Written by: Rita

Trend Guide

Morgan Stanley points out that GOOGL and META are severely undervalued. Nominal valuations may seem expensive, but after adjusting for stock-based compensation (SBC) accounting treatment, the real valuation is actually underestimated by more than 30%, far below historical levels. In the short term, AI funds are on the sidelines, but long-term opportunities are evident.

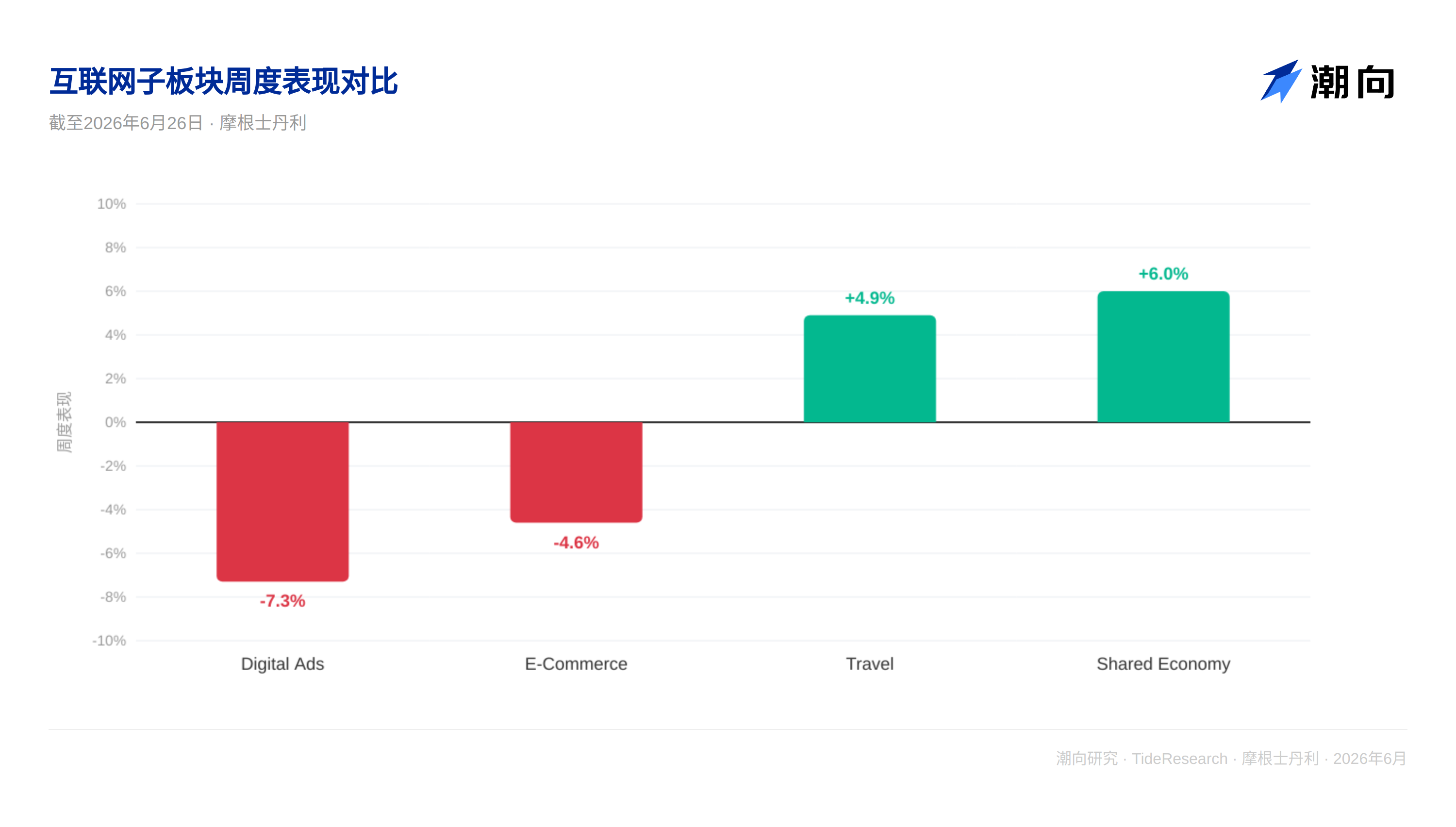

Internet stocks have recently weakened. As of June 26, the internet index has fallen by 6%, with Google and Meta both down over 4% and Snap down 5.4%. Meanwhile, travel and sharing economy stocks have increased by 4.9% and 6.0%, respectively. The issue reflected behind this divergence is straightforward: where should the funds in the AI era flow?

Morgan Stanley's assessment is that internet giants have not yet sufficiently proven their profitability in the AI era, so the market is temporarily investing in safer travel and sharing economy companies. However, this judgment may be overly pessimistic.

Two Worlds of Valuation

Internet companies face a statistical trap. Looking at nominal EV/EBITDA, AMZN is 11.0 times, GOOGL is 16.1 times, and META is 8.9 times, which doesn't seem high. But the problem is that the EBITDA calculation for these companies implicitly assumes that the stock component of employee compensation should be counted as a cost.

If this assumption holds, the earnings of these companies are severely underestimated. Morgan Stanley’s analysis shows that once adjusted for accounting treatment, treating SBC as a cash cost rather than a paper cost, these companies’ EV/EBITDA multiples would rise significantly. For example, the adjusted median multiple for digital media companies jumps from 16.3 times to 31.1 times, an increase of 91%. Yet even then, these multiples remain below the five-year average of 31.6 times.

In other words, the true valuation of internet giants is underestimated by more than 30% by the market.

AI Monetization is Still Awaiting

Morgan Stanley has tracked several key indicators. In a data table, the expected EPS growth rates for digital advertising companies (GOOGL, META, SNAP, etc.) for 2026 are -22%, -11%, and -20%, all negative. This indicates that the market lacks confidence in these companies' earnings growth this year. The reason is clear: massive AI infrastructure spending has raised IT costs, and internet advertisers are still observing return on investment, showing no signs of significantly increasing spending for now.

However, this observation period may not last long. Once the monetization path for AI models becomes clear, such as new advertising formats brought by generative AI, funds will flow in rapidly. The high leverage characteristic of digital advertising companies means that once earnings growth turns positive, the stock price reaction will be very intense. Morgan Stanley provides a positive EPS growth expectation for 2027, indicating that analysts believe this turning point will come.

Weak in the Short Term, Opportunities in the Long Term

Report data shows that the internet index has fallen by 5.5% in the past week, 10.3% over the month, 14.2% over three months, yet is up 14.2% year-to-date. This indicates that the recent sell-off is a short-term technical adjustment, not a trend reversal. In the long run, AI funds will ultimately flow to companies that can truly monetize AI capabilities, and internet giants are core members of this list.

There are three key catalysts: the launch of AI advertising products and ROI validation; changes in interest rate expectations, as internet companies are very sensitive to interest rates due to their high discount rate requirements; and the repricing of valuation centers. Once the market accepts the framework of "adjusted valuations post-SBC," there will be significant upside for internet stocks.

Trend Perspective

The smartest aspect of Morgan Stanley's report is that it pierces a market illusion by using the SBC adjustment perspective. Internet companies are mispriced by the market, not worthless. This kind of contrarian thinking is often seen in bottom areas; when the pessimistic pricing of the market itself contains opportunities, it is often the best entry point.

It should be noted that Morgan Stanley's analysis assumes that SBC should be considered real cash cost. This assumption is controversial in both academia and practice. Some believe that the real cost of stock compensation should be calculated based on market value at the time of exercise, rather than a fixed value at the time of grant. This technical detail is important because it directly affects the multiple. But even conservatively, considering the midpoint value between before and after adjustment, the valuation discount of internet stocks remains very evident.

The flow of AI funds ultimately depends on monetization, not the technology itself. Internet companies have accumulated years of AI applications in advertising, recommendations, search, etc., rather than starting from scratch. Compared to chip manufacturers still struggling with production capacity, the issue for internet companies is merely conversion rate, that is, how to turn AI capabilities into products that users are willing to pay for. Once this conversion begins to accelerate, the revaluation will happen swiftly.

Disclaimer

This article is a整理与解读 of third-party brokerage research reports by Trend Research. The ratings, target prices, profit forecasts, and related judgments quoted in the text are solely the opinions of the analysts from that brokerage and represent the position of their institutions, not the views of Trend Research, and do not constitute any investment advice.

The market has risks, and decisions should be independent. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。