Author: flowie, ChainCatcher

The RWA coverage has always been extensive, encompassing different asset classes such as stablecoins, bonds, stocks, real estate, and how they integrate with the blockchain. Previously, we briefly summarized the seven major subfields and representative vertical players in the RWA track through the RWA series article "RWA Chart: An Overview of the Progress of the Top 10 Head Projects and Summaries of 20 Early Projects".

However, looking at the overall trend in the RWA track this year, it is mainly driven by US bonds. The projects with high TVL in the RWA field are mainly US bond projects, and the increased deployment of RWA by DeFi protocols such as COMP and MKR is mainly centered around US bonds. The introduction of US bonds to the blockchain is currently the most typical case in RWA.

As for why US bonds have become the cornerstone of this round of RWA narrative, as we have repeatedly mentioned in previous articles, a most direct logic is that with the continuous interest rate hikes by the Federal Reserve, the rise in US bond interest rates has prompted many DeFi protocols or crypto investors to turn to obtaining risk-free high-yield returns from US bonds.

But apart from the very clear demand for returns, one rarely mentioned real pain point is that the barrier to entry for US bond investment has always been high. Even for US citizens, the cumbersome KYC and account opening processes have kept most people out, let alone non-US citizens. At this point, how to integrate US bonds from off-chain to on-chain in a compliant manner, reduce the investment threshold for US bonds, and bring the returns of US bonds to on-chain users is a practical problem faced by many projects that has real value but is also full of obstacles.

Bringing US bonds onto the blockchain is no easy task. As Kyle Samani, co-founder of Multicoin Capital, said, "This is a standard problem. You need to get all relevant parties, such as issuers, underwriters, fund managers, auditors, buyers, sellers, brokers, banks, etc., to agree on new standards."

Not only the tokenization of US bonds, but also the tokenization of other assets such as the bond market, stocks, real estate, etc., to bring traditional real-world off-chain assets onto the blockchain, also involves the participation of many intermediary parties such as government regulators and management institutions. The compliance issues and legal risks involved are quite complex.

Perhaps we can start by understanding the process and real obstacles of implementing RWA and how players in this track innovate in reducing user entry barriers and increasing liquidity, focusing on the most representative and relatively easy-to-standardize aspect of bringing US bonds onto the chain.

Different players, how to bring US bond returns onto the blockchain?

The seemingly emerging trend of bringing US bonds onto the blockchain has been brewing for a long time. In addition to tokenized US bond funds from asset management companies, new players in the on-chain US bond protocol are committed to tokenizing US bond returns, and stablecoin protocols indirectly bring US bond returns to crypto users through asset reserves. According to RWA data research platform rwa . xyz, the tokenized US bond market alone has exceeded $680 million (excluding indirect introduction methods), with an average on-chain US bond yield of over 4%.

1. Asset management companies that have been early adopters: Arca, Franklin Templeton, WisdomTree

Asset management companies with a leaning towards traditional finance may be among the first players to target the tokenization of US bonds. In 2020, digital asset management company Arca's innovation department, Arca Labs, finally registered a fund for investing in US government bonds with the US SEC after more than two years and nine submissions. This fund, also known as a BTF (Blockchain Transfer Fund), is regulated by the US Investment Company Act of 1940.

Arca Labs can convert the shares of the US government bond fund into tokens called ArCoin, which are recorded and stored on the Ethereum blockchain. Purchasing ArCoin is equivalent to subscribing to Arca Labs' US government bond fund. The pricing of ArCoin is based on the net asset value of the fund.

The ultimate ownership of ArCoin is maintained by a transfer agent regulated by the SEC and operated by Securitize, a blockchain company focused on tokenizing real-world assets. Currently, investors (both US and non-US) who have joined Securitize's KYC/AML process or have a Securitize ID can purchase ArCoin, and Arca only accepts subscriptions in US dollars.

Franklin Templeton, the largest publicly traded fund management company with assets over a trillion dollars, also launched the government money market fund FOBXX on the Stellar blockchain in April 2021. FOBXX is the first US registered mutual fund to process transactions and record share ownership on a public blockchain, regulated by the US Investment Company Act of 1940. From its registration, management, and disclosure, Franklin Templeton offers one of the most rigorously regulated products. FOBXX is currently the largest player in the tokenized US bond market.

The transfer agent for FOBXX will maintain official records in ledger form, with the blockchain serving as a secondary record. In April of this year, FOBXX also expanded to Polygon.

According to the FOBXX website, at least 99.5% of the fund's total assets are invested in securities fully backed by the US government, cash, and repurchase agreements or cash. Each share of the FOBXX fund is represented by a "BENJI" token, with the BENJI token price pegged at $1. FOBXX distributes the returns of US government bonds to BENJI holders, who are shareholders of the FOBXX fund, through its developed application, the Benji Investments app.

BENJI's target market is US investors, both retail and institutional investors can participate. Investors must have an exclusive on-chain wallet for transactions (created by the fund's transfer agent during account opening) and complete purchases and other transactions through the Benji Investments app. Investors cannot currently use stablecoins to purchase BENJI, and the BENJI tokens purchased by users are only used as proof of receiving US bond returns, with little leverage utility.

FOBXX's total asset size has now reached nearly $300 million, with the Stellar Foundation injecting $20 million, and FOBXX's annualized rate of return in the past year is 3.75%.

One of the major ETF providers in the US, Wisdom Tree, also has a deep layout in the tokenization of US bonds. In January 2022, Wisdom Tree announced the launch of a new fintech product directly targeting US investors, called "Wisdom Tree Prime," which aims to provide selected investment opportunities from government debt to cross-asset categories in token form on the blockchain.

In December, the SEC approved Wisdom Tree's 10 digital fund portfolios. Like Arca's products, these funds are products under the Investment Company Act of 1940, issued on the Stellar and Ethereum blockchains, with the transfer agent maintaining official records in ledger form, and the blockchain serving as a secondary record. Investors also need to conduct transactions through their launched Wisdom Tree Prime mobile app.

According to Wisdom Tree's website, the related US bond products of Wisdom Tree Prime include Short-Term Treasury Digital Fund (WTSYX), Floating Rate Treasury Digital Fund (FLTXX), 3-7 Year Treasury Digital Fund (WTTSX), 7-10 Year Treasury Digital Fund (WTSTX), Long-Term Treasury Digital Fund (WTLGX), and TIPS Digital Fund (TIPSX). The Short-Term Treasury Digital Fund (WTSYX) manages approximately $1 million in assets. However, this product is still in testing and has not been opened to a wider audience.

According to Wisdom Tree, the target users of Wisdom Tree Prime are not institutional crypto investors, but US retail investors. Currently, Stride and Galileo are their payment partners, and users can pre-fund their Prime accounts through ACH transfers and then store the returns at Daofu Bank. In addition, the Wisdom Tree Prime Visa debit card will initially be provided as a virtual card, and can be used for payments with Apple Pay, Google Pay, and Samsung, with a physical debit card to be released shortly.

Overall, these traditional finance-leaning asset management companies' approaches to tokenizing US bonds are almost identical, operating in the form of tokenized fund shares. The requirements for holding fund token shares and investing in the fund are the same. Holders of fund token shares need to register their addresses on the fund's whitelist, and addresses not on the whitelist will not execute transactions. Investors generally need to be US residents, and only fiat currency transactions are supported, not transactions with stablecoins or other cryptocurrencies. The blockchain mainly serves as a secondary record, with the official records of the fund's transfer agent still managed in ledger form.

In other words, although these asset management companies' exploration of tokenizing US bonds is relatively strict in compliance, it simply applies blockchain technology for ledger purposes, and has little connection and liquidity with the crypto world of DeFi.

It is worth mentioning that Robert Leshner, the founder of Compound, announced the establishment of a new company, Superstate, on June 29, which, according to its submitted application, almost plans to operate in the form of tokenizing fund shares similar to the traditional financial institutions mentioned above. However, Robert Leshner has a background related to the US Department of the Treasury, and whether this operating method will bring new gameplay remains to be seen.

2. Stablecoin players who go with the flow: MakerDAO, Frax Finance

Compared to the above asset management companies, stablecoin protocols such as Maker indirectly obtain US bond returns by using treasury assets to allocate US bonds.

Recently, MakerDAO, which has been widely discussed for its layout in RWA, has been increasing its investment in US bond assets this year. As one of the earliest DeFi protocols to lay out RWA, MakerDAO did not initially invest directly in US bonds. It initially explored investments in solar energy, real estate, and other RWA asset allocations, but ultimately, these assets had too many default risks and did not progress much.

For MakerDAO, diversified asset allocation not only considers substantial growth in returns but also reduces reliance on a single asset, reducing many single-point risks. Previously, nearly half of MakerDAO's reserves came from stablecoins in the Primary Stablecoin Module (PSM), with nearly 70% of them being USDC. This means that MakerDAO had to bear the risk of USDC becoming unpegged even without returns.

In contrast, US bonds are almost risk-free interest rate products, and due to the continuous rise in US bond interest rates under the interest rate hikes, MakerDAO's layout in US bonds is almost a natural fit. According to official data, as of May, MakerDAO's total RWA investment portfolio reached 2.34 billion DAI, mainly used to purchase US government bonds. According to the dune panel, over half of MakerDAO's income comes from interest-bearing RWA assets.

With substantial income growth, MakerDAO has also raised DAI deposit rates several times this year, first from 1% to 3.49%, and most recently directly to 8%, exceeding the risk-free rate of 5% for its underlying asset, the US dollar. The purpose is to expand the usage of DAI and DSR. Recommended reading: "How Did DAI's 8% Excess 'Risk-Free Rate' Come About?"

It is worth mentioning that MakerDAO's method of allocating US bond assets does not use an asset issuance platform but holds US bond assets through a trust legal structure. According to MIP65 proposal, MakerDAO has entrusted Monetalis to design the overall legal framework, and Monetalis is using a trust legal framework based in the British Virgin Islands (BVI) to achieve on-chain and off-chain integration.

Through this trust structure, MakerDAO is able to convert reserve assets into fiat currency, then purchase US bond ETFs through a custodial bank to obtain corresponding returns, and then distribute protocol income to DAI holders by raising the DAI deposit rate.

In addition to MakerDAO, the algorithmic stablecoin protocol Frax Finance has also been exploring the use of US bond and other RWA assets. Frax Finance and MakerDAO previously faced similar dilemmas, namely, over-reliance on USDC as collateral. Earlier this year, USDC becoming unpegged led to both DAI and Frax falling below $0.90, further pressuring Frax Finance to strengthen reserves and reduce reliance on USDC.

At the beginning of this year, Frax Finance revealed in a media interview that its 2023 plan includes establishing a Federal Reserve Master Account (FMA) to directly hold US short-term bonds. However, this plan was seen as almost a "pipe dream" by many crypto KOLs, and Frax Finance has not disclosed any subsequent progress on this.

In the upcoming Frax V3 version, some progress on US bond and other RWA asset reserves has been revealed. In July, Sam Kazemian, the founder of Frax Finance, mentioned in an interaction with the community that the assumption behind FRAX's operation since its inception was that it would operate under the assumption that USDC would not become unpegged. However, when USDC becomes unpegged, the redemption value of 0.95 USDC + 0.05 USD FXS is less than $1.00. Therefore, FRAX v3 will change this situation through many new AMOs and features tied to the "sovereign dollar."

On August 7, the founder of Frax Finance proposed to "use FinresPBC as the off-chain RWA partner of FRAX v3." FinresPBC is a stablecoin technology service provider, and the proposal mentioned that FinresPBC will provide services to the Frax protocol, including holding US dollar deposits, issuing and redeeming Paxos USDP and Circle USDC stablecoins, and holding, purchasing, and selling US government bonds. Each month, FinresPBC will publicly release a complete list of all reserves held for the Frax protocol.

However, regarding the method of using trust law to introduce US bond returns, Kenji, a crypto KOL, believes that there are still risks such as asset default, agent risk, and regulatory risk. In particular, the Corporate Transparency Act of 2024 in the US will require even DAOs to disclose the actual controllers and influential stakeholders, which conflicts with MakerDAO's existing RWA framework.

In "RWA Discussion: Compliance, Subdivision Tracks, and Prospects", the founder of dForce, Mindao, stated that if MakerDAO sets up its own trust to hold US bond assets, it will at least have fewer operational risks than using indirect methods like Circle. More importantly, this model will affect the entire stablecoin market, and decentralized stablecoins may have the opportunity to overtake in the curve. Because decentralized stablecoins with US bond interest have greater appeal than centralized stablecoins. It can adjust the risk composition of underlying assets more flexibly in terms of both returns and programmability.

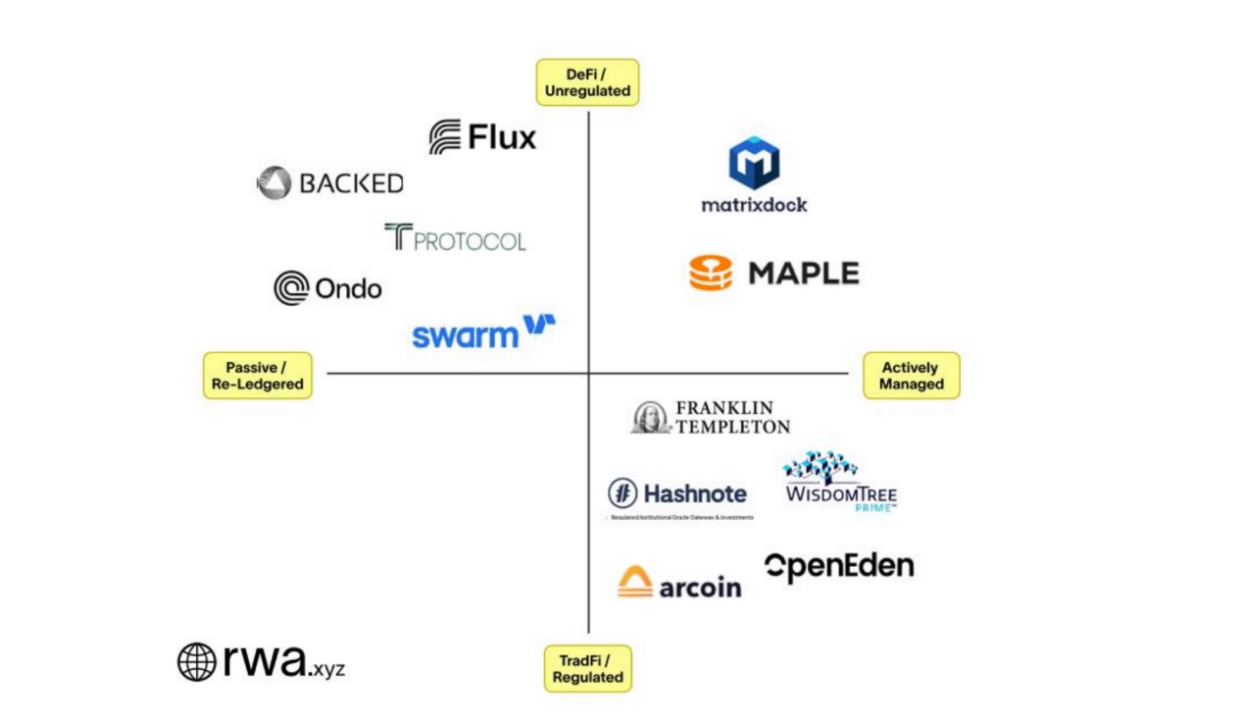

3. Crypto newcomers seeking to lower investment thresholds: Ondo Finance / Flux Finance, Matrixdock / T Protocol

Whether it is traditional financial asset management companies tokenizing US bonds or stablecoin protocols indirectly providing returns to their stablecoin users through a trust, the tokenization of US bonds does not have market circulation and is basically a purely off-chain model. The limitations of this model are also very obvious. The tokenization of US bonds by traditional asset management and crypto asset management companies mainly targets non-crypto investors in the US, requires strict KYC, and generally requires the use of a dedicated app, and does not support cryptocurrency subscriptions. The investment threshold is still relatively high. And stablecoin protocols only limit income to their stablecoin holders.

For crypto users, there is still the pain point of how to invest more idle crypto assets in US bonds with a low threshold. For DeFi projects, they need to consider how to distribute US bond returns in a compliant and low-threshold manner through tokenization to crypto users.

The latest tokenization of US bonds research report from the RWA research platform rwa . xyz lists DeFi protocols such as Ondo Finance / Flux Finance, Matrixdock / T Protocol, Maple, Backed, Swarm, and others in the exploration of US bond tokenization. However, due to compliance requirements, most US bond tokenization protocols require KYC, and regional restrictions are also very obvious, which also means that they face the problem of limited issuance scale.

Compared to the tokenization of US bonds by traditional asset management companies, their compliance methods for introducing US bonds to the blockchain are different. In addition, they support the use of stablecoins, which is relatively more convenient in operation. The following briefly analyzes some US bond tokenization protocols with relatively high TVL and exploration in bypassing KYC.

Ondo Finance, founded in 2021, has team members with rich backgrounds from institutions such as Goldman Sachs, Fortress, Bridgewater, and MakerDAO. Earlier this year, Ondo Finance announced the launch of tokenized funds, providing institutional investors with the opportunity to invest in US government bonds and institutional-grade bonds.

Compared to the cumbersome registration process of mutual funds, Ondo Finance chose to use a fund exemption issuance method, but this means higher requirements for investors, who need to meet the SEC's definition of accredited investors and qualified buyers, i.e., individuals or entities investing at least $5 million. Accredited investors can invest using USDC or dollars, with USDC being converted to dollars through Coinbase and then purchasing US bond ETFs through Clear Street, a bulk brokerage platform for institutional investors. The resulting income is distributed to institutional investors in tokenized form.

This investment threshold is still very high, but the lending protocol Flux Finance launched by Ondo Finance allows ordinary investors to indirectly obtain US bond income. Flux Finance allows OUSG holders to pledge OUSG to borrow stablecoins. As a stablecoin provider in the Flux Finance lending pool, there is no need for KYC to indirectly obtain US bond investment income. Currently, Flux Finance has a total supply of nearly $40 million.

In contrast to the fund exemption issuance method, the on-chain bond platform Matricport launched by Matrixport has chosen to establish a Special Purpose Vehicle (SPV) as the issuer to purchase and hold US government bonds. Matricport has launched a product based on US government bonds called Short-term Treasury Bill Token (STBT). According to compliance regulations, it still requires customers to undergo KYC and register their addresses on a whitelist, with a minimum investment requirement of $10 USD, and does not provide services to customers in mainland China, Singapore, the US, Canada, and other regions.

Similar to OUSG, STBT allows users to invest using stablecoins. STBT, through its issuer, converts stablecoins into fiat currency for a "third-party custodian" to purchase underlying government bonds. However, it currently does not disclose a "third-party custodian" like Ondo Finance.

It is worth mentioning that in the exploration of lowering investment thresholds, Matrixport has launched the permissionless US bond investment protocol T Protocol. Compared to Ondo Finance indirectly introducing permissionless US bond returns to crypto users through the lending protocol Flux Finance, T Protocol achieves permissionless US bond investment by wrapping the STBT issued by MatrixDock.

According to HashKey's report "HashKey: Tokenizing RWA with US Treasuries as an Example", the TBT token launched by T Protocol is a wrapped version of STBT. Investors deposit stablecoins into T Protocol, and T Protocol mints TBT. When it accumulates to 100,000 USDC, it entrusts a partner to purchase STBT. TBT is pegged to 1 USD and can be redeemed through the protocol, distributing US bond returns through a rebase mechanism. There is also another type of wTBT, which is a non-rebase wrapped version of TBT. HashKey believes that behind TBT is the protocol's purchase of STBT and the USDC reserves that have not yet been used to purchase STBT, making T Protocol an intermediary between non-Matrixdock users and Matrixdock. TBT is also a potential competitor to stablecoins.

Conclusion: What are the noteworthy impacts of US bond RWA on DeFi?

Combining the relevant protocols introducing US bond returns to the blockchain and some analysis in Mint Ventures' podcast review article "RWA Discussion: Compliance, Subdivision Tracks, and Prospects", there are two main impacts of US bond RWA on the crypto market worth noting:

First, retaining crypto funds on-chain to slow down capital outflows. After experiencing a long bear market, it has been difficult to find low-risk and profitable avenues for idle stablecoins and other crypto assets. US bond RWA to some extent fills this demand for risk-free returns, slowing down capital outflows on-chain. From a longer-term perspective, Mindao, the founder of dForce, raised a thought: stablecoins have tokenized the US dollar, but the native interest of the US dollar has not been tokenized until now. A currency cannot be a true currency without its own interest. When these two are combined, it means that we have truly tokenized the currency of the US dollar on-chain, which is significant.

Second, the impact on the stablecoin landscape. On the one hand, stablecoin protocols like MakerDAO have reduced their reliance on centralized stablecoins like USDC by allocating assets to US bonds, reducing operational risks, and attracting a large number of users to hold their stablecoins due to their yield. On the other hand, platforms like T Protocol and OpenEden issue stablecoins to help users gain exposure to yield-bearing US bonds, injecting new forces into the stablecoin market to some extent.

In addition, as US bond RWA explores compliance and technical integration between crypto finance and traditional finance, it may provide valuable insights for other RWA assets entering the crypto market.

References:

"An Allocator's Guide to Tokenized Treasuries"

"HashKey: Tokenizing RWA with US Treasuries as an Example"

"RWA Discussion: Compliance, Subdivision Tracks, and Prospects"

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。