This article details the underlying mechanism flaws of Terra, the operating mechanism and unique architecture of Mint Cash, and the related token airdrop plan.

Author: Shin Hyojin, Founder of Mint Cash

Translator: Frank, Foresight News

In fact, what happened with Terra and its stablecoin ecosystem is truly one of the most interesting, dramatic, and unbearable stories in the history of cryptocurrency, second only to the collapse of FTX in terms of value loss.

While critics may tell investors involved in the Terra/LUNA collapse that they participated in a carefully planned Ponzi scheme over the past three years, a closer look at how Terra started, what it once promised, and who was affected reveals that the reality is not so simple.

This is a stablecoin project that promised a truly meaningful vision and had the execution capability to make it work.

Case Study of "Decentralized" Stablecoins

We have heard countless stories of people converting their funds into UST and depositing them into Anchor Protocol instead of a bank account. This is not because they are fervent cryptocurrency enthusiasts blindly investing in leveraged trading, but because UST allows them to access the banking infrastructure that many of us take for granted.

For example, some families in Ukraine transferred their life savings to Anchor deposits because their banks were closed during the war; people in Venezuela, Argentina, and other Latin American countries hold UST and deposit it into Anchor because their governments do not allow them to freely hold and exchange dollars to hedge against inflation; small communities in sub-Saharan Africa hold UST instead of dollars, trying to avoid the impact of foreign exchange controls during inflation. But they were all severely affected after the collapse of UST.

These are the real stories revealed by people who sent emails to a former Anchor employee shortly after the collapse of UST. In a similar crisis, more people were also severely affected by FTX because they believed they held their USDT in their spot accounts at FTX, and 6 months later FTX also collapsed.

Are they no longer so foolish and have withdrawn all their money from cryptocurrencies? No, most of them actually turned to holding USDT in Binance hot wallets or Binance Earn, desperately trying to hedge against inflation in the absence of stable financial infrastructure.

Most of the liquidity in cryptocurrencies does indeed come from speculative demand, which no one in the crypto industry can deny, and it is not likely to change soon. We even hope to get the same speculative demand, but ironically, it is an unexpected side effect that makes UST on Anchor or USDT on exchange wallets a speculative demand.

Why do they choose USDT or UST instead of something fully regulated? It is well known that neither of these stablecoins has 1:1 fiat currency backing. For UST, the situation is relatively simple—the 20% yield provides these people with a good opportunity to easily hedge against crazy inflation levels. But for USDT, this is actually because they often have higher over-the-counter liquidity, as Bitcoin liquidity is highly correlated with USDT.

"Unregulated" makes them a popular choice for drug traffickers and criminals, and also allows people in regions with inadequate financial infrastructure or high capital and foreign exchange controls to safely avoid the devaluation of their national currency.

We are the same, we believe in the right to financial privacy and capital freedom of movement, and stablecoins not fully backed by "legal" assets are more likely to achieve these properties, as proven by USDT and UST. Holding Bitcoin directly is another popular choice, but in an economy where dollarization has made significant progress, this may not be a choice for many people.

UST and Anchor have the opportunity to be a better choice than USDT, as Anchor deposits do not require the complex KYC login process of exchanges, especially for those who should rely on over-the-counter trading in any case. For the average person, it is simple enough to replace exchange-based stablecoin savings products.

However, in a fatal collapse of UST and Anchor, the world lost a potential better alternative to USDT. This is the beginning of our story.

Terra Stable Mechanism: The Story So Far

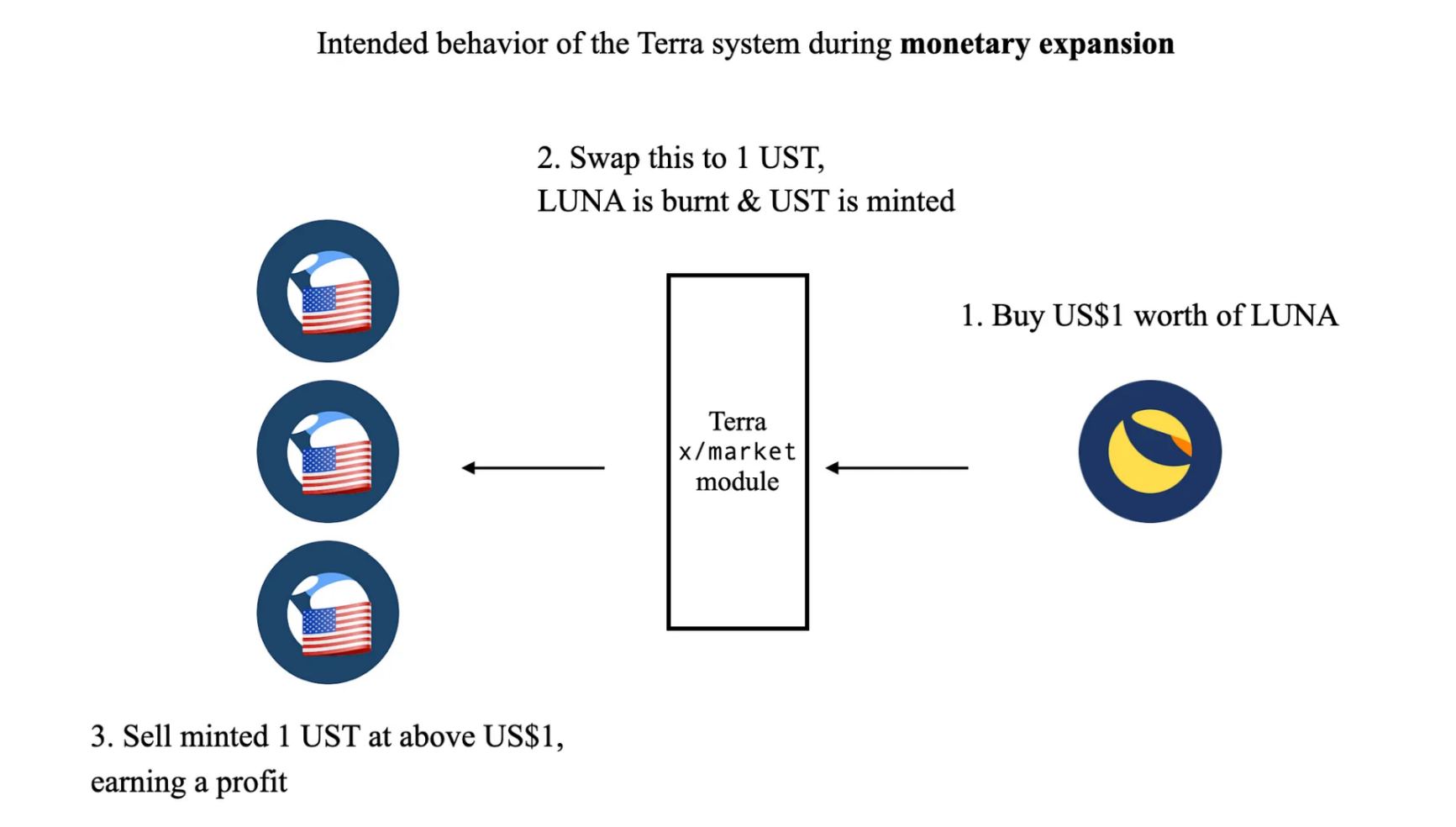

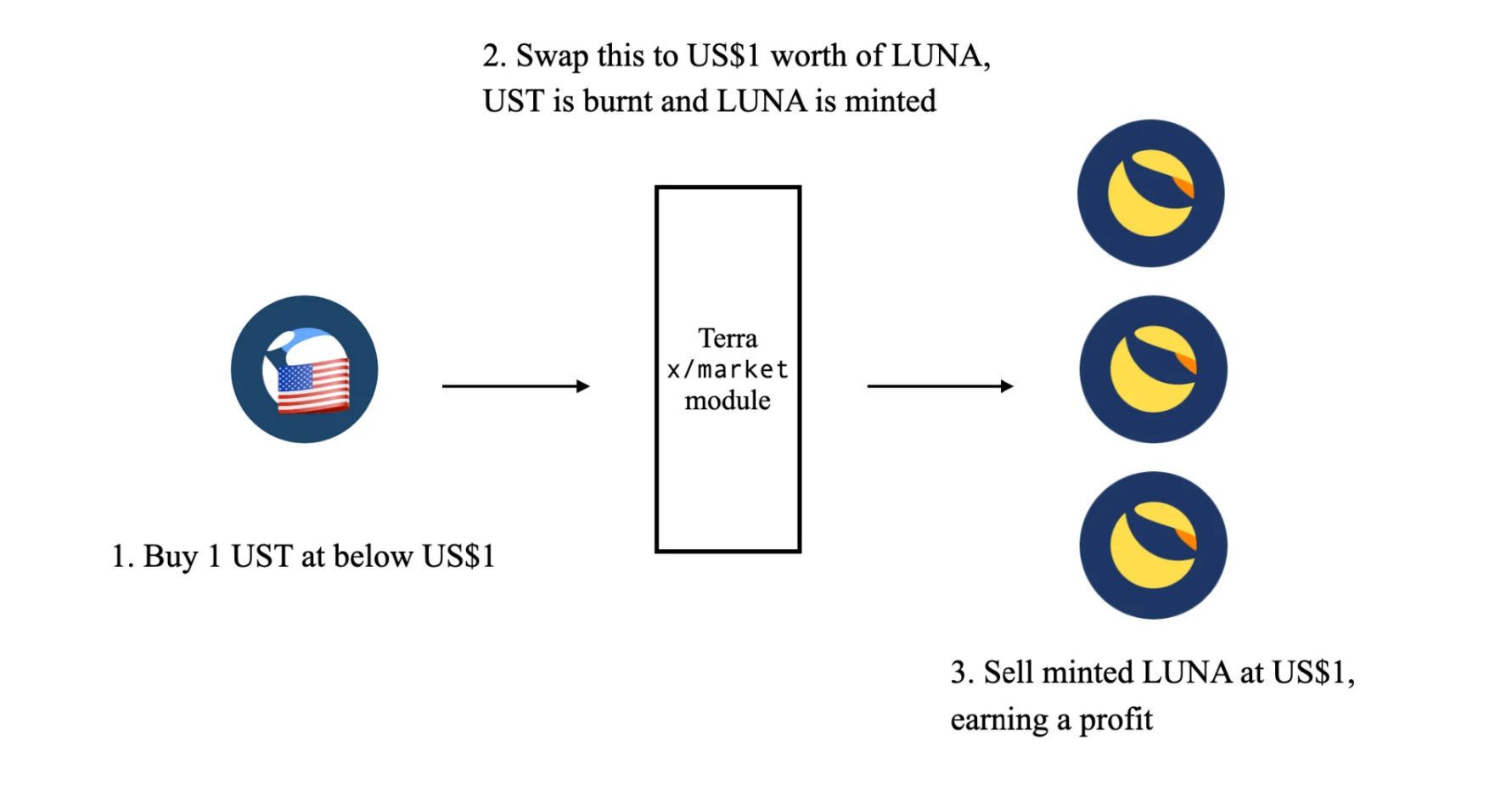

Before we delve into the details, let's briefly review how Terra works. UST is an "algorithmic" stablecoin designed to be pegged to 1 USD through an arbitrage-based mechanism that allows UST to be synthetically exchanged with LUNA.

The basic idea behind Terra is to allow 1 UST to always be exchangeable for 1 USD-worth of LUNA, with the value of LUNA provided by Terra's price oracle protected by validators, and vice versa.

- When the value of 1 UST is higher than 1 USD, external arbitrageurs are incentivized to buy LUNA worth 1 USD from the market, exchange it for 1 UST, and sell it at a price higher than 1 USD to make a profit;

- When the value of 1 UST is lower than 1 USD, external arbitrageurs are incentivized to buy 1 UST at a price lower than 1 USD, exchange it for LUNA worth 1 USD, and sell it at a price of 1 USD in the market to make a profit;

At least, this is the theoretical operating mechanism, and the rest is history.

So, what went wrong?

First, there are several little-known facts about the actual operation of Terra's minting (officially known as the Terra Market Module) because the above explanation is oversimplified and omits several key points.

The Terra Market Module executes the above minting and burning synthetic exchange mechanism (first implemented in Columbus-2) based on two parameters set by governance (BasePool and PoolRecoveryPeriod):

BasePool is a parameter defined in TerraSDR units that defines the total virtual liquidity available for exchange over the PoolRecoveryPeriod block count period;

PoolRecoveryPeriod is a parameter defined in Tendermint block count that defines the frequency at which BasePool should be reset (replenished) to its initial state;

In the Terra system, it is crucial to set these parameters correctly, as if the virtual liquidity parameter is not set slightly below the actual market liquidity of LUNA (i.e., relative to the actual fiat currency on exchanges), the entire system will quickly spiral into a death spiral.

Identifying the Basic Problems of the Terra Stable Mechanism

Why is this happening? Let's see what happens in the following scenarios without external market makers maintaining the peg:

Virtual liquidity is significantly less than the actual market liquidity of LUNA

When external participants sell large amounts of LUNA in the market (which is much higher than the liquidity defined by the on-chain market module), and at the same time, the value of UST also decouples downwards, the system will not have enough virtual liquidity to keep up with the trading volume of LUNA in the external market.

This means that even with enough external arbitrageurs participating, the on-chain market module cannot burn enough UST to mint LUNA on time to restore the value of UST, and the decoupling of UST becomes prolonged, leading to a loss of trust in the system, more UST being sold—over time, the crisis will only worsen until it loses all value and enters a death spiral;

In theory, in this situation, although with the loss of trust in the system, people are likely to sell the LUNA they hold, the supply of LUNA will not be affected.

Virtual liquidity is less than the actual market liquidity of LUNA

This means that if there is enough capital, manipulating the market value of UST below 1 USD is relatively easy (due to low market liquidity). Even without attackers, a large number of people trying to exit the system will lead to this problem.

But this time, the on-chain market module can mint more LUNA than the external market can handle, and due to this oversupply, the value of LUNA rapidly plummets. If this situation continues, LUNA will continue to be minted until it loses all value, and as LUNA loses value, UST will also lose any value, leading to arbitrage against the market module and entering a death spiral.

In simple terms, buying LUNA from the market will not have arbitrage incentives, as the on-chain changes will be less than the actual buying pressure off-chain, leading to unlimited minting of LUNA.

To prevent the second scenario from occurring, the Terra whitepaper initially defined a maximum upper limit for the supply of LUNA—this was quietly removed at some point between Columbus-3 and Columbus-4, leading to unlimited minting of LUNA during the Terra crisis. Even if they did not remove the upper limit on the supply of LUNA, a death spiral similar to the first scenario would follow when the contraction of UST supply is required to be greater than allowed by the supply limit.

Another change introduced shortly after the Columbus-4 upgrade was to redirect all UST/LUNA exchange transactions on the Terra Station frontend to Terraswap (and later Astroport), while the LUNA/UST exchange transactions on Terra Station continued to burn LUNA to mint more UST.

While the actual functionality of Terra Core itself remains intact (i.e., manual interaction through Terra LCD will still allow for the native exchange of UST to LUNA), end users have effectively lost the ability to contract the value of UST. Columbus-5 made another change to the market module, allowing different exchange liquidity limits for UST to LUNA and LUNA to UST exchanges, but this was reverted shortly after.

Another important parameter of the Terra Market Module is the oracle time delay, but many people are not aware of this. In 2019 alone, Terra experienced one oracle attack, leading the team to deploy patches on the Terra oracle that largely improved oracle-based attacks but sacrificed potential decoupling resilience.

Initially, the Terra oracle only provided the current spot price of LUNA to the on-chain market module. This led to an attack—attackers artificially created large bid-ask spreads for LUNA on the South Korean cryptocurrency exchange Coinone, allowing attackers to repeatedly exchange TerraKRW (another stablecoin pegged to the Korean won instead of the USD) and LUNA on-chain, although with little funds, it allowed for the minting of more LUNA than initially intended.

The Terra team initially responded by temporarily deploying additional exchange liquidity to narrow the spread, and then changed their oracle logic from spot price to a 15-minute moving average. This did not prevent the same attacker from executing another attack, a similar attack—just forced to execute the same attack over a longer period (due to the additional 15-minute delay). Therefore, the Terra team responded again by changing the oracle logic to a 30-minute VWAP of on-chain spot price data.

As pointed out in Medium articles and reports, this made sense at the time, as the liquidity of LUNA on exchanges was low.

However, this requires trade-offs, slower oracle price feeds would mean arbitrage between on-chain and off-chain markets is also possible, quickly diluting the value of LUNA.

However, Terra did not seem to truly delve into this oracle trade-off issue until the collapse of Terra, and the only parameter adjusted was the time delay between spot price and on-chain oracle.

The stronger liquidity of the LUNA market triggered other issues that were not covered in any of the company's previous research: the implicit risk caused by oracle delays in high liquidity markets with high trading volumes. Typically, as markets become more liquid, assuming lower volatility, because the more liquid the market becomes, the more capital is needed to effect the same change in spot price. However, this is not always the case—when markets become volatile in these environments, there is a large outflow of capital.

In this scenario, if there is a problem, the oracle delay will be fatal, as the arbitrageurs described above have a lot of room for capital outflow. Since UST liquidity on DeFi was limited to AMMs like StableSwap (such as Curve Finance), which did not exist in 2019, this made the issue more severe, as StableSwap curves are designed to maintain the peg for as long as possible until it quickly decouples.

As mentioned earlier, due to the inherent delay of Terra's oracle, it simply does not have enough time to cope with high volatility and high liquidity markets.

In conclusion, we believe that even as the Terra ecosystem continues to evolve, further research has not been conducted in this area, and it is expected that Luna Foundation Guard (LFG) will take over this work by becoming another native module on the Terra blockchain holding Bitcoin as collateral. In this process, it is speculated that market makers will take over the maintenance of the UST peg without fundamentally changing its underlying mechanism—unfortunately, the well-known attack occurred before TFL and Jump Trading fully implemented the original native LFG module plan.

Mint Cash: Continuing from Where We Left Off

Mint Cash is a continuation of the work done in the Terra stablecoin system, addressing its mechanism-level flaws and unlocking more use cases. This is a major redesign involving many fundamental changes, to the point where it is closer to a overcollateralized stablecoin like DAI rather than an algorithmic system like UST. Specifically:

- All stablecoins are fully backed by Bitcoin collateral, partly inspired by Jump Trading's original proposal for Luna Foundation Guard (LFG);

- Providing an organic synthetic exchange mechanism between the Bitcoin collateral, Mint (equivalent to LUNA), and CASH (equivalent to UST);

- Anchor becomes part of the stablecoin leverage, rather than a printing press;

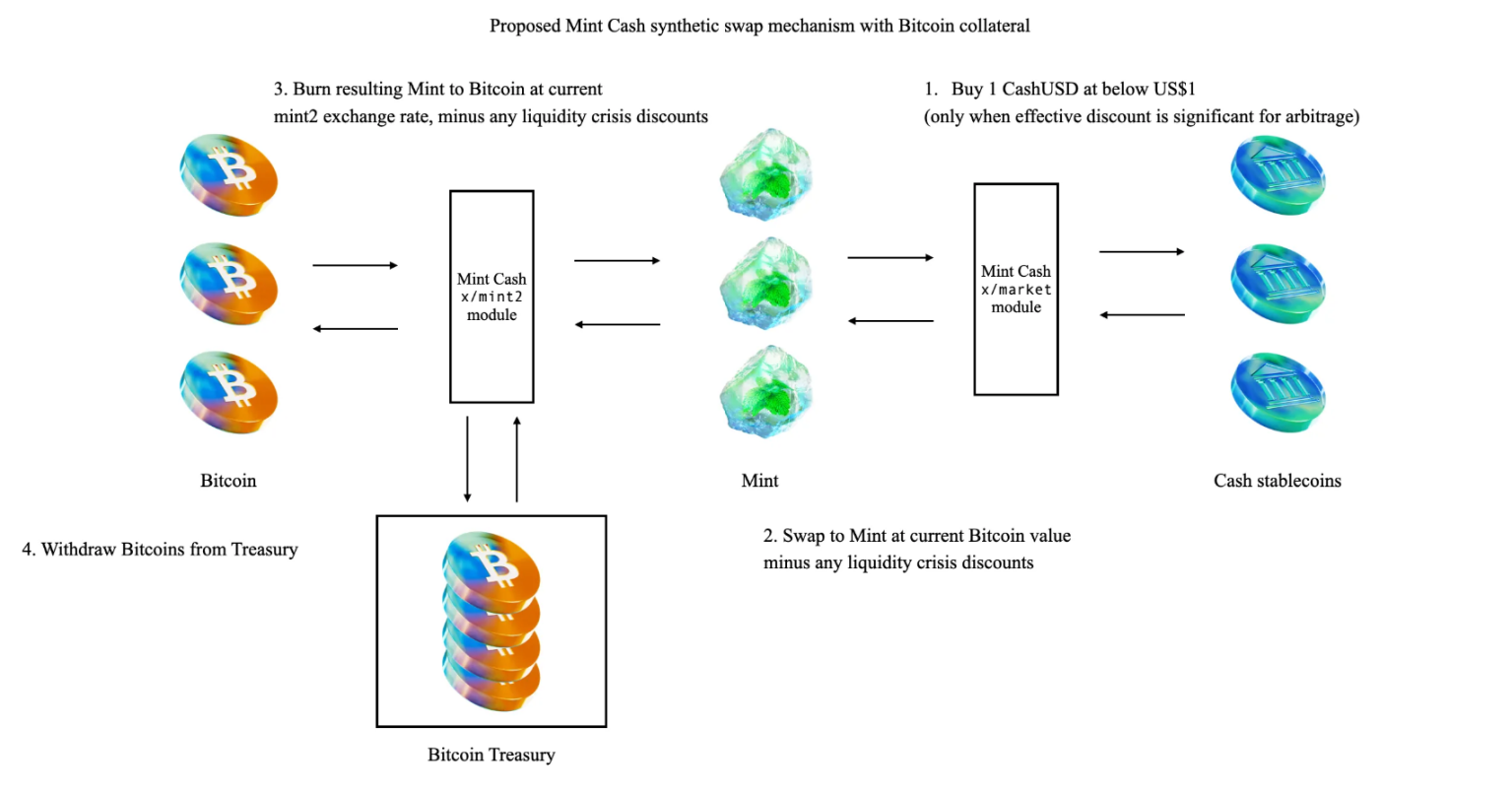

The first challenge of this redesign is defining a market where the Bitcoin collateral can be synthetically exchanged for stablecoins, and vice versa—similar to LUNA/UST. The Luna Foundation Guard (LFG) proposal suggested creating another market module and allocating virtual liquidity parameters governed by simulated Bitcoin liquidity—similar to the existing market module between UST/LUNA.

One issue with this approach is that there will be no market liquidity between the stablecoins we create and the Bitcoin collateral at launch. When there is no market liquidity, it may not be possible to set the synthetic market parameters as there is no reference market to determine these parameters.

To mitigate this situation, we have used a new type of trading curve, which essentially generates trading liquidity on demand. This will serve as the initial market generation bootstrapping mechanism, as it can establish a market for any existing illiquid asset, as long as there is demand for those assets in exchange for liquidity assets.

This also involves a trade-off, as this curve will generate exponential implied volatility (i.e., exponential increase in delta and linear increase in gamma values), so the goal is to gradually phase it out through a hybrid market with both on-demand liquidity and synthetic market curves (similar to the original LFG proposal).

This process is completely permissionless and does not require intervention from the project team. Anyone can "exchange" Bitcoin for MINT or CASH. Perhaps most importantly, without providing explicit Bitcoin collateral, it is not possible to mint new MINT or CASH. This also means that under this redesign, any free airdrops or private sales of tokens are not possible.

The value of MINT represents how much of the corresponding assets in the Mint Cash system are explicitly collateralized by Bitcoin. This also means that similar to the oracle attack described above, it is possible, but as an initial mitigation measure, the value of Bitcoin is used as an oracle reference rather than directly obtaining the market value of MINT, which is likely to initially lack liquidity.

This is intended to mitigate some of the oracle issues mentioned above by introducing non-synthetic assets as collateral, resulting in a linear correlation between price and oracle, rather than exponential.

In summary:

- Anyone can mint MINT by providing Bitcoin collateral through the "mint2" module;

- Anyone can burn MINT to exchange it back for Bitcoin, minus any taxes or liquidity discounts;

- MINT can be freely exchanged with the stablecoin CASH through the market module;

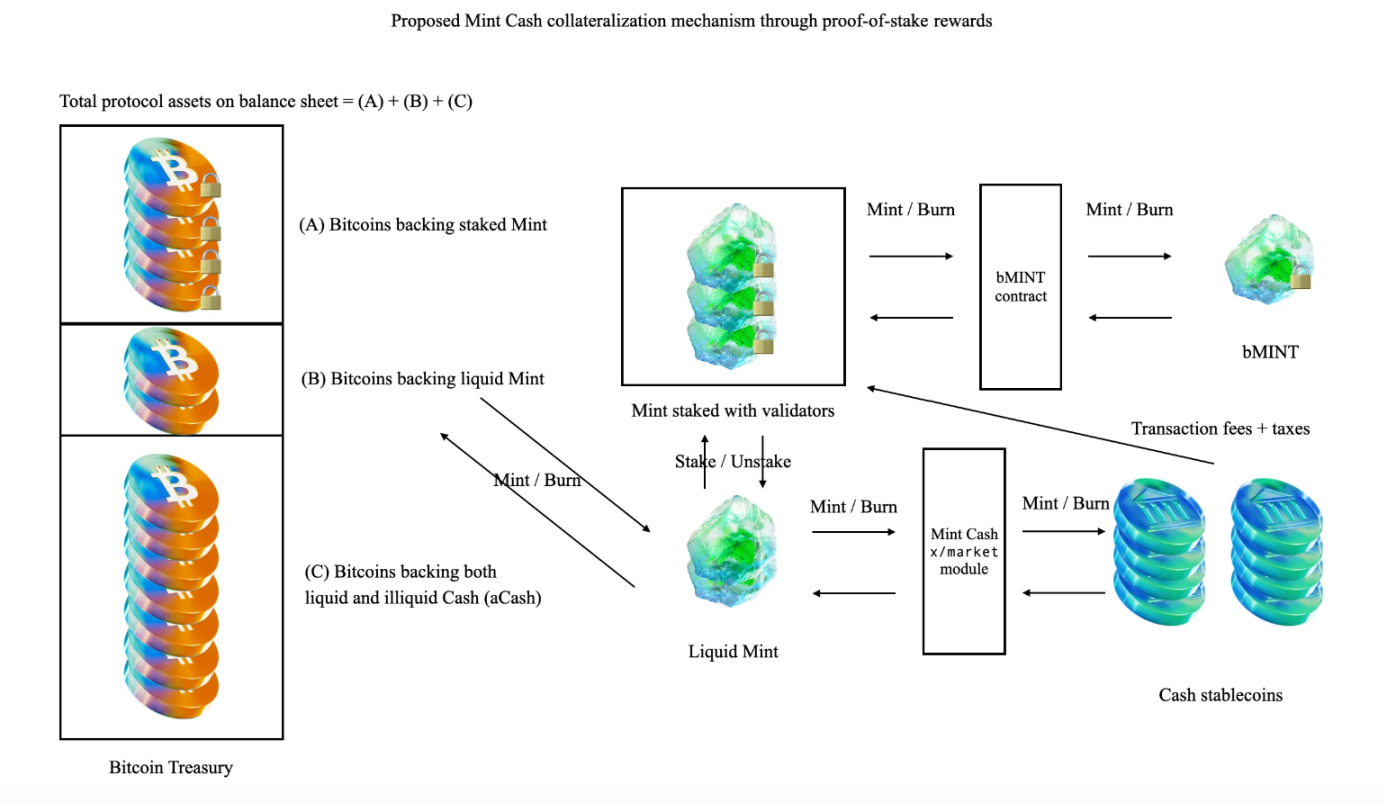

This sounds quite simple. Additionally, there are four additional key mechanisms to ensure the stability of the currency:

- MINT staking module (bMINT) with a time limit for unstaking;

- Liquidation module;

- Tax module (inherited from Terra's original tax policy);

- Anchor Sail itself;

MINT Staking: Better Overcollateralization, Incentivizing PoS

A major issue with overcollateralized stablecoins like DAI is the lack of incentives for providing and withdrawing stablecoin supply. As Do Kwon pointed out in a previous Medium article:

DAI is the most widely used decentralized stablecoin on Ethereum, but it has serious scalability issues due to the mismatch between its monetary policy and supply and demand.

DAI is provided by users looking to leverage exposure to ETH and ERC-20 assets;

Users looking for a stable value store in USD on-chain need DAI;

When the demand for stability exceeds the demand for Ethereum asset leverage, this mismatch becomes a problem. The recent use of DAI in many DeFi protocols has led to a significant increase in demand for DAI (mismatched with leverage demand), resulting in trading at a significant premium to the USD, and the Maker Foundation has taken emergency measures to restore the peg.

The scalability issues of DAI can also extend to all other stablecoins on Ethereum, where the cost of minting these stablecoins is higher than the face value of the minted assets. The currency supply is limited by the willingness of the market to bear excess capital costs (e.g., leverage demand), which is unrelated to the demand for stablecoins. In turn, the obstacles of DAI's monetary policy also limit the growth and adoption of DeFi.

Objectively, his statement about the issues with DAI is very reasonable. Overcollateralization relies on taking on leveraged positions, which are essentially leveraged long positions. Clearly, people prefer to seek stablecoins rather than go long on ETH or other assets, leading to a mismatch in supply and demand.

So, how do we solve this problem while ensuring that the system always remains collateralized? Our answer is actually to combine it with Proof of Stake (PoS) and liquidity staking.

Staking means actively taking on financial risk and committing to long-term network growth in exchange for stable transaction fees. This aligns perfectly with those who want to provide collateral for stablecoins, as they also actively take on financial risk and commit to stability, while also receiving some rewards generated by the system.

People can either delegate MINT to validators or mint bMINT (a derivative of Mint for liquidity staking), taking on the risk of under-collateralization while exclusively receiving ongoing transaction fees, as well as taxes levied on stablecoin CASH or Anchor interest.

This makes staking MINT slightly different from standard PoS blockchains. Firstly, in the event of a protocol-triggered liquidation, MINT stakers are first affected by the average cut across the entire validator set (without the consequences typically brought about by other security-related slashing events). The protocol also sets a minimum staking rate globally, which is used as a factor in whether to trigger protocol-wide forced liquidation.

Unstaking may also be subject to a vesting period, meaning that MINT will be released from staking after a period of time, rather than immediately.

Protocol-Wide Collateral Liquidation

Another feature of the Mint Cash system is the protocol-wide liquidation module, which exists in most synthetic asset protocols. When the current value of staked MINT falls below the minimum minting collateralization rate, liquidation is triggered, calculated as follows:

mintstakingrate = stakedmint / (stakedmint + liquidmint + (liquidcash + acashsupply) * mintoracle_price)

There is a protocol-wide parameter "LiquidationWeights" that determines how much indirect loss MINT stakers should face compared to liquid MINT, to bear the responsibility of currency contraction. This is necessary because:

- Liquidating heavily weighted MINT collateral will lead to significant decoupling of bMINT, which will also lead to liquidation of the Anchor Protocol—potentially exacerbating the possibility of protocol runs;

- Liquidating lightly weighted MINT collateral will result in a higher impact of MINT on the Bitcoin oracle price;

In the liquidation auction, both MINT and CASH are accepted. Bids priced in CASH take precedence over bids priced in MINT. Any assets received will be immediately burned to ensure that the current MINT collateralization rate is above the minimum collateral threshold.

Additional fees are charged for liquidation events:

- Protocol liquidation fee: a fee charged by the protocol to control fund outflows;

- Liquidation premium: paid to the liquidator as compensation for participating in the protocol liquidation;

Cash Tax

Mint Cash directly inherits Terra's monetary policy, which, in addition to standard transaction fees, also imposes taxes on transactions priced in stablecoins. There are two reasons for this:

- No inflation risk incentives: Unlike most PoS assets, there is no inflation in the Mint Cash system, as all minted assets must be directly backed by Bitcoin. This is particularly important because MINT stakers bear additional collateral risks compared to liquidity MINT holders—additional incentives are needed for this;

- Monetary tightening economic leverage: Typically, higher tax rates are associated with monetary tightening, and vice versa, similar to interest rate factors. When monetary tightening is needed, the adjustment speed of these monetary levers should be faster than standard governance proposals (if needed) in addition to standard liquidation procedures, due to the direct correlation between tax rates and interest rates in the Mint Cash system, this is relatively insignificant;

Anchor Rates as Part of Mint Cash Monetary Policy

In modern economic theory, domestic interest rates play a crucial role in monetary policy and stability. The 20% interest rate on Anchor is crucial to Terra's tremendous success—claiming to be the "benchmark interest rate for all DeFi." DAI also has a similar concept called DAI Savings Rate, which also incentivizes staked DAI holders to earn some interest while contributing to the protocol's stability.

It is worth noting that higher foreign interest rates are always associated with higher leverage costs (i.e., reduced liquidity in the domestic market), higher inflation rates (i.e., currency devaluation in the foreign exchange market), or both. Meanwhile, lower rates are generally considered to lead to net capital outflows.

Given this, we can establish a "safety buffer rate" between on-chain anchored currency rates and real-world rates, where the difference in rates is sufficient to prevent large-scale capital outflows without leading to higher effective borrowing rates. This buffer rate can be funded by:

- Returns provided by external liquidity staking derivatives, including staked ETH, staked SOL, staked ATOM, etc.;

- Any efficiency improvements achieved through smart contracts automating the loan process rather than through banks, resulting in less spread;

As long as external LSTs (such as Lido or EigenLayer) have sufficient risk hedging strategies or resilience to known slashing events to maintain a constant known rate relative to their underlying assets, the LST can also be used to represent leveraged positions of underlying un-staked assets. Hedging positions can also be used to combine multiple asset positions and reduce risk while increasing return exposure. This should help incentivize borrowing on the protocol, rather than relying solely on market makers or artificial token incentives.

As mentioned earlier, stablecoins deposited into Anchor are not subject to taxation. However, their interest will be automatically taxed, either burned or transferred to the treasury to reward MINT stakers. As this corresponds to the synthetic M1 supply, while the underlying cash corresponds to M0, exporting CASH to other blockchains may focus on aCash (anchored deposited cash) rather than underlying CASH to simplify tax calculations.

Anchor Sail is our new version of Anchor, also featuring non-USD denominated deposit functionality. This is achieved through a new synthetic forex lending module, allowing users to borrow CASH pegged to another stablecoin they are familiar with, such as CashEUR or CashKRW. Since CASH can be minted as long as Bitcoin has liquidity against the underlying currency, this greatly expands the coverage for users who want to continue using non-USD currencies—this was also a primary feature request for the original Anchor.

Why not build on Terra Classic?

A common question we have received from the Terra/LUNA Classic community is: why not build on Terra Classic to rebuild UST?

We need to start from a clean slate for several reasons:

- Fundamental redesign—Fundamentally, Mint Cash is a radical redesign, although still based on similar ideas, concepts, and blockchain code that once powered the old Terra stablecoin protocol. While we could fork the existing Terra Classic and start from there, some of the damage caused by excessive inflation may be irreversible;

- Unresolved flaws—As mentioned above, one of the reasons for this complete redesign is because the old Terra stablecoin protocol has fundamental flaws that have gone unresolved for years. In any case, this would require a major rewrite of the core stablecoin protocol itself. Such work is beyond the scope of a single team working on an existing blockchain but requires the funding, support, and infrastructure level of a new company and project;

- Centralized infrastructure—Some infrastructure, such as the LCD (Light Client Daemon) and block explorer, is gradually becoming independent of Terraform Labs, thanks to the work of the Terra Classic community. However, the Terra stablecoin protocol and a significant portion of its core DeFi building blocks (such as Anchor) are designed to be operated by centralized entities rather than for fully decentralized ownership migration. This includes the WLUNA contract on Ethereum (originally designed as part of the now-retired Shuttle Bridge, as part of Mirror, without providing appropriate design choices for decentralized asset migration on the Ethereum blockchain), Anchor/Mirror, and other TFL-built protocol CosmWasm contract ownership, and operational infrastructure associated with these smart contracts (e.g., Anchor commands manually called by the contract administrator every Epoch);

- Asset allocation and curbing inflation—With the collapse of the Terra stablecoin, severe inflation has led to significant entities holding large amounts of these now nearly worthless tokens, which is detrimental to ordinary LUNA holders. Asset allocation on the Terra blockchain has been very centralized among TFL, VCs, exchanges, market makers, and large validators. In conclusion, fixing all these issues without a reboot would be very difficult, as even a full chain rewrite would leave these participants with a significant supply;

However, we also sincerely hope to help the Terra Classic community at least recover from some of the significant losses caused by the catastrophic collapse of the Terra stablecoin system. This is why we have decided to introduce a "Burndrop" program, where only those interested in the new ecosystem we intend to build can receive rewards, while those uninterested can still benefit from the burned tokens and reduced supply.

Burndrop: Airdrop Allocation Plan for Burning USTC

The Burndrop program will distribute a basket of tokens, which will be distributed upon the launch of Mint Cash. This will include the following two assets (with the possibility of including more tokens as the situation develops, as we continue to build the Burndrop plan for final distribution):

- oppaMINT (OPtion Per Annum MINT): a special call option token that allows its holder to mint new bMINT at a high discount rate (50%+) based on the current spot price of the option, with specific rates to be announced closer to the release date;

- ANC: the governance token for Anchor Sail;

oppaMINT will significantly lower the barrier to entry for both past and present Terra Classic token holders, with those who burned more USTC receiving more allocated oppaMINT, and the tokens issued after launch can also be freely transferred, so they can be sold at any time if the user does not want them.

oppaMINT will also provide funding to VCs for project financing, as the Mint Cash system cannot mint new MINT or CASH tokens without explicit Bitcoin collateral.

ANC is similar to the previous ANC token, as stakers continuously receive buybacks funded by Anchor's yield, while also compensating borrowers. The difference is:

ANC will directly govern certain aspects of the native Mint Cash protocol, and MINT staking will always be subject to a fixed vesting period. While there are many more changes to the ANC token economics than described, more details will be announced closer to the release date.

Conclusion

We have covered a lot of details in this article. In summary, we are very serious about building this right and are committed to realizing the untapped potential of the original Terra protocol—including its diverse stablecoin system, the liquidity market related to Bitcoin, and all protocols accepting the CashUSD stablecoin, including Anchor Sail itself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。