Author: Liu Ye Jinghong, Wiseman Notes

What is Mobile Money

Mobile money is not the same as mobile payment. According to the definition of the African Development Bank, mobile money, unlike money held in traditional bank accounts, refers to money stored on a user's SIM card, with the SIM card replacing the bank account as the user's identification code.

Therefore, mobile money is a financial services innovation that extends financial services to areas and populations not covered by traditional banks, leveraging information and communication technology and non-bank physical networks, and has two main features: customers complete deposits and withdrawals outside the banking system; and customers complete transactions through a mobile interface.

The operation of a mobile money account is somewhat similar to Venmo, but with one key difference: no need for a bank account. To deposit or withdraw cash from the application, the mobile money system uses human agents who carry cash and a phone to key locations nationwide, including remote rural areas. Mobile money can also be used for cashless transactions, including purchasing goods or paying bills.

Mobile Money Market

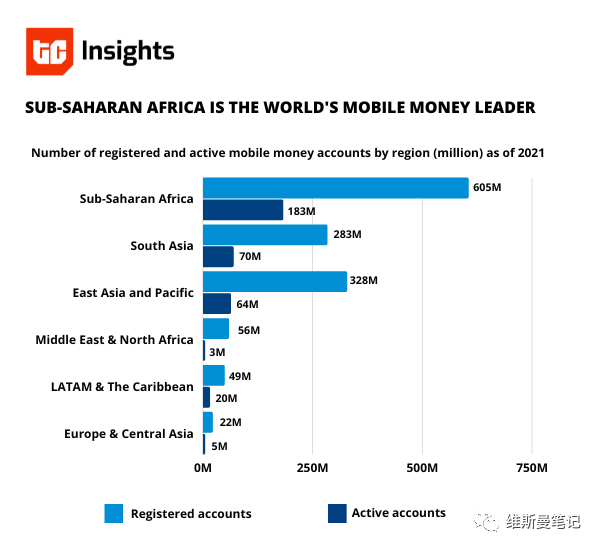

According to the 2021 report of the GSM Association (GSMA), $697.7 billion (a 40% increase year-on-year) was processed through mobile money options in sub-Saharan Africa. This region also accounted for nearly 70% of the global transaction volume last year ($1 trillion), far exceeding South Asia ($156.3 billion).

Additional information in the GSMA report indicates that there are already over 184 million active mobile money wallets in Africa, compared to just 161 million accounts a year and a half ago. It is believed that the latest data in 2023 will show even greater growth trends.

Why is There a Demand for Mobile Money

For most people, modern mobile payments, electronic money, and even cryptocurrencies are quite popular, so why is there still a demand for mobile money? There are three main reasons:

1. Low Financial Inclusion in Remote and Underdeveloped Areas

Globally, there are still large remote and underdeveloped areas, with typical examples being African countries, where the financial needs of the population cannot be met. According to the World Bank's 2023 report, only 28% of the population in African countries use the internet, meaning that over 70% of people cannot access modern, convenient financial services.

Citing data from The Global Findex Database 2021, the global ownership rate of individual accounts is 76%, meaning that 24% of the global population still does not have personal accounts.

2. High Operating Costs of Traditional Bank Branches and ATMs

The operating costs of promoting traditional bank branches in sparsely populated remote areas and economically underdeveloped areas are high, with low profitability. Using an ATM requires opening a personal account and a bank card at a branch, turning this issue into a "chicken and egg" problem. Therefore, mobile money can expand the range and scope of financial services with minimal infrastructure investment, making it more inclusive.

3. High Threshold for Mobile Banking and Third-Party Payment

Existing mobile banking or third-party payment service providers require users to have a personal account and associated bank card for operation. For economically underdeveloped areas, there may not be traditional bank branches to handle such services.

Based on the above three points, it is clear why seemingly outdated mobile money technology is still widely used. Mobile money is almost the only inclusive financial service available in underdeveloped and remote areas.

MTN MobileMoney Case Study

Before introducing Web3, I need to briefly introduce the existing mobile money operating model.

MTN is the largest telecommunications operator in Africa, with operations in 22 countries in Africa and the Middle East, serving 219 million users. The mobile money service launched by MTN is called MTN MobileMoney, which is the most widely used mobile money in Africa and has been extended to East and West African countries such as Uganda, Cameroon, Ghana, Ivory Coast, Rwanda, Benin, Nigeria, and Zambia.

Users can register as registered users through their mobile numbers and receive a mobile money account based on the telecommunications operator. They can increase the balance of their mobile money account by depositing cash at authorized agent locations. Users can use their mobile phones to complete remittance operations, and the recipient will receive a withdrawal SMS from MTN. After verifying the account at the agent location, they can withdraw cash. Users can also store cash in their accounts and use mobile money to pay bills and purchase goods at MTN's partner institutions.

In terms of business profitability, MTN mainly relies on remittance service fees. In the case of both parties being MTN mobile money users, the maximum fee for remittance services is only $1. The affiliated agent locations do not have the right to charge various fees and can only earn commissions provided by MTN after users deposit or withdraw cash.

In terms of the business model, MTN's entire operating network is divided into three roles: custodian banks, super agents, and retail agents. Custodian banks are responsible for safeguarding MTN customer funds, super agents provide mobile money and cash management and allocation to retail agents on behalf of financial institutions or partners, and retail agents directly assist users in using MTN mobile money and conducting deposit and withdrawal transactions.

Shortcomings of MTN MobileMoney

Although mobile money fills the gap in inclusive financial services in underdeveloped areas, there is still a lot of room for improvement. The current shortcomings include three main points.

1. Complex Processes Highly Dependent on Agents. Whether it's account registration or remittance and deposit/withdrawal, it all needs to be done at retail agent locations. However, retail agents are not as widely available as convenience stores like 7-Eleven. Without coverage from retail agents and partner institutions, it is almost impossible to complete the service.

2. High Maintenance Costs. MTN currently maintains over 20,000 retail agent locations, and there are many environments that rely on manual processing. The high operating costs of the extensive agent network are also a drawback in economically underdeveloped areas.

3. Only Supports Local Currency. Currently, MTN only supports local currency services and a very small number of insurance-related financial services. It is not comprehensive enough for broader inclusive financial services. This includes not providing savings services such as current and fixed-term deposits, as well as more advanced financial products.

Integration of Mobile Money with Web3

So, what can the integration of mobile money with Web3 bring? There are still three main advantages.

1. Permissionless Inclusive Financial Network. Web3 does not require account opening or various proofs. Users can directly obtain a decentralized account by binding their SIM card with a Web3 wallet address. They can also directly connect to the open financial world of Web3 and access inclusive financial services through protocols like MakerDAO. There is no need for centralized custodial institutions to safeguard funds, as high-trust financial services can be achieved through open protocols.

2. Extremely Low-Cost Decentralized Ledger. Unlike the high operating costs of MTN's over 20,000 retail agent locations, the integration of mobile money with Web3 allows for direct decentralized financial services through blockchain, all completed via the internet. Through technologies like Layer2, the fee rate can be compressed to well below $1.

3. Open Financial Network for Cross-Currency Transactions. Under the current mobile money system, supporting only local currency payments is not enough to achieve inclusive finance. Economic underdevelopment and even regional financial crises (such as the bankruptcy of Greece) make holding local currency a disaster for people with low incomes. By introducing Web3 into mobile money, people can use compliant USD digital currencies like USDC to avoid local currency depreciation. They can also purchase compliant assets like RWA to safeguard and increase their wealth.

The open finance brought by Web3 offers a borderless and more diverse inclusive financial solution, but it also faces a series of issues such as fraud, rug, and hackers. The dark forest of Web3 requires promoters to conduct some centralized review and screening. I never believe that what Web3 needs is a completely unregulated, completely decentralized utopian world. Therefore, introducing appropriate regulatory and financial institutions to assist the open Web3 network may be the future of Web3. This is my understanding of the open Web3 network, balanced.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。