meaning the reward will not exceed the user's upfront costs (staking capital + trading fees). The reward requires a 12-month lock-up period, and if users want to cash out the reward early, it can be reduced by up to 90%.

Overall, the clear benefits of introducing trading rewards include:

- Incentivizing trading volume in the short term: Through rewards in dYdX v3, traders essentially receive compensation during trades, which helps drive the growth of trading volume.

Factors to consider:

Types of users the protocol wants to attract

For dYdX, eligibility for rewards is easy and without locking conditions, which may attract many short-term users, diluting the rewards for genuine users.

For Kwenta, requiring upfront capital and a lock-up period may not be attractive to short-term users, potentially reducing dilution of rewards for long-term users.

Our Thoughts: Trading rewards may be an effective way to initially guide the protocol, but should not be used indefinitely, as continuous token issuance will devalue the token. It should also not occupy a large proportion of monthly supply and inflation for the protocol, and locking is important for mitigating selling pressure.

Value Accrual to the Chain

Case Study: dYdX

The launch of the dYdX chain marks a new milestone for the protocol. On January 18, the dYdX chain even briefly surpassed Uniswap, becoming the largest DEX by trading volume.

In the future, we may see more derivative DEX following this path. The major changes in token economics for the dYdX chain update include:

Staking for supporting chain security, not just for generating returns

In v3: Rewards in the safety pool were issued in DYDX tokens, but were eventually disabled after DIP 17 was approved by community vote.

In v4, the dYdX chain requires validators to stake DYDX tokens to operate and protect the chain. Delegation (staking) is a crucial process, where stakers delegate validators to perform network validation and block creation tasks.

100% of all trading fees will be distributed to delegators and validators.

In v3, all generated fees were collected by the dYdX team, which was a concern for some in the community.

In v4, all fees, including trading fees and gas fees, will be distributed to delegators (stakers) and validators. This new mechanism is more decentralized and aligns with the interests of network participants.

PoS delegators can choose validators to stake their DYDX tokens and receive a share of income from their validators. Delegator commissions range from a minimum of 5% to a maximum of 100%. Currently, according to Mintscan data, the average validator commission rate on the dYdX chain is 6.82%.

In addition to these changes, the new trading incentive measures also ensure that rewards do not exceed the net trading fees paid. This is an important factor, as many concerns about v3 were focused on inflation and unsustainable token economics, although updates later had minimal impact on token performance. Xenophon Labs and other community members raised questions about whether rewards could be "gamed," a topic that has been discussed multiple times in the past.

In v4, users can only receive trading rewards equivalent to 90% of the net trading fees paid to the network. This will improve the balance between demand (fees) and supply (rewards) and control token inflation. The reward cap is 50,000 DYDX per day for 6 months, ensuring significant inflation will not occur.

Our Thoughts: The dYdX chain is at the forefront of the industry's move towards greater decentralization. The validation process plays a crucial role on the new chain: protecting the network, voting on proposals on the chain, and distributing staking rewards to stakers. Coupled with 100% fee distribution to delegators and validators, it ensures that rewards align with the interests of network participants.

Value Accrual in Liquidity Centers

Case Study: Synthetix

Synthetix, as a liquidity center for multiple perpetual and options trading frontends such as Kwenta, Polynomial, Lyra, dHEDGE, has created its own custom features, built its own community, and provided trading frontends for users.

Among all integrators, Kwenta is the primary derivatives exchange driving most of the trading volume and fees to the entire Synthetix platform. Synthetix is able to capture the value brought by Kwenta and other exchanges, attributed to Synthetix's token economics. The main reasons include:

Staking SNX is the first step for trading on integrators

Even with their own governance token, Kwenta only quotes asset prices in sUSD, which can only be minted by staking SNX tokens.

In addition to Kwenta, other integrators like Lyra, 1inch, and Curve (Atomic Swaps) also utilize sUSD, hence requiring SNX tokens. Therefore, Synthetix's frontend integrators allow value accrual to SNX tokens.

Reward distribution to integrators

In April 2023, Synthetix announced the large-scale distribution of its Optimism tokens to traders. Over 20 weeks, Synthetix distributed 300,000 OP tokens per week, while Kwenta distributed 30,000 OP tokens per week.

From the second quarter to the third quarter of 2023, Synthetix was able to attract higher trading volume and fees. This played a crucial role in the growth of Synthetix's price.

It can also be seen from the chart that the total value of staked SNX is highly correlated with the price of SNX. As of January 22, 2022, Synthetix's staked TVL is approximately $832 million. Their staked token ratio is the highest (81.35%), compared to dYdX, GMX, and Gains Network.

Our Thoughts: For a liquidity center, the relationship should be mutually beneficial. While Synthetix provides liquidity to these integrators, it also receives fees from them, indirectly driving trading volume for Synthetix's TVL. As demand for their integrators' trades increases, this will lead to increased demand for SNX, reducing selling pressure and indirectly boosting the token's value. Therefore, collaborating with more frontend integrators is beneficial for Synthetix and its token holders.

2. Buyback and Burn

Buyback can be done by using a portion of income to buy tokens on the market, directly boosting the price, or burning to reduce the token's circulating supply. This will reduce the token's circulating supply, and with reduced supply, future prices are expected to rise.

Gains Network has a buyback and burn program, where a portion of traders' losses can be used to buy back and burn GNS based on the gDAI collateralization ratio. This mechanism has led to the burning of over 606,000 GNS tokens, equivalent to approximately 1.78% of the current supply. Due to the dynamic nature of GNS supply through its minting and burning mechanism, it's difficult to determine if the buyback and burn has a significant impact on the token price. Nevertheless, this is a way to counter GNS inflation, which has kept the supply fluctuating between 30-33 million over the past year.

Synthetix recently voted to introduce a buyback and burn mechanism in its Andromeda upgrade. This proposal may reignite interest in SNX, as holders are impacted in both staking fees and holding deflationary tokens. This reduces the risk of pure staking, as the buyback and burn allocation can serve as a backstop for any events (such as the TRB event).

The main advantages of this mechanism are:

Ability to control/reduce supply: This ensures that token holders do not gradually dilute their holdings with rewards or issuance to other holders.

Encourages token holding: Token holders/stakers receive additional utility by holding a "deflationary" asset.

However, the effectiveness of buyback also depends largely on:

- Protocol's income to maintain the significance of burning: Without a stable income stream, the mechanism will not be sustainable, and its reduced impact may lead to a loss of incentive for users to hold the token.

Our Thoughts: The burning mechanism may not directly impact the price, but it can promote the idea of purchasing deflationary tokens. It is effective for protocols that generate strong income and have most of their total supply already in circulation (e.g., RLB). Therefore, it is suitable for protocols like Synthetix that are already established and have low supply inflation.

3. Token Distribution and Unlocking Schedule

Recording the token distribution and vesting schedules for different stakeholders is crucial to ensure that parameters do not favor certain stakeholders. For most protocols, major holder allocations include investors, teams, and the community. For community tokens, this includes airdrops, public sales, rewards, and DAO tokens, among others.

The distribution of SNX is calculated based on the increase in token supply from the reward issuance in the February 2019 monetary policy change.

When examining the distribution and unlocking schedules of these protocols, we have drawn some conclusions:

GMX and Gains Network are exceptions here in raising funds solely through public token sales. "Community-owned" protocols can reduce user concerns about investors, incentivizing them to hold the token and participate in the protocol.

dYdX and Synthetix have reserved a significant supply for investors, at 27.7% and 50% respectively (before supply changes). However, dYdX has a long lock-up period of about 2 years, while Synthetix has a 3-month lock-up period after TGE, followed by quarterly unlocks.

GMX and Gains Network both transitioned from another token to the current token, meaning that most of the supply was unlocked at launch. This implies that the further release of future rewards will make up a small proportion of the circulating supply.

dYdX and Synthetix have both reserved a significant supply for rewards (>=50%). However, dYdX rewards are pure issuance, while Synthetix distributes a portion of fees + rewards, which unlock over 12 months. This reduces SNX inflation compared to DYDX.

Due to the significant differences in the holders and mechanisms adopted by different protocols, there is no clear formula for token distribution or unlocking. Nevertheless, we believe the following factors generally benefit the token economy for all stakeholders:

The community should receive the majority of tokens.

Team token allocations should not be excessive, and the unlocking schedule should be longer than most holders, as this may indicate their belief in the project.

Investor token allocations should be minimal, with a long unlocking period.

Token releases should be spread out over a period of time and include some form of locking to prevent significant inflation at any point in time.

4. Governance and Voting

Governance is crucial for derivative DEXs, as it empowers token holders to participate in the decision-making process and influence the direction of the protocol's development. Some decisions that governance can make include:

Protocol upgrades and maintenance

Derivative DEXs often require upgrades and improvements to enhance functionality, scalability, and growth. This ensures that the protocol remains up-to-date and competitive.

For example, in a recent snapshot for GMX, governance passed a proposal to create a BNB market on GMX V2 (Arbitrum) and GMX v2 fee distribution.

Risk management and security

Token holders can collectively decide on collateral requirements, liquidation mechanisms, bug bounties, or emergency measures to be taken in the event of violations or exploits. This helps protect user funds and build trust in the protocol.

Recently, Synthetix suffered a $2 million loss due to TRB price fluctuations. This highlights the importance of ongoing review of parameters—adding volatility circuit breakers and increasing sensitivity to skew parameters for pricing volatility peaks.

Liquidity and user incentives

Token holders can propose and vote to support liquidity provider incentive strategies, adjust fee structures, or introduce mechanisms to enhance liquidity provision.

For example, governance in dYdX has passed the v4 launch incentive proposal.

Transparent decentralized community

Governance should establish a decentralized community with transparency and accountability. Publicly accessible governance processes and on-chain voting mechanisms provide transparency in the decision-making process.

For example, DEXs like dYdX, Synthetix, and GMX have adopted on-chain voting mechanisms to promote decentralization.

Our Thoughts: Through governance, a strong and inclusive community can be created for stakeholders involved in derivative DEXs. Having on-chain voting mechanisms and decision transparency can build trust between stakeholders and the protocol, as the process is fair and accountable to the public. Therefore, governance is a key feature of most crypto protocols.

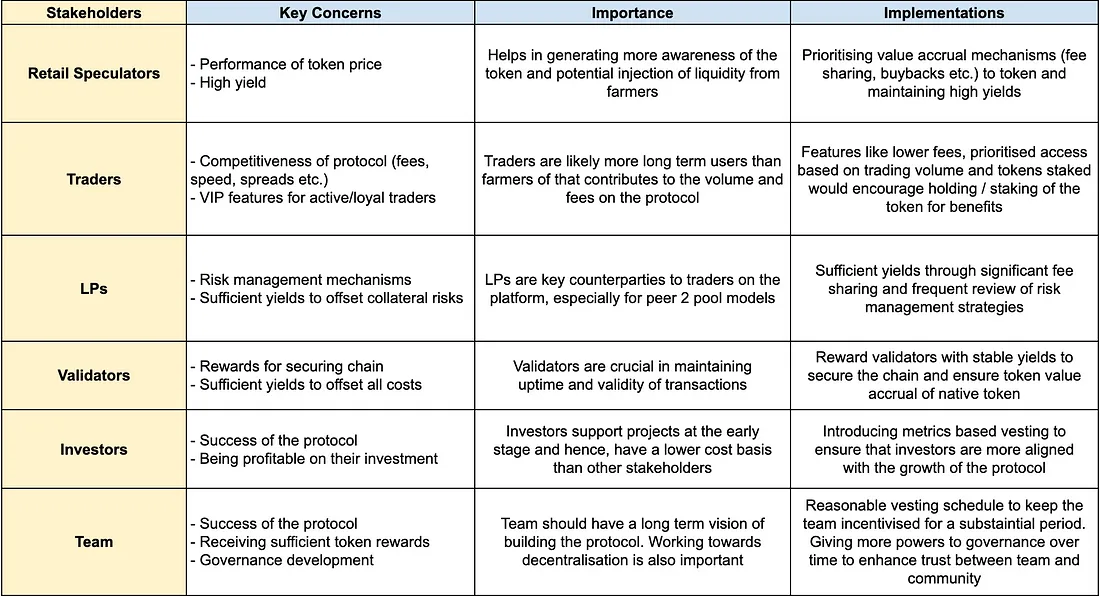

Exploring New Mechanisms

In addition to the above factors, we believe there are many innovative ways to introduce additional utility and incentivize demand for tokens. Protocols need to prioritize introducing new mechanisms based on their targeted stakeholders and the factors most important to them. The table below shows key stakeholders and their primary concerns:

Given the diverse concerns, it's impossible to cater to all stakeholders. Therefore, for a protocol, it's crucial to reward the right user groups to ensure sustained growth. We believe there is room for introducing new mechanisms to better balance the interests of different stakeholders.

Conclusion

In conclusion, token economics is a core part of crypto protocols. Determining successful token economics does not have a clear formula, as there are many factors that can impact performance, including factors that the project cannot control. Nevertheless, the crypto market changes rapidly and continuously, highlighting the importance of flexibility and adjusting based on market conditions. From the examples above, it can be seen that trying new mechanisms can be highly effective in achieving exponential growth.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。