Original author: Su Yang

Original editor: Xu Qingyang

Original source: Tencent Technology

News on July 15, ASML announced its financial report for the second quarter of 2026. Total net sales of 9.326 billion euros, net profit of 2.918 billion euros, both core indicators exceeded Wall Street analysts’ expectations.

As the most crucial lithography equipment manufacturer in the upstream of wafer manufacturing, ASML’s performance surging reflects the arms race occurring throughout the technology industry.

Among these, giants like Amazon, Google, and Microsoft have invested hundreds of billions of dollars in infrastructure, igniting enormous downstream demand for high-end AI chips, including logic and storage, pushing wafer fabs to accelerate expansion, making the demand for lithography machines heat up.

While delivering impressive second-quarter financial reports, ASML also significantly raised its full-year performance guidance for the second time this year, raising the forecast for total sales in 2026 to between 43 billion and 45 billion euros (approximately 49.1 billion to 51.4 billion dollars).

It is worth noting that ASML itself is also driving capacity expansion, planning based on approximately 65 low numerical aperture (Low NA) EUV capacity planning for 2026, to increase capacity by 30% in 2027, and is studying a further 30% capacity increase in 2028. At the same time, it plans based on approximately 130 immersion DUV capacity planning for 2026, to increase capacity by 30% in 2027, and is studying a further 30% capacity increase in 2028.

Driven by this, ASML has firmly established itself as the largest listed company by market value in Europe. Since 2026, ASML’s stock price has risen by more than 68%, doubling over the past 12 months.

Gross margin soars to 54% significantly raises revenue guidance

ASML key financial data

ASML achieved strong year-on-year and quarter-on-quarter growth in several key financial metrics in the second quarter, also exceeding Wall Street analysts’ forecasts.

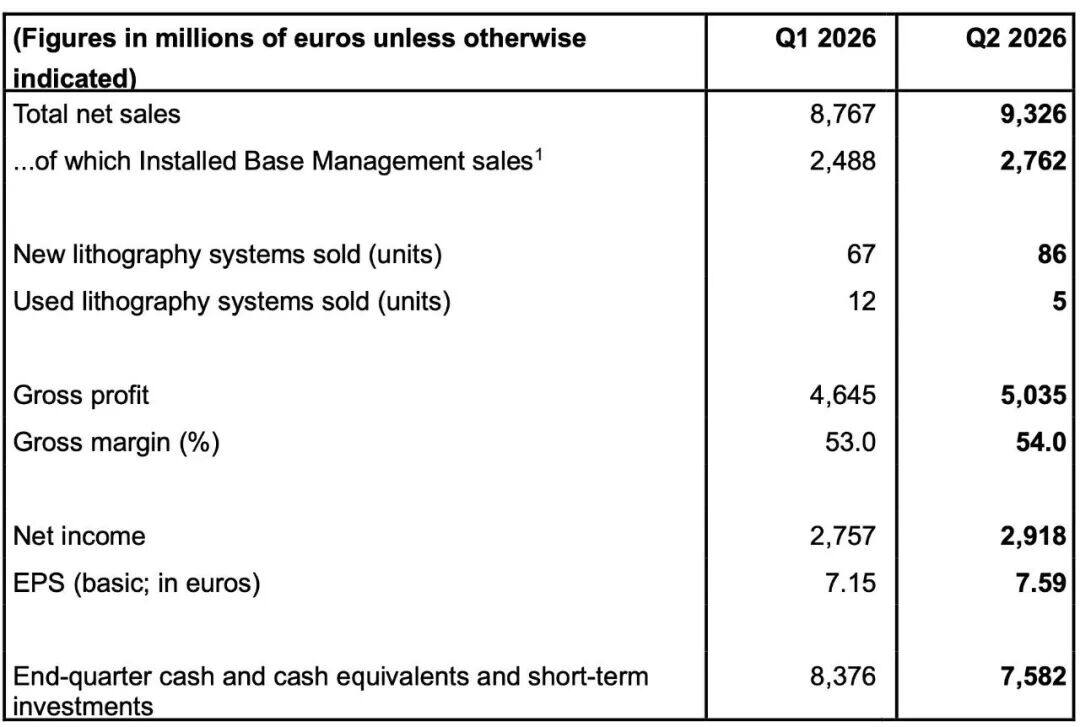

Total net sales in the second quarter reached 9.326 billion euros, continuing to grow compared to 8.767 billion euros in the first quarter; compared to 7.690 billion euros in the same period last year, it rose by 21.3%, significantly higher than the mean analyst forecast of 8.83 billion euros by Visible Alpha and the general expectation of 8.8 billion euros from LSEG.

By revenue composition, among the total net sales of 9.326 billion euros, the equipment segment accounted for 6.564 billion euros, while after-sales service was 2.762 billion euros.

This quarter's gross profit increased to 5.035 billion euros, with a gross margin reaching 54%, higher than the 53% in the first quarter, exceeding the company's own upper guidance limit. In terms of equipment delivery, ASML sold a total of 86 new lithography systems and 5 second-hand lithography systems in the second quarter, with new machine sales significantly increasing from 67 units in the first quarter.

"The net sales and gross margin exceeded expectations, primarily due to the after-sales service sales exceeding forecasts." said Peter Wennink, President and CEO of ASML.

Net profit also performed impressively. This quarter's net profit reached 2.918 billion euros, steadily increasing from 2.757 billion euros in the first quarter; compared to 2.290 billion euros in the same period last year, it surged by 27.5%, significantly surpassing the general market expectation of 2.6 billion euros.

Thanks to extremely strong order momentum in the first half of the year, ASML made the most aggressive forecast revision this year. The company raised its full-year total net sales forecast for 2026 from the previous quarter’s announcement of 36 billion-40 billion euros, to a significant adjustment of 43 billion-45 billion euros; at the same time, it raised full-year gross margin expectations from 51%-53% to 54%-56%.

This adjustment range is extremely rare in the semiconductor equipment industry and directly reflects the urgency of downstream customers’ orders. For the upcoming third quarter, ASML provided an extremely optimistic outlook, expecting quarterly sales to be between 11 billion to 12 billion euros, with gross margin further increasing to 55%-57%.

Storage, logic wafer fabs are in a frenzy

ASML business breakdown

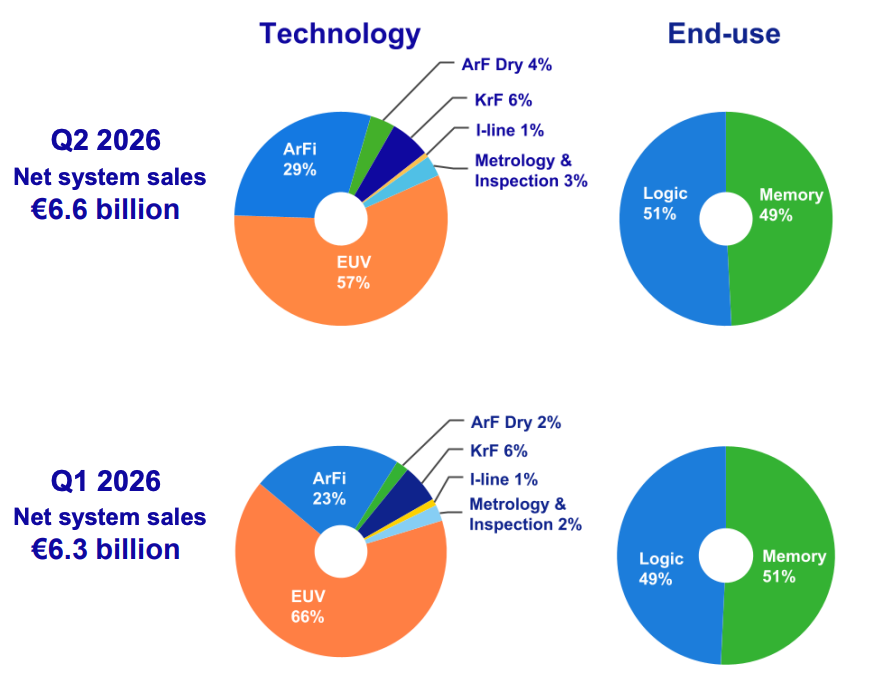

In the sales structure of net systems for the second quarter of 2026, logic chips reclaimed dominance, accounting for 51% of revenue compared to 49% for storage chips. In the prior first quarter, the order proportion from storage customers historically surpassed logic customers at 51%.

From a technical structure perspective, although the revenue contribution from EUV systems decreased from 66% in the first quarter to 57%, it still remains ASML's primary revenue pillar. In terms of shipment volume, ASML sold a total of 16 EUV systems in the second quarter, unchanged from the first quarter.

In contrast, ArFi (Immersion Deep Ultraviolet Lithography) systems welcomed a rebound in the second quarter, with revenue contribution increasing from 23% in the first quarter to 29%, and sales rising from 17 units in the first quarter to 23 units, indicating wafer fabs’ replenishment demand for deep ultraviolet equipment.

South Korea firmly retains its position as the “largest customer”

Due to the intertwining effects of export controls and the global factory construction boom, ASML's global shipment destinations saw noticeable adjustments in the second quarter.

For the past two consecutive quarters, South Korea has been the single largest market region, contributing 43% to ASML's revenue this quarter, indicating that storage giants represented by Samsung Electronics and SK Hynix maintain a high level of equipment procurement investment domestically in South Korea.

At the same time, the Taiwan market displayed a strong rebound, with its revenue contribution rising significantly from 23% in the first quarter to 30%. In contrast, the revenue contribution from the mainland Chinese market decreased from 19% in the first quarter to 14% in the second quarter. However, management anticipates that mainland China’s contribution to total revenue for the full year will remain around 20%.

"The incremental demand in the mainland Chinese market mainly comes from the logic chip sector, driven primarily by domestic demand." Dai Houjie stated that since ASML raised its overall revenue base for the year in the second quarter, it implies that, while the percentage remains unchanged, the absolute procurement value from the mainland Chinese market has indeed increased proportionally with the overall market.

Since ASML raised its overall revenue guidance for the year in the second quarter, it indicates that the absolute value of procurement in the mainland Chinese market is still steadily increasing.

Among other regions, the revenue contribution from the U.S. market this quarter was 9%, compared to 12% the previous quarter; the revenue proportion for the Japanese market was 4%.

EUV and DUV lithography machine capacity expansion by 30%

After the financial report, CEO Peter Wennink and CFO Dai Houjie deeply dissected the deeper industry logic and regional market trends behind the performance in a video interview.

Peter Wennink indicated that due to the ongoing supply constraints of DDR5 and HBM (High Bandwidth Memory), prices are rising, and major manufacturers are accelerating capacity expansion across the board. At the same time, the most advanced memory nodes have significantly higher requirements for lithography intensity (including low numerical aperture EUV and advanced immersion equipment), leading ASML to expect a massive 75% increase in revenue from storage customers in 2026.

Simultaneously, Wennink emphasized that driven by AI demand, major customers are beginning to push for advanced process expansion, and logic chips are also performing strongly, with revenue from advanced foundry logic business expected to grow by about 25% in 2026.

Faced with unprecedented order pressure, Wennink revealed that ASML plans to ship about 65 low numerical aperture EUV devices in 2026, aiming for a 45% increase in EUV business revenue for the year; simultaneously, shipments of immersion systems are expected to reach 130 units.

"We plan to increase EUV capacity by 30% in 2027 based on 2026 levels. Looking ahead to 2028, we have already received a large number of EUV orders from customers, which also prompts us to seriously assess the possibility of further increasing EUV capacity by 30% in 2028. As EUV orders grow, DUV will also grow, with immersion DUV continuing to play an important role. We plan to increase its capacity by 30% in 2027, and we are evaluating the possibility of further increasing capacity by 30% in 2028." said Wennink.

Regarding the outstanding performance of the installed base management (mainly referring to after-sales services and hardware and software on-site upgrades), CFO Dai Houjie emphasized that this is an increment segment that the market has not fully recognized. This business generated revenue of 2.762 billion euros in the second quarter, with a quarter-on-quarter growth of 11%, exceeding the company's previous expectations by a full 300 million euros.

Dai explained that in the current environment of extreme capacity strain, customers are accelerating the procurement of ASML's upgrade solutions to raise production line efficiency in the shortest time possible.

Since many upgrades are software-driven and do not require physical equipment downtime or occupy too much machine modification time, customers can immediately gain productivity improvements after installation. As the scale of EUV installations continues to expand, the corresponding installed base management business scale is also continually expanding, this high-margin business is expected to achieve over 30% growth in 2026, becoming a significant contributor to the company’s overall profit margin.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。