Author: Deep Tide TechFlow

Introduction

On March 16, 2026, the NVIDIA GTC 2026 conference officially opened, and Jensen Huang's keynote speech reignited market enthusiasm.

After listening to the speech, you believe NVIDIA will be the core beneficiary of this wave of AI globalization, and thus you turned around and invested in NVIDIA stocks.

You did not experience a complicated account opening process, and you did not wait for the US stock market to open; just a few clicks of the mouse, and the tokenized NVIDIA stocks had already landed in your on-chain wallet, with fees so low they were almost negligible.

A few years ago, this was almost unimaginable. Today, the market size for tokenized stocks has exceeded $1.07 billion.

When it comes to breaking down the walls between ordinary investors and global quality assets, Ondo is undoubtedly the name that cannot be ignored.

In September 2025, the leading RWA project Ondo Finance announced the launch of Ondo Global Markets, opening trading for over 100 stocks and ETFs simultaneously, thus moving tokenized stocks from scattered experiments to large-scale expansion. Now, just over six months later, Ondo alone holds over 60% of the market share for tokenized stocks, becoming the uncontested leader in this field.

Perhaps this is the truly noteworthy aspect:

In a market with unlimited potential and no shortage of competitors, a nearly unavoidable center has emerged in its explosive initial phase.

When "on-chain freely traded stocks" are no longer just a nice story, a stronger curiosity is stirred by this "cliff-like lead":

In a place where everyone can see the opportunity, Ondo has managed to turn that opportunity into its own territory—how did it manage to do that?

Data Deep Dive into Ondo: From Surface to Depth, Layered Leadership

Before answering "how did Ondo achieve this", let's first take a look at how far ahead Ondo is compared to its competitors.

And determining a market's competitive landscape is best understood through data.

Especially in a field like tokenized stocks, which is still in the early stages of explosive growth, who is leading and who is following—data often speaks more honestly than any story.

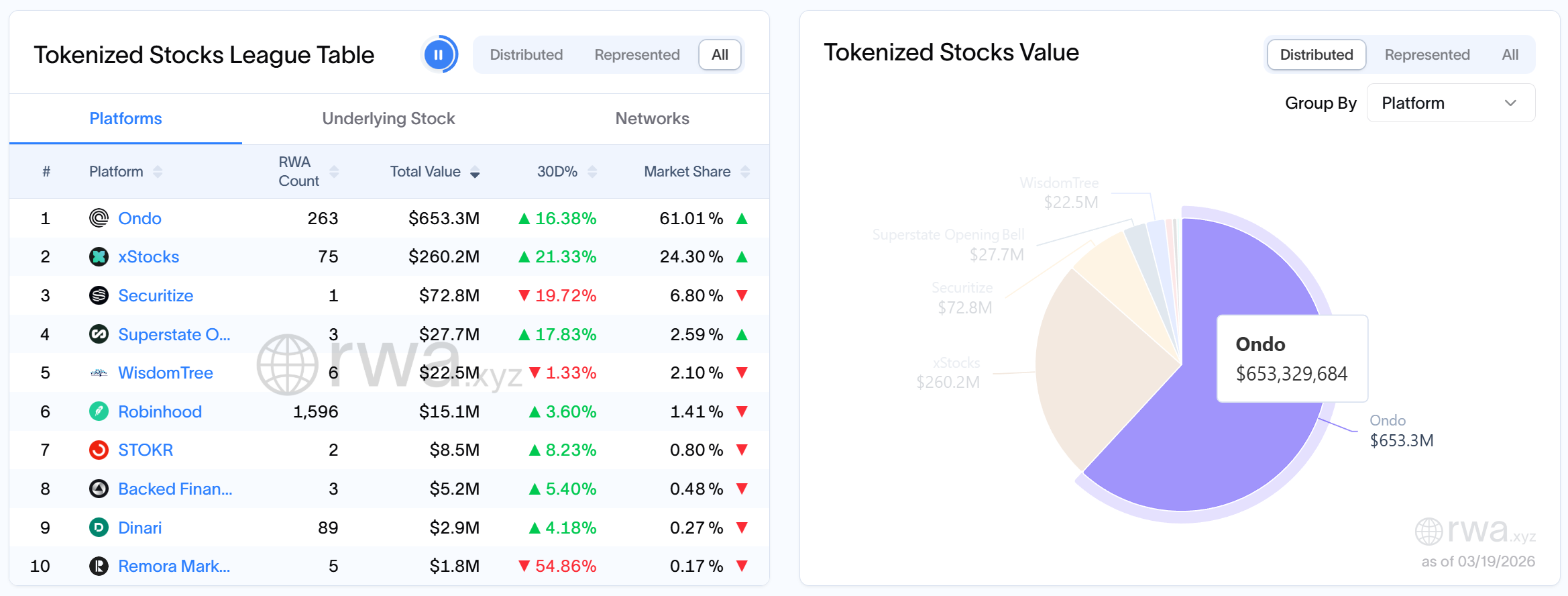

Most people, when discussing the competitive landscape of tokenized stocks, like to describe the situation where Ondo and xStocks coexist as a "dual duopoly," but funding volume has already provided a different answer.

According to data from RWA.xyz, the current total on-chain value of tokenized stocks has surpassed $1.07 billion, with Ondo alone accounting for approximately $653 million. Looking back at earlier data, it can be seen that as early as January 2026, the on-chain value of Ondo's tokenized stocks had already exceeded the total of all other platforms. Now, this advantage has not only remained but has actually continued to widen.

In terms of market share, Ondo holds over 61% of the market share in tokenized stocks, while the second-ranked xStocks holds only 24.65%.

Compared to the "dual duopoly" scenario, Ondo has already created a sufficiently notable gap, being more than 2.47 times ahead of its second competitor.

Now looking at trading volume and users, the comparison becomes even more direct.

According to official data, Ondo's cumulative trading volume has surpassed $12.7 billion, with a daily peak trading volume of $170 million, and a monthly trading volume of $2.18 billion.

Meanwhile, according to RWA.xyz data, under the premise that the total number of holders in the current tokenized stock market is about 199,000, the number of holders on the Ondo platform is 82,900, accounting for about 41.7%. Although it is slightly lower than xStocks' 121,800, Ondo’s monthly active address number of 48,600 is higher than xStocks' 35,200.

The higher frequency trading and more active users represented by these two sets of data can well explain: Ondo's lead is not just about “money gathering here”, but about “actually making the stock market happen on-chain”.

What is even more noteworthy is that the growth of this market continues:

According to RWA.xyz data, over the past 30 days, Ondo's number of users grew by 11.03%. Even with a market share of 61%, it continues to maintain a double-digit monthly user growth rate, indicating that Ondo's current leadership is not a completed stock result but a dynamic process that is still accelerating.

From any dimension, the data points towards the same conclusion: Ondo is the leader in the tokenized stock market.

However, data can only tell you "how much ahead", but it cannot answer "why ahead".

The only certainty is that this multi-dimensional layered leadership is not a random result of a single product decision, but a reflection of a complete strategy.

This strategy is what truly deserves to be dissected.

The Absolute C Position: The "Trio" of Asset Coverage, Transaction Experience, and Ecological Entry

To do tokenized stocks well, what needs to be honed is far more than simply moving stocks on-chain.

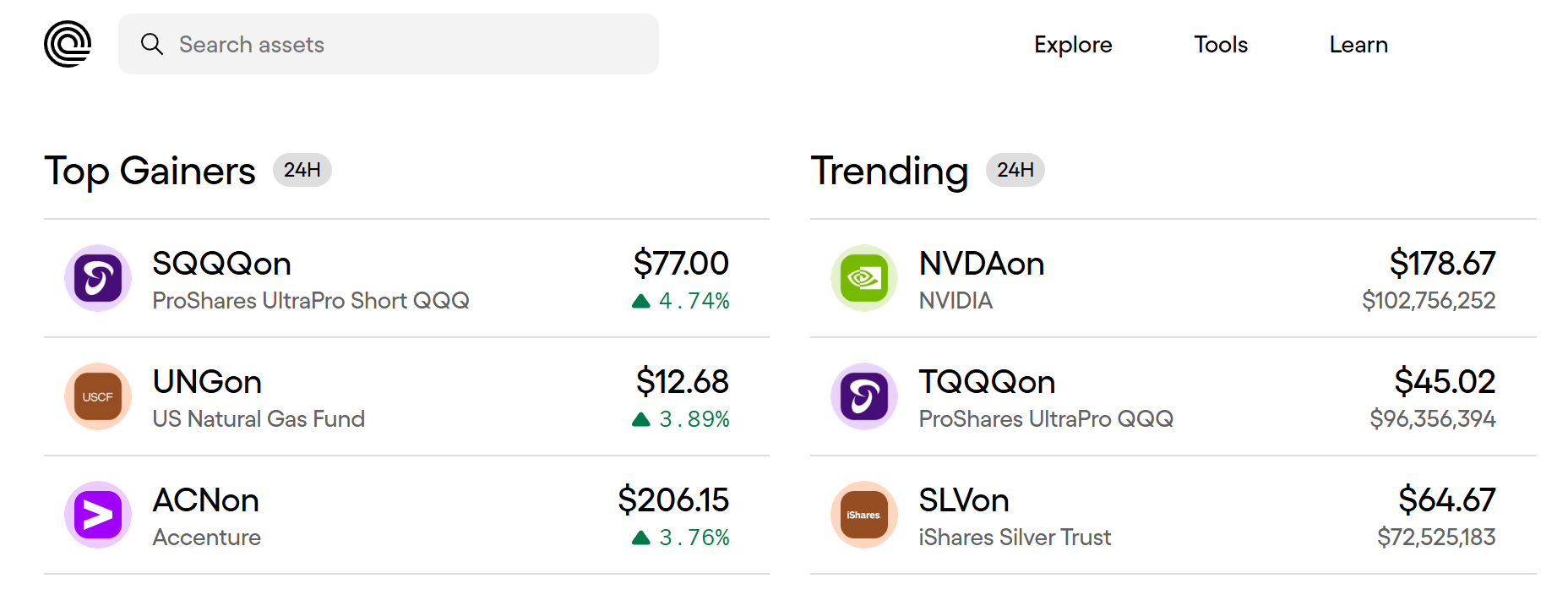

Supporting 265 Tokenized Stocks and Filling the "Shelf" of the On-Chain Stock Market

265 is the number of tokenized stocks supported by Ondo, with no platform surpassing it.

The 265 tokenized assets cover US-listed companies, Chinese concept stocks, energy and commodity-related assets, bonds, index ETFs, as well as leveraged and inverse ETFs among multiple asset classes.

The fuller the shelves, the richer the choices, the more users can be satisfied, and the more reasons there are to retain users.

Faster, Better, Cheaper: Maximizing the On-Chain Stock Trading Experience

Of course, after moving more stocks on-chain, the focus shifts to "why would users trade stocks here, on-chain".

This is a competition of trading experience.

Compared to other platforms, Ondo supports 5 x 24-hour trading, meaning users do not have to stay up late waiting for the US stock market to open. Additionally, Ondo has better liquidity, smaller spreads, and lower fees; large transactions often have slippage below 0.03%, prices are almost in real-time with NASDAQ, and no minting, redemption, or management fees are charged.

Whether it's faster, better, or cheaper, every aspect of experience optimization hits the users' most sensitive points of concern.

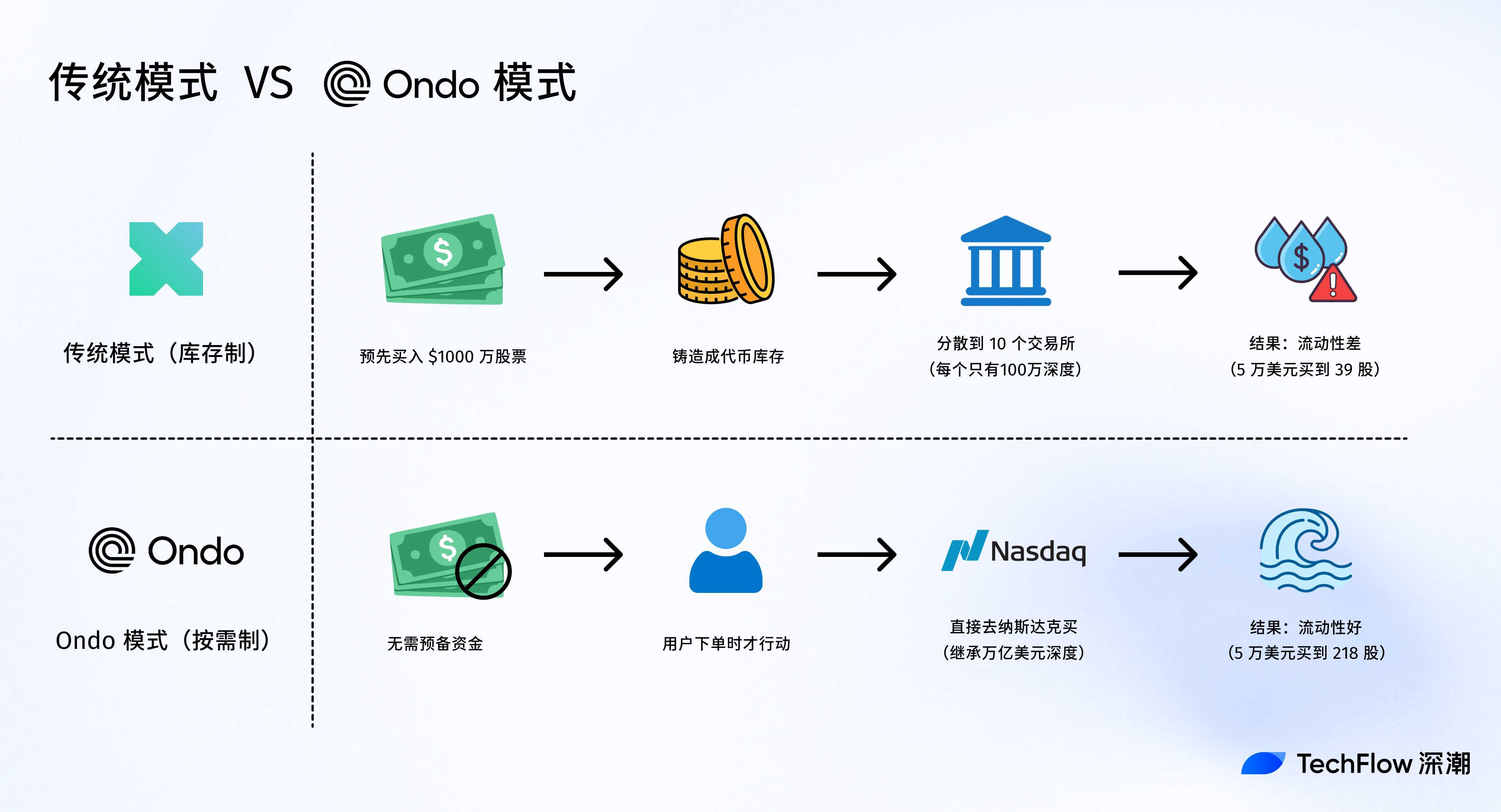

All of this cannot be separated from the fundamental skills of Ondo's underlying design, with the most critical aspect being Ondo's adoption of the "wrapped tokenization + instant atomic minting and burning" design.

The justification for choosing the wrapped tokenization design is compelling: in a native tokenization model, a token is a legal share that must be recorded directly in the issuer's equity structure chart, which makes the process too slow and the legal procedures too complex.

In contrast, wrapped tokenization is more pragmatic and scalable: the token is anchored to the real asset and utilizes regulated custodians and mature market infrastructure to bring publicly traded assets on-chain, without the issuer's participation; the token represents a claim on the underlying shares and is held by the custodian.

Regarding the custodial risks brought about by the wrapped model, Ondo President Ian De Bode provided a vivid analogy: stablecoins are essentially wrapped tokens.

This brings up an interesting discussion: given the already very successful "preliminary version" of stablecoins, since we can accept bringing USD on-chain in this way, why can't we accept bringing stocks on-chain in this manner?

In this regard, Ondo President Ian De Bode's viewpoint is also quite clear: the wrapped model constructed with a strong legal, custodial, and verification framework is currently the most effective and scalable method to bring real-world assets on-chain.

The market's feedback has, to some extent, already validated this point: Ondo's wrapped model occupies 60% market share, while those attempting to adopt stricter or closer to native token structures hold only single-digit market shares.

If wrapped tokenization addresses "how to bring assets on-chain", then instant atomic minting and burning resolves another key issue: how to make these assets more efficiently traded on-chain.

Ondo does not stockpile in advance and build liquidity as in traditional models; rather, when a user places an order, the platform will then buy actual stocks and mint token versions on-chain.

When a token is minted, it becomes a standard ERC-20 token that can circulate 7 x 24 hours on-chain and participate in on-chain finance.

When a user wants to sell, Ondo will burn the token and sell the stock on NASDAQ.

This mechanism effectively avoids the cumbersome path of "stockpiling first, selling later" in traditional models, bringing Ondo two irreplaceable advantages: one is stronger liquidity in an open market, directly accessing trillions of dollars of liquidity in the traditional market; the second is scalability, as there is no need to prepare a capital pool in advance for each stock, allowing the platform to easily expand to hundreds or even thousands of stocks.

Beyond Technology: Seizing the Entry Point

While it is said that "a good wine needs no bush", technology can determine the upper limit of a product, while distribution often dictates growth speed.

Therefore, in addition to honing technology and product skills, another key move for Ondo is to extensively collaborate, embedding Ondo's tokenized stocks and ETFs widely into the entry points where users frequently appear.

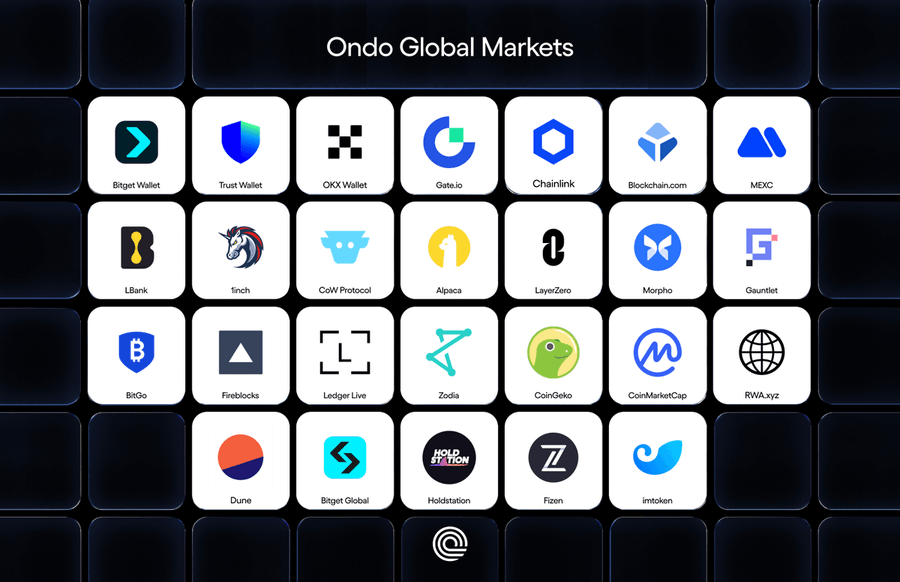

On the wallet side, Ondo has partnered with well-known wallet projects like MetaMask, Trust Wallet, and Ledger; on the exchange side, Ondo has connected with leading trading platforms like Binance, Bitget, and Gate; on the DeFi side, it has integrated with active protocols like Morpho, PancakeSwap, and 1inch; in terms of multi-chain expansion, Ondo has also integrated with mainstream chains like Ethereum, Solana, and BNB Chain, with user bases in the millions, and will expand to Ondo Chain in the future.

The importance of this goes far beyond just having an impressive collaboration list, but truly changes the user's access path.

When wallets, exchanges, and DeFi protocols all start to become distribution channels for Ondo, this means users no longer need to specifically seek out Ondo, but will continuously encounter Ondo within their already familiar usage paths.

Once the entry point is secured, customer acquisition costs, usage thresholds, and migration difficulties will be rewritten simultaneously.

From the data perspective, the effectiveness of this strategy is also quite immediate: whether integrating Solana or cooperating with Binance Alpha, both have brought significant increases in trading volume and active users to Ondo. According to official data, since partnering with Ondo in September 2025, the trading volume of tokenized stocks and ETFs integrated through the 1inch aggregator has exceeded $2.5 billion.

When the three abilities of asset breadth, trading experience, and ecological entry are combined, Ondo effectively answers the three questions most concerning users: Do you have what I want to buy? Is the buying experience good? Can I use it anywhere?

Also, because these questions have been proactively answered, regarding Ondo's leadership, we want to clarify not just the present, but the future.

On the Eve of $150 Trillion Stocks Going On-Chain: Ondo's Narrative of "New On-Chain Asset Infrastructure"

When discussing growth in a market of tokenized stocks, attention cannot be solely focused on on-chain.

If we only look at the present, the tokenized stock market is already quite lively: the market size has surpassed $1 billion, discussions are heating up rapidly, leading platforms are emerging, and more users are purchasing familiar US stocks and ETFs on-chain for the first time.

However, it is vital to remember that the total market value of global stocks is approximately $150 trillion; by comparing tokenized stocks' $1 billion scale, it seems rather insignificant.

The tokenized stock market, rather than being intensely competitive, is more like a supermarket that has just been opened a crack.

This is also the starting point for discussing Ondo's future growth.

In a market with a development rate of less than 0.001%, due to layers of friction such as broker commissions, custody fees, foreign exchange losses, time costs of T+2 settlements, and account opening barriers in the traditional stock market, as long as on-chain stocks consistently outperform traditional paths in trading time, cross-regional accessibility, settlement efficiency, liquidity scheduling, and usage costs, more users will be willing to migrate, and more assets will be willing to go on-chain in the future.

On this basis, Ondo's progress in compliance will further support growth: previously, due to regulatory requirements, Ondo's tokenized stocks faced strict geographical restrictions preventing US citizens or residents from participating. In November 2025, the SEC announced the conclusion of a two-year investigation, without recommending any charges against Ondo. Shortly before that, Ondo announced the acquisition of SEC-registered broker-dealer Oasis Pro Markets; these two initiatives will accelerate Ondo's development in the US market.

Meanwhile, another driving force comes from Ondo's significant leadership position in the tokenized stock market.

Of course, from the perspective of the long-term health of the industry, the community may not necessarily wish to see a platform maintaining a long-term monopoly. Competition is always beneficial, and a diverse ecology is more conducive to innovation.

However, if we return to the realities of business and market laws, we must also acknowledge: once a center is formed, it usually isn't easily replaced, and Ondo has clearly become that center.

Financial markets have never been a world where flow and funds are equally distributed, especially in on-chain finance; the more dependent the sector is on liquidity, depth, brand, trust, and synergy, the more likely the evident Matthew effect emerges: users gather in places with the deepest liquidity, funds lean towards platforms with the most consensus, and partners prioritize connecting with the player most likely to become infrastructure. Once a positive feedback loop is formed, it's increasingly difficult for new players to catch up.

Apart from the market space and center effect, a third growth logic is even more noteworthy: DeFi composability.

In the traditional market, holding rights to a stock often only means: rising, falling, and dividends.

However, when a stock is tokenized on-chain, it transforms from being merely "a tradable asset" to "a composable asset".

The difference between the two is not just one function, but an entire imaginative space.

You can hold it, trade it, collateralize it, connect it to aggregation trading networks, and allow it to freely seek better liquidity and lower execution costs across various platforms. It acts like a building block that can be embedded into the entire financial system; once the underlying interfaces are opened, it becomes the super lever tokenized stocks can genuinely leverage.

From Ondo's series of collaborative integrations with DeFi projects, it is clear Ondo recognizes this.

For example, by collaborating with 1inch, Ondo's tokenized stocks will achieve better liquidity based on aggregated trading functionalities; further, Morpho has confirmed it will accept Ondo's stock tokens as collateral, allowing users to use on-chain stocks for DeFi lending in the future. This will further enhance the usability of tokenized stocks, turning them from isolated assets into nodes that can connect with more DeFi components. As more DeFi modules improve progressively, this potential will only continue to be amplified.

Any one of these three forces is sufficient to support Ondo's continued growth.

And if they all materialize in the coming years, then the narrative of Ondo Global Markets may not just be confined to "a tokenized stock platform", but rather a more imaginative growth space for a new on-chain asset infrastructure.

This may be the most noteworthy aspect of Ondo to watch for beyond growth in the future.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。