What Walsh inherits is a central bank with visible internal cracks, and Trump's expectation for him can be summarized in two words: cut interest rates.

Written by: Zhao Ying

Source: Wall Street Journal

Trump will personally preside over the oath of office ceremony for the new Federal Reserve Chair Walsh, an arrangement that breaks recent conventions and brings the 70-year power struggle between the White House and the Federal Reserve back into the spotlight. History shows that every Federal Reserve Chair seeks to balance political pressures with policy independence, and Walsh is no exception—but the situation he faces is far more complex than the outside world imagines.

According to a report from the Wall Street Journal citing White House officials, Trump will personally host Walsh's oath of office this Friday at the White House. This breaks recent traditions—ceremonies are usually held within the Federal Reserve, and the President rarely attends. The last time a Federal Reserve Chair's oath was held at the White House was during Alan Greenspan's inauguration in 1987, almost forty years ago.

The fixed income team at Cailian Securities (Sun Binbin, Sui Xiuping, Lu Xingchen) pointed out in their latest research report that although Walsh is not a "dovish chair," it cannot be ruled out that there will be no interest rate cuts this year—the relationship between the Federal Reserve Chair and the US President is not static but changes over time.

However, Walsh is not taking over a prepared Federal Reserve. At the end of April’s FOMC meeting, three governors from Cleveland, Minneapolis, and Dallas cast the most unusual dissenting votes since October 1992—not against the fact of rate cuts, but against even hinting at rate cuts. This means that Walsh inherits a central bank that is already showing internal rifts, while Trump's expectation of him is precisely rate cuts.

White House Oath Ceremony: An Arrangement Full of Political Signals

The arrangement of this oath ceremony itself has already sent out a strong signal. When Powell was inaugurated in 2018, the ceremony was held within the Federal Reserve, and Trump did not attend; the most recent sitting President to personally attend an inauguration was George W. Bush, who attended Ben Bernanke's oath in 2006. Trump's personal hosting of this ceremony directly demonstrates his close attention to the appointment of this Federal Reserve candidate.

On a procedural level, this handover process is also unusually long. Walsh was confirmed by the Senate last week for a four-year term; Powell's term as Chair expired last weekend, but he stated that he would remain on the Federal Reserve Board as a governor, with that term extending until January 2028. Walsh had also agreed to divest part of his personal investments before officially taking office, which delayed the handover process to some extent. During the transition period, Federal Reserve Vice Chair Philip Jefferson represented the central bank at the G7 finance ministers and central bank governors meeting held in Paris this past Monday.

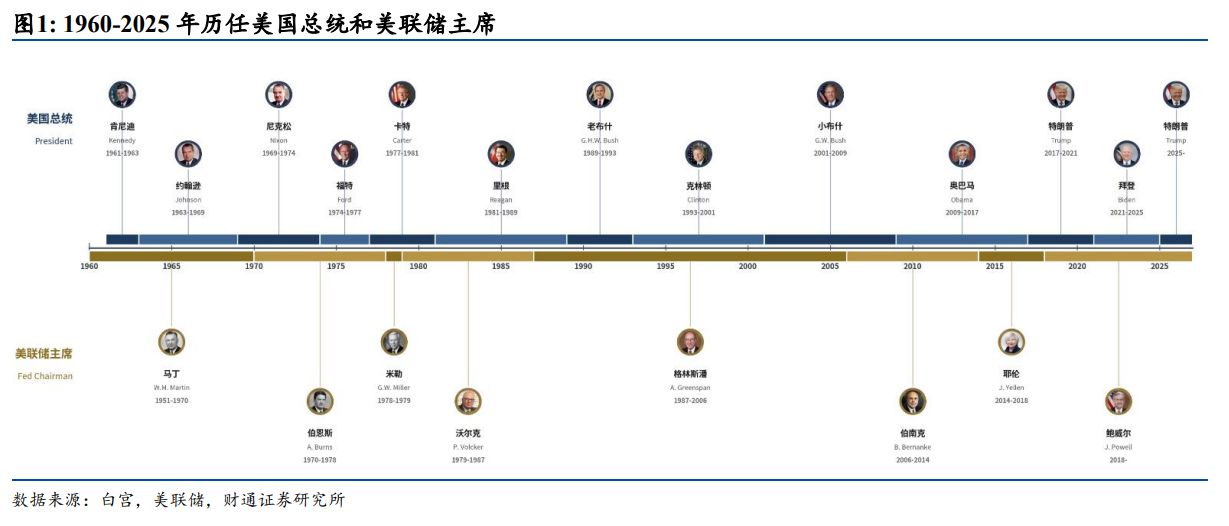

70 Years of Power Play: From Martin to Powell

Cailian Securities' report systematically reviewed the historical relationships between Federal Reserve Chairs and Presidents since 1960, outlining a clear evolutionary trajectory.

William Martin, in the absence of an institutional moat, had to rely on personal reputation to maintain independence. After taking office, he refused to act as an agent for the Treasury, promoting a shift in the decision-making center of the Federal Reserve from New York to Washington, and expanding decision-making authority to the entire FOMC. When Truman met him on the streets of New York, he simply walked away after saying "Traitor."

Arthur Burns' failure stemmed from his own disbelief that monetary policy could end inflation, which opened the door for political pressure from Nixon. Nixon applied pressure through private letters, intervened in the composition of the board, and even sent senior advisors to directly lecture Federal Reserve staff. Burns maintained formal institutional independence but made significant compromises in substantial policy direction, ultimately destroying the credibility of the Federal Reserve.

William Miller represents the most direct political collaboration model—deliberately chosen to align with Carter's political objectives, he became a victim in the face of external crises. By the summer of 1979, inflation had become Carter's biggest political crisis, leading to Miller's reassignment as Treasury Secretary, thus clearing the way for the nomination of a true inflation hawk.

Paul Volcker upgraded independence from "personal credibility protection" to a triple moat of "personal credibility + institutional framework + market credibility." Carter, knowing that appointing Volcker would come at a political cost, still made this choice—as policy advisor O'Sullivan said, this "ultimately squeezed inflation out at the cost of high unemployment, while also squeezing him out of a second term." Although Reagan issued a "command" to Volcker before the 1984 election not to raise interest rates, and in 1986 initiated an "FOMC ambush" through appointed governors, he ultimately failed to significantly alter policy direction.

Alan Greenspan kept the game beneath the surface with technical bureaucratic language, clashed fiercely with the elder Bush, and reached a "Washington-style peace" with Clinton, but during George W. Bush's tenure, he crossed boundaries by supporting tax cuts, becoming the first Federal Reserve Chair in history to proactively "intrude" into the field of fiscal policy.

Ben Bernanke exemplified the model of natural convergence between the White House and the Federal Reserve in a crisis, facing most pressure from Congress and within the Federal Reserve rather than the White House. Janet Yellen responded to Trump's attacks with "depoliticized language + strict self-restraint," becoming the first Federal Reserve Chair to be replaced by a new president since Carter did not renew Burns' term.

Jerome Powell faces the most severe presidential pressure since Burns. During Trump's first term, Powell acted under both external political pressure and internal economic judgments, leading to three consecutive interest rate cuts and a halt to balance sheet normalization in 2019; in his second term, faced with Trump’s investigation based on cost overruns of Federal Reserve remodeling projects and implied threats of dismissal, Powell's response became significantly tougher, elevating the defense of Federal Reserve independence to a historically new height of legality, formalization, and transparency. In his final meeting as Chair, the FOMC maintained interest rates unchanged with a rare dissent of 8 to 4.

Walsh's Dilemma: A New Chair in a Tight Spot

The situation Walsh inherits is rare in history—he faces pressure from the White House for interest rate cuts as well as hawkish resistance from within the FOMC.

Walsh is not a traditionally defined dove. He was appointed a Federal Reserve governor by George W. Bush at the age of 35, making him one of the youngest governors in Federal Reserve history. Following the formal launch of QE2 in 2010, he became the only FOMC governor publicly questioning the expansion direction, resigning early in 2011, which was widely interpreted in the market as a silent protest against the Federal Reserve's over-expansion. His background as an investment banker at Morgan Stanley, executive secretary of the White House NEC, and tight connections with the Republican core circles suggest that his anticipated policy independence is not lower than that of historically similar chairs.

Cailian Securities' report outlines four core points from Walsh's recent speeches and Q&A sessions:

- Firstly, he defines the Federal Reserve's independence more precisely than his predecessor, believing that political interference in monetary policy does not affect the Federal Reserve's independence. This serves both as a desensitization measure against Trump's pressure and leaves room for maintaining policy independence in the future without public conflict;

- Secondly, he holds a negative view on forward guidance, suggesting that markets may need to adjust to a more "silent" Federal Reserve;

- Thirdly, he places significant emphasis on inflation, directly refuting Trump's claim that rising oil prices reflect "false inflation";

- Fourthly, he believes that productivity improvements brought about by artificial intelligence will make interest rate cuts possible, resembling the logical structure of Greenspan's insights into productivity booms in the late 1990s.

Interest Rates Cuts and Balance Sheet Normalization: A Clear Direction with Cautious Steps

Cailian Securities believes that monetary policy under Walsh is highly likely to exhibit characteristics of "clear direction but cautious steps."

In terms of the timing of interest rate cuts, inflation has been above target for five consecutive years, making stabilizing inflation expectations a higher priority. Walsh's emphasis on inflation, especially his denial of the "false inflation theory," indicates that he will not easily cut rates until inflation has clearly receded within target ranges. In the short term, demand growth from data center investments may further offset rate cut space, leading to a slowdown in the pace of cuts constrained by data. The report notes that if Trump grants Walsh more respect, the rate cuts could come sooner; if Trump continues to exert strong pressure, to defend the Federal Reserve's independence, Walsh may actually lean towards cutting rates later.

Regarding the pace of balance sheet normalization, Walsh believes that the expansion of the balance sheet has effectively extended the Federal Reserve's monetary policy boundaries into the fiscal realm, making normalization logically necessary. But he also acknowledges that it took 18 years for the Federal Reserve to accumulate its balance sheet to this extent; normalization is not something that can be accomplished overnight and is expected to proceed slowly and orderly. Additionally, initiating balance sheet normalization without rate cuts can almost be seen as a proactive provocation of conflict with the White House—this also determines that normalization will proceed in a manner that avoids triggering direct confrontation before interest rate cuts begin.

The core conclusion from Cailian Securities is that replicating Greenspan-style management and returning to a scarce reserve model requires first winning support within the Federal Reserve; acting too hastily will only backfire. Judgments regarding Walsh's future policy path should not be based solely on his personal stance or relationship with the White House, but should return to macro trends—where inflation stands, the elasticity of growth, the direction of oil prices, and the tightness of financial conditions—to deduce the most likely choices under different scenarios.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。