Original source: 51 Insights | Marc Baumann

Original translation: Deep Tide TechFlow

Deep Tide Guide: For fifteen years, betting on crypto infrastructure has meant buying tokens - this is the core promise of the "fat protocol theory": protocols capture value, and tokens are your share. However, Marc Baumann points out in this in-depth analysis that this deal is dead. In June, Solana set a historical record for tokenized stock trading volume, processing 96% of on-chain stock trades, yet SOL still dropped to $77, down 73% from its peak. Robinhood's chain processed $568 million in daily trading volume in two weeks, while Ethereum only earned $1,538 in settlement fees from it. Value creation has escaped from the token layer to the equity layer—Stripe acquired Bridge, Mastercard acquired BVNK, Kraken acquired Backed Finance, every value event has occurred in equity rather than tokens. More brutally: many token projects from the past decade were never viable for traditional market financing—tokens solved the problem of allowing early investors to exit without the company needing to create value.

For fifteen years, betting on crypto infrastructure has meant buying tokens.

This has been the foundational financial promise of the industry, formally articulated in 2016 as fat protocol theory: applications will be commoditized, protocols will capture value, and tokens represent your share in the protocol. If the network wins, you win.

This deal is dead. Today, I will tell you why.

June: A Moment That Should Have Fulfilled Promises

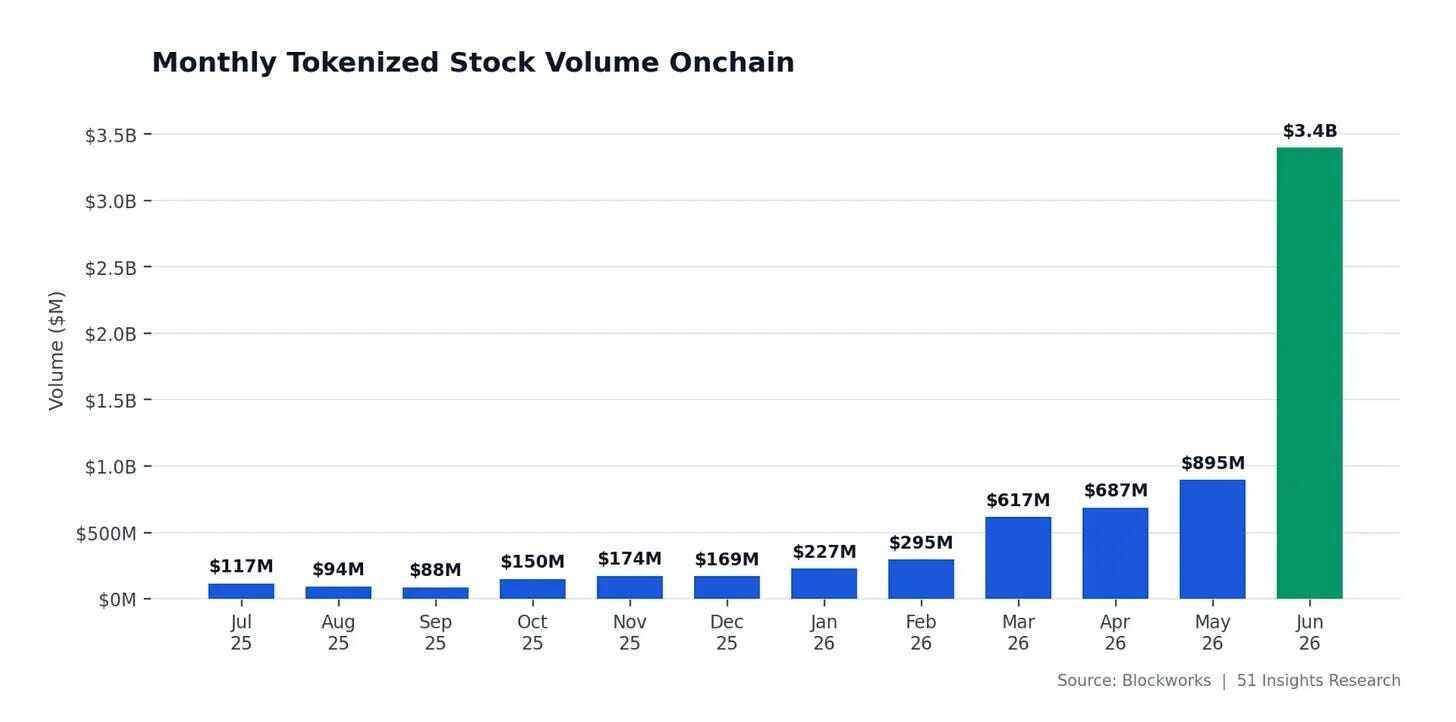

In June, tokenized stocks traded on-chain for a record $3.86 billion, a month-on-month increase of 145%.

The flashpoint was SpaceX's listing on Nasdaq on June 12, raising $7.5 billion with tokenized SpaceX stock launching on Solana the same day. Tokenized SPCX alone traded for $1.19 billion, accounting for about 31% of the month’s total tokenized stock trading volume. Solana took on approximately 96% of the trading volume. On June 23, tokenized assets surpassed meme tokens for the first time in the daily spot trading volume on Solana. Active addresses retested annual highs, and throughput approached historical records.

Yet the price of SOL was around $77. It has halved over the past year, down 73% from its peak, hitting its lowest level since December 2023 in mid-June.

Figure: Solana price trend. Source: Google

The fastest growing category in the crypto space is priced as a declining network.

The mainstream explanation is macro factors: bear market, ETF fund outflows, patience required.

My interpretation differs. What is breaking this cycle is the value link itself. Value creation has left the token layer and shifted to the equity layer—those companies building infrastructure. And these companies do not have tokens. Look at where funds are actually flowing:

- Stripe acquired Bridge for $1.1 billion in February 2025

- Mastercard signed an agreement in March to acquire BVNK for up to $1.8 billion (Coinbase had previously been close to acquiring it for around $2 billion, but the deal fell through in November)

- Kraken agreed to acquire Backed Finance (the issuer of xStocks) in December 2025, preparing for its IPO in 2026

- Securitize is listing its common stock on the New York Stock Exchange and tokenizing it on Solana on the first day of listing

None of these value events occurred in tokens. Each one took place in equity.

The reason is simple: equity is an executable right to cash flow

The reason is boring but legal: equity is an executable right to cash flow. Most tokens are not.

When $3.86 billion in tokenized stocks traded on Solana, the network only earned a fraction of a cent per transaction, as the near-zero fee is the product itself. The minting and redemption spread, custodial fees, and market-making profits—all flow into the income statements of issuers, brokers, and exchanges. Tokens made the headlines; companies made the income.

Ethereum Dissection: $1,538 vs $816,000

Robinhood launched its own chain on July 1—a Layer 2 built on Arbitrum’s tech stack that offered tokenized stocks to customers in over 120 countries. Within a week, it processed $568 million in daily trading volume. Then ARK Invest’s Lorenzo Valente released an income dissection: since its launch, the chain earned about $816,000 in total revenue, of which Robinhood retained about 89%, Arbitrum took 10%, and Ethereum earned only $1,538 for settlement.

Fifteen hundred dollars, or 0.15%, to secure the entire system.

Fat protocol theory asserts that the foundational layer captures value. Here is the foundational layer capturing $1,538.

Meanwhile, financial instruments successfully capturing Robinhood chain value do exist—it trades on Nasdaq under HOOD. There is no Robinhood chain token, nor does anyone miss it.

The internet has run this experiment. TCP/IP, HTTP, and SMTP created more value than any technology in history, yet captured none of it. Value flowed to what was built on top: Google, Amazon, Netflix, Airbnb. By the late 1990s, carriers laid more than 80 million miles of fiber to own the internet's growth, while the most vocal prophet of that time, George Gilder, promised there would be "no losers in a trillion-dollar market." Within a year, two of the carriers he praised went bankrupt. Over $500 billion evaporated, and 216 telecom companies went out of business, while 85% of the fiber remained dark in 2005. That dark fiber later made bandwidth cheap enough for YouTube to exist. The pipes created value, while the companies on top captured value. The crypto Layer 1 is replaying the telecom trade.

The More Brutal Truth: Structural Problems in Token Financing

Many token projects of the past decade could not secure financing in traditional markets: no revenue, no executable rights to future revenue, and no credible plans to generate either.

In the equity market, such companies would not be funded. In crypto, they’ve been massively funded because tokens solve a problem that securities can never resolve: they allow early investors to exit without the company needing to create value.

Binance Research recorded this in 2024. When tokens launched, only 13% of the supply was in circulation, with about $155 billion in locked supply scheduled to flood the market from 2024 to 2030. Venture funds buy at private prices and sell in unregulated secondary markets after a one-year cliff, rather than the 7-10 year wait required for equity. Counterparties? Retail investors. Even venture capitalists themselves acknowledge: Dragonfly's Haseeb Qureshi described these price discoveries as occurring in "manipulated, delusional, or both" private markets.

All of this doesn’t require fraud. That’s the worst part. The structure is disclosed and legal; it pays people not to build.

Celestia and Polkadot: Fundamentals Improve, Prices Hit New Lows

Celestia (TIA) launched with an 8% annual inflation rate, peaking at nearly $20.85 in February 2024. Then on October 30, 2024, a cliff unlock released 176 million tokens, nearly doubling the circulating supply, as early supporters sold off, and buyers hedged using perpetual contracts, with approximately 409 million tokens to continue unlocking until early 2027. The token currently trades below $0.40, down approximately 98% from its peak. These emissions were supposed to bind usage: in the most recent 24-hour period, the entire network recorded only $89 in fees. Not $89 million. Eighty-nine dollars, with a market cap close to $370 million.

Celestia is not an exception; it’s the pattern. Polkadot was among the top five assets in 2021, valued at over $50 billion, with each cycle's pitch being the same: another step up. On June 28, it hit a historic low of $0.7993, six years post-launch. DOT currently trades below $0.90, down approximately 98%, even lower than its launch price in 2020. And this happened after the project did everything holders demanded: setting a hard supply cap of 2.1 billion DOT in March, cutting issuance by over half, obtaining a Nasdaq-listed spot ETF in the same month, and remaining at the top of developer activity rankings. Fundamentals improved. Prices still hit new lows because prices were never tethered to fundamentals from the start.

Solana is the strongest counterexample, which is precisely why June was so illustrative. SOL has real fee capture, real staking economics, and the deepest usage in the industry, yet it still decoupled. If the best tokens can't translate record usage into price, weaker tokens have no arguments at all.

The Asymmetric Reality: Public Investors Cannot Access the Value Layer

This leaves an uncomfortable asymmetry:

The layer public investors can buy does not capture value. The layer that captures value is largely inaccessible to public investors because it exists in private companies absorbed by Stripe, Mastercard, and Kraken, before the prospectus is printed.

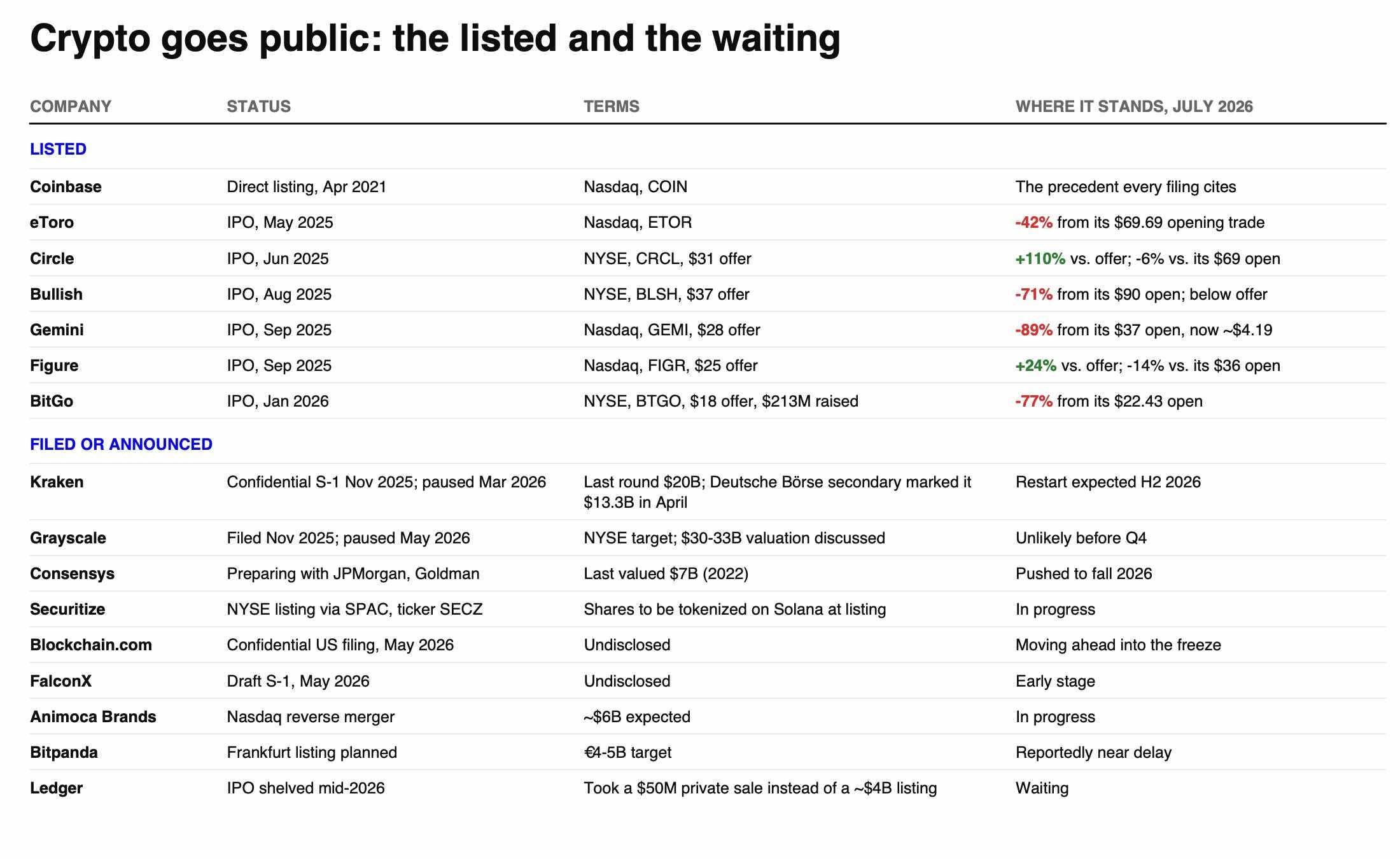

…Unless they IPO, right? Crypto companies raised $3.4 billion through IPOs in 2025, and the pipeline for 2026 is forming. Then public market audits swept over them: Gemini down 89% from its opening price, BitGo down 77%, Bullish down 71%. Meanwhile, companies with continued, usage-linked revenue held their ground: Circle continues to trade above about 110% of its offer price, Figure above about 24% of its offer price. Equity is not a magic wrapper—it is a claim on cash flow, and when cash flow is real, this claim has held up even in the worst crypto markets.

What the Bear Market is Really Doing: A Complete Audit

This is what this bear market is truly doing. A downturn is an audit. It separates "claims on something" from "claims on attention," and it does not respect asset class boundaries: it has almost equally brutally repriced exchange stocks tied to trading volume leverage. A decade of crypto capital formation is being marked to market, while the mark falls precisely where there are legal claims to real cash flow.

Possible Counterarguments

Tokens are programmable claims, and claims can be rewritten. Fee switches, buybacks, and revenue sharing could re-couple usage and prices; Solana’s Alpenglow upgrade along with a genuine regulatory framework might just achieve this. Dragonfly's Haseeb Qureshi also pointed out that 13% of circulating supply at launch was normal in the last cycle, so the structure isn’t new; perhaps what’s new is that marginal buyers have stopped appearing. And it could just be beta. Tokenized RWA has risen 40% year-to-date, while the broader crypto market has dropped about 20%, so divergences could compress when the macro turns. My bet is it won’t compress much because the divergence is contractual, not cyclical.

Fat protocol theory says value will aggregate at the protocol layer, and tokens are your share. This cycle demonstrates that value aggregates in entities holding legal claims, and those legal claims have never been in tokens—they have always been on the equity sheet.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。