TL;DR

- TSMC's Q2 2026 revenue is approximately NT$1.27 trillion, with a year-on-year increase of 67.9% in June, and AI demand continues to materialize.

- Bernstein maintains a target price of NT$2,780, betting on high capital expenditures translating into more AI capacity.

- High valuations require gross margins to keep up; clients seeking second sources and geopolitical risks will continue to suppress upward space.

TSMC's second-quarter revenue is about NT$1.27 trillion, with a quarter-on-quarter growth of approximately 12% and a year-on-year growth of about 36%, falling within the range of the company's previous dollar revenue guidance, and close to the upper middle segment. TSMC's official website indicates that the revenue for June alone is NT$442.68 billion, a month-on-month growth of 6.2% and a year-on-year increase of 67.9%.

This set of data reinforces the market's bets in one direction: demand for AI chips, advanced processes, and advanced packaging continues to outpace supply. Bernstein has recently maintained an Outperform rating for TSMC, and set a target price of NT$2,780. Compared to the closing price of NT$2,440 on July 13, this target price still leaves room for upward movement, but investors are now more concerned about capacity, gross margins, and the ramp-up of the N2 process rather than just quarterly revenue.

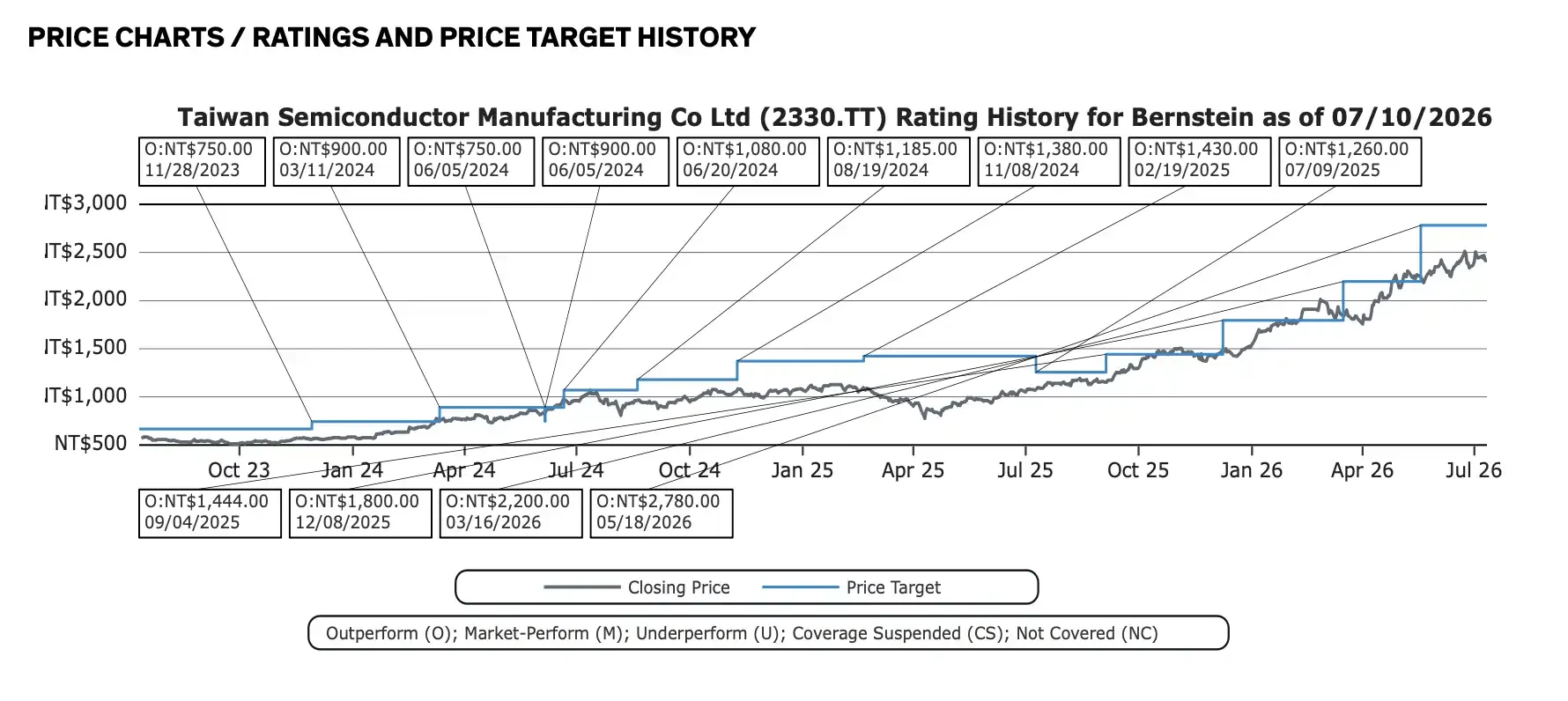

Bernstein continuously raises TSMC's target price

TSMC will hold a Q2 earnings presentation on July 16. With Q2 revenue already disclosed, the suspense shifts to how management will update annual demand, advanced packaging capacity expansion, capital expenditures for 2026 to 2027, and whether high levels of investment will start to pressure gross margins.

Q2 revenue close to upper guidance range, June year-on-year growth nearly 68%

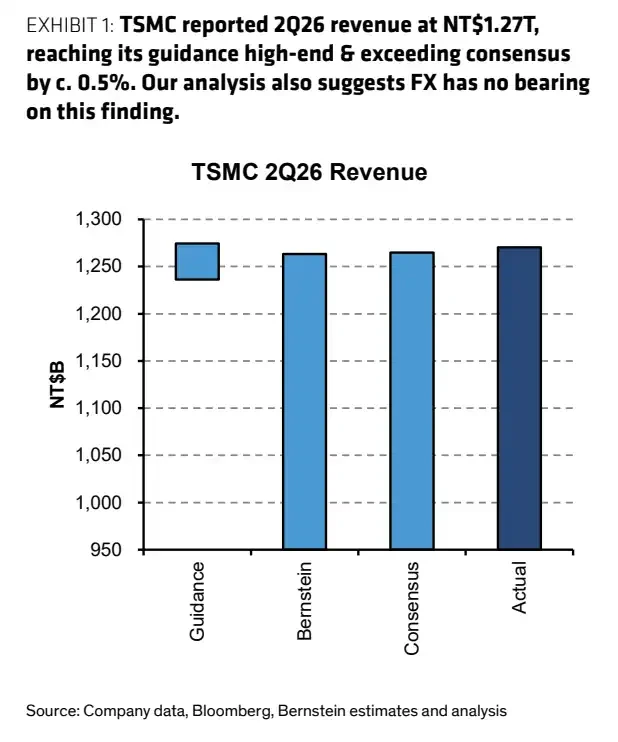

The revenue of NT$1.27 trillion in Q2 is the most direct figure in this report. The company previously provided guidance for Q2 dollar revenue in the range of US$39 billion to US$40.2 billion, with an exchange rate assumption of 31.7. According to this calculation, Q2 revenue is about US$39.6 billion, which is within the guidance range and close to the upper middle segment.

The revenue for June alone was NT$442.68 billion, continuing to rise from May's NT$416.97 billion. The total revenue for the first half of the year is NT$2.404 trillion, a year-on-year increase of 35.6%. This indicates that orders for advanced processes and AI-related demand are still being converted into actual revenue, rather than remaining solely within capital market expectations.

Q2 2026 revenue comparison bar chart, actual revenue approximately NT$1.27 trillion, higher than some market estimates and falling within the company's guidance range.

Gross margin is another key factor. The source report estimates the gross margin for Q2 to be approximately 65%, but TSMC's previous official guidance was 65.5% to 67.5%. Prior to the official earnings release, the more cautious statement is that the market still expects TSMC's gross margin to remain high, but the final numbers will be confirmed with the earnings report on July 16.

For wafer foundries, whether they can maintain high gross margins depends on the proportion of advanced processes, capacity utilization, depreciation pressure, and customer bargaining power. TSMC's current advantage lies in the fact that AI and high-performance computing demand are still helping it absorb higher capital expenditures.

US$56 billion capital expenditure for AI capacity

Whether TSMC's valuation can continue to hold is not only determined by how much Q2 revenue exceeds expectations, but also by its ability to turn AI demand into deliverable capacity.

Bernstein's model estimates that TSMC's capital expenditure will be US$56 billion in 2026, increasing further to US$68 billion in 2027. This scale reflects two layers of pressure: the continued increase in demand for advanced processes and the bottleneck of advanced packaging capacity for AI chip deliveries.

According to the source report's standards, CoWoS capacity is expected to reach 135,000 pieces per month by the end of 2026 and 195,000 pieces per month by the end of 2027. For Nvidia, AMD, and large cloud vendors' self-developed AI chips, advanced packaging capacity directly affects whether chips can be delivered on time. After wafer manufacturing is completed, if the packaging process cannot keep up, final shipments will still be constrained.

This is also the reason why the market will keep a close eye on TSMC's capital expenditure guidance. High capital expenditures indicate strong demand but also bring rising depreciation and cash flow pressure. As long as customers are willing to lock in capacity and advanced process prices can be sustained, high investment is seen as a growth investment. If AI demand slows, high investment could inversely squeeze profit margins.

The N2 process will also be a focal point of the earnings report. TSMC's leading position in advanced processes remains its main moat distinguishing it from other foundries. The market wants to confirm whether the N2 ramp-up is proceeding as planned, whether customer integration is smooth, and whether cost pressures from the new process can be offset by prices and scale.

Target price of NT$2,780 is not low, and stock price has already priced in AI

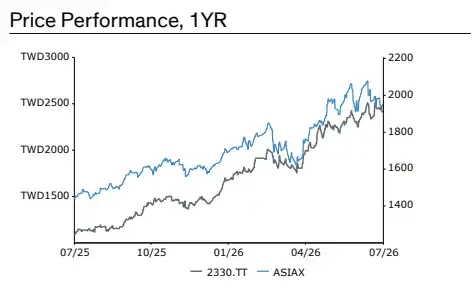

As of July 13, 2026, TSMC's stock closing price was NT$2,440. Bernstein's target price of NT$2,780 is based on about 20 times one-year forward earnings valuation, still corresponding to some upward space.

However, this is no longer a story of undervalued reversal. According to the source report standards, the current stock price corresponds to about 21 times forward earnings. The market has already priced in high amounts for AI demand, advanced process leadership, and high gross margins.

TSMC's stock price has consistently risen over the past year, currently around NT$2,440, with a TTM relative performance of 86.5%.

Future stock price will depend more on performance realization. As long as revenue, gross margin, and capacity expansion continue to exceed expectations, the high valuation can be absorbed by profit growth. Once capital expenditures keep rising but profit margins begin to loosen, investor tolerance for the current valuation will decrease.

Over the past 12 months, TSMC's relative performance reached 86.5%. The market has viewed it as one of the core beneficiaries in the expansion of AI infrastructure. The more core the asset, the more likely it is to endure valuation pressure when expectations cool slightly.

Second sourcing is heating up, but temporarily difficult to replace TSMC

The competitive risks currently do not stem from TSMC's leading position being undermined, but from clients beginning to seek more options amidst tight capacity.

Recently, it has been reported that Samsung has raised prices by about 15% for some new customers at the 4/5nm and 8nm nodes, and is discussing a 2nm AI chip project with Anthropic and Meta. Intel has also drawn market attention regarding its potential involvement in Google TPU-related supplies, but existing discussions point more towards advanced packaging or EMIB stages, and cannot simply be equated with wafer foundry orders.

These news items are unlikely to have a substantial impact on TSMC's revenue in the short term. TSMC still has significant advantages in leading process yields, scale, and customer base. The real signal is that when the supply of advanced processes and advanced packaging is chronically tight, major customers will be more proactive in seeking a second source of supply.

Even if alternative solutions have limited short-term capacity and long technical validation cycles, they may weaken TSMC's bargaining flexibility in the medium to long term. Geopolitical uncertainties and client concerns over overly concentrated supplies will also ensure that diversification demand continues to exist.

For TSMC at the current valuation level, these risks do not need to immediately impact revenue. As long as they affect the valuation multiples that investors are willing to assign, that is enough to cause stock price fluctuations. The questions that need to be answered at the earnings presentation on July 16 are also very specific: how quickly will advanced packaging expand, will the ramp-up of N2 pressure gross margins, and can high capital expenditures continue to be absorbed by AI orders? TSMC remains one of the strongest companies in the AI manufacturing chain, but to realize the target price of NT$2,780, more capacity and profit margin data needs to keep pace.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。