Original link:https://x.com/chamath/status/2029650649819009211

Original author:Chamath Palihapitiya

Translation: Ken, Chaincathcer

The modern stock market is built on infrastructure that existed long before digital networks emerged.

The global stock market has a market capitalization of over $150 trillion, yet trading hours remain limited, settlement still relies on multiple layers of intermediaries, and many investment opportunities in high-growth companies are still restricted to a small number of investors.

These structural limitations restrict the ways capital flows, the participants involved, and the speed of ownership changes.

Market infrastructure providers are already exploring how to modernize systems using tokenization. Institutions including the New York Stock Exchange, NASDAQ, and DTCC have begun developing tokenized equity and settlement infrastructure.

As the adoption of equity tokenization grows, these barriers begin to diminish.

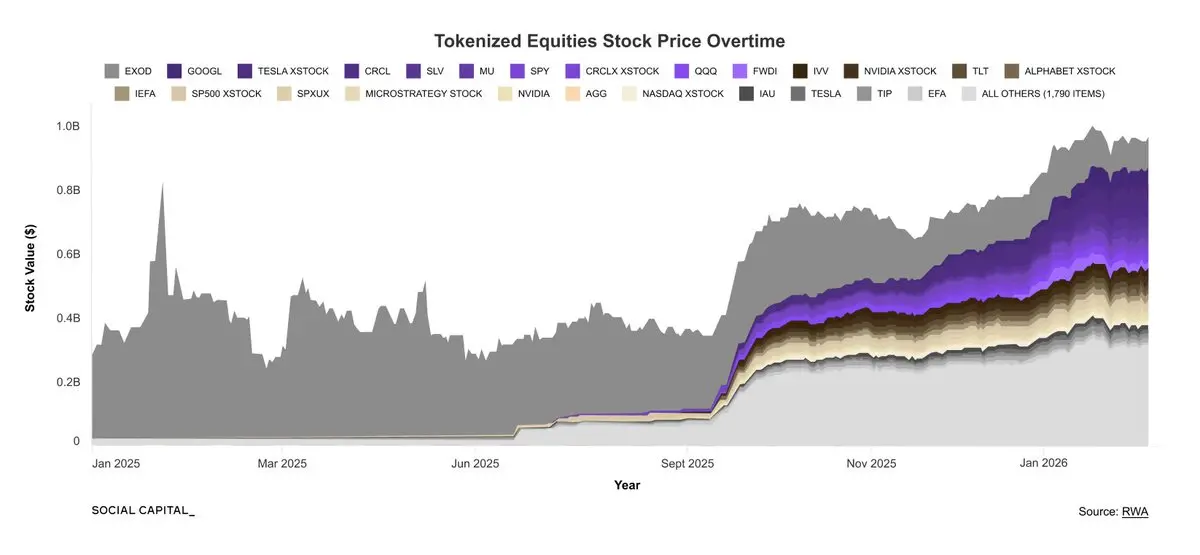

Since the beginning of 2025, the market capitalization of equity tokens has increased nearly 3.5 times, reflecting a broader shift toward the tokenization of real-world assets.

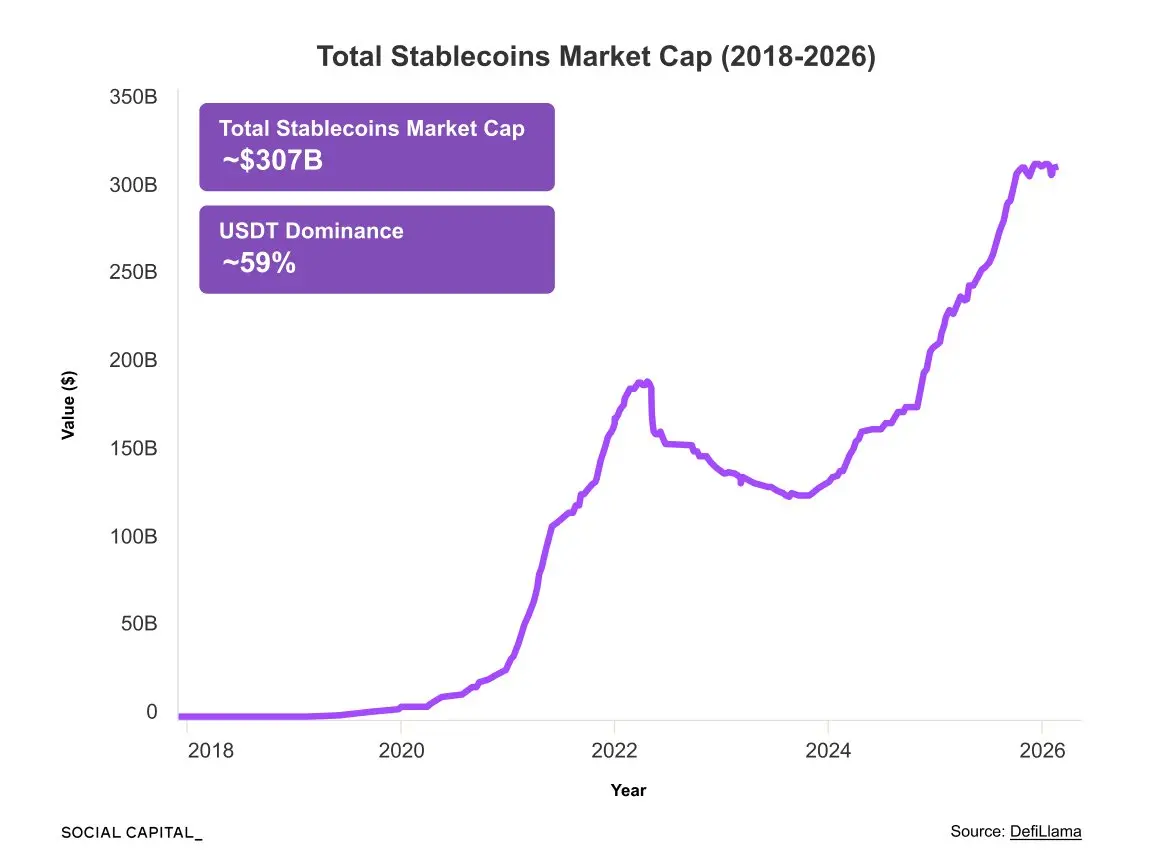

This expansion coincides with the rise of stablecoins. These tokens pegged to fiat currencies have grown more than tenfold in less than five years and have now become the primary settlement layer for on-chain financial activities:

Although the functions of stablecoins differ from equity tokens, their rapid adoption indicates that when tokenized financial instruments can offer significant infrastructure advantages, they can achieve considerable scale.

Equity tokens represent the next test: Can tokenization expand from payments to ownership of financial assets?

What are equity tokens?

Equity tokens are not just traditional stocks placed on the blockchain.

Traditional stocks represent ownership in a company.

Equity tokens are blockchain-based assets that represent shares in a company or structured rights associated with these shares, with ownership tracked and transferred through Distributed Ledger Technology (DLT).

Tokenized equity can address three major market gaps 24/7

All-day trading:The market is shifting from a trading model of five days a week (or shorter) to 24/7 continuous trading.

Even today, about 11% of U.S. stock trades occur outside of regular trading hours.

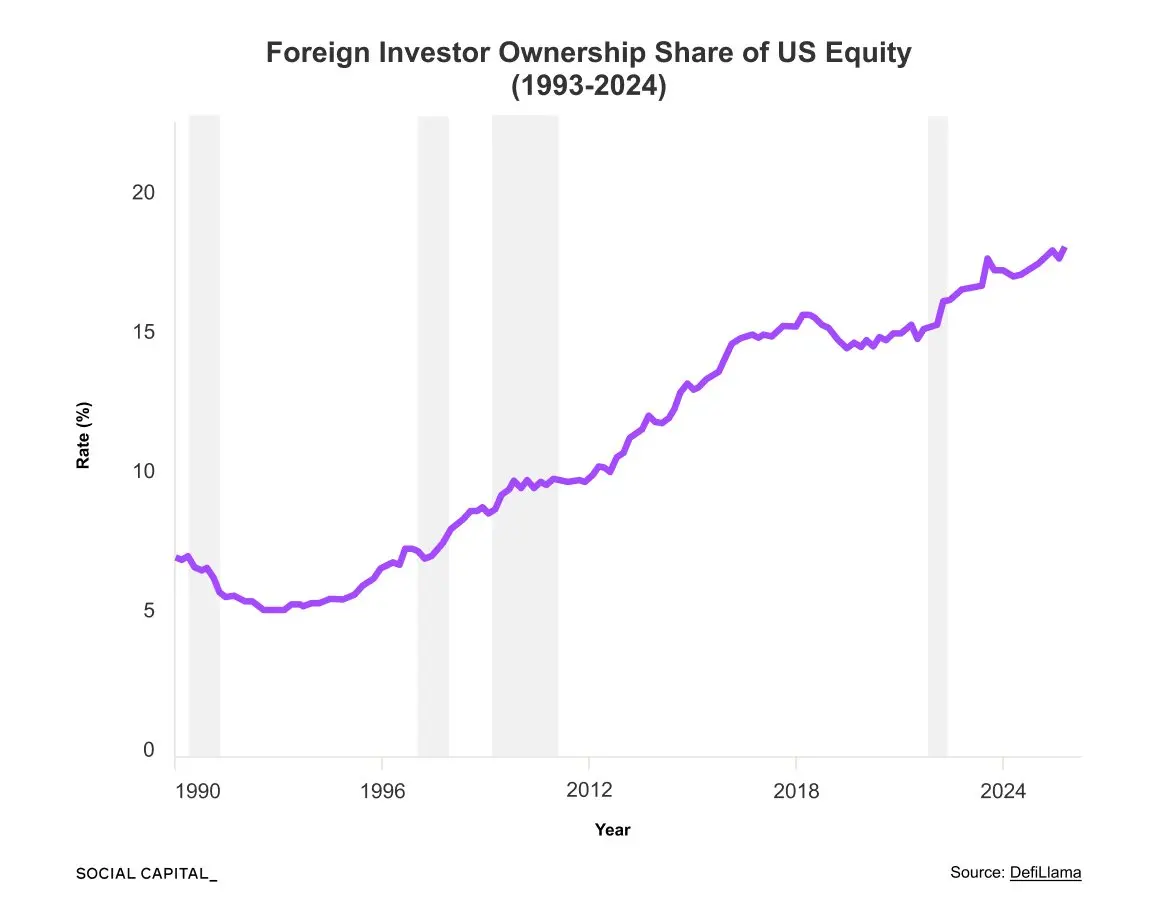

A 24/7 market structure can quickly incorporate new information into prices during after-hours trading and better accommodate a global base of shareholders, as foreign investors currently hold about 15% of U.S. stocks.

Ownership:In traditional finance, equity ownership is recorded across multiple intermediaries, including brokers, clearing houses, and central securities depositories.

Tokenization reduces reliance on these layers and allows ownership to be tracked directly on a shared ledger.

This transforms equity from static records into programmable financial assets.

Owners can use their assets as collateral to obtain on-chain loans. They can use it to secure credit. They can also place it into automated liquidity pools to generate returns.

In traditional markets, similar operations often require multiple intermediaries and additional settlement steps. Each interaction with an intermediary incurs brokerage fees and commissions that ultimately get passed on to holders of equity assets.

Even a slight reduction in post-trade friction is estimated to save the stock industry $5 billion to $10 billion annually.

Access restrictions:While the first two advantages primarily apply to publicly traded stocks, tokenization also addresses access restrictions in private markets.

Under current securities regulations, many private placements are limited to accredited investors. This usually requires the investor to have a net worth of $1 million (excluding primary residence) or an annual income of $200,000, or a combined annual income of $300,000 with a spouse.

Private companies must also control the number of shareholders to maintain their unlisted status. U.S. regulations require that once a company registers, if the number of shareholders exceeds 2,000 or if non-accredited investors exceed 500, it must report to the U.S. Securities and Exchange Commission.

Additionally, institutional venture capital funds often require limited partners to commit millions of dollars.

As a result, most investors have little opportunity to access these high-growth private companies before they enter the public market.

Equity tokenization promises to bridge this access gap.

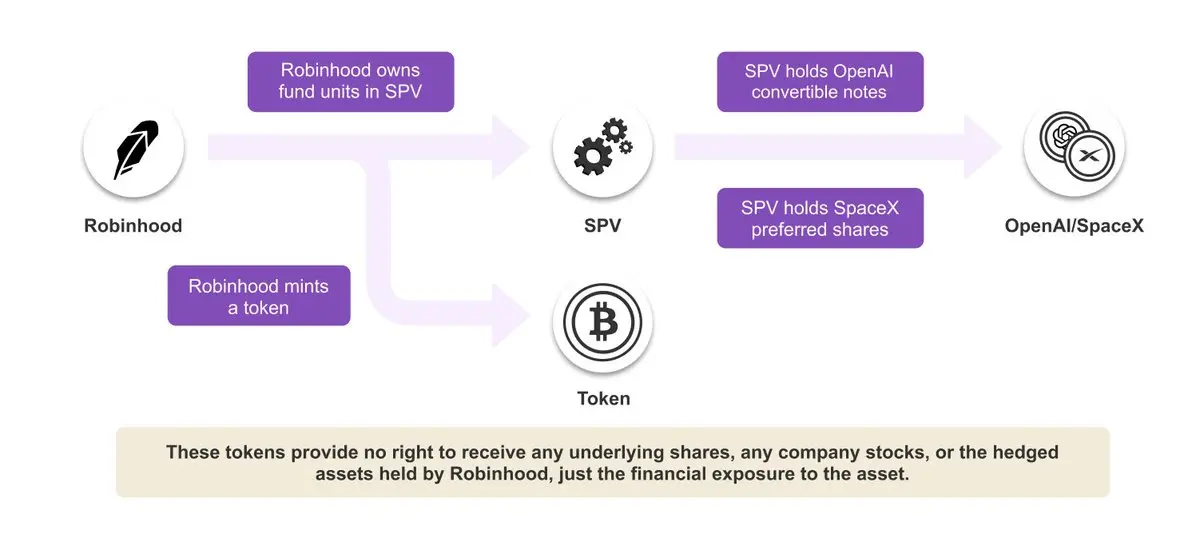

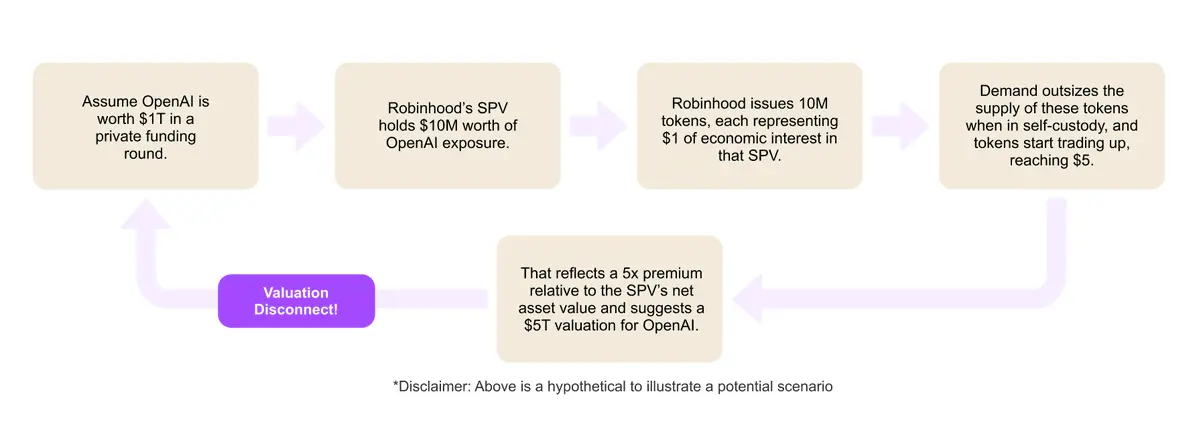

Equity tokens can be issued through various structural models, but the most common approach presently relies on special purpose vehicles (SPVs).

In this structure, the SPV holds the underlying shares while the tokens represent economic claims to that entity. This allows issuers to provide investors with exposure to investments in private companies that were previously limited to venture capital firms and institutional investors.

For example, Robinhood recently announced that it would promote the issuance of tokens for OpenAI and SpaceX to qualified users in the EU.

These tokens give investors exposure to investments in two of the hottest private companies globally. However, they do not represent direct ownership of shares in OpenAI or SpaceX. Instead, these tokens represent financial rights linked to an intermediary.

This highlights a core challenge of equity tokenization: the rights represented by the tokens are not always standardized.

Different issuers can design tokens with substantial differences in economic rights. For instance, with Robinhood, it is currently unclear whether the SpaceX tokens offer preferred stock rights or whether they can convert into common stock if SpaceX eventually goes public.

Preferred and common stocks differ in liquidation priority, voting rights, and return characteristics. Without clear definitions of these terms, it becomes difficult for investors to price or compare tokens tied to the same company.

Consequently, many tokenized private equity products offer economic exposure rather than direct ownership. Since tokens operate at a different legal level than the underlying shares, investors must understand their structure before assuming what they own.

Despite these structural ambiguities, demand from investors for access to private markets continues to grow. In this larger context, companies are staying private (unlisted) for longer periods.

Surveys indicate that about 90% of Americans are willing to allocate part of their retirement savings to private assets, particularly among Generation Z and millennial investors.

Equity tokenization is expected to bring more opportunities to enter private markets, sustained liquidity, and new ways to build financial ownership.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。