Author:Long Yue

Morgan Stanley says that AI has not ended, but it's now the turn for hyperscale cloud providers to lead.

Michael Wilson, Chief U.S. Equity Strategist at Morgan Stanley, sent a clear signal to clients in the latest weekly report: reduce semiconductor holdings and turn to hyperscale cloud providers. This is not bearish on AI, but a rotation—three similar adjustments have already occurred during the AI investment cycle, and Wilson believes this is the fourth.

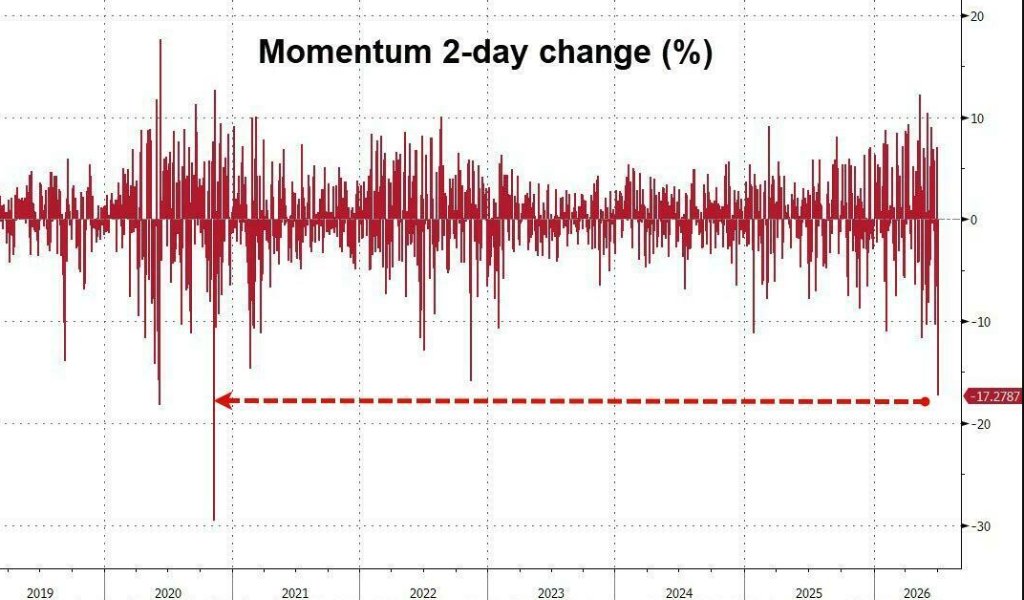

Chip stocks have cooled significantly after experiencing historic gains since the end of March. High beta momentum stock combination (i.e., storage and chip stocks) recorded the largest two-day drop since the onset of the COVID-19 pandemic. Wilson assesses that this pullback "may have further room to go."

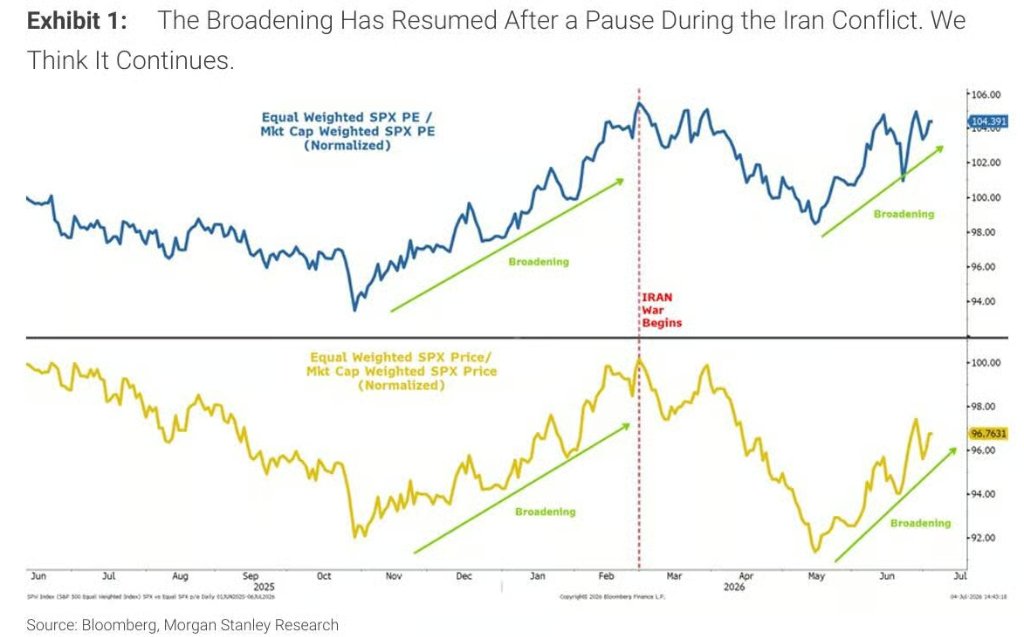

This assessment is not a spur of the moment—Wilson proposed the framework of “market broadening” trade in his annual outlook back in November 2025, with the core logic being: the U.S. economy will enter a new phase of expansion after completing a rolling recession by April 2025, and profit growth will exceed expectations, with market leading growth force expected to spread from AI capital expenditure beneficiaries to broader sectors.

This assessment was interrupted by the Iran war in February 2026. Rising oil prices and the market re-evaluating the Federal Reserve's interest rate hikes stalled the broadening trade, allowing semiconductor stocks to shine again with AI computing power narratives. Now, with oil prices retreating and inflation expectations stabilizing, Wilson believes the conditions are ripe again.

Similar to "Silver Topping": Storage Chips are the Biggest Risk Point

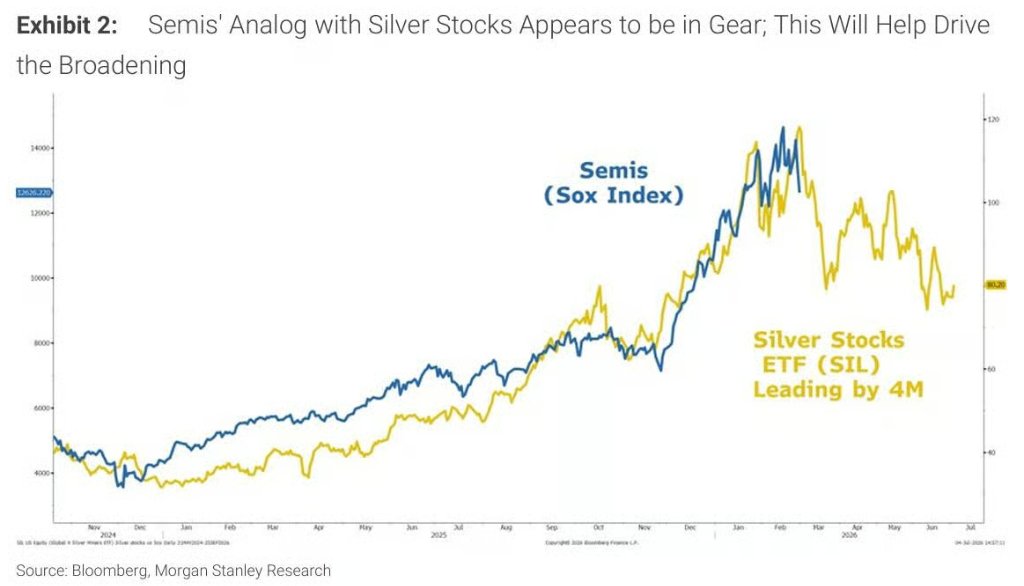

Wilson made a specific analogy in the report: the movement of semiconductors is highly similar to silver.

There are two reasons: first, both have experienced parabolic price rises; second, both are highly correlated with the commodity market, which has historically seen large fluctuations in prices.

J.P. Morgan first made this analogy in early June, which now seems to be coming true. He further pointed out that this round of adjustment will be led by the memory sub-sector—because memory is the category in the semiconductor complex that is "most like a commodity," with high price elasticity and rapid reversals.

After Micron's earnings report was released, semiconductor stocks saw a significant drop, and Wilson believes this confirms that the market has made "the peak rate of change in earnings expectations" a core focus.

Meta's Statement Ignited the Fuse

The direct catalyst for this rotation was an announcement from Meta.

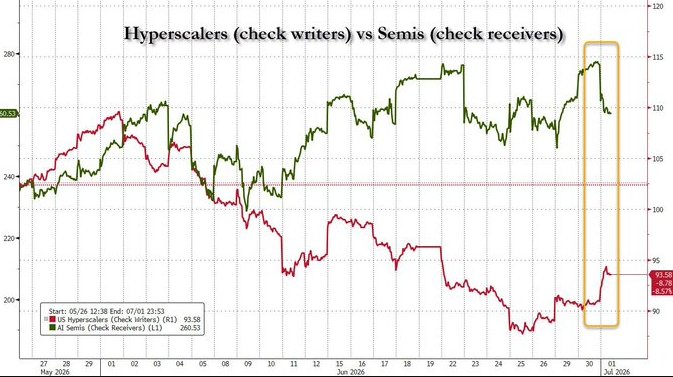

Last week, Meta announced that it would start selling its excess computing capacity to external customers. This move sent a signal to the market: the capital expenditure growth rate of hyperscale cloud providers might be reaching a turning point.

Wilson wrote in the report that the performance divergence between hyperscale cloud providers (i.e., Microsoft, Google, Amazon, Meta, etc.) and semiconductor stocks is fundamentally unsustainable—because the semiconductor manufacturers' demand fundamentally relies on the capital expenditure willingness of cloud providers. Historical patterns show that whenever the two diverge to extremes, "mean reversion" often occurs: cloud providers will either downgrade capital expenditure guidance or announce a change in direction, thereby triggering corrections in semiconductor stocks.

Meta has just provided such a reason.

It is important to note that Wilson explicitly stated this does not mean the AI capital expenditure cycle is over, but that there will be meaningful resets and rotations midway through the cycle. His exact words were: "This is a peak in the rate of change, not a peak in the overall capital expenditure cycle."

In fact, since the release of ChatGPT in November 2022, such phase corrections have already occurred three times, and this is the fourth.

Why Buy Cloud Now, Not Chips?

Wilson's logic is as follows: hyperscale cloud providers (like Amazon AWS, Microsoft Azure, Google Cloud, etc.) have lagged in stock performance in recent months, but the fundamentals remain strong.

He lists three reasons:

First, the core business is robust. Cloud providers have a strong business base that does not entirely rely on the AI capital expenditure narrative.

Second, they have a unique position in the AI application layer. Wilson believes cloud providers have a leading advantage in "developing and implementing the agentic application layer," and this value is underappreciated in the market.

Third, the potential for cost reductions is overlooked. Wilson refers to this as "an undervalued cost reduction lever."

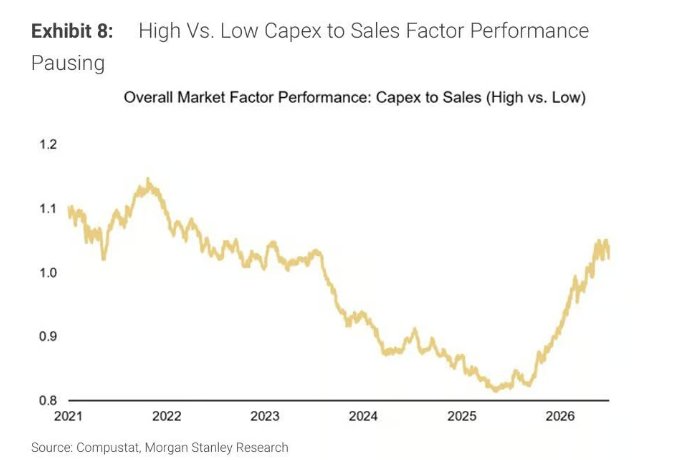

Meanwhile, the “high capex/sales factor” tracked by Morgan Stanley has shown topping signals after a strong performance over the past year. Cloud providers have already undergone a relative underperformance round, digesting this pressure; whereas chip stocks may just be starting.

“Broadening Trade” Restart: Not Just Buy Cloud

In addition to hyperscale cloud providers, Wilson also listed other preferred directions under the broadening trade:

Consumer discretionary is Wilson's most preferred direction. The logic is that consumer spending is shifting from services to goods, with improved pricing for goods, compounded by strong earnings revisions. He believes this is "the most convincing expression" of the broadening profit story.

Transportation also benefits from the arrival of the economic expansion cycle.

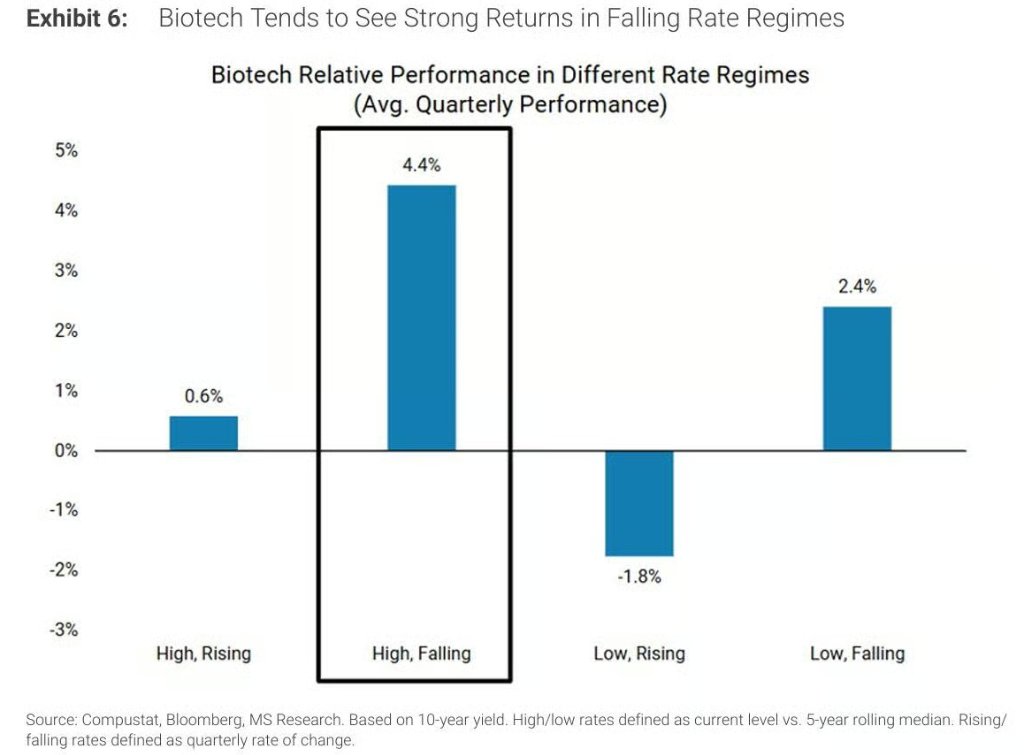

Biotechnology is representative of interest-rate-sensitive sectors. Historical data shows that under a high and declining interest rate environment, biotechnology has annualized returns close to 20%. J.P. Morgan expects core CPI to remain below 3%, with policy interest rate expectations still too hawkish; once corrected, biotechnology will directly benefit. Additionally, the ongoing warming merger cycle will provide extra catalysts for this sector.

Macroeconomic Background: Falling Oil Prices Stabilize Rates, Providing Soil for Rotation

Wilson's broadening logic also has an important macroeconomic support: the significant drop in oil prices.

Falling oil prices help stabilize bond rates, and stable rates are one of the key driving forces behind the broadening trade. J.P. Morgan's baseline forecast is: falling energy prices, peak inflation related to tariffs, and controllable service and housing inflation, together will lead the Federal Reserve to maintain rates this year, rather than raising them.

The current bond market still prices in 1.5 interest rate hikes before the first quarter of next year. Wilson believes that once this overly hawkish expectation is corrected, it will constitute a positive surprise for the stock market.

He also specifically mentioned that Federal Reserve Chair Waller stated at the Sintra conference that "inflation risks have subsided," reiterating the dual mandate of employment and prices. Coupled with last week's weaker-than-expected non-farm payroll data, Wilson believes this helps further lower hawkish rate expectations, providing support for the broadening trade.

This is Rotation, Not an End

Wilson clearly summarized at the end of the report:

“The market will begin to broaden, and the indices are entering a consolidation/correction phase, which is happening." "Among AI winners, leading sectors have rotated for many years. This is merely the next rotational development in the cycle." "This is just the next rotation—from semiconductors to hyperscale cloud providers, along with the aforementioned other broadening trade targets.”

The relative underperformance of semiconductor stocks following Micron's earnings report has made the market realize that "the peak rate of change" has become a core concern of the market. Meta's announcement about selling excess computing capacity solidified this expectation. The consolidation of the high capex/sales factor could further prompt other cloud providers to lower their capital expenditure guidance expectations.

All of this is fueling the broadening trade.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。