The World Cup is about to kick off. On the day of the opening match, two events will occur almost simultaneously.

One is money. As of the day before the match, the total transaction volume of the "World Cup champion" contracts from Kalshi and Polymarket has exceeded $2 billion—without a single match being played [1]. The other is recognition. Two days before the opening, the crypto exchange Kraken was announced by FIFA as the official crypto exchange sponsor of the World Cup (Supporter level, covering North America and Europe; financial terms undisclosed) [5][6][7].

However, what this article truly seeks to ask is a more fundamental question that sports media typically won't address: When the World Cup actually kicks off, how do these on-chain contracts "know" who won? How does the price fluctuate with the match, how are contracts handled when a team is eliminated, who decides the outcome, and how much of the over $2 billion wagered is real—this marks the first day that the prediction market transitions from "pre-match static numbers" to "event operation."

Following the previous issue (a static data panorama on the eve of the opening match), this installment discusses: how this machine truly gets operational at kickoff.

Data is accurate as of June 11, 2026. All prices and transaction volumes are subject to change, and the publication timing may differ. This article does not predict any match results.

Act One · How $2B Accumulated—And "Which $2B"

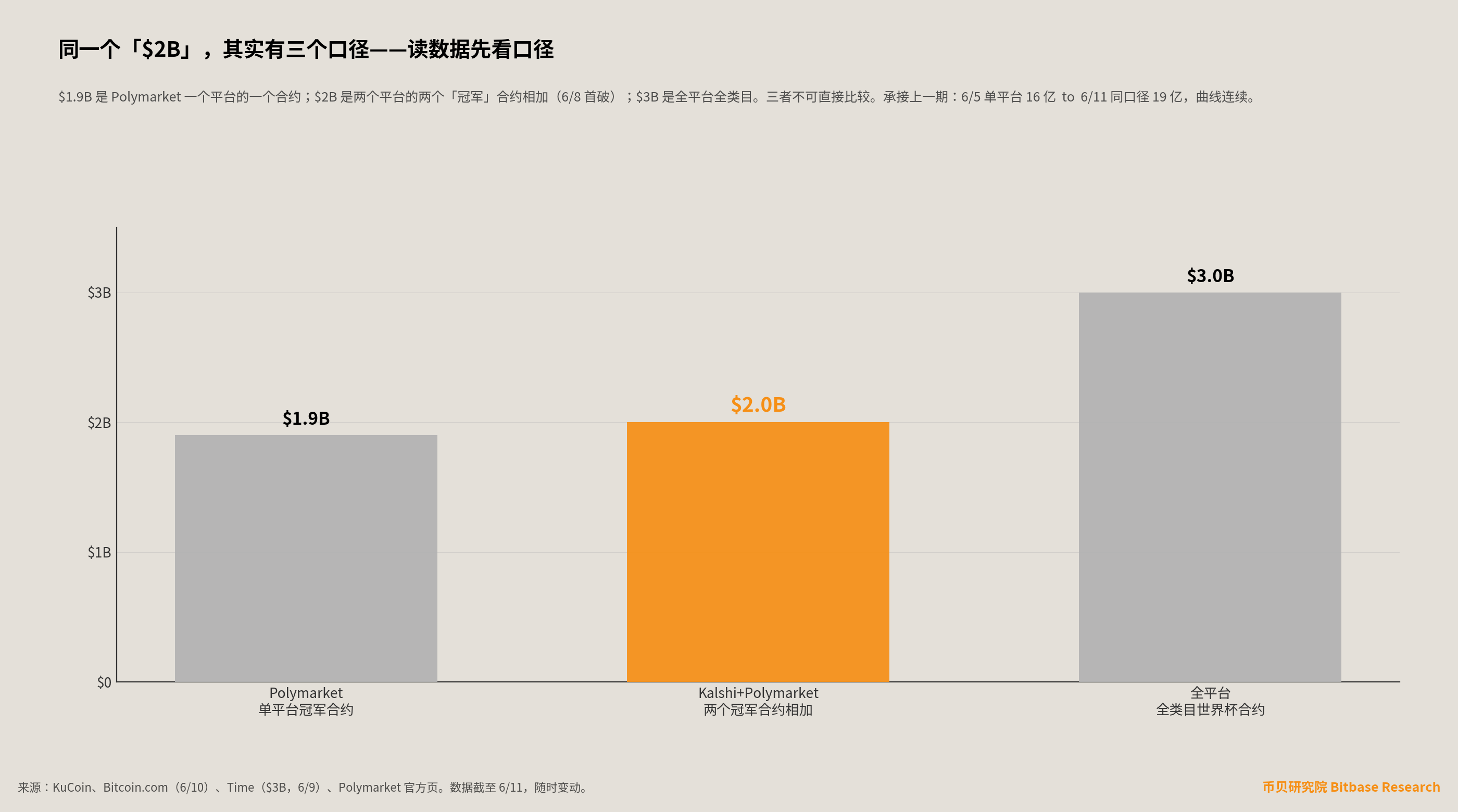

Let's break down that standout figure.

Before the opening match, Polymarket's single platform "World Cup champion" contract has accumulated a transaction volume of about $1.9 billion (since it opened on July 2, 2025) [4]; the Kalshi contract contributed around $132 million; together, they first surpassed $2 billion on June 8 (two days before the match) [1]. If we broaden our view to include all platforms and all World Cup-related contracts (not just "champion"), the entire sector's transaction volume has exceeded $3 billion [3].

Connecting back to the previous issue: we recorded that Polymarket's single platform had $1.6 billion on June 5. Six days later, the same measure had reached $1.9 billion. The curve is continuous when measured by the same standards.

Looking at the entire field, data from the Pew Research Center shows: the combined monthly transaction volume of Kalshi and Polymarket surged from less than $5 billion in September 2025 to about $24 billion in April 2026; by comparison, the average monthly betting volume for legal sports betting in the U.S. last year was about $14 billion. The size of the prediction market has already surpassed traditional sports betting [3].

As for how the market views the championship as of June 10, Spain is priced at approximately 16.5% on Polymarket and about 17.4% on Kalshi, France closely follows at around 16%, England and Portugal each at about 11%, defending champion Argentina at around 9%, and Brazil at about 8% [1]. These are just the market's current pricing, not predictions, and not judgments from this article.

Act Two · Individual Match Contracts: How This Machine Operates After Kickoff

$2 billion is the long-term contract for "who will win the championship." However, what truly comes to life after the match starts are the individual contracts covering each game.

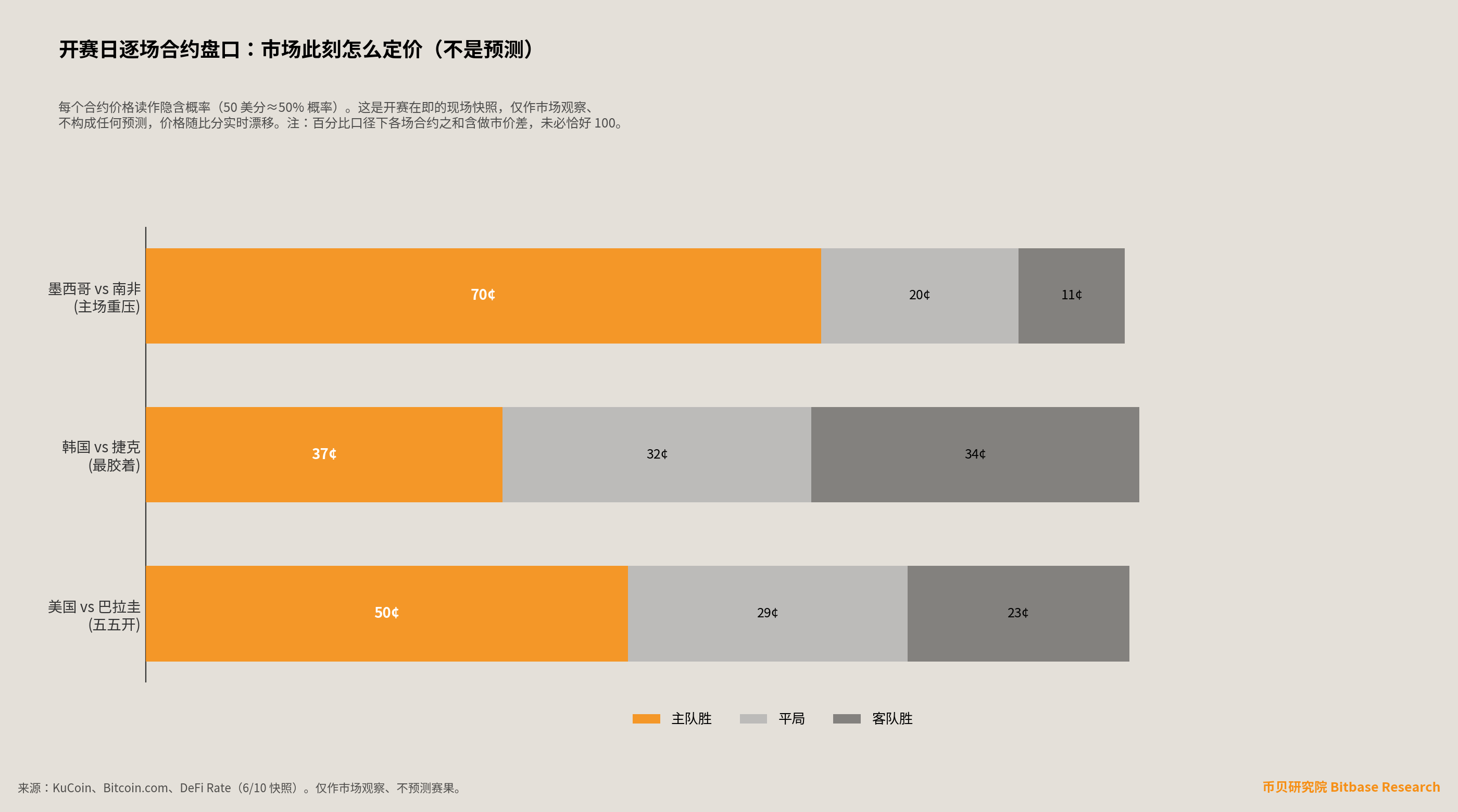

The odds for the opening day have already been posted (the following reflects the market's current pricing and serves as a snapshot, not a prediction): in the win-draw-loss contracts for the first match, the home team Mexico is priced as the heaviest favorite for that game; the other game on the same day, South Korea vs. Czech Republic, is perceived by the market as the most contested of the four opening matches, with South Korea at approximately 37 cents, Czech Republic about 34 cents, and a draw around 32 cents, almost evenly split; while the USA vs. Paraguay is viewed as a "50-50" situation—USA at around 50 cents, Paraguay around 23 cents, and a draw around 29 cents. The "total goals" contracts for the four opening matches are skewed toward lower scores, with the implied probability of "under 2.5 goals" ranging from 57% to 59% [2][8].

The operational logic of each contract is the same: prices fluctuate between 1 cent and 99 cents, directly interpreted as implied probabilities—50 cents indicates the market believes there is about a 50% chance. As the match progresses and the score changes, prices fluctuate accordingly.

There is a mechanism that will repeatedly occur after the match starts but is rarely explained: elimination zeroing. When a team is mathematically incapable of winning the championship, its "championship Yes" contract will immediately zero out and settle as "No" [4]. As the group stage progresses, the first batch of eliminated teams will emerge—this will be the first large-scale and real zeroing out of these championship contracts. This is one of the most crucial on-chain moments to watch during the tournament.

Act Three · How On-Chain Contracts "Know" Who Won: Two Paradigms

This is something that should be explained on the opening day but is almost never addressed.

An on-chain contract is just a piece of code. It cannot watch the game. So, when Mexico and South Africa finish their match, how does the on-chain "Mexico wins" contract "know" what happened in the real world and then pay the money to those who guessed right?

The answer is called oracles—the bridge that feeds real-world information into on-chain contracts. Currently, there are two different paradigms in the industry answering this question.

First: UMA's "optimistic oracle," primarily used by Polymarket (accounting for about 78% of its market). "Optimistic" means: it initially assumes that the submitted result is correct, then allows a period for others to challenge it. The specific process is—an approved proposer puts up $750 PUSD as collateral, submitting the result "Mexico wins"; next, there is a 2-hour challenge window in which anyone can stake the same collateral to oppose it; if there is no opposition, the market automatically settles based on this outcome, with those who guessed right immediately receiving $1, and those who guessed wrong getting zero, with no need for manual claiming. If there is a challenge, the dispute escalates to votes by UMA token holders to decide the outcome [9].

This whitelist has a backstory: In March 2025, a market called "Ukrainian Minerals" faced a governance attack, affecting about $7 million, exposing the structural weakness of "anyone can submit results." Thus, in August, UMA passed the UMIP-189 proposal, restricting proposal rights to the whitelist—from the initial 37 addresses to an expansion of 177 by November 2025, with the threshold being at least 5 proposals in the past 6 months and an accuracy rate of over 95%. However, it is important to emphasize: the right to challenge remains open to everyone—you do not need to be on the whitelist to oppose any result you believe is incorrect [10].

Second: Chainlink's "multi-source aggregation," used by FIFA official partner ADI Predictstreet and Myriad (Polymarket also has about 15% of its market using Chainlink). On June 9, ADI Predictstreet announced that it adopted Chainlink as its exclusive oracle infrastructure, actively aggregating match results from multiple data sources to automatically complete market creation, settlement, and payment, highlighting "no disputes, instant settlement" [11].

Comparing the two paradigms makes the differences clear: in response to the question of "who determines the truth," UMA's answer is "trust first, leave a challenge window, vote in disputes," while Chainlink's answer is "aggregate from multiple authoritative data sources, automatically feed prices, and leave almost no room for disputes." This is not an either-or situation—Polymarket relies primarily on UMA, but part of the market also integrates Chainlink; for clear and unambiguous events like World Cup match outcomes, both paradigms are much safer than ambiguous political or geopolitical markets.

ESPN will tell you who won. But how do on-chain contracts "know" who won—behind this operation are two completely different decentralized designs.

Act Four · How Much of the Over $2 Billion is Real

This series has been discussing how prediction markets grow. However, as a content piece not focused on casino narratives, we must add a sobering counter-question to this "$2 billion" story.

First, let's look at how money is settled. All of these contracts are priced in USDC, a dollar-pegged stablecoin, and settled on the Polygon chain [12]. One detail illustrates the issue well: a contract that is almost certainly going to win often trades between $0.995 and $0.999 before formal settlement—because some traders prefer to cash out at $0.999 now rather than wait a few hours to complete the oracle process to get the full $1 [9]. This reflects the immediacy brought by the stablecoin settlement layer.

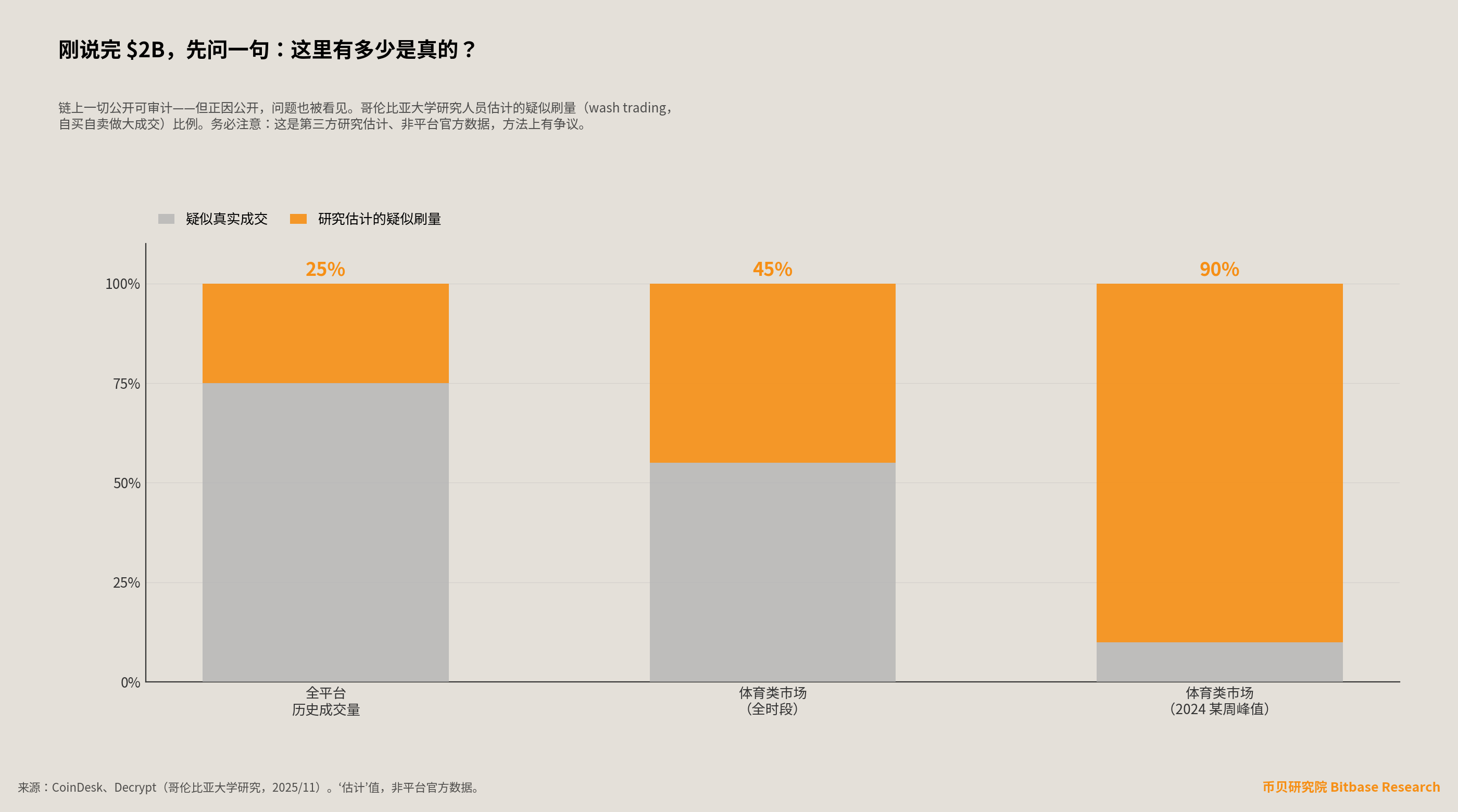

But now comes that sobering counter-question. The benefit of being on-chain is complete transparency, accessible to anyone for auditing. Yet, precisely because it is public, problems also come into view: researchers at Columbia University estimate that about 25% of Polymarket's historical transaction volume may be "wash trading" [13]; and in sports markets, this proportion across all time periods is approximately 45%, with a peak of up to 90% in one week in 2024 [14].

It is important to emphasize that this is an estimate from third-party research, not the platform's official data, and the methodology is also contentious—such as a statistics professor at Rutgers University believing that the narrative around manipulation is exaggerated and carries some bias. But even if we discount the estimate, it still reminds us of one thing: when you see the number "$2 billion," it measures the scale of market activity, not $2 billion in genuine transactions from different individuals.

The platform is also responding. On June 10, Kalshi launched new regulations against insider trading—requiring traders on high-manipulation-risk markets to disclose employer information and introducing a market risk scoring system [15]. This is a hurdle that prediction markets must overcome on their path to maturity.

Conclusion · The Same Bet, Two Identities

Finally, let's return to something fundamental—what do these contracts mean in your jurisdiction?

Some put it very plainly: Betting $100 on France to win, on a sports betting platform like DraftKings, it is categorized as "gambling" regulated by various states, strictly geographically fenced; while buying a "France to win" contract on Kalshi, it is a legally recognized "trade" for adults across all 50 states in the U.S. The same bet, the same excitement during penalties, but the legal identities are worlds apart [16].

This is at the core of the regulatory divergence discussed in the previous issue: prediction markets follow the "event contract" path of the CFTC in the U.S., while sports betting follows state licensing paths. In the days leading up to the opening match, states like Minnesota, New Mexico, and Nevada continue to assert: these so-called prediction markets are essentially "disguised sports betting." This legal battle about "what it really is" is far from over.

The legality of the same World Cup contract can vary completely across different jurisdictions. Readers must verify the rules applicable in their own locations.

As the starting whistle blows, this machine, with over $2 billion wagered, priced in stablecoins, adjudicated by oracle, and monitored by regulators, truly begins to operate. Over the next month, we will witness its first real settlements, its first real zero-outs, and after the final on July 20, we will look back at the market and those predictive models to see who got it right.

How it operates may be more worthy of observation than who ultimately wins the championship.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。