自ETH进入本轮上涨周期时,每次短期的震荡调整,市场都会开始传播ETH解质押的数据情况。但从供需关系来看,目前机构共识产生的需求远大于解质押的供给,并且我们认为长期满载的解质押情况并不可持续。自以SharpLink为代表的财库公司开始买入至今,美股的持有ETH的公司实体已经持有了近200亿美元的ETH,占总供应量的3.39%,其中Bitmine距离持有ETH总量5%的目标实现还有75%的进度。未来加密友好政策的进一步落地和华尔街的对ETH长期价值形成共识,ETH的“抢购”才刚刚开始,伴随着降息周期即将到来,我们将长期ETH目标价格上调,认为ETH市值在1-2个牛熊周期中将超越BTC。

一、解质押数据

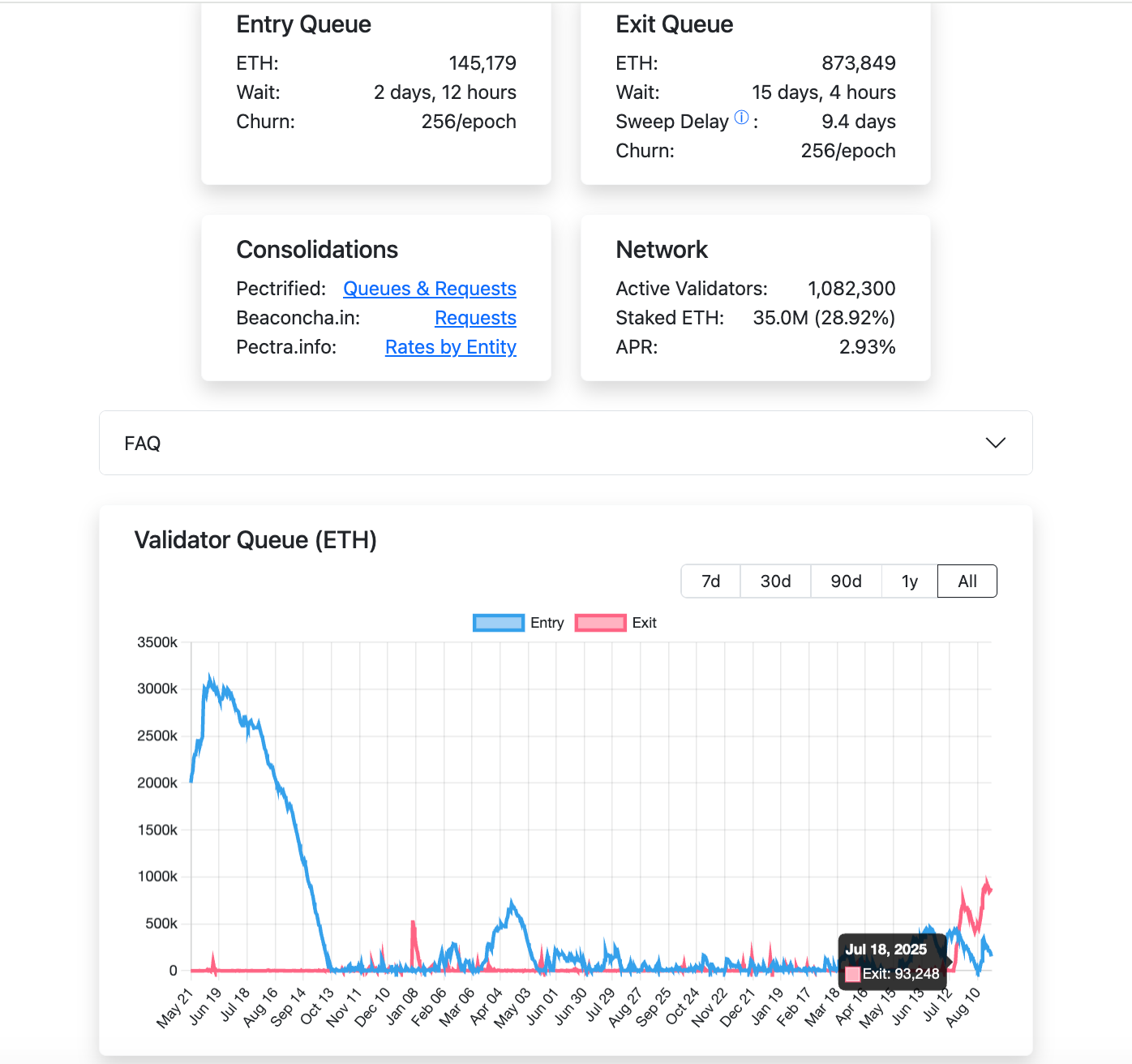

自2025年5月以太坊 Pectra(Prague+Electra)主网升级生效后,质押的理论退出速率按 ETH 数量计价并被硬顶为 256 ETH/epoch(1 epoch≈6.4 分钟)。换算为日,即理论上限为256 × (1440 ÷ 6.4) = 256 × 225 = 57,600 ETH/天。

自7月18日开始,ETH主网的解质押情况就一直处于满载排队的状态,目前(8月24日)有873,849枚ETH在等待解质押,需要15天4小时消化。

ETH一周解质押的数量有上限,最大为57,600*7=403,200枚ETH,而上周ETH财库公司买入531,400枚,在财库公司保持买入状态下,即便解质押部分的100%进入流通也可完全被消化。我们认为,目前ETH的网络价值并没有完全被市场认可,且解质押的ETH并不完全进入流通,随着共识的进一步形成,满载状态的解质押也将改善。

简单来说,解质押并不代表完全的市场供给情况,虽解质押总量随着ETH价格上涨,呈现一定的负相关性,但我们认为,该部分的供给不会主导ETH进入由涨转跌的行情。

二、财库公司与ETF的需求分析

自2025年6月以SharpLink为代表的ETH财库公司开始进入市场,印证了此前我们对于美国将ETH作为金融上链新基建首要阵地的推测(具体内容见我们于6月11日与7月3日发布的《写在暴涨前夕,我们为何看好ETH》,《山雨欲来,市场合力将推动ETH实现价值发现》)。财库公司为代表的机构级购买力入场,根本上改变了ETH价格波动的主导力量。

1、财库公司的运行逻辑-囤币增长即溢价

加密货币财库公司的市场溢价(MNAV)来源于投资者对其买入资产增长潜力的认可。DAT公司通过融资(股票增发或债务)增持加密资产,形成飞轮效应:更多加密资产 → 资产负债表扩张 → 股价上涨→ 更多融资能力 → 进一步增持。这种循环放大市场对囤币股的乐观预期,推动 MNAV 溢价。这种飞轮效应在微策略公司的成功中得以印证,而ETH相对于BTC具有一些更适合做财库资产的特点。

2、ETH财库公司有何不同-资产自带收益

与BTC的买入稀缺性的有限资产不同,ETH作为加密世界最大的DeFi网络,规模化持有将会天然产生收益。

- 质押收益:以太坊自2022年“合并”后转向PoS机制,赋予ETH生息资产属性,同时其生态系统支持DeFi、RWA等高收益活动。这些特性为DAT提供了稳定的现金流来源,构成“现金流溢价”的基础。截至2025年8月,以太坊质押总量达3600万枚ETH,占总供应量的30%,平均年化收益率约为2.95%(实际收益率约1.5%-2.15%)。1.5%的无风险收益,类似传统债券的现金流。

- 流动性收益:通过在以太坊生态中DeFi协议提供流动性获取额外收益。2025年,以太坊DeFi协议TVL约为1200亿美元,流动性挖矿的年化收益率通常在2-10%之间。假设囤币股通过DeFi协议提供流动性,保守估计可获得3.5%的年化收益。综合质押收益(1.5%)和流动性收益(3.5%),囤币股可实现约5%的年化现金流收益。采用折现现金流(DCF)模型,假设折现率为5%,现金流溢价为1倍MNAV,即总MNAV倍数为2倍。

- 其他溢价:以太坊的EIP-1559机制通过销毁基础交易费用,使ETH具备潜在通缩特性。2025年,以太坊预计净增发73万枚ETH(年通胀率约0.6%),但随着网络的销毁。若未来ETH实现净通缩,ETH价格可能仅以上涨并放大囤币股的现金流收益,间接提升MNAV溢价。

3.财库公司的买量才刚刚开始

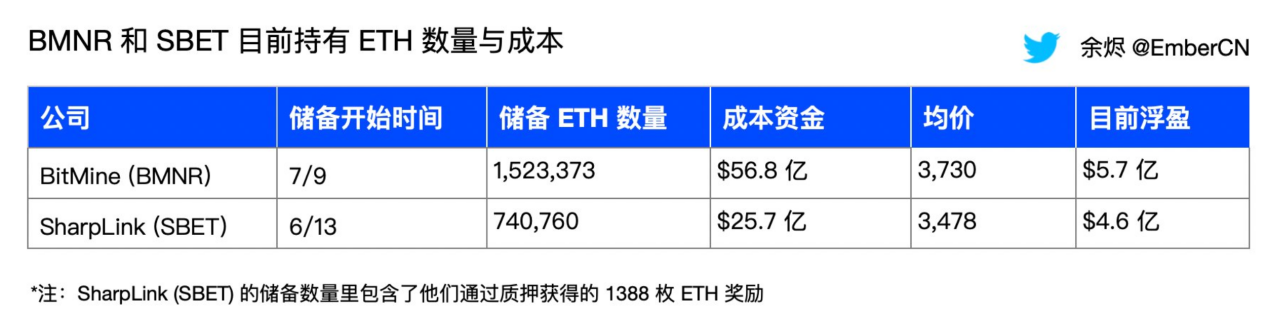

以BMNR和SBET的ETH财库公司的买入成本较高,且后手充足,传统金融的整体买量还处于启动阶段。据余烬总结的数据,BitMine (BMNR) 从 7月9日开始储备了1,523,373 ETH,成本为56.8亿美元,平均价格为3,730 ETH,而SharpLink (SBET) 从6月13日开始储备了740,760 ETH,成本为25.7亿美元,平均价格为3,478 ETH,另包含通过质押获得的1,388枚ETH奖励。随着以太坊价格持续上涨,两家公司持有成本将随之增长。

从未来的融资能力来看:

BMNR:根据 2025 年 8 月 12 日发布的 Prospectus Supplement,BMNR 已将 ATM总额提高至245亿美元,预计已通过 ATM 机制累计融资约 44.5 亿美元,持有约 152 万枚 ETH,理论上仍有约180-200亿美元可用。如果ETH 价格按照 4700 美元/枚计算,BMNR 大约可增持约 426 万枚 ETH,使其潜在总持仓上限接近 578 万枚 ETH,接近持有总量5% 的目标。

SBET:SharpLink 自 2025 年 6 月启动 ETH 国库战略以来,通过 ATM 融资(累计约 12 亿美元)和注册直售等方式,迅速累积了约 740,760 枚 ETH。其 ATM 上限经调整后已由初始额度增加至最高60亿美元,除此之外预计通过定向增发等方式获得约6亿美元资金。假设融资全部用于购买ETH,根据ETH成本,预计剩余ATM余额可购买85.1万枚ETH。

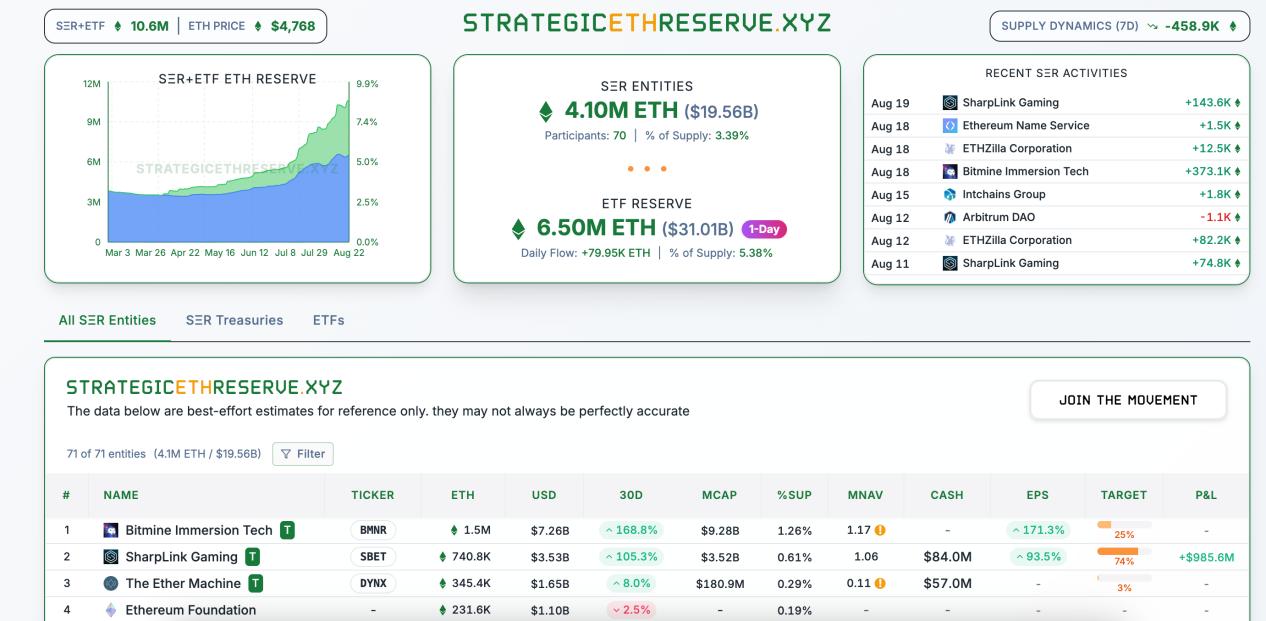

目前,美股的持有ETH的公司实体已经持有了近200亿美元的ETH,占总供应量的3.39%,其中Bitmine距离持有ETH总量5%的目标实现还有75%的进度。

每日ATM可获得资金:

MicroStrategy是比特币财库策略的代表,其交易量在牛熊市中差异显著。

MicroStrategy在2020年实施比特币财库策略,在2020-2021牛市期间,股价已从13美元涨到最高至540美元,每日交易量大幅增加,但受市场活跃度和BTC价格影响较大。若按近期股价和平均交易量估算,每日交易额约为35亿至70亿美元。

而在2022年熊市期间,比特币价格从6.9万美元爆跌至1.6万美元,MicroStrategy股价腰斩,交易量显著萎缩,日均交易量降至2亿至5亿美元。

对比ETH DAT公司,可能会出现相似的情况:

BitMine当前交易量已达到每日20亿美元,最高达到60亿美元,已接近或超过MicroStrategy在上一轮牛市峰值,受到市场受到高度关注。而SBET目前每日交易量波动较大,平均为5000万股,每日交易量约为10亿美元。若市场进入熊市,DAT公司交易量可能萎缩至1亿至5亿美元每日,类似MicroStrategy在2022年的表现。假设每日交易量中10%-20%可转换为ATM,那么持续目前交易量的情况下下,每周可筹集20亿-40亿美元进行购买ETH,按照ATM上限,预计持续3个月。

4、ETF的长期表现依然强势

ETF作为以大规模、低成本获得成功的被动基金,已经成为传统大规模资金配置的首选。自5月16日至8月15日,ETH ETF创下了连续14周净流入,最高单周净流入28.5亿美元,资产净值占供应总量5.38%的数据记录,其中192亿价值(68%)的ETH是在14周中积累起来的,综合买入成本预估在3600美元左右。

贝莱德的ETHA是占比最大的ETF,持有大约2.93%的代币,当前市值172亿美元。2025年4月至今,ETHA每周都处于净流入状态,净流入资金约80亿美元,最大单周净流入23.2亿美元。

目前,全球黄金ETF(加总各地 ETF/ETP)的规模为3860亿美元,比特币为1795亿美元,而以太坊仅为326亿美元,若以太坊叙事可持续,追平当前的比特币ETF规模所需1400亿美元的增长买量。

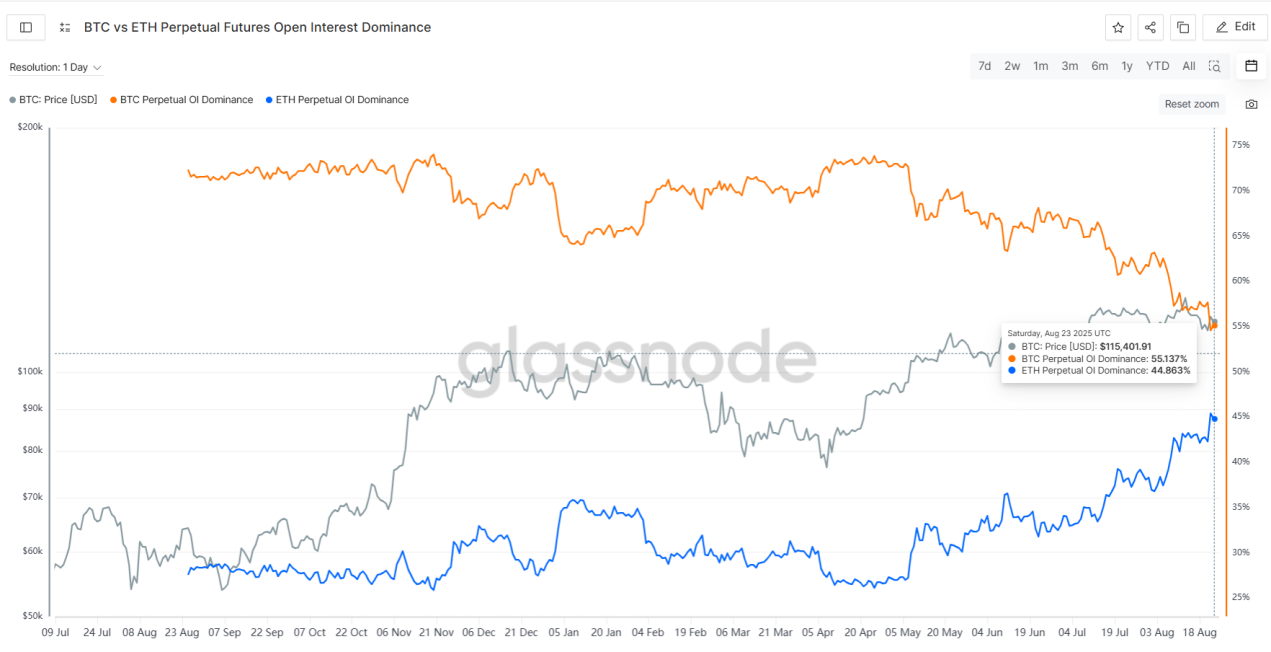

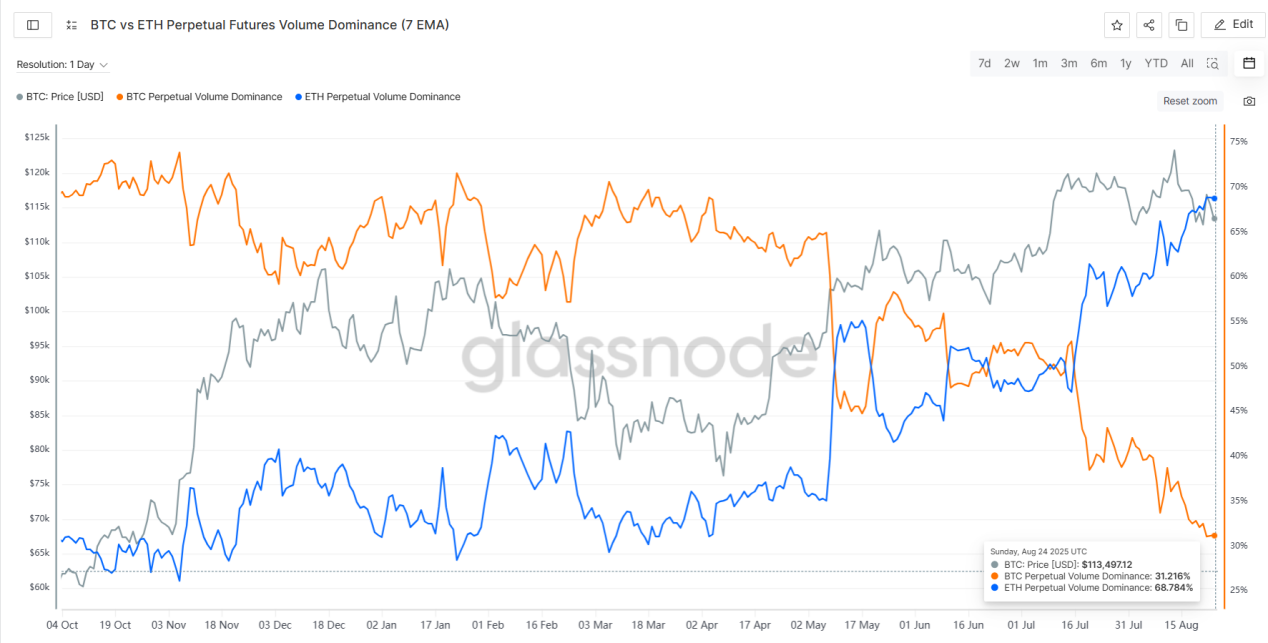

5、市场风偏从BTC转向ETH交易

从合约的持仓量和交易量看,BTC明显降温,资金集中流入ETH。5月初,BTC合约持仓量占比为73%,目前仅为55%;ETH持仓占比则从27%上涨至45%。

从合约交易量来看,BTC的交易量占比从5月初的61%下降至目前的31%;ETH的交易量占比则从5月初的35%上涨至目前的68%,占比在持续提高。

从链上巨鲸近期的行为来看,目前链上出现抛售BTC转而购买ETH的风偏转向行为。据@ai_9684xtpa数据,8月20日开始,一个沉睡7年的BTC远古巨鲸将部分BTC售出,现货上换仓71,108 ETH(价值约3.04亿美元),平均成本约4284美元/ETH。后来总持有增加到105,599 ETH(价值约4.95亿美元)。同时在Hyperliquid上构建ETH多单,并在8月25日向ETH信标链质押269,485 ETH(价值12.5亿美元),直接超越以太坊基金会持仓(23.1万枚)。

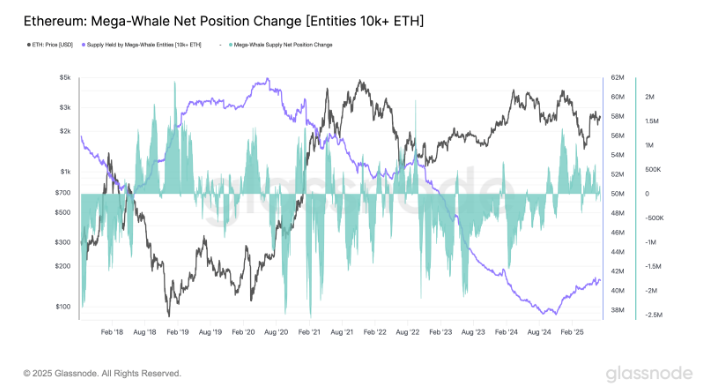

在2025年Q2期间链上以太坊鲸鱼(持有 10,000 至 100,000 ETH 的钱包)在 2025 年第二季度增持了 200,000 ETH(5.15 亿美元),而超级鲸鱼(持有 100,000 ETH 以上)持有的 ETH 总量已从 2024 年 10 月的历史最低点 3756 万 ETH 回升至 4106 万 ETH 以上,自 2024 年 10 月以来增持了 9.31%。

三、BTC筹码结构仍相对稳定

由于风偏转向从BTC到ETH,BTC近期表现相对弱势。从ETF看,有较大幅度的净流出;从链上巨鲸来看,出现大量巨鲸将BTC换手为ETH。从币圈四年周期的过往经验来看,本轮牛市再有2-3个月就达到与此前牛市相当的时间长度。因此,市场存在担忧:BTC是否即将开启熊市,如果BTC进入熊市,ETH如何能够独善其身,走出独立的上升行情?

我们认为,目前美国的财政周期比此前两轮加密牛市时的周期有所延长,同时BTC的筹码结构仍相对稳定,现处于震荡状态。

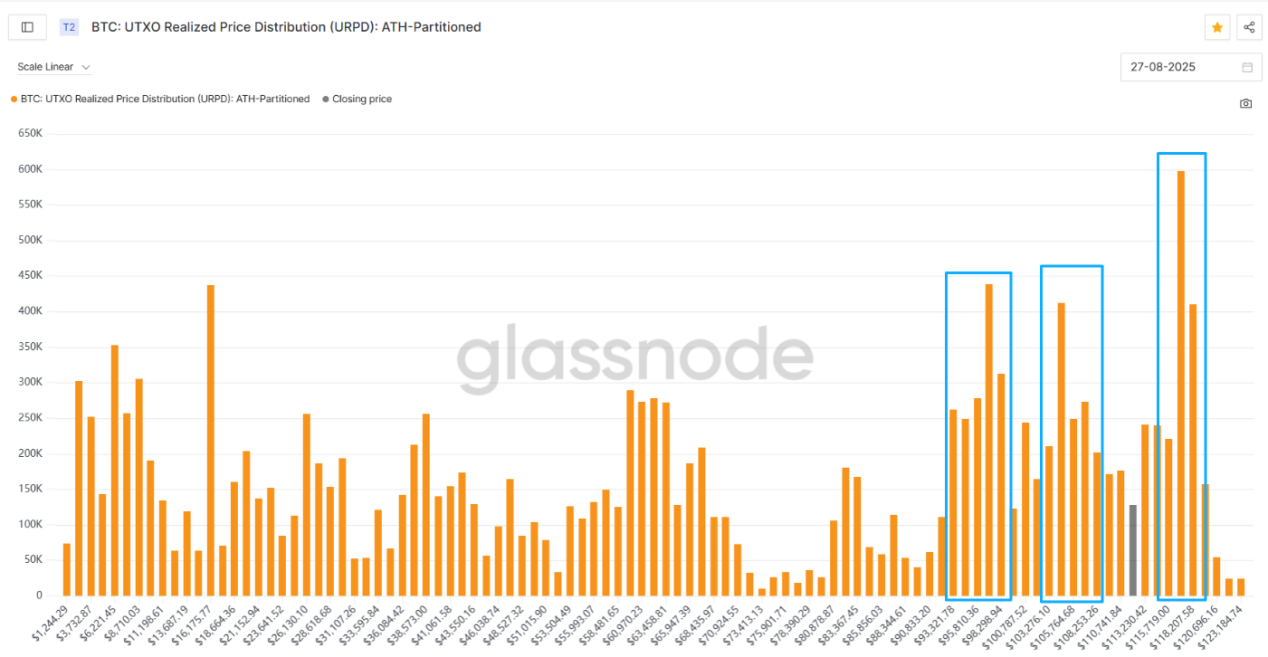

下图是BTC筹码成本分布示意图,灰色柱子为当前价格,蓝色方框中为当前主要的筹码集中区域,分别是93K-98K,103K-108K,以及116K-118K。这三个区域所累积的筹码量巨大, 大量低成本的筹码在该区间完成换手,从而形成了相对较为有力的支撑。

当前,116K-118K的筹码属于微亏状态,下方则有93K-98K,103K-108K两个区间的筹码处于盈利状态。目前BTC价格表现虽然相对弱势,但是,下跌至11K附近获得支撑,下方仍有两个较大的支撑区域,整体处于震荡状态。

此外,当前短期持有者持仓成本大约为108800。当BTC在该位置上方运行时,短期持有者整体仍处于盈利状态,不会发生恐慌性抛售。回顾历史,可以看到在2024年初曾有2次触及短期持有者持仓成本线附近出现反弹的情况,也有2025年2月份第一次触及该成本线就跌破的情况。如果跌破该成本线,BTC将进入中期调整,从而影响加密行业整体走势。

目前,BTC处于关键的位置上,昨日触及该成本线后出现反弹,本周应密切关注BTC能否在该位置上企稳。

四、持续改善的宏观环境

1.美国法规下的根本性估值逻辑重塑

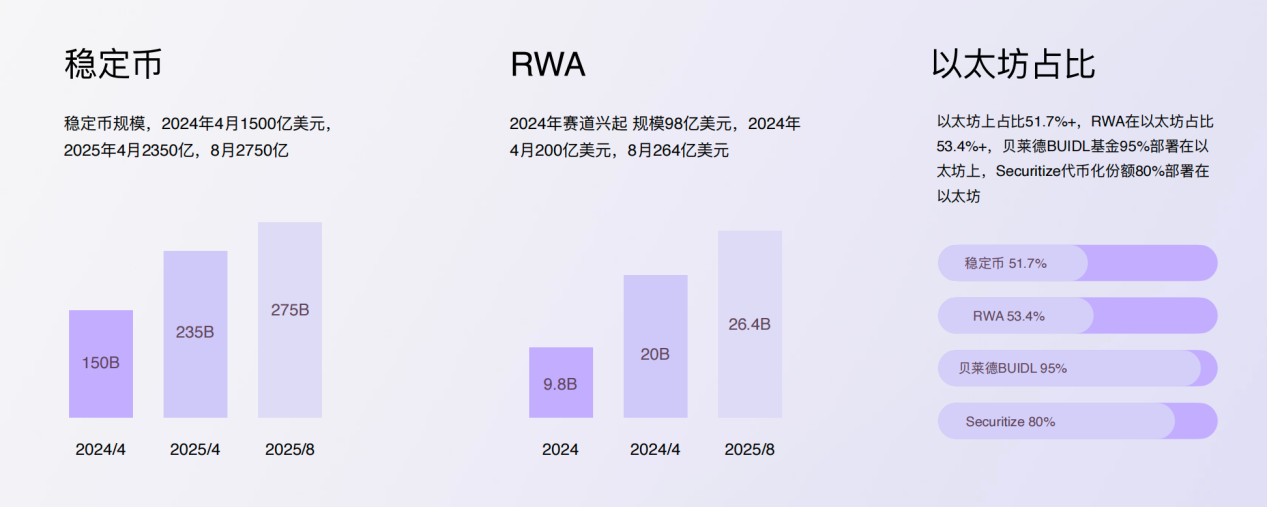

2025年7月,美国GENIUS稳定币法案正式立法,与BTC相比,稳定币1:1锚定美元,更高的资本效率使其更适合作为化债工具。同时稳定币可以推动全球资本高效流入美元体系,支持美国国债购买和链上金融资产的流动性注入,促进美元霸权的数字化扩展。目前,稳定币总市值2750亿美元,而BTC市值为2.2万亿美元,BTC全球矿机价值预估在150-200亿,ETH市值5500亿,质押价值约1650亿。未来,无论是代替BTC部分化债的职能,还是推动资产上链价值的覆盖,亦或是容纳新的支付体系,稳定币的规模在长期都会加速扩张,快速成长至数万亿级美元的市场规模。

而ETH作为稳定币和DeFi的主要基建场所,其价格一方面受益于出于金融链上化的网络安全而进行的ETH购买,还将受益于内生的DeFi模型:稳定币注入基础流动性-DeFi生态利用稳定币创建杠杆和衍生品购买更多ETH-交易活动激增驱动Gas费并促进ETH烧毁。通过ETH网络的交易费用(Gas费)和权益证明(PoS)作为现金流收入,引入现金流折现(DCF)模型进行粗略估值试算,在乐观条件下(7%增长率、9%折现率,杠杆因子3),ETH市值有潜力超过3万亿美元,超越目前BTC市值。

2.降息周期即将到来

8月22日,鲍威尔在Jackson Hole会议上发表演讲,表示通胀仍偏高、但就业的下行风险在上升;在政策仍处“限制性”区间的背景下,委员会将“谨慎推进”,必要时会调整政策立场。分析师们普遍认为9月降息几乎“已成定局”,并代表着一次鸽派的转向拐点。演讲发布后,

加密相关股票和ETH相关标的应声大涨,ETH收回周初的全部跌幅冲向4887历史新高。

在过去的降息周期里,ETH的表现普遍优于BTC,伴随九月议员结束假期重返国会,加密政策的推动将快速推进,ETH的金融上链和DeFi繁荣预期还未落地,为ETH行情提供了积极的宏观环境。

3、稳定币和RWA发展的首选

美国政府和金融机构推动金融上链的步伐富有持续性,目前稳定币规模达2750亿美元,RWA规模264亿美元,其中稳定币50%+运行在以太坊网络,RWA在以太坊占比53.4%,DeFi总TVL1611,60%+部署在ETH上。⻉莱德BUIDL基⾦95%部署在以太坊上,Securitize代币化份额80%部署在以太坊。

在本文中,我们跟踪了部分定量清晰且规模占比庞大的数据进行分析。整体来看,近期供给端解质押数据并不会改变ETH上涨趋势,需求端无论是财库公司还是ETF的新增买量的可预见上限还远未触达,且建仓成本较高。随着美国法规下根本性的金融逻辑转变,ETH同时兼具内外部增长联合推动价格上涨的资产,随着宏观环境改善和政策的进一步发展,长期ETH市值将超越BTC。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。