Inscriptions of Summer

Previously, everyone was speculating on which track the bull market would start from, social, gaming, or ZK? Now there should be no suspense, without a doubt, it is "inscriptions".

However, how to view "inscriptions" seems to be a confusing matter. Builders, investors, old OGs, newbies, different people have different opinions. For a long time, I was indoctrinated with a wrong view that "inscriptions are a new way of issuing assets, similar to the frenzy of MEME coins", which led to a wrong understanding, until I saw the articles by Mr. Wang Feng (@wangfeng_0128) and Joslter (@jolestar), and then realized the true meaning of inscriptions.

In this article, I will explain why "the essence of inscriptions is actually a third type of token, SFT, distinct from NFT and FT" and the $ORDI valuation model brought about by this understanding, and finally comment on several common cognitive errors.

What is SFT

For a long time, we have formed several fixed understandings of tokens. Tokens are generally divided into two types: FT and NFT.

The English term for fungible tokens is "fungible token", abbreviated as FT. The word "fungible" means "interchangeable". As the name suggests, the characteristic of FT is that any two units of tokens are exactly the same and can be exchanged with each other, so they are "homogeneous" as a whole. Because FT directly corresponds to value units in the real world, such as currency, common stocks, and points, and can be added or subtracted, it is easy to understand and therefore appeared earliest. As early as when Ethereum had just launched in 2015, Vitalik Buterin proposed the idea of implementing FT through smart contracts, and Fabian Vogelsteller proposed the ERC-20 standard in November 2015. After 2016, ERC-20 became the most widely used and well-known token standard, opening up a huge industry worth billions of dollars.

The English term for non-fungible tokens is "non-fungible token", abbreviated as NFT, which is the opposite of FT in all aspects. In FT, any two units of tokens are exactly the same and interchangeable, while each NFT is unique, one-of-a-kind, and cannot be replaced, and cannot participate in calculations. FT represents abstract quantity units, while NFT represents specific digital items, such as virtual artworks, domain names, music, game equipment, and so on. In order to show their uniqueness, each NFT has its own unique ID (determined by the creating contract address and serial number) and metadata. The main standard for NFT is ERC-721, proposed by William Entriken and three others in January 2018. In the first three years of NFT's birth, it can be said to have been a silent supporting role. It wasn't until 2021, with the popularity of encrypted artworks, that the NFT industry suddenly exploded. In the first five months of 2022, the new asset scale of NFT reached 36 billion US dollars. Today, NFT is considered one of the most important infrastructures for Web3 and the metaverse.

SFT is a semi-fungible token, which is a new type of token that is parallel to FT and NFT. Since it is called "semi" fungible token, as the name suggests, it is between FT and NFT, and can be split for calculation, while also having uniqueness.

It is important to note that because BTC lacks smart contract functionality, the previous issuance of tokens was "defined" from the perspective of the ETH technology stack, such as the token standard for FT being ERC20, and for NFT being ERC721, what about SFT? In September 2022, the team Solv Finance, where Mr. Meng Yan (@myanTokenGeek) is located, proposed ERC3525, which first defined the SFT token standard for the ETH ecosystem.

Although the ERC3525 proposed by the Ethereum ecosystem has been around for nearly a year, it has not caused much of a stir in the market. One reason, of course, is the bear market, but another reason is that the SFT tokens issued in cooperation with Solv are all financial assets of institutions, or belong to the bond market, targeting institutional traders, and have nothing to do with ordinary retail investors.

How to Issue FT on the BTC Chain?

Before various smart contract platforms appeared, many people had already experimented with issuing FT and NFT on the BTC chain. The most famous of these is the Colored Coins scheme.

Colored coins refer to a set of technologies that use the Bitcoin system to record the creation, ownership, and transfer of assets other than Bitcoin, and can be used to track digital assets and tangible assets held by third parties, and to trade ownership through colored coins. The so-called "coloring" refers to adding specific information to Bitcoin UTXO to distinguish it from other Bitcoin UTXO, thus bringing heterogeneity to homogeneous bitcoins. Through the colored coin technology, the issued assets have many of the same characteristics as Bitcoin, including preventing double spending, privacy, security, transparency, and resistance to censorship, ensuring the reliability of transactions.

It is worth noting that the protocol defined by colored coins will not be implemented by general Bitcoin software, so specific software is needed to identify transactions related to colored coins. Obviously, colored coins only have value within a community that recognizes the colored coin protocol; otherwise, heterogeneous colored coins will lose their coloring properties and revert to pure satoshis. On the one hand, colored coins recognized by small communities can issue and circulate assets using the many advantages of Bitcoin; on the other hand, it is almost impossible for the colored coin protocol to be merged into the largest consensus Bitcoin-Core software through a soft fork.

The Mastercoin project conducted an initial token sale in 2013 (today we call it an ICO or initial token sale), and successfully raised millions of dollars, which is considered the first ICO in history. The most famous application of Mastercoin is Tether (USDT), the most well-known fiat stablecoin, which was initially issued on the Omni Layer.

The biggest difference from Colored Coins is that on the chain, Mastercoin only publishes various types of transaction behaviors, and does not record related asset information. In Mastercoin nodes, a state model database is maintained by scanning Bitcoin blocks in off-chain nodes. Compared to Colored Coins, the logic it can accomplish is more complex. And because it does not record and verify states on the chain, transactions between them do not require continuity (continuous coloring). However, to implement the complex logic of Mastercoin, users need to trust the off-chain database in the nodes, or allow Omni Layer nodes to verify.

How to Issue NFT on the BTC Chain?

The above two protocols mainly involve issuing FT assets on the BTC chain. As for NFT assets, it is necessary to mention Counterparty.

Counterparty was launched in January 2014, initially as a platform for FT financial asset tokens, but quickly became the birthplace of some of the earliest NFTs, such as Spells of Genesis, Rare Pepes, and Sarutobi Island. In Counterparty, you must give up a special Counterparty transaction to transfer ownership of the token. Counterparty nodes will parse the data of this transaction off-chain, and then update a ledger/database stored in Counterparty nodes. This is done using OP_RETURN, a method for storing arbitrary data in Bitcoin transactions (thus allowing data to be stored in the Bitcoin blockchain).

The real explosion of Counterparty came after the launch of 1774 NFTs in the Frog Pepé series. Collectors used the Counterparty wallet to store these NFTs, and Counterparty used OPRETURN outputs to anchor the indexes of these NFTs to the Bitcoin blockchain. The OPRETURN output can carry data up to 80 bytes, enough for Counterparty to include the description, name, and quantity of the NFTs (but for ordinal NFTs, the only limitation on data volume is the size limit of the Bitcoin block, which we will discuss later).

In addition to using OP_RETURN, BTC itself has been evolving, and the technological changes brought about by SegWit (2017) and Taproot (2021) updates have paved the way for the launch of Ordinals.

The Ordinals protocol is essentially created for NFTs existing in the Bitcoin ecosystem. In January 2023, Casey Rodarmor introduced Ordinals, describing it as electronic art. Its principle is simple. Satoshi (sat) is the smallest unit of Bitcoin, named after its creator, Satoshi Nakamoto. Since there are 100 million sats in one Bitcoin, each sat is equal to 0.00000001 BTC. When all 21 million Bitcoins have been mined, there will be 21 trillion sats. Normally, each sat is indistinguishable from the others. Because each sat is equivalent to another sat and can be exchanged equally, they are considered fungible.

The Ordinals protocol is a system that can distinguish and track individual sats. When a new Bitcoin block is mined and new Bitcoins are created as mining rewards, the protocol assigns a unique number to each Bitcoin based on its mining time, with smaller numbers corresponding to earlier sats.

When a transaction occurs, the Ordinals protocol tracks each transaction in subsequent transactions in a "first in, first out" manner. The numbered sats are called Ordinals, as the identification and tracking mechanism of the numbers depend on the chronological order of creation and transaction. After a sat is identified by the Ordinals protocol, users can engrave arbitrary data on the sat to give it unique characteristics, defined as encrypted art. This functionality was only made possible after the SegWit (2017) and Taproot (2021) upgrades to Bitcoin Core.

When an Ordinal is engraved, Inscriptions are bound to a special type of taproot code. Although this method imposes more restrictions on storing arbitrary data on Bitcoin, it allows Inscriptions to contain more and larger data. Creating and interacting with Inscriptions requires running a full Bitcoin node and a special wallet that supports Ordinals. In the end, we have:

Ordinals + Inscriptions = NFTs

The Ordinals theory can be imagined as a way of observing the Bitcoin blockchain with special goggles, allowing users to create, view, and track additional information related to each sat.

So the ultimate question is, how do we issue SFT assets based on the BTC chain?

The Essence of Inscriptions Tokens is SFT

The BTC chain lacks smart contract functionality, so the issuance of any asset requires the use of scripts such as OP_RETURN or TAPROOT. Therefore, there are theoretically two ways to issue SFT:

- "Adding" a certain "uniqueness" to the basis of FT tokens,

- "Adding" a certain "homogeneity" to the basis of NFT tokens.

This is where the BRC-20 token comes in, using the second method. As mentioned in the previous section, "users can engrave arbitrary data on the sat to give it unique characteristics." So, engraving a piece of text makes it a textual NFT (corresponding to Loot on Ethereum), engraving an image makes it an image NFT (corresponding to PFP on Ethereum), and engraving a piece of music makes it an audio NFT. So, if we engrave a piece of code, and this code is a code for "issuing FT fungible tokens," what would that be?

BRC-20 achieves this by using the Ordinals protocol to set inscriptions as JSON data format to deploy token contracts, mint and transfer tokens. The JSON contains executable code snippets that describe various properties of the token, such as its supply, maximum minting capacity, and unique code, which can be implemented on the Bitcoin network.

So we see something that seems strange: when engraving inscriptions, we are engraving "one piece," which is 100% an NFT, and "one piece" can be split, with the homogeneous tokens inside being split out one by one. This is somewhat similar to the concept of "wholesale and retail" in the real world, which is why some people might think "inscriptions are NFTs that can be split," but this property, which has both NFT and FT attributes, is exactly what we mentioned earlier as SFT!

Domo (@domodata) inadvertently, through this seemingly atavistic technical method, has achieved the issuance of SFT assets without using smart contracts, which is truly a great achievement!

How to Issue SFT on the ETH Chain?

In the previous section, we briefly discussed how non-smart contract public chains (such as the BTC chain) issue FT and NFT, and for smart contract platforms like Ethereum, how they issue FT and NFT is well known to everyone, using the common ERC20 and ERC721 token standards. So the question is, how do we issue SFT on the ETH chain? There are two token standards to choose from: ERC-1155 and ERC-2535.

ERC-1155 is a multi-token standard. In essence, we prefer to call it a multi-instance NFT standard. It is suitable for a relatively narrow application scenario, where the same NFT has multiple identical instances. Note that they must be completely identical, with no differences between instances.

ERC-3525 is a semi-fungible token standard, a universal standard with a very broad applicability. It can identify multiple similar but not identical tokens as "of the same kind," and then allows special operations such as mutual transfer between tokens of the same kind. In effect, it allows mathematical operations such as merging, splitting, and fragmentation between tokens of the same kind.

The main difference between the two lies in the definition of "of the same kind."

- ERC-1155 considers that objects of the same kind must be completely identical, with no differences.

- ERC-3525 considers that objects of the same kind can be similar but not identical, with key properties being the same, but non-key properties allowed to differ.

For SFT tokens that only issue MEME attributes, ERC-1155 is sufficient, while for assets with more financial properties, ERC-3525 is more suitable. Unfortunately, whether 1155 or 3525, there has been no widespread use in the Ethereum ecosystem, with only a few institutional users issuing a small number of debt-based SFTs.

Why Did Inscriptions Succeed?

Inscriptions is a very broad and generalized term, originally defined as "engraving content on the chain." Looking back at history, we can clearly see that the NFTs in the form of inscriptions were not successful and did not cause much of a stir. At that time, the focus of the discussion was whether it was worth issuing NFTs based on the BTC chain after the existence of smart contract versions of NFTs (ERC-721).

Based on the concept of fully on-chain games, we can introduce the concept of fully on-chain NFTs here. As we all know, NFTs based on Ethereum's ERC-721 store only the address of the content in the metadata. If the content is stored on a traditional cloud server, the address is a web link. If the content is stored in a distributed storage, the address is a hash value. No wonder Musk has been mocking NFTs, saying "at least encode the small picture onto the blockchain." Therefore, we can say that NFTs on Ethereum are "off-chain storage of content, on-chain storage of addresses." If centralized or distributed storage servers disappear, the NFTs also disappear.

In contrast, the inscriptions version of NFTs is truly fully on-chain NFTs, with the content directly stored in the on-chain space of BTC, using sequenced sats to point to the content. This is indeed an advantage, but this advantage is not enough to convince everyone. So, before March, Ordinals NFTs were lukewarm, just a small market for small images, until the emergence of BRC-20.

I believe the success of BRC-20 is due to the following reasons:

- BRC-20 implemented the issuance of SFT assets on a non-smart contract public chain in a simple way, which is the most essential reason for its success (Ordinals NFTs were not successful in the early stages).

- BRC-20 adopts a fair distribution principle, different from the "VC model" in the Ethereum ecosystem, which can open the market in a short time through a wider wealth effect, triggering FOMO (in stark contrast to Solv Finance).

- The leading SFT token ORDI has experimental MEME coin properties, which bring more imagination (or consensus value) due to the lack of an intrinsic valuation model for such tokens.

- SFT has the dual advantages of FT and NFT, allowing it to directly use existing infrastructure for FT and NFT. Therefore, inscriptions tokens can be traded on NFT trading platforms like OpenSea, centralized exchanges like Binance and OKX, and even decentralized exchanges like Uniswap. Initially, when traded as NFTs, they have low liquidity, making it easier to drive up prices (pump), and after listing on centralized exchanges, there is a large amount of liquidity to support it.

- It captures overflow funds from the BTC ecosystem. For a long time, BTC holders who wanted to participate in DeFi, NFTs, games, and social activities could only do so through cross-chain operations. Now, there are native BTC products that can be used.

Valuation of ORDI

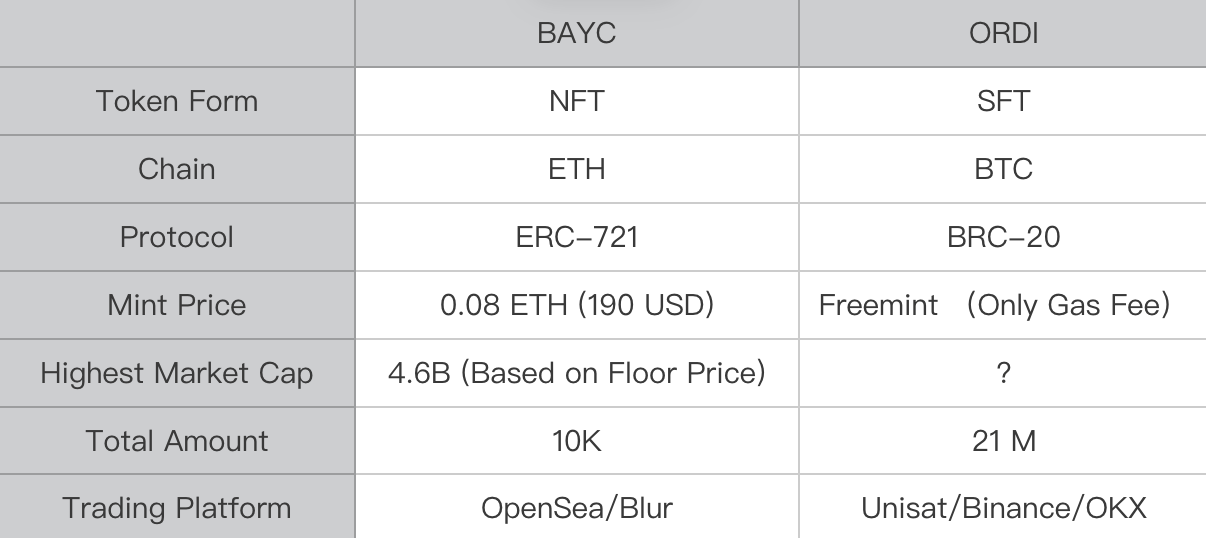

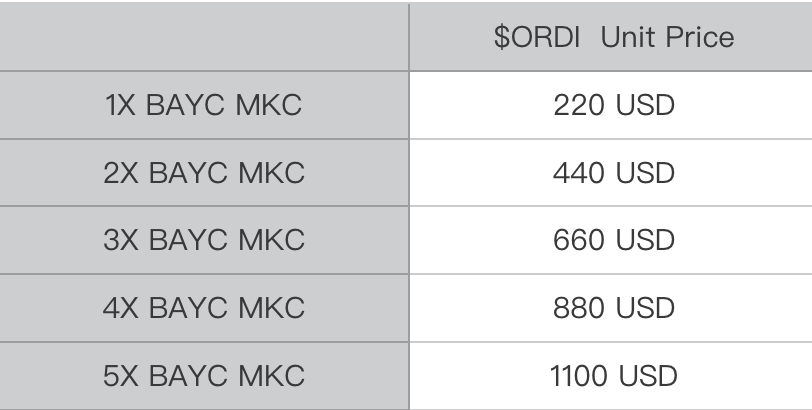

$ORDI is the first SFT token in the BTC ecosystem and has MEME properties, so it does not have an intrinsic valuation model. In other words, the only limitation is your imagination. However, we can still make an estimate by looking at the leading NFT project BAYC.

BAYC has always been a leading NFT project, similar to fair distribution (low-price minting), followed by a thousand-fold increase, reaching a peak market value of about $4.6 billion in May 2022.

As the first token of BRC-20, $ORDI only requires a small amount of gas to mint for free, and then it has increased by a thousand-fold. Its current price (December 2023) is stable at $70. Assuming ORDI continues to maintain its position as the leading SFT token in the future, its peak market value should at least align with BAYC, which would be $220 at that time. However, because $ORDI can be traded on centralized exchanges, its liquidity is much higher than that of NFTs like BAYC (many speculative traders only trade on centralized exchanges and do not use wallets), so a total market value 3-5 times that of BAYC is also acceptable. Therefore, we have the following table:

This method of valuation through horizontal comparison is of course quite rough, so take it with a grain of salt. After all, when emotions come into play, the price is up to you.

Several Misconceptions

Like the blind men and the elephant, when a new thing with many new features appears, each person may only see one leg or a long nose of the elephant, but don't think that is the whole elephant. In the past six months, I have seen many people's explanations, many of which have misled my understanding. It wasn't until I read articles by Mr. Wang Feng and Joslter that I truly understood the essence of inscriptions.

- Inscriptions are a new token distribution method.

This understanding is completely wrong. The so-called "engraving" is simply uploading content to the blockchain space, a method that has existed for several years. In fact, a few mining pools even offered related engraving services. And when Ordinals engraved NFTs, it did not catch on until it switched to engraving homogeneous tokens in JSON format. So the correct understanding should be: inscriptions tokens are a new form of token, SFT.

- Inscriptions are just a capital pump and dump for MEME coins.

This view was my previous understanding, and it is both right and wrong. After all, the bull and bear cycles of the entire web3 are too obvious. Any track, including DeFi and NFTs, follows a "narrative + pump + dump" cycle over a four-year period. And ORDI does indeed have MEME coin properties. But this understanding only sees the first leg of the elephant and does not see the essence of "inscriptions tokens as a new form of token, SFT," it is a biased generalization.

- Inscriptions are a backward technology, a regression.

This view is half right and half wrong. Currently, in public chains, the non-smart contract BTC chain and the smart contract ETH chain should not be confused. For the BTC chain, it seems that the only way to issue SFT is through BRC-20 or a variant of a similar protocol, but for smart contract public chains, issuing SFT in the form of inscriptions is indeed a regression from a technical standpoint, as there are better ERC-1155 and ERC-3525 standards. It can only be seen as speculation and hype.

- Inscriptions are a counterattack by the BTC ecosystem against the ETH ecosystem.

This view is half right and half wrong. The ETH ecosystem already has SFT standards, but it has not been developed, mainly because it has only involved VCs and institutions, not benefiting retail investors. Retail investors can only choose BRC-20 protocol tokens issued through fair distribution, which is a resistance to VCs and a resistance to the "orthodoxy" of Ethereum. However, this "resistance" is only the second leg of the elephant, not the elephant itself. Don't generalize based on a biased view.

- Inscriptions are like carving on gold.

This view is both right and wrong. If BTC is compared to digital gold, the metaphor is apt, but it still overlooks the essence of inscriptions tokens as a new form of asset, SFT, and is a biased generalization.

Through the above discussion, we can see that the essence of the inscriptions track is the outbreak of a new form of token, SFT. For non-smart contract public chains, the only way to issue SFT seems to be through the "memo field" of BRC-20, while for smart contract public chains, there are two ways: one is to issue through smart contracts using the VM, and the other is to issue through the "memo field" without using the VM. In the next article, we will explore the two evolutionary directions of "inscriptions tokens": recursive inscriptions and smart inscriptions.

This article is original by @hicaptainz.

Reference:

https://foresightnews.pro/article/detail/36629

https://www.theblockbeats.info/news/33844

https://www.chaincatcher.com/article/2105332

https://www.mytokencap.com/news/429220.html

https://www.bitget.com/en/news/detail/12560603860470

https://www.gate.io/en/blog_detail/1558/the-next-trillion-dollar-market-what-is-sft

https://www.sohu.com/a/646897073_382039

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。