TL;DR

- Morgan Stanley expects the AI scaled network opportunity to be about $70 billion by 2030, expanding more than four times compared to last year's estimate.

- From 2026 to 2027, the scaled network will still primarily use copper cables, and CPO may only achieve a 20%-30% penetration by 2029-2030.

- Keysight Technologies, Astera, Broadcom, and Semtech will benefit first, while Corning, Lumentum, and Coherent are more likely to benefit later.

Morgan Stanley's latest report estimates the AI scaled network market opportunity in 2030 at around $70 billion and brings the lifecycle of copper cables in AI clusters back into focus.

This is not a story of "CPO exploding immediately." AI clusters are transitioning from single rack to multi-rack, necessitating denser and faster connections between GPUs, which in turn enlarges the overall pie of the back-end network. However, before power consumption, distance, and bandwidth density really approach their limits, short-distance connections still exhibit strong inertia for copper cables.

This report offers a restrained timeline: in 2026-2027, the CPO penetration rate in scaled networks will be close to zero; slight introductions will begin in 2028; and by 2029-2030, it may reach a meaningful level of 20%-30%. The market opportunity has been significantly raised, but for optics to genuinely capture the lion's share of the scaled network, a larger GPU domain and more mature supply chain need to be in place simultaneously.

$70 Billion Opportunity Comes from Multi-Rack; It’s Not Optical Modules That Expand First

The core of this upgrade is the clear increase in connection demand between servers and racks following the expansion of AI clusters.

In traditional single rack scenarios, the distances between GPUs are relatively short, and copper cables still have advantages in cost, latency, and power consumption. For short-distance connections, especially within 7-9 meters, copper cables remain the most straightforward solution. In recent years, stronger SerDes, retimer, PAM4/PAM6, and other technologies have continually extended the lifespan of copper cables and repeatedly delayed the timeline for optical alternatives.

Changes occur as clusters continue to grow. Training and inference clusters expand from a single rack to multiple racks, requiring inter-rack communication between GPUs, with signal speeds advancing from 100G to 200G and 400G. As distances increase and speeds rise, electrical loss, insertion loss, and noise management difficulty also rise, bringing copper cables closer to performance boundaries.

2024-2030 Back-end Network Revenue Forecast; Scaled Network Revenue Rises Rapidly, with a Market Opportunity of Approximately $70 Billion in 2030.

For investors, this determines the order of beneficiaries. Those benefiting first will not necessarily be CPO suppliers but rather chip and module companies that enable copper cables to continue running faster and farther; as multi-rack clusters become more widespread, the elasticity of optical engines, passive optics, lasers, and testing equipment will become more apparent.

2026-2027 is Still the Copper Cable Window; CPO Will Not Explode Until After 2029

The appeal of CPO lies in bringing optical components closer to switching chips or computation chips, reducing the transmission distance of high-speed electrical signals on the board, thereby improving power consumption and bandwidth density. The challenge is that it’s not just about changing a wire, but rather altering encapsulation, manufacturing, testing, maintenance, and the division of supply chain responsibilities.

This is also why CPO will not explode fully in 2026. The CPO penetration rate in scaled networks will be close to zero in 2026-2027, with slight introductions starting in 2028; truly meaningful adoption is not expected until 2029-2030. At that time, if the multi-rack GPU domains expand as planned, CPO's penetration rate in scaled networks could reach 20%-30%.

CPO Penetration Rate Forecast by Scale; Scaled CPO Will Only Rise to 20%-30% by 2029-2030.

This leaves at least a two-year window for the copper cable chain. Astera Labs' Scorpio X-Series has already entered initial mass production, Broadcom has connection opportunities in the AMD MI400/Helios ecosystem and customized ASICs, while Semtech is participating in the transition phase through its low-power copper cable and linear optical solutions.

More importantly, copper cables and optics do not exist in a simple replacement relationship. Large cloud vendors will mix DAC, ACC, AEC, AOC, NPO, and CPO based on distance, power consumption, cost, maintainability, and reliability. Short-distance, intra-rack, and near-rack connections will still retain a significant amount of copper cables, while CPO will take on more high-density, long-distance, and higher power consumption sections.

NVIDIA Roadmap Boosts Optical Demand, but the Pace Depends on Platform Implementation

CPO becomes truly significant in direct relation to NVIDIA's next-generation AI platform roadmap.

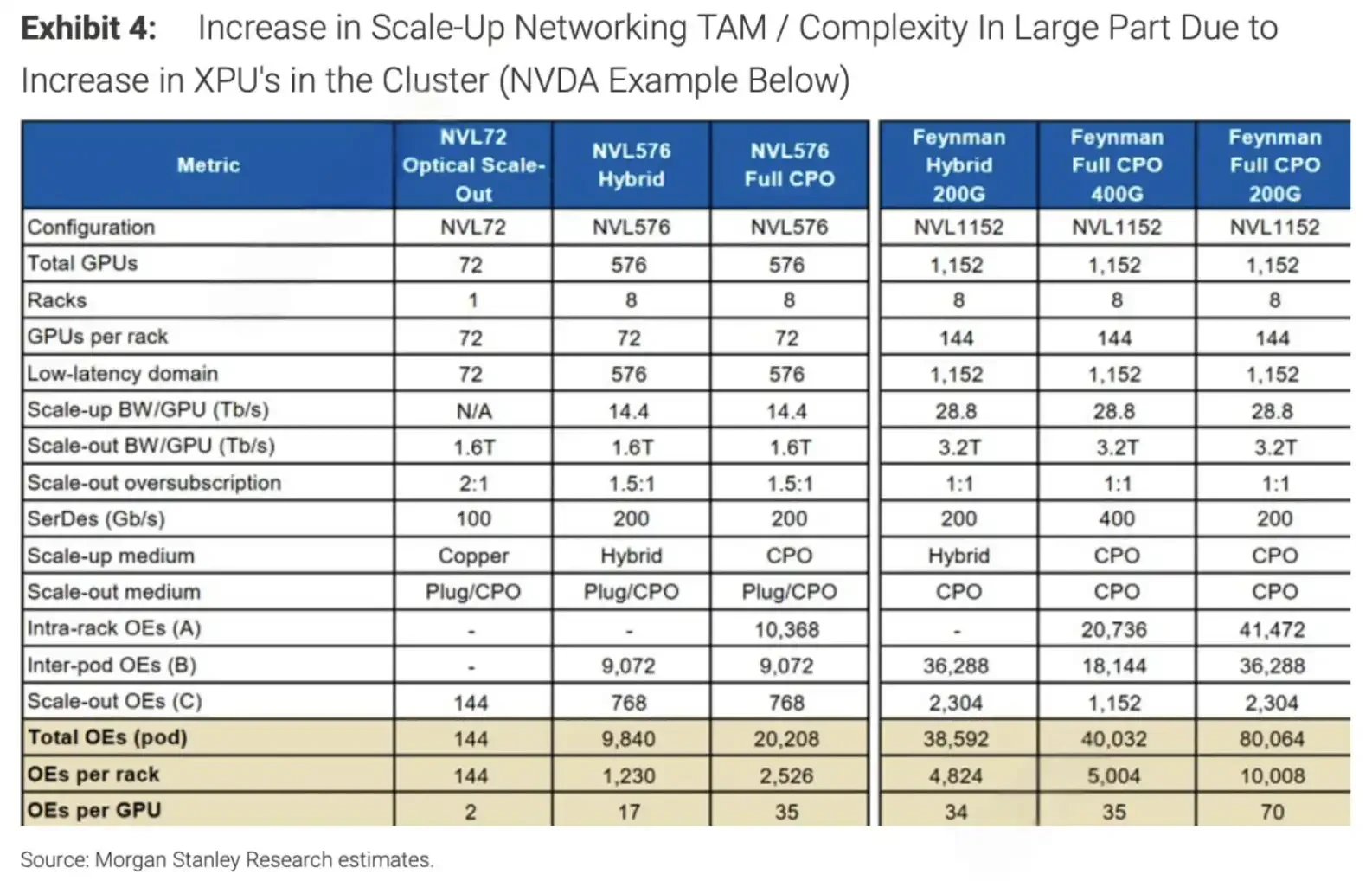

NVIDIA's official technology blog shows that Vera Rubin Ultra NVL576 will form a 576-GPU NVLink domain composed of eight 72-GPU racks, using copper cables and direct optical connections; the Feynman Era's Kyber NVL1152 is targeted towards larger-scale interconnections, also using a direct optical solution.

As the GPU domain expands, the demand for optical engines will not simply increase linearly. In this report’s estimation, the number of optical engines per GPU may rise from the current two to a range of 35-70. This means that once architectural transitions occur, the volume of optical content will increase significantly.

Comparison of XPU Cluster Size and OE Demand; GPU Domain Expands from 72 to 576/1152, with the Number of OE per GPU Rising from 2 to 17-70.

This is also why Corning (GLW), Lumentum (LITE), and Coherent (COHR) have been included in this main storyline. Corning benefits from passive optics and glass-related content, while Lumentum and Coherent are more related to lasers, optical engines, and optical components. After integrating scaled CPO adoption rates into their models, the profitability elasticity of related companies depends increasingly on the pace of adoption.

However, this remains the elasticity of "if adoption occurs," rather than realized revenue. There are market divergences regarding NVIDIA's roadmap; some industry analysts suggest that certain configurations of Kyber or Rubin Ultra may be delayed, while NVIDIA has responded that the roadmap remains unchanged. For the optical chain, the key is not the name of a single product generation, but whether the large GPU domain enters mass production as planned and whether non-NVIDIA XPU ecosystems adopt similar connection paths.

Keysight Technologies Is More Like a "Shovel Seller," Testing Equipment Doesn’t Rely on Orders

In this main storyline, the logic of Keysight Technologies (KEYS) differs from that of optical module companies. It doesn’t need to bet on whether copper cables or CPO will ultimately win since the more AI network architectures there are, the higher the demand for testing and verification.

Currently, the AI back-end network has not unified into a single standard. NVIDIA has NVLink and subsequent expansion routes, while non-NVIDIA camps have UALink, SUE, PCIe, and different cloud vendors' proprietary interconnection solutions. Each architecture requires testing for signal integrity, error rate, interoperability, power consumption, and reliability.

According to Investing.com, Morgan Stanley has upgraded Keysight Technology’s rating from Equal Weight to Overweight, raising the target price from $350 to $400, citing reasons such as AI investment, network architecture diversification, and the enhanced demand for 800G, 1.6T, and 3.2T testing. AI-related revenue from Keysight is estimated to account for the mid-teens percentage of total revenue.

In contrast, the elasticity of optical device companies is more concentrated on CPO adoption rates and specific platform rhythms. If NVIDIA's roadmap progresses smoothly, Corning, Lumentum, and Coherent would benefit more directly; if copper cables continue to extend their lifespan in 2026-2027, Astera, Broadcom, and Semtech's short-term certainty may actually be higher.

CPO Will Eventually Enter a Core Position, But Cloud Vendors Are Not Ready to Move All at Once

The report's counterintuitive aspect is that it simultaneously recognizes CPO will eventually move into a core position while emphasizing that short-term copper cables should not be underestimated.

CPO faces significant obstacles. Large cloud vendors are concerned about vendor lock-in; once optical components are deeply integrated into switching or computing packages, subsequent replacement, maintenance, and multi-vendor procurement become more complex. Manufacturing yield, thermal management, maintainability, and quality risks will also impact the speed of adoption. If cost premiums cannot be offset by power savings and bandwidth density improvements, adoption will be delayed.

There are also architectural divergences. NVIDIA's roadmap might drive a higher proportion of optical connections, but self-developed architectures like Google TPU adopt different topologies, potentially reducing reliance on traditional CPO solutions. While the non-NVIDIA XPU ecosystem creates opportunities for companies like Broadcom and Astera, lack of unified standards also means the supply chain cannot scale swiftly under a single solution.

Thus, the revision of the $70 billion market appears more as an enlargement of the overall AI back-end network pie rather than a single technology route having secured victory. In 2026-2027, copper cables will still dominate in intra-rack and short-distance scenarios; after 2028, optics will start to enter a more central position; and by 2029-2030, CPO may finally achieve genuinely meaningful penetration in scaled networks. The most common misconception in the market is equating "CPO will eventually come" directly with "CPO will explode immediately."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。