According to the current assessment results from S&P Global Ratings, it believes that the stablecoins in the United States (Gemini, Pax, USDC) are the strongest, while offshore stablecoins (Tether, TUSD) are the weakest.

Compiled by: AiYing Compliance

New York, December 12, 2023 - S&P Global Ratings has launched its stablecoin stability assessment service, aimed at evaluating the ability of stablecoins to maintain relative value stability to fiat currencies. This is an important development for the company, which has committed to using its strong analytical and risk assessment capabilities to support both traditional finance (TradFi) and the growing decentralized finance (DeFi) client base.

S&P Global Ratings uses its analytical approach to assess the stability of stablecoins on a scale of 1 (very strong) to 5 (weak) based on the following criteria:

- Governance: This includes who can make key decisions, and which features can align interests with stablecoin holders, risk preferences, policy and reserve transparency, and the comprehensiveness and frequency of reserve proof or audit.

- Legal and Regulatory Framework: Considers the framework and the extent to which it can provide visibility and confidence in the stablecoin's future pegging ability.

- Convertibility and Liquidity: Analyzes the technical characteristics and protocols supporting the primary market convertibility of stablecoins, secondary market liquidity, and underlying payment rails.

- Technology and Third-Party Dependencies: Focuses on the risks related to the blockchain used for stablecoin exchange, core smart contracts, and potential third-party dependencies, such as reliance on data sources or oracles used by smart contracts.

- Track Record: Includes any recent decoupling, its reasons, and the reliability of remedial measures (if any).

Method of Assessing Stablecoin Stability

The stability assessment of stablecoins is S&P's view on the ability of a stablecoin to maintain its peg to a fiat currency (or a basket of currencies). The market price of stablecoins may deviate for various reasons. S&P will assess the impact of these deviations on their evaluation by integrating quantitative and qualitative factors. Quantitative factors mainly include:

- The degree of deviation of stablecoin price from the fiat currency (downward or upward);

- Duration of the deviation (long-term or short-term).

Some qualitative factors include:

- The reasons for the deviation—e.g., whether the deviation is primarily due to a decline in the quality of assets supporting the stablecoin or technical failures;

- Issuer/protocol response to the deviation—e.g., the issuer of the stablecoin committing to inject additional funds/assets when the assets supporting the stablecoin encounter issues.

For example, if S&P observes that a price deviation is not promptly corrected, such as due to the devaluation of reserve assets, and the stablecoin issuer does not have a credible action plan to address the issue in a timely manner, they may assign the lowest rating of 5 points, as S&P expects the stablecoin to be unable to re-establish its peg within a few days. They would only raise the assessment if they believe the fundamental reasons for the price deviation have been resolved or no longer exist. However, if S&P believes that the weakened track record may pose a risk to future price stability, they may maintain a weaker assessment.

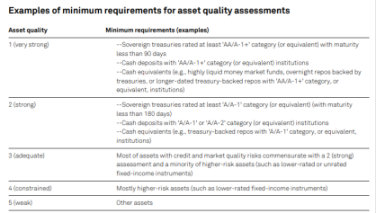

Asset Quality

When examining the quality of assets supporting stablecoins, it is necessary to consider several aspects:

- The credit risk of these assets;

- Whether the market value of these assets fluctuates;

- Who is responsible for safeguarding these assets, the quality of the custody agreement, and the trustworthiness of the custodian;

- Other factors that may affect asset liquidity, such as foreign exchange risk.

- When evaluating asset quality, there are minimum standards for credit risk and market risk (specific examples are shown in Table 1).

Rating Criteria:

- 1 point (very strong): If the credit quality of the assets is excellent—e.g., a country's debt rating reaches 'AA' grade, or cash deposits held in an institution rated 'A-1+', it would be considered very reliable and given 1 point.

- 2 points (strong): If the reserve assets are slightly lower in credit rating but still able to fulfill financial commitments, such as sovereign debt rated 'A' or cash deposits from institutions rated at least 'A-2', S&P would consider it reliable and give 2 points.

- 3 points (adequate): If most assets meet the minimum standard of reliability of 2 points as defined by S&P, but are mixed with some higher-risk assets (e.g., lower-rated or unrated fixed-income instruments), they would be given a moderate score of 3 points, considered adequate.

- 4 points (constrained): If the assets are mainly just enough to meet financial commitments, but are susceptible to economic downturns or changes, with higher risk, they would be given 4 points, indicating constraints.

- 5 points (weak): If the assets are mainly unstable (typical of stocks or cryptocurrencies), or if the current value of the assets is lower than the face value of the stablecoin in circulation, it would be considered unreliable and given 5 points, indicating a weak rating.

Circumstances Leading to a Downgrade

If S&P finds that the custodian of these assets has a questionable reputation, it may discount the rating of asset quality. A custodian with a poor reputation may bring logistical challenges and affect overall market confidence. If they believe that the current rating does not cover additional risks, such as those related to foreign exchange, they may also adjust the rating. For example, if the supporting assets are denominated in a different currency than the one pegged to the stablecoin, this risk may come to the surface.

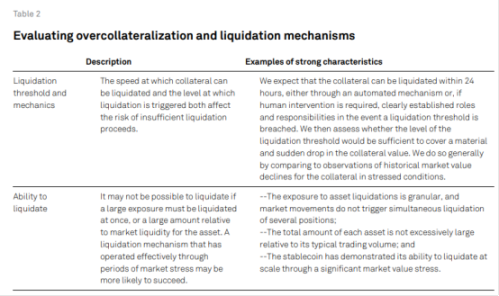

Overcollateralization and Liquidation Mechanism

Is your stablecoin overcollateralized and sellable?

If a stablecoin's collateral exceeds the required amount and there is a robust collateral liquidation mechanism to mitigate asset quality risk, S&P may raise the asset quality rating by two notches. The specific factors for the increase are shown in Table 2. If one factor is well-implemented, they would raise the asset quality rating by one notch; if both factors are well-implemented, they would raise it by two notches.

If a stablecoin is supported by multiple types of assets or overcollateralization and liquidation mechanisms, S&P would first need to analyze each pair of asset types and mechanisms separately. For example, they may find that a certain type of asset has a strong liquidation threshold, while another does not.

Next, they would consider how collateral losses would affect stablecoin holders. For example, if overcollateralization cannot be freely converted between various asset types, stablecoin holders may directly face the losses brought by the weakest asset type/mechanism combination, and their assessment would be based on this combination.

If a stablecoin's collateral includes a reserve fund specifically designed to cover collateral losses, they may not have this concern during the evaluation.

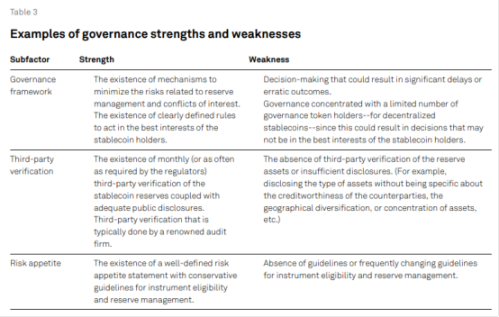

Specific Governance Analysis

I. Governance

S&P will analyze the risks associated with stablecoin managers (issuers), understand how their internal procedures and policies generate or reduce risks, and the frequency and comprehensiveness of third-party verification (see Table 3). S&P will also analyze the issuer's risk preferences and their approach to asset management.

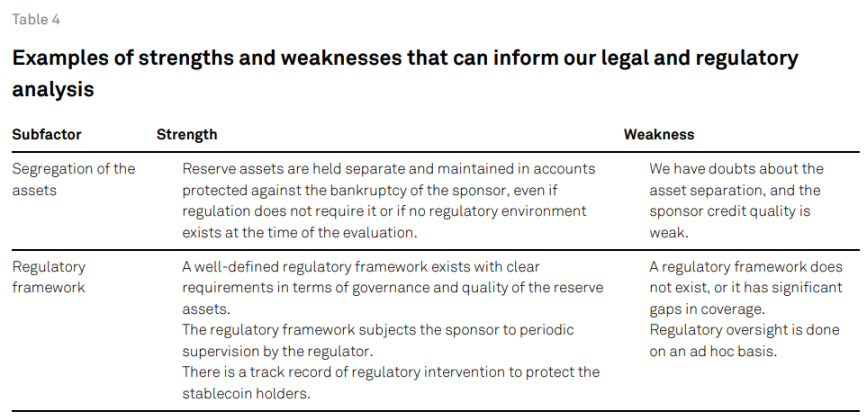

II. Importance of Legal and Regulatory Framework

The existence of effective direct or indirect legal and regulatory frameworks is crucial for stablecoins and their sponsors, as it sets legal and regulatory requirements to protect the rights of holders. For example, certain frameworks require the separation of reserve assets from the sponsor's assets, set minimum quality requirements for assets, or require regular supervision of stablecoin sponsors and their management.

First, we assess whether the reserve assets are legally separated from the sponsor's assets and whether they are protected in the event of bankruptcy. Then, we evaluate the scope and intent of the regulatory framework, as well as its focus on maintaining the stability of the coin. Additionally, we also examine the regulatory authority's ability to take preventive or corrective measures, such as when stablecoin sponsors fail to fully comply with requirements (see Table 4).

In general, we consider the lack or weakness of legal isolation of assets as a negative factor—unless we believe that the sponsor's creditworthiness is sufficient to minimize the risk to the assets.

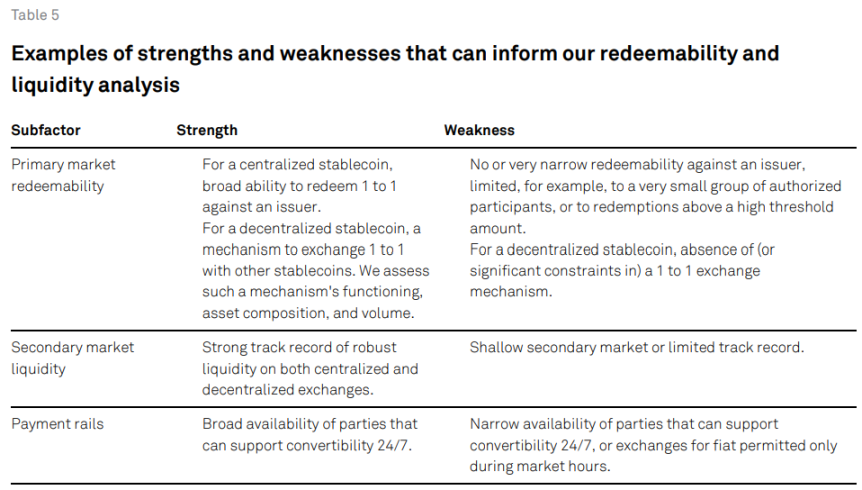

III. Convertibility and Liquidity

The ability of holders to exchange stablecoins for fiat currency at a 1:1 ratio provides an arbitrage opportunity, which can be used to support price stability when the market price of stablecoins deviates. S&P arrives at an overall liquidity and convertibility assessment based on a comprehensive evaluation of three sub-factors (see Table 5). The strength of one sub-factor may offset the weakness of another sub-factor.

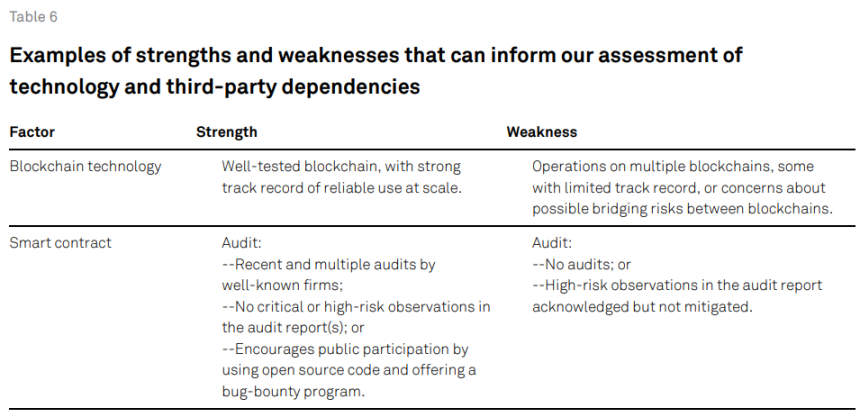

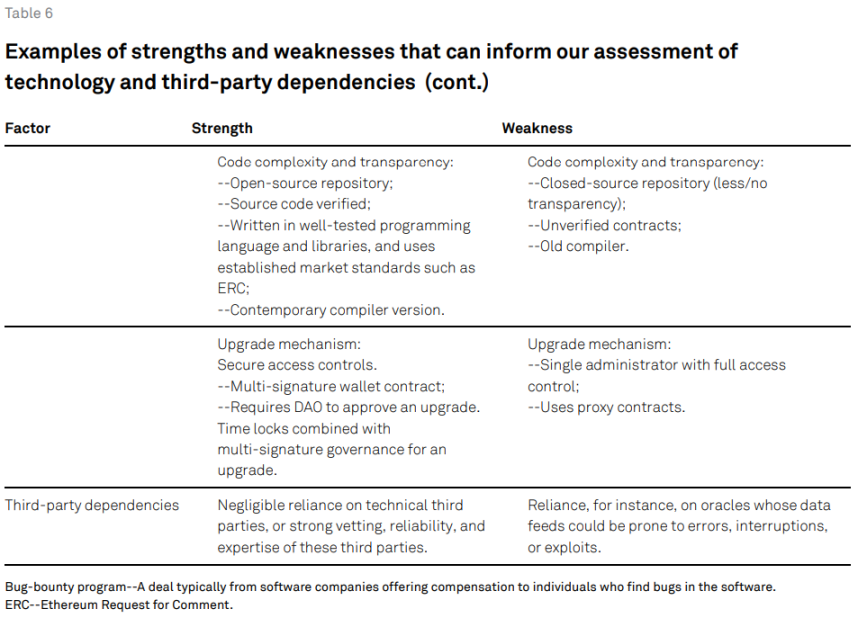

IV. Technology and Third-Party Dependencies

The blockchain technology and smart contracts supporting stablecoins have a significant impact on the stablecoin's ability to maintain its peg to fiat currency and the ability of holders to timely convert to fiat currency. They consider three sub-factors in the overall assessment (see Table 6).

Blockchain Technology Resilience

S&P evaluates the strength of the underlying blockchain technology. For example, they consider how long it has been operational, the volume of transactions it has processed, and its reliability record and any history of interruptions or failures. Some stablecoins operate on multiple blockchains, which can support stability by opening additional sources of liquidity but may also pose potential risks to users when transitioning from one chain to another (often referred to as "bridge risk").

Smart Contract Resilience

S&P also focuses on the quality of smart contract audits, code complexity and transparency, and upgrade mechanisms. Definitions of related terms can be found in the glossary.

Audit is a critical step in identifying and mitigating potential vulnerabilities that could lead to fund losses. Multiple external audits by reputable audit firms generally serve as a positive factor in their assessment of smart contract strength.

In terms of code complexity, it is crucial to write smart contracts using well-tested programming languages and modern compiler versions. Using outdated compiler versions with known vulnerabilities may lead to exploitation. In terms of transparency, best practices include open-sourcing the repository of smart contracts and allowing verification of the source code, enabling anyone to inspect and verify the functionality of smart contracts.

S&P also focuses on the upgradeability of smart contracts, which involves changing business logic while retaining the contract state. Upgradeability allows for the resolution of vulnerabilities while the smart contract is running. However, it is important to understand who has the authority to implement upgrades and what security measures have been taken to prevent malicious actors from modifying smart contracts. Using proxy contracts adds complexity and increases the likelihood of critical flaws.

Third-Party Dependencies

These may include dependencies on technical aspects or on oracles.

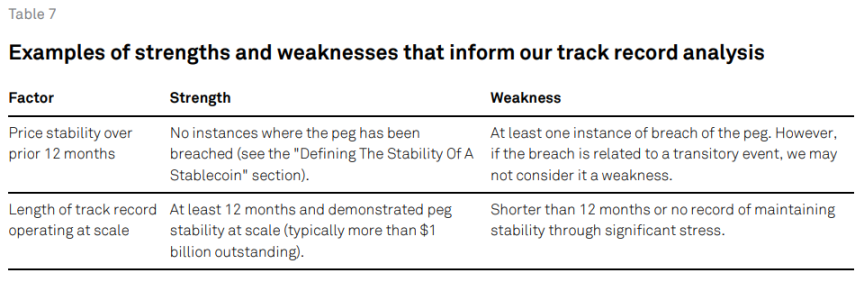

V. Track Record

S&P typically examines a stablecoin's price stability record over the past 12 months and how long it has been in operation on a large scale (see Table 7). They also assess past decoupling events, as described in the "Defining Stablecoin Stability" section.

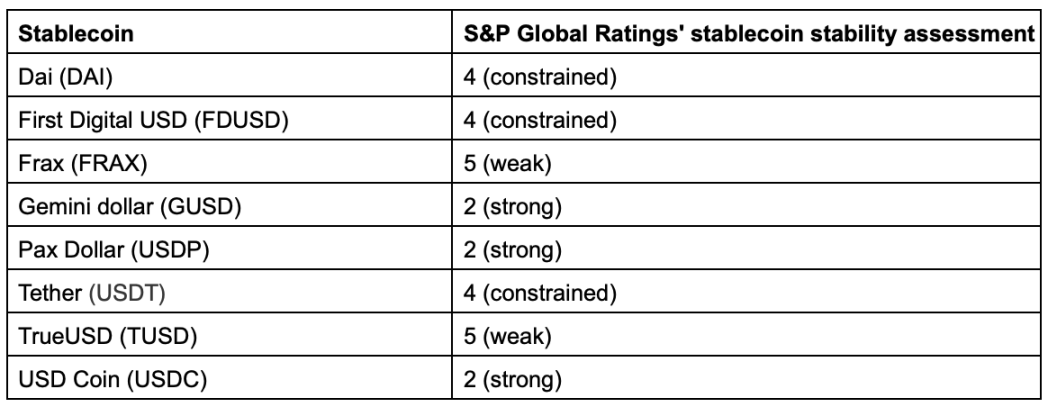

Assessment of Eight Leading Stablecoins from Strongest to Weakest

According to S&P's analysis, the public assessment of eight stablecoins: DAI, FDUSD, FRAX, GUSD, USDP, USDT, TUSD, and USDC, shows their stability in maintaining peg to fiat currency ranging from 2 (strong) to 5 (weak) (see the table below).

As indicated by their analysis method, the quality of assets supporting stablecoins is the key driving factor in the final assessment. In other areas, weaknesses in regulatory oversight, governance, transparency, liquidity and redeemability, and track record are the main factors contributing to lower ratings for stablecoins (algorithmic stablecoins and stablecoins based on corporate credit are not within the scope of the assessment).

According to the current assessment results from S&P Global Ratings, it believes that the stablecoins in the United States (Gemini, Pax, USDC) are the strongest, while offshore stablecoins (Tether, TUSD) are the weakest.

Sources:

https://www.spglobal.com/_assets/documents/ratings/analytical-approach-stablecoin-stability-assessments.pdf

https://www.prnewswire.com/news-releases/sp-global-ratings-launches-stablecoin-stability-assessment-302012532.html

https;//www.aiying.io

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。