Written by: Lacie Zhang, Bitget Wallet Researcher

Introduction: A New Abbreviation on the Wall Street Trading Desk

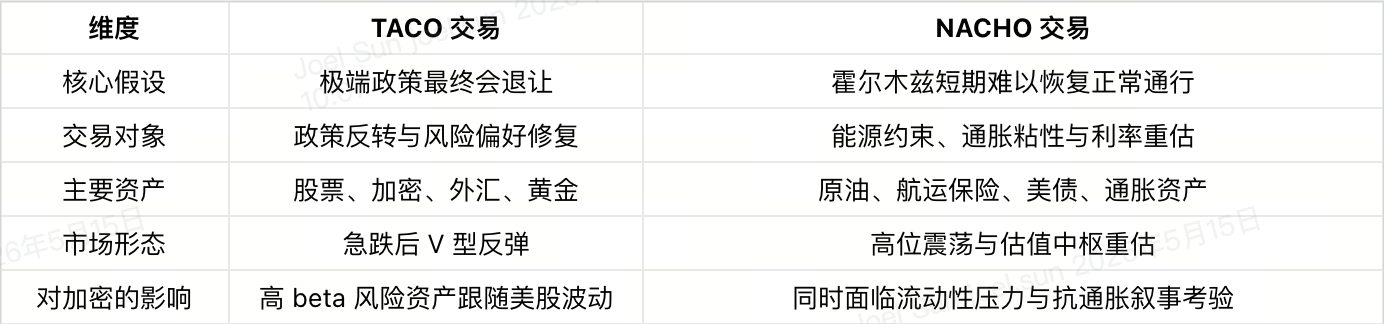

A few months ago, Wall Street was repeatedly discussing a trading abbreviation that carried a hint of sarcasm: TACO, Trump Always Chickens Out, meaning "Trump always backs down."

It described the typical market perception of Trump's policy style over the past period: first issuing extreme threats, triggering panic sell-off in risk assets; then, under market pressure, negotiating space, or political costs, releasing calming signals, resulting in a rebound in asset prices. For traders, the core of TACO is not believing in the policy itself, but believing that there will always be a withdrawal after extreme pressure.

However, entering the second quarter of 2026, the keywords on Wall Street trading desks began to change, and another new abbreviation began to gain popularity: NACHO, Not A Chance Hormuz Opens, meaning “There is almost no chance of the Strait of Hormuz reopening in the short term.”

This term was first popularized by Bloomberg Opinion columnist Javier Blas on X, "We thought we were getting a TACO. But so far we are getting a NACHO." This means that the market originally thought this was another game of retreat after Trump's extreme pressure, but what is currently seen is a stalemate in the Strait of Hormuz that is difficult to resolve quickly.

Subsequently, Nobel laureate Paul Krugman further amplified this concept in his Substack article "The Logic of NACHO". He believes that unlike the tariff issue, the crisis in the Strait of Hormuz is not an event that can be easily reversed by a statement, a meeting, or a social media post. Restoring normal passage in the Strait requires not only political will, but also military de-escalation, shipping restoration, insurance repricing, energy inventory buffers, and rebuilding minimum trust among all parties.

This is also the biggest difference between NACHO and TACO. TACO trading bets on political concessions, while NACHO trading faces physical bottlenecks and trust gaps that are harder to quickly reverse.

For the crypto market, this is not a distant energy market story. Oil prices, inflation, U.S. Treasury yields, Federal Reserve interest rate cut expectations, and global risk appetite will transmit through the same chain to BTC/ETH/altcoins and on-chain yield products, the linkage between crypto assets and global macro variables is being re-strengthened.

1. TACO vs NACHO: The Market Begins to Reassess the Pricing Logic of the Same Conflict

To understand NACHO, one must first understand TACO.

In the TACO era, the market traded on the reversibility of political threats. Trump would send tough signals, causing market panic and a drop; then the policy tone would ease, and traders would start buying the crushed risk assets, waiting for a V-shaped rebound. The institute's previous article on TACO trading has dismantled this pattern: extreme threats, panic selling, calming statements, retaliatory rebounds constitutes a market script that is repeatedly staged.

The reason this logic is effective is that instruments like tariffs, trade negotiations, and technical restrictions themselves possess considerable adjustability. Trump can threaten to impose tariffs, or he can postpone them; he can release strong rhetoric, or he can seek steps down at the negotiating table. For the market, as long as there is a belief that the policy will ultimately back down, panic selling can become a buying opportunity.

But NACHO faces a completely different problem.

The Strait of Hormuz is not an executive document that can be withdrawn at any time, nor is it a Truth Social post that can be easily modified. It is the physical chokepoint in the global energy transport system, involving crude oil transportation, LNG trade, shipping companies, insurance companies, naval deployments, regional security, and the geopolitical games between multiple sovereign nations.

When the market begins to believe that the Strait of Hormuz is unlikely to return to normal passage in the short term, the trading logic fundamentally changes. Investors' focus will also shift from whether political figures "back down" to global energy supply, inflation expectations, and the path of monetary policy itself.

2. Why Hormuz is Important: The Physical Choke Point of the Energy Market

To understand NACHO, one must first grasp the true weight of the physical bottleneck that is the Strait of Hormuz. This strait, only about 33 kilometers wide, carries about 25% of the world's oil shipping, about 1/3 of LNG trade, and almost all exports from major oil-producing countries like Saudi Arabia, the UAE, Qatar, and Iraq.

Since the blockade took effect in March, tanker traffic first plummeted by 70%, with over 150 vessels stranded outside the strait, and traffic volume approached zero within days. Subsequently, Brent crude oil surged past $100 per barrel for the first time in four years, with a monthly increase of as much as 55.32%, marking the largest monthly gain on record. JPMorgan warned in a report early May that global commercial oil inventories would reach "operational stress levels" by early June, and if the strait does not reopen by September, the market will have to start using inventories that can only maintain minimal operations, further compressing the space for subsequent supply recovery.

The impact of the blockage of Hormuz goes far beyond rising oil prices; more critically, it elevates the cost structure of an entire supply chain: blocked tanker traffic leads to re-quoting of shipping insurance, shipowners and charterers demanding higher risk premiums, tightening expectations for crude and LNG supply, accelerating inventory consumption, ultimately propagating to prices of fuel, freight, fertilizers, plastics, food, and electricity.

This is why the Hormuz crisis is difficult to understand through the "policy noise" of the TACO era. Tariffs can be postponed, statements can be retracted, negotiations can resume; but restoring a maritime passage requires rescheduling ships, re-quoting insurance, re-coordinating ports, re-arranging refinery inventories, and even requires both buyers and sellers to trust that the route is safe enough.

Even if one day there is a signal of easing, the energy market will not immediately experience the "V-shaped reversal" as in the stock market. Tankers will not suddenly arrive at ports because of a piece of news; refineries will not immediately fill their inventories due to a statement; insurance companies will not instantly reduce risk premiums due to a negotiation. The recovery speed of the physical world is naturally slower than the trading speed of financial markets. This is exactly the judgment that Tim Duggan, author of The Oil Report, has presented in a long article, which has been circulated internally among several investment banks — "Tanker physics outruns any diplomatic timeline"; no matter how dramatic the political stage is, the physical world has its own rhythm.

Therefore, the core of NACHO trading is to re-answer a deeper question: If the global market is about to face higher energy costs, stronger inflation pressures, and more unstable supply chains, then stocks, bonds, gold, dollars, and crypto assets all need to change their pricing hub under the new price constraints.

3. The Three Pillars of NACHO Trading: Insurance, Oil Prices, and Interest Rates

The reason NACHO has slowly transitioned from an abbreviation on a trading desk to a cross-asset narrative is that it simultaneously changes the three core pricing pillars of major asset classes: shipping insurance, oil prices, and interest rate expectations.

First Pillar: Insurance companies will not underwrite ships crossing Hormuz. Risk rates for Gulf War insurance skyrocketed in March to 2.5% of the hull value, about 8 times the pre-war benchmark. Even when some top insurers attempt to renew underwriting, the additional clauses almost eliminate all "upside gains". In the context of NACHO, even if a political temporary ceasefire is reached, shipowners and charterers will demand significantly higher risk premiums, which effectively locks in the marginal benefits of "reopening the strait".

Second Pillar: Oil prices will remain in the triple digits for a long time. Although Brent has cooled from the wartime peak of $126 at the end of April, it is still hovering above $100, about 38% higher than pre-conflict levels. Goldman Sachs recently pointed out in a report: "As long as the strait remains closed for another month, Brent must remain above $100 for the entirety of 2026." An eToro analyst quoted by CNBC provided a precise summary: "For much of this crisis, every piece of ceasefire news has triggered severe sell-offs in crude oil, with traders continually pricing in a 'solution' that never arrives. This means that if the uncertainty of passage through Hormuz continues, oil prices will carry a higher geopolitical risk premium, and even if there is a short-term dip, as long as the market does not see a sustainable recovery path, the oil price hub may remain above pre-crisis levels.

Third Pillar: The Federal Reserve cannot cut rates amidst inflation. Within the NACHO framework, sustained high oil prices → strong inflation stickiness → the Federal Reserve is forced to maintain "higher for longer" → front-end U.S. Treasury yields continue to rise, and the yield curve flattens overall. If inflation rises unexpectedly due to energy prices and tariff expectations, U.S. Treasury yields could spike above 4.5%, continuously suppressing the liquidity environment and valuations, constituting a negative for all risk assets that rely on low interest rates and liquidity overflow — and the crypto market happens to be at the very end of this transmission chain.

4. What NACHO Means for the Crypto Market: A Repricing from Risk Assets to On-Chain Dollar Returns

For the crypto market, the impact of NACHO is not simply bullish or bearish, but rather a switch in the pricing framework. Over the past period, crypto assets have been more focused on ETF inflows, on-chain ecosystems, and internal narratives such as AI, memes, and RWA; but within the NACHO framework, oil prices, inflation, U.S. Treasury yields, dollar liquidity, and Federal Reserve policy paths become key variables influencing market risk appetite again.

The high beta attributes of BTC, ETH, and altcoins will be reinforced: Sustained high oil prices will bolster inflation expectations; rising inflation pressure will compress the Fed's rate-cutting space; high U.S. Treasury yields will suppress global liquidity and risk asset valuations. Translated into the crypto market, this means "rising oil prices → enhanced inflation stickiness → delayed rate-cut expectations → tightened liquidity → pressure on risk assets". In this environment, Bitcoin may not immediately behave like "digital gold", but is more likely to first follow the fluctuations of risk assets like Nasdaq.

The narrative of BTC as a safe haven will be tested again: Geopolitical conflict, energy crises, and inflation pressures theoretically benefit the narrative of non-sovereign assets. However, Bitcoin's safe-haven properties do not automatically activate; in the initial phase of a market shock, investors first deal with margins, dollar cash, and risk exposure, and BTC is often sold first as a liquid asset. Only when the market shifts from short-term liquidity shocks to long-term concerns about inflation, fiscal, and sovereign credit may BTC's "digital gold" logic take precedence again.

Altcoins and high-valuation narrative assets will face higher discount rate pressure: Many altcoin projects lack stable cash flow, and their valuations largely depend on user growth expectations, ecological subsidies, trading heat, and market risk appetite. When real interest rates rise and the cost of capital increases, these forward-narrative assets' valuations are theoretically compressed more severely.

Stablecoins, RWA, and on-chain dollar yield products re-enter the macro narrative center: If NACHO strengthens the "higher for longer" interest rate environment, the attractiveness of dollar cash flow and short-duration yield assets will rise again. In traditional markets, this corresponds to money market funds, short bonds, and T-Bills; in the on-chain market, it corresponds to stablecoin yields, tokenized U.S. Treasuries, tokenized money market funds, and RWA yield products. Also, geopolitical and energy trade disruptions will highlight the value of stablecoins as a 24/7 global settlement asset.

5. Navigating in the NACHO Era: Survival Rules for Investors

Writing to this point, let's return to the most realistic and important question: as an ordinary crypto investor, how should one respond to this new NACHO script?

The most direct change is that the market is no longer suitable for overly relying on "V-shaped reversals." In the TACO era, many trades were built on an implicit assumption: extreme policies would ultimately ease, and the holes created by panic selling would eventually be quickly repaired. But NACHO is different; it faces not a policy noise that can be withdrawn with a statement, but a reality constraint formed by energy transport, shipping insurance, inventory consumption, and interest rate expectations. Rebounds may still occur, but their rhythm, amplitude, and certainty will decrease. For highly leveraged traders, this means that the margin safety net is more important than directional judgment, and surviving is more important than guessing the timing of any rebound.

At the same time, macroeconomic variables also need to be back in the view of crypto investors. Many people previously were accustomed to only looking at candlesticks, on-chain data, funding rates, project narratives, and exchange popularity, but in the NACHO environment, oil prices, EIA inventories, OPEC+ production, CPI, PCE, U.S. Treasury yields, and SOFR-OIS spreads will influence the crypto market through liquidity and risk appetite. Crypto assets have not detached from the global financial system, especially after deep participation from ETFs, institutional funds, and dollar liquidity; macro research is no longer a backdrop, but part of the trading framework.

In terms of asset selection, the market may prefer certainty. Currently, Wall Street advocates "abandoning soft for hard," and the market prefers assets with stronger cash flow, settlement demand, store-of-value consensus, or real yield sources. Therefore, moderately increasing BTC's weight relative to altcoins and focusing on RWA-related assets may be a good choice, while also allocating certain positions in gold and the energy sector as hedges.

Finally, respect the irreversibility of "non-protocols" and retain respect for sudden changes. Krugman's core insight is that "the only possible protocol is no protocol," but NACHO does not mean that Hormuz will never reopen, nor does it mean that the market can only operate in a one-way direction of high oil prices, high interest rates, and high volatility. Ceasefires, agreements, unilateral de-escalations, and insurance rate declines can all trigger rapid recoveries in risk assets. What needs to be avoided is treating any narrative as the only answer. Whether betting that the crisis will prolong or that the crisis will be quickly resolved, excessively one-sided positions are equally fragile.

Conclusion: From "Coward Game" to "Unresolvable Stalemate"

TACO taught the market one thing: under sufficient pressure, Trump will always blink.

NACHO taught the market another thing: when geopolitical issues embed physical and trust irreversibility, no party has the ability to "blink."

Perhaps this is the true meaning of the NACHO trade: the market is no longer just trading a statement, but is trading a reality that cannot be changed by a statement.

From TACO to NACHO, the market narrative shifted from "betting on reversal" to "accepting the new normal," from "expecting concessions" to "confirming blockades," from "the valuation illusion of soft assets" to "cash is king in hard assets." For crypto investors searching for direction in this cycle, the most important may not be guessing which day Hormuz will reopen, but realizing that when macro narratives again become core variables in the crypto market, we must reevaluate our positions, risk controls, and asset allocations as "noble macro traders."

At the end of the article, Krugman left an open-ended question: "How much more destruction must the world and the U.S. endure before Trump is willing to accept reality?" For the crypto world, a similar question is equally valid: during this NACHO cycle, how many more fluctuations must we endure before truly learning to coexist with the macro?

Uncertainty was once the greatest certainty of the TACO era.

And in the NACHO era, living with uncertainty may just be the new certainty.

Recommended reading: The Return of TACO Trading: When Trump’s "Coward Game" Becomes a Deadly Swing in the Crypto Market

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。