Author: Haseeb, Managing Partner at Dragonfly

Translation: Peggy, BlockBeats

Editor's note: In the repetitive cycle of noise proclaiming "crypto is dead," the author Haseeb Qureshi (Managing Partner at Dragonfly) reflects on his personal experience and reviews the process of a crypto VC growing from scratch to scaling, discussing specific issues such as fundraising, positioning, winning deals, post-investment support, and team building.

This article dissects the operational logic of VC from a practical perspective: under the structure where returns follow a power-law distribution, how to understand "non-consensus judgment," how to view hit rates and heavy investment strategies, why "winning deals" is more crucial than "picking the right projects," and why this is a business requiring long-term patience.

For those wanting to understand how VCs operate, this is a direct and specific experience sharing.

Here is the original text:

I have a bad habit: Whenever I achieve something, I can't help but write down how I did it.

We just completed the fundraising for Dragonfly Fund IV, a $650 million crypto VC fund (and at this time, nearly half of the media once again feels that "crypto is dead"). Currently, we manage approximately $4 billion in assets, with around 45 people in New York, San Francisco, and Singapore, and we have become one of the largest VC platforms in this industry where "most people couldn't survive."

So, when a few people asked me to write about how Dragonfly has come this far, I thought: Why not?

To be honest, if someone had given me a blueprint for "how to build a VC firm from scratch" when I first started Dragonfly, it would have been invaluable to me. But the reality is—almost no one will tell you these things.

Honestly, this article will probably only be useful to 0.01% of readers, so spending so much space writing it might not make much sense. But never mind. If you are considering building a VC, or if you happen to be me from 10 years ago—this article is for you.

When I first entered the crypto VC space, most people thought this industry was "dead." It was 2018, just after the ICO bubble had burst, and the whole industry was in free fall. Most of the people who entered the industry with me had already left.

But I always believed that crypto is something destined to exist long-term—it belongs to the kind of idea that once you truly understand it, you can never "pretend you didn't understand." So when people ask me why I've always been optimistic about crypto, my answer is actually very simple: If I didn't believe in it, I would have left long ago. Now, it's too late for me; this optimism has spread to the back of my head.

Therefore, when I met Bo and decided to build Dragonfly together, we didn't expect much enthusiasm from the market. But every VC has to start from scratch.

Lesson #0: For the first fund, you must put your life on the line

The lifeline of a VC is one thing: money.

To have a fund, you must first be able to raise money. If you don't have access to capital (or partners who can help you raise funds), then you are not ready to start a fund.

For your first fund, you must raise money from friends. Your boss, your boss's boss, anyone you know who is wealthy and reputable—even if they are just acquaintances.

If your reputation is not tied to this fund, then it means you haven't taken enough risk. I've seen too many first-time fund managers fantasizing about "preserving their reputation in case the fund fails."

This is an illusion.

If you are not all in, you have no chance of success. If you fail, yes, you will lose face and lose some important people's money. But if you want any chance of success, you must use all the resources you can to make your first fund a success. If you are not willing to do so, then you should not attempt to build a VC.

Once you secure startup capital from those who "have good reason to take a chance on you," you need to move on to larger pools of capital: family offices (super-wealthy families), fund of funds (funds that invest in other funds), and institutional capital (university endowments, foundations, sovereign wealth funds).

Generally, this moves from easier to harder, from lower to higher.

Alright, now you start pitching your fund to these "moneyed" investors. But here’s the problem: as someone doing a fund for the first time, what gives you the right to manage their money?

There is only one answer: you must have a clear and expressible advantage.

Lesson #1: Find a niche angle where you are stronger than anyone else, no matter how small it is

When we established Dragonfly, crypto VC was still a very small field. But even so, there were already several dominating players: Polychain, Pantera, and a16z. In our eyes, they were unshakeable giants.

So initially we couldn't possibly lead any projects. No one wanted our money. We had to find an angle that would allow us to "squeeze into rounds." Just like startups, new funds must be focused.

The initial idea was: Bo is in Asia and I am in the US, so we would focus on "East-West connections." Crypto is global, and we could serve as a bridge between Asia and America, helping founders on both sides enter each other's markets.

This positioning was not enough for us to lead. No founder would want an "East-West fund" to be the lead investor. But it was strategic enough to allow us to secure a small seat—which was enough for us to start squeezing in.

Lesson #2: Do the dirty and hard work

It turns out, this kind of East-West arbitrage was something that almost no one else was competing with us for. I initially wondered: why wasn’t anyone doing such an obvious opportunity?

Later I understood the answer: because it was really, really difficult.

This meant we had to operate a fund spanning both Asia and the US simultaneously, with extremely high daily work intensity; more coordination, more late-night Zoom calls, more language barriers, and nearly no normal life.

If there were a way not to do this and still succeed, who would choose this path? But we had no choice. So we endured it. We worked harder than others and were more jet-lagged than anyone else.

Many people imagine VC as an elegant career: summer vacations, quarterly team-building trips to go skiing. We did none of that. No money, no time, no breathing room. Our closest moment to "winter sports" was during the crypto winters.

Lesson #3: Optimize like a startup

Once you have a niche angle and start to get into rounds, you need to establish a feedback loop. Investing is essentially a feedback loop; the tighter, the better.

Investors ask startups to be highly data-driven and quantitative, yet they themselves often do not do this at all.

You should document everything: your discussions, projects you missed, use AI to record and analyze your fundraising and investment committee meetings; review the biggest deals in the industry, figure out why they succeeded, and summarize it into a theory; study your previous great investors and find their commonalities. Now, with AI, all this is much easier than before.

But most investors do not care about this. They basically rely on "gut feeling" to invest. Success often depends on whether they are lucky or how strong their network is.

Luck might help temporarily, but it is not a strategy and will not compound like cold, hard optimization.

Lesson #4: Talent is everything

The management level of VCs is generally poor; I mean organizational management. One-on-one communication, training systems, KPIs, responsibilities, transparency, all-hands meetings… these basic things are done poorly by many VCs.

Later I understood the reason: VCs do not "filter for management ability" like companies do.

Poor management in companies will eventually lead to failure; but VC is a power-law industry, as long as a few individuals can generate power-law returns, the fund can survive even if overall management is a mess.

However, in the long run, good management itself is an advantage. It can retain the strongest talents and help them grow into the next generation of core members. VCs notoriously do poorly at "generational succession" and internal promotion, with many partners even afraid of hiring younger people who are smarter than they are.

At Dragonfly, we have attracted and retained a group of individuals who would have gone to larger, better platforms. We gave them stability, voice, and independence, proving through actions that we value them—and this is a key reason why we can outperform our peers.

Lesson #5: Be stupidly ambitious

What I find incredible is that most new VCs struggle to articulate "what kind of institution they want to become." "We want to invest in good companies and be the best partners to founders."

Ugh. This is like an entrepreneur saying, "My goal is to maximize shareholder value."

You need to have a real ambition and say it out loud.

When we first started, our ambition was simple: to beat Polychain.

Just that one thing. At that time, Polychain was the benchmark for crypto VCs. Later, when we actually began to surpass it, I realized I needed to upgrade the goal: to become a Top 3 crypto fund. This goal drove us for a long time. Now, in my opinion, we are already in the Top 3, so the goal has become Top 2, then Top 1. As for where we are currently, I'll leave it to readers to judge.

Lesson #6: First pretend you have done it, then make sure you actually do it

For your first fund, you have no brand. So, you must use the little social endorsement you have to immediately forge a sense of brand.

Get into hot projects, even if the amounts are small. Collect logos to trade for more logos. In Fund I, we wrote very small checks in many hot companies: dYdX, Anchorage, Starkware. These amounts were insignificant, but these names gave us the wedge to keep moving forward.

We called ourselves a "research-driven fund." The so-called research was me writing blog posts like "Wouldn't it be crazy if this happened." We called it Dragonfly Research, and at the time, that even counted as research.

We claimed to have the strongest connections in Asia. This was theoretically true, but at the beginning, we also didn't know what others wanted from Asia. We were telling stories while trying to figure things out in real-time and gradually systematized it. Initially, we just pushed the story out as hard as we could—and it really worked.

Lesson #7: Trends are not your friends

Resist the temptation to chase trends. Crypto is full of foolish fads: NFTs, TCRs, P2E, chat bot tokens, VC-backed meme coins...

Our most successful investments often came from avoiding the craziness—and heavily investing when others abandon the track. We never touched Terra, Axie, or Yuga; after Terra collapsed, we invested in the Ethena seed round; before the 2024 election frenzy, we invested in Polymarket.

Each cycle has an irresistible narrative. You feel pressure from the team, LPs, and Twitter. But most hot trends ultimately prove to be a waste of money.

The truly difficult part is the psychological aspect. When you have rejected a project that everyone else is scrambling for, and it rises 5 times the next week, you feel foolish. But chasing trends usually results in a portfolio of "projects that were popular 18 months ago"—the worst configuration.

Your job is to invest in what matters 3–5 years down the line, and hot markets almost never possess this foresight.

Lesson #8: Control your distribution capability

It was once said that a16z is a "media company with a VC business," which was a joke but has now become the truth.

VCs are essentially in the storytelling business. You must build an audience and encourage the whole team to become signal sources. Encourage members to build personal brands and reward them for speaking out. The brand of a VC, unless you are Sequoia, is almost entirely tied to individual people. This is a "people" business.

Some funds even prohibit employees from tweeting, which I completely do not understand. If you expect founders to excel at social media, why can't you?

Lesson #9: Cultivate power

This is a key step for a fund to transform from a beginner to a heavyweight player.

As Dragonfly gradually gained influence, many doors began to open automatically. Exchanges, banks, market makers, and even projects we had never invested in sought to establish relationships with us. At first, I felt this was a distraction: why not look at new projects instead of chatting with established institutions?

Later I realized: the essence of VC is branded money. You win a deal because the founder believes your money is better than others. In fact, all money is green.

Marc Andreessen once said: A VC's job is to lend their brand and power to those who do not yet have it. So, you need not only a brand but also influence. Founders want to know if you can get them in the room and whether your words carry weight.

As the fund grows, you must evolve from a purely investment institution into a platform. The best founders want more than just capital; they want to know if you can genuinely help them further their agenda. We built a platform team at Dragonfly, supporting everything from token design to exchange listings to executive recruiting. It’s not glamorous and doesn’t directly generate returns, but it compounds over time. Once the flywheel starts turning, it becomes difficult for competitors to replicate.

Lesson #10: Almost all the money comes from a very few deals

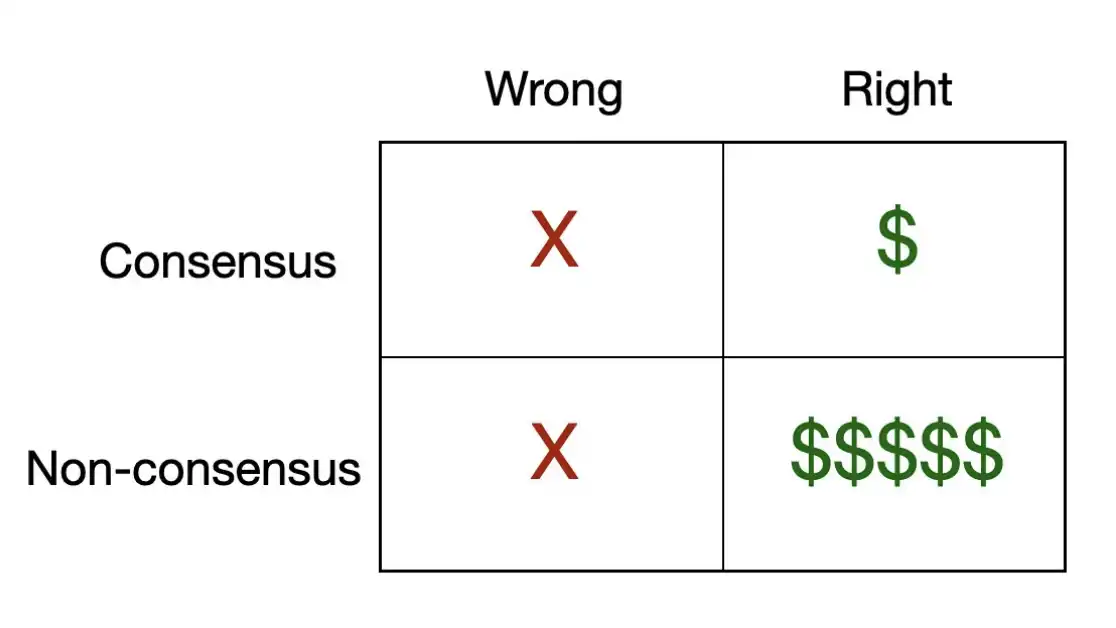

There is a simple matrix that can describe the essence of VC investments.

Many hot projects are actually "trades that consensus agrees on." This means most people believe this company will win, and it indeed does win in the end. These types of trades are usually not bad, but it is difficult to make much money from them because they have often been fiercely bid up by the market, with prices raised very high.

Almost all the real money is made from those "non-consensus but correct" trades. The reason is that these deals are often structurally undervalued in pricing, and your chances of getting a return of 100 times or more almost entirely comes from here.

Venture capital returns follow a power-law distribution, and the math is unforgiving. In a typical fund, the returns from the top three projects often exceed the total returns from all other projects combined. This means that for the vast majority of trades you make, each one separately is not important. What truly matters is whether you hit that one or two projects that define the entire fund's lifecycle.

This brings a counterintuitive conclusion: your hit rate is almost unimportant. What really matters is how many "heavy punches" you threw. Therefore, every time you look at a project, you should ask yourself one question: does it have the potential to become a "fund returner"?

If the answer is negative, then why would you still make this investment?

And that same cruel inference: consensus trades almost never produce such outcomes. If everyone thinks a project is great, then the price has already been reflected in, and your upside is sealed off. The truly generational investments are often those—projects where other smart people would think you were foolish for investing.

Lesson #11: If you can't win that deal, then everything before that is meaningless

The value chain of VC can be broken down into four phases: Sourcing (finding projects) => Selection (judging) => Winning (winning deals) => Supporting (post-investment support)

Finding projects is the first step for a new VC. You must establish a real engine that can continuously find projects.

Judgment is what most people think is the most important skill ("selecting projects"), but in reality, it occupies only a small part of the entire game.

Winning deals is the most crucial part. Even if you have the best project sources in the world and the sharpest judgment, if the founder chooses someone else, everything is meaningless. At the highest level of venture capital, the truly scarce resource is "access to opportunities." The best founders are often oversubscribed; they can choose their investors freely. Therefore, you must provide them with a reason to choose you. This comes back to your brand, platform capabilities, and the relationships and reputation you have built over the long term—all the preceding lessons ultimately converge here.

Post-investment support is the final step, and it also reinforces earlier "finding projects" and "winning deals." Support determines your NPS (Net Promoter Score) and whether this cycle can continue. If you genuinely stand by the founder's side, they will become your best salespeople: introducing you to the next great founder and endorsing you in small groups. This industry is small and very closed, and reputations spread quickly. An angry founder can ruin a dozen of your future deals; while a genuinely satisfied founder can open doors for you for the next decade.

Lesson #12: Venture capital is a "slowly getting rich" business

You will see many people in this industry rise rapidly and become shooting stars of success.

You must outlast them. Some people earn too fast, too much; some start to get lazy, gradually believing that they "should be so successful." The selection process in the crypto industry is particularly cruel. In every cycle, a group of overnight millionaires is born; and in every cycle, most of them will disappear. Traders who made 50 times their money retreat to Lisbon; founders who raised funds at outrageous valuations quietly shut down their companies. Ultimately, the tourists will leave.

You are not a tourist. In VC, measuring progress takes many years. There is no real "overnight success." Most of the value in your fund often remains unrealized for many years. This means you have become the embodiment of that famous New York Times article—

That's fine.

Your job is to keep the ship steady. Debris, wreckage, high tides, low tides—these will all happen. You must always stand there, alongside your team, alongside your founders, alongside the entire ecosystem. Your compensation is to act as long-term capital.

So, you really have to think long-term.

Lesson #13: Raise funds when the timing is right

Founders hate fundraising, and VCs feel the same way, and it is not easy.

Fundraising as a VC is an entirely different cultural system from fundraising as a founder. I came from a middle-class background. When I was a professional poker player, I thought I had seen "rich people." Only later did I realize—it's not even close.

Fundraising itself is an art, and it heavily depends on your audience.

Raising funds from family offices is about relationships. These are wealth families that have been passed down through generations, each with a very unique way of operating, and building trust takes time. They rely heavily on social endorsement.

Institutional capital and fund of funds are another kind of creature: process-oriented, heavily due diligence, placing more importance on forms than on dinner. They want to see track records, processes, and a sustainable advantage.

To be a truly great fundraiser, you must learn to speak both languages simultaneously.

But overall, there is one prerequisite for successful fundraising: you must have either a strong status or have already generated returns; and if you have not yet generated returns, you must tell an incredibly good story about where those returns will come from.

Lastly, and most importantly: timing is everything.

LPs almost always buy high and sell low. So, you should do the opposite. It sounds simple in theory, but is excruciatingly painful in practice.

Your best fundraising windows often occur when the market is hottest and LPs are most excited—exactly when you should be the most cautious in deploying investments. And when the market hits rock bottom and everyone is downcast, that's when LPs least want you to invest—yet that is precisely the wrong time to avoid investing.

The top VCs learn to fundraise when the conditions are best for raising capital, and to invest when asset prices are at their best. And these two events almost never happen at the same time.

Above, I have shared some experiences I learned while building Dragonfly. I am sure I have missed some and undoubtedly there are many lessons I have yet to learn.

Building a VC is a constantly changing game. Each cycle brings a new set of roles, and there will always be mistakes you could completely avoid but are still awaiting you around the corner.

But the underlying principles have never changed: stake your reputation; find your advantage; do the dirty and hard work that others are unwilling to; hire people better than you and truly treat them well; and—maintain patience.

Ultimately, venture capital rewards those who persist long enough to see the other side of the cycle.

This is certainly not "the final answer on how to build a VC." But it's the kind of article I really wish someone had written for me back then. I hope it helps you. If you are doing something cool in the crypto space, feel free to reach out to me.

Disclaimer: This article does not constitute any investment advice. Building a VC fund is hard, and you are highly likely to fail. But who knows—maybe you should give it a try.

Good luck.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。