Data Description: BTC adopts a spot price of approximately $60,005 as of June 28. The company's holdings and equity use the latest SEC disclosures submitted by Strive as of June 18 and June 22. Market prices do not completely synchronize with company disclosure times; the calculations involving coverage in the text are snapshot estimates.

1. Summary

On June 16, Strive changed the dividend frequency of SATA from monthly to every business day.

Strive claims it is the first security traded in the US market to pay dividends on a business day basis. SATA currently has an annualized dividend yield of 13%; by July 2026, it has declared a daily dividend of $0.0493 per share over 22 business days, totaling $1.0846 per month.

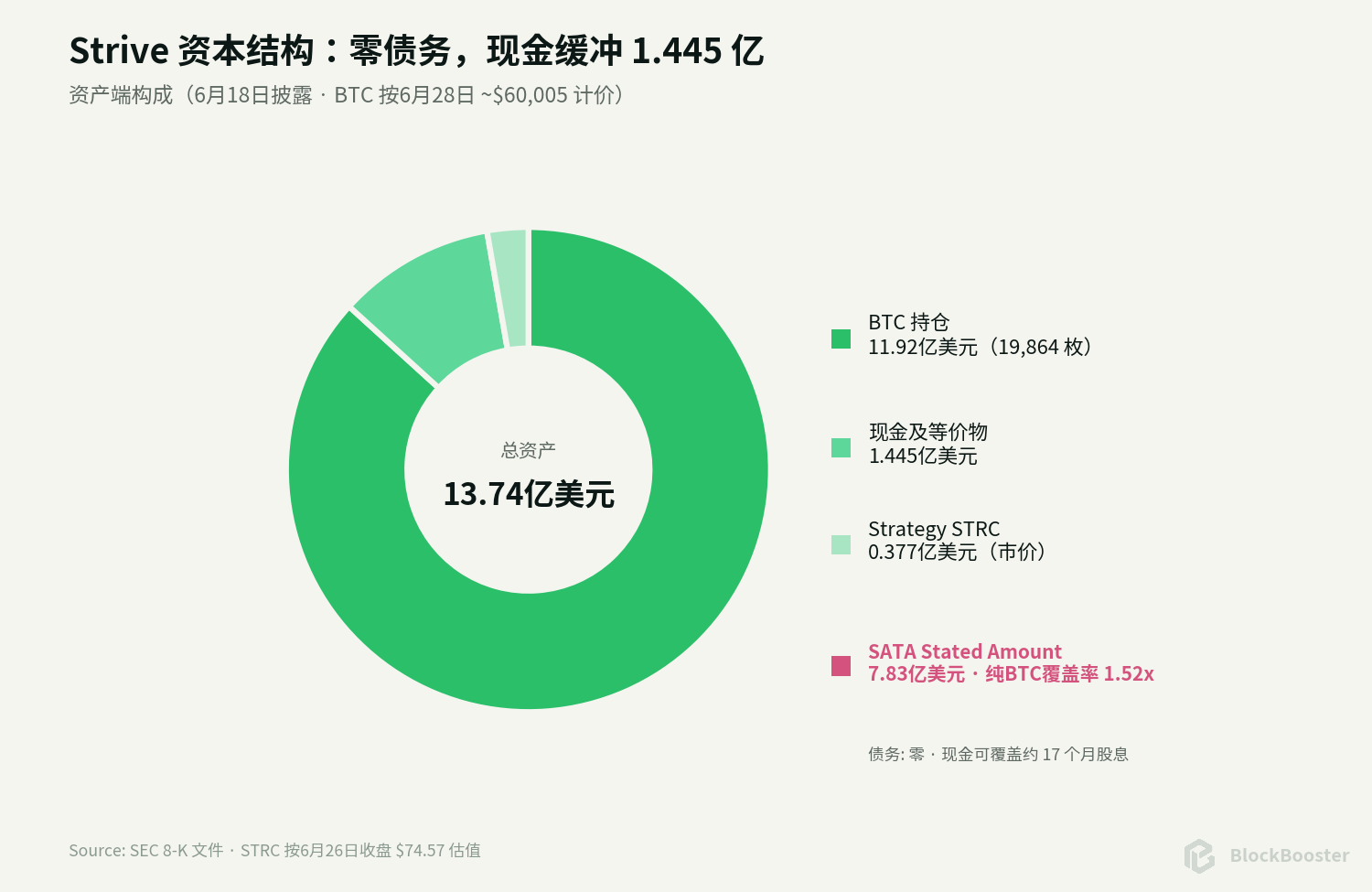

As of June 18, Strive holds 19,864 BTC, $144.5 million in cash, and 505,000 shares of Strategy's STRC preferred stock; SATA has issued 7,829,502 shares, with a stated amount of $100 per share, resulting in a preferred stock principal of approximately $783 million. Based on BTC's price of approximately $60,005 on June 28, the value of the BTC holdings is approximately $1.192 billion.

The conclusions of this article are as follows:

First, SATA is a class of corporate preferred equity that has no maturity date, can defer dividends, but will accrue them. SATA has priority over common stock in the order of settlement, but still ranks below the company's creditors and does not have a direct lien on a specific batch of BTC. From a legal structure perspective, it bears the risk of Strive's credit + BTC balance sheet risk.

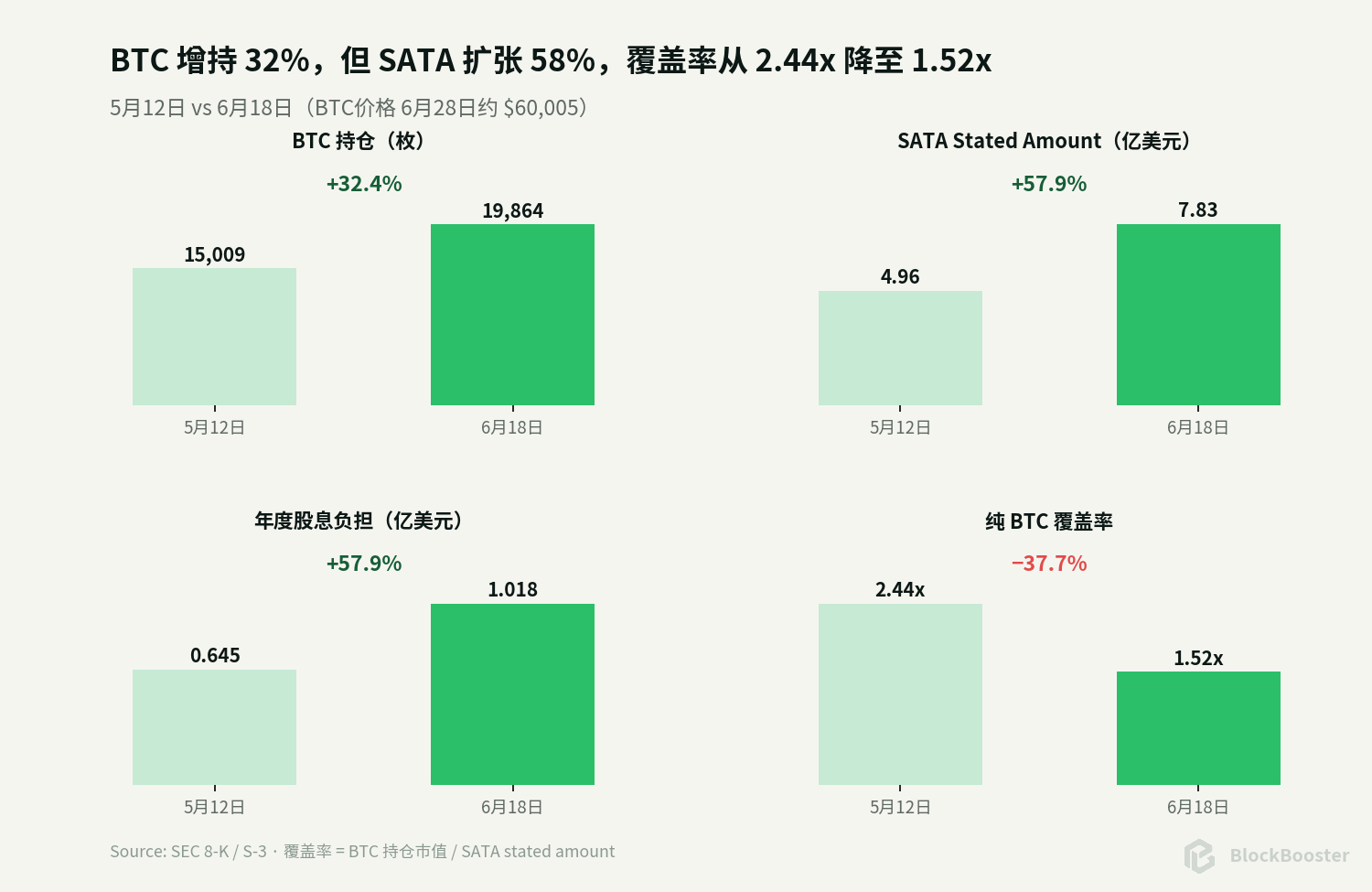

Second, Strive's BTC quantity continues to grow, but SATA is expanding faster, and the coverage has significantly compressed since May. From May 12 to June 18, BTC holdings increased from 15,009 to 19,864, a growth of about 32.4%; meanwhile, SATA shares increased from 4,959,500 shares to 7,829,502 shares, a growth of approximately 57.9%. During the same period, BTC dropped from approximately $80,624 to around $60,005. As a result, the coverage ratio of pure BTC to SATA's stated amount fell from about 2.44 times to about 1.52 times. If BTC drops further by about 34.3% to around $39,416, the pure BTC coverage ratio will fall to 1 time.

Third, there is a thick cash buffer, but it cannot be mixed with collateral. Strive's latest cash disclosure is $144.5 million; based on STRC's closing price of $74.57 on June 26, the value of 505,000 shares of STRC is approximately $37.66 million. The coverage ratio of liquid assets to SATA's stated amount is approximately 1.76 times.

Fourth, SATA has been re-priced in the secondary market. SATA closed at $87.75 on June 26, a discount of 12.25% from the $100 stated amount, resulting in a static current yield of approximately 14.81% based on the $13 annual dividend. Using the latest SOFR at approximately 3.64% as a benchmark, the market current yield spread of SATA is about 1,117 basis points.

Fifth, daily dividends improve the granularity of cash flows, not the stability of principal. SATA fell from $97.38 on June 22 to $87.75 on June 26, a decline of about 9.9% over four trading days. A single price drop negated about nine months of the stated dividend. Daily dividends can attenuate gaps and dividend capture trading around monthly ex-dividend dates but cannot convert perpetual preferred shares into money market funds.

Therefore, the most noteworthy aspect of SATA is not "13% credited daily," but that it slices the balance sheet of a BTC treasury company into two layers: common shareholders absorb remaining volatility, while preferred shareholders receive priority cash flows while bearing risks related to company credit, perpetual duration, financing channels, and BTC valuations.

2. Background

2.1 Latest Capital Structure

Strive has acquired more BTC, but has not increased the dollar value of BTC assets; meanwhile, the principal of preferred stock and annual dividend burdens have risen rapidly.

From May 12 to the present, the number of BTC has increased by about 4,855, but the price has dropped by about a quarter, offsetting the quantity increase. The dollar value of the BTC holdings has decreased from approximately $1.21 billion to about $1.192 billion; however, the SATA stated amount has increased from about $496 million to approximately $783 million. This is indeed the reason the coverage ratio compressed from 2.44 times to 1.52 times.

2.2 What Dividends Depend On

The current annual cash dividend burden for SATA is approximately: $783.95 million × 13% ≈ $101.8 million/year

Strive pays SATA dividends primarily relying on the following sources:

- Cash raised from SATA or common stock ATM issuance;

- Existing cash reserves;

- Sale or liquidation of other securities;

- Sale of BTC if necessary;

- Future operational income or other financing that may arise.

Therefore, SATA is a cash flow commitment highly sensitive to the continuous openness of capital markets. When the market is willing to accept new shares at a price close to or above $100, Strive can expand its BTC reserves and maintain dividends through financing; when SATA trades significantly below $100, the economics of new financing become noticeably worse.

For example, at the current price of $87.75, if the company issues a share of SATA near this price, it would only generate approximately $87.75 in gross income, yet it would add $100 in stated amount while assuming an annual dividend burden of $13. Simply calculated based on proceeds, the financing cash cost would be approximately: $13 ÷ $87.75 ≈ 14.81%

If the funds raised are primarily used to buy BTC, for every additional $87.75 of assets, there corresponds $100 of preferred stock stated amount, and the pure asset coverage ratio will suffer dilution. Continuing aggressive ATM issuance in this scenario would only be rational if management believes that future BTC returns, common stock financing, or market price recovery will sufficiently compensate for structural deterioration.

2.3 Cash Coverage Duration

Based on $144.5 million in cash and the annual SATA dividend burden of approximately $101.8 million, looking solely at dividends and completely ignoring operating expenses and new issuances, cash could cover approximately 17.0 months.

If the STRC valued at approximately $37.66 million at current market price is also included, the dividend coverage time can increase further. However, this number does not indicate "how long the company can survive":

- The company still has employee, listing, audit, legal, and transaction costs;

- Continued issuance of SATA will increase annual dividend burdens;

- STRC may depreciate synchronously during BTC declines and credit tightening;

- Cash is not specifically placed in custody for SATA holders;

- Management may use funds to continue buying BTC or pursue other corporate purposes.

Cash buffers do reduce the short-term probability of being forced to sell BTC but cannot eliminate financing dependence.

3. What SATA's Daily Dividends Changed

3.1 Actual Daily Amount

The formal declaration for July 2026 is:

- Each business day per share $0.0493;

- A total of 22 business days;

- Monthly total of $1.0846 per share.

Based on the current 7,829,502 shares, if the number of shares remains unchanged throughout the month, the cash dividend for July would be approximately $8.49 million.

3.2 It Truly Reduced Calendar Trading of Dividends

Traditional monthly or quarterly preferred stocks accumulate accrued dividends before the ex-dividend date and produce visible price adjustments on the ex-dividend date. Dividing a month's cash into daily payments can:

- Lower the single ex-dividend amount;

- Reduce dividend capture trading around a single ex-dividend date;

- Smooth out cash flow return;

- Facilitate holders who wish to reinvest or pay expenses frequently.

This is SATA's true product innovation.

3.3 However, Daily Dividends Did Not Eliminate Price Risk

SATA closed at approximately $97.38 on June 22 and at $87.75 on June 26, a decline of about 9.9% over four trading days, resulting in a loss of $9.63 per share. Calculating with the annual dividend of $13, this is equivalent to approximately 8.9 months of stated dividends.

During the same period, STRC dropped from approximately $88.79 to $74.57, a decline of about 16.0%. The smaller relative decline of SATA indicates that its higher coupon, cleaner balance sheet, and product novelty may still command some premium.

Daily dividends smooth out cash flow but do not smooth out credit prices.

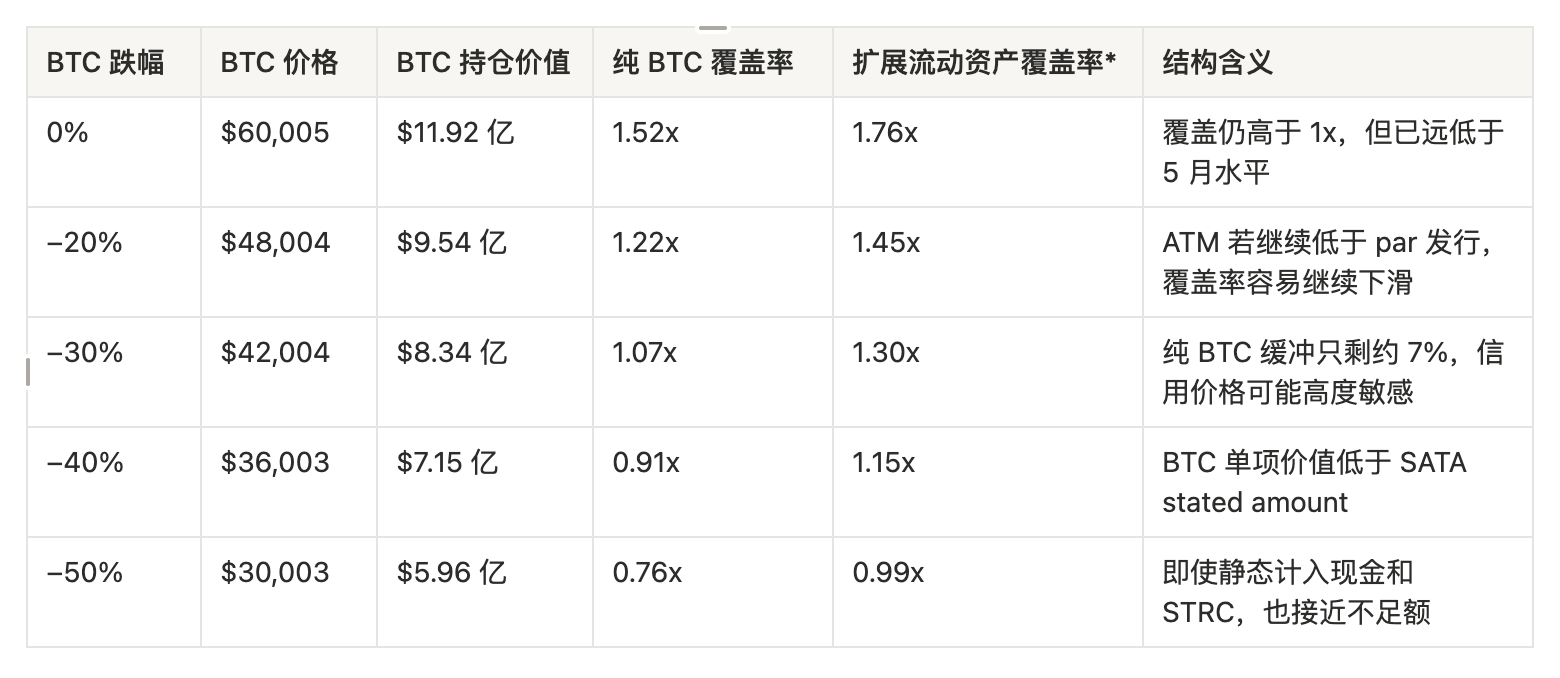

4. How BTC Price Changes Impact Margin of Safety

The following stress tests use the current snapshot as a starting point:

- BTC: 19,864;

- Current BTC price: approximately $60,005;

- SATA stated amount: approximately $783.95 million;

- Cash: $144.5 million;

- STRC holdings at current market price: approximately $37.66 million.

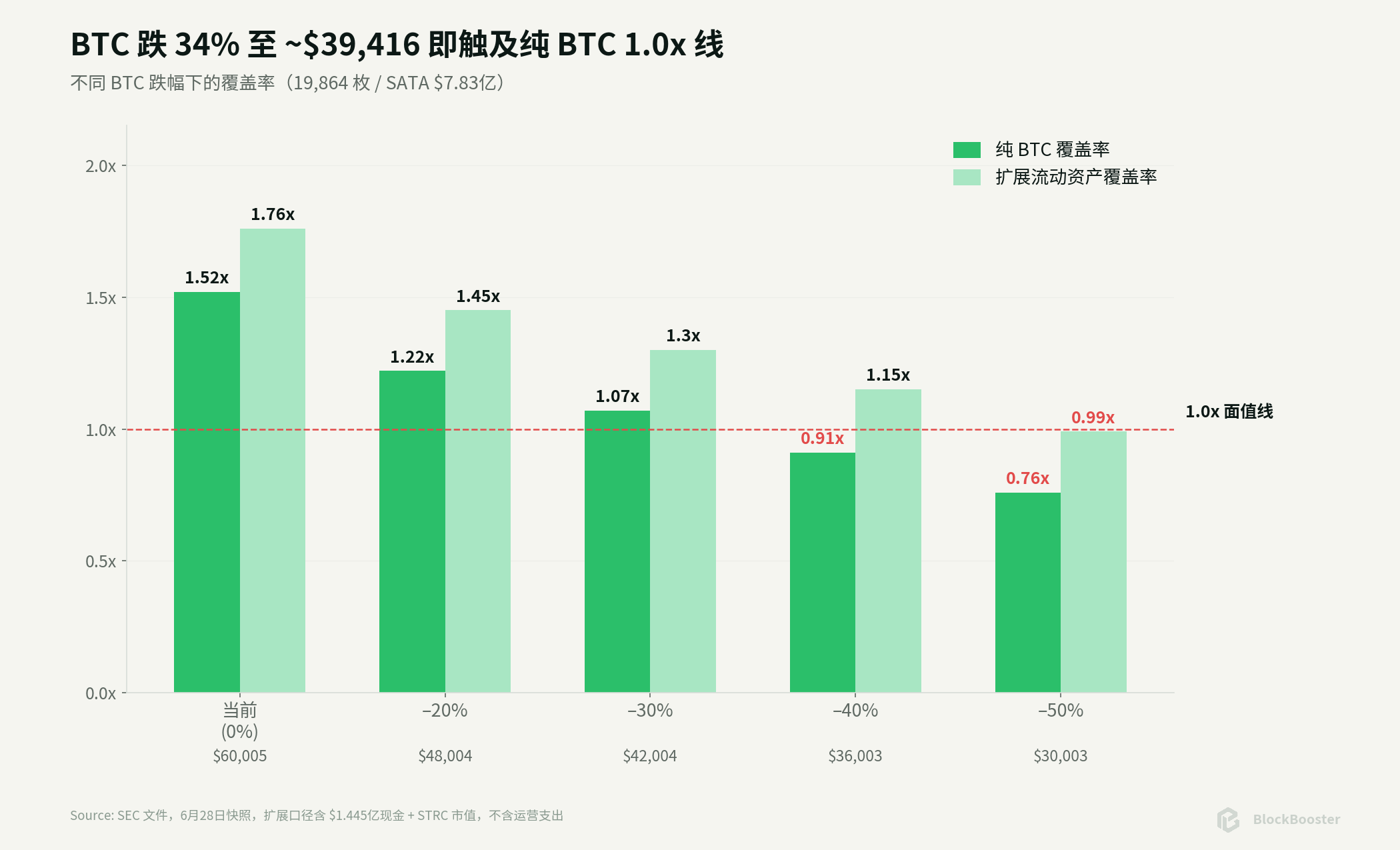

The "pure BTC coverage ratio" only compares the value of BTC to the SATA stated amount; the "expanded liquid asset coverage ratio" mechanically adds cash and current market value of STRC without representing legal collateral, and assumes STRC does not drop with BTC.

*The expanded metric assumes cash and STRC value remain unchanged, which is overly optimistic in reality amidst a sharp BTC decline.

The price at which the pure BTC coverage ratio drops to 1.0x is approximately:

$783.95 million ÷ 19,864 ≈ $39,416/BTC

Relative to the current approximately $60,005, a drop of about 34.3% indicates that 1.52 times cannot be seen as a solid margin of safety.

But it cannot simply be stated that if BTC drops to $39,416, SATA will "default." SATA is a preferred stock rather than a bond with a maturity date; the company still possesses cash, other assets, financing capabilities, and the option to adjust capital allocation. More likely scenarios include:

- SATA's market price sharply declines ahead of time;

- ATM issuance efficiency declines;

- Management raises the coupon to stabilize prices, which in turn increases cash burdens;

- The company reduces BTC purchases, sells other assets or BTC;

- In extreme cases, defer dividends.

Credit deterioration is a continuous process and not a mechanical default triggered by a single price line.

5. Key Risks

5.1 Reflexivity Below Par in ATM Issuance

When SATA is above or close to $100, new issuances can raise funds relatively efficiently; when SATA falls to $87.75, continued issuance would exchange cash at a price lower than the stated amount for a higher preferred stock principal and dividend burden.

The negative feedback loop may be: SATA declines → financing costs rise → cash raised per share decreases → coverage deteriorates → market demands a higher yield → SATA continues to decline.

The company can pause or slow down ATM issuances to prevent mechanical dilution, but the cost is a slowdown in BTC purchases, weaker narratives in capital markets, and increased reliance on existing cash.

5.2 Cash Flow and Financing Channel Risks

Current cash is sufficient to cover approximately 17 months of static dividends, but this measure excludes operating costs and potential future issuances of SATA. If capital markets close, the company must ultimately choose between reducing BTC purchases, selling securities, selling BTC, or deferring dividends.

5.3 Governance of Dividend Rates and Cash Cost Stickiness

The board can adjust the coupon monthly, but the current low price limits the downward adjustment space. The weaker the price, the more the market hopes for higher yields; the higher the coupon, the greater the company's cash burden. This is an endogenous credit reflexivity.

5.4 Preferred Stock is Not a Bond

Deferred accrued dividends protect holders, but suspending dividends does not equate to bond default. Investors may not receive timely cash and may not possess recourse as creditors. In liquidation, obligations to creditors and other senior claims must still be satisfied first.

6. Relative Value

6.1 SATA vs. STRC: Which is Cheaper

Current static current yields:

- SATA: approximately 14.81%;

- STRC: approximately 15.42%.

This price difference needs to be viewed alongside the following factors:

- Strategy has a larger size, deeper financing channels, and higher dollar reserves;

- However, Strategy has about $6.7 billion in convertible bonds and approximately $15.5 billion in preferred stock nominal size, leading to a more complex capital structure;

- Strive's latest full disclosure shows no debt, but the company has a short history, small size, and weak liquidity;

- SATA has a higher coupon and pays dividends daily, but the coverage is rapidly declining;

- Both have perpetual durations, issuer call rights, and BTC tail risks.

Therefore, it cannot be asserted that SATA is superior to STRC simply because of "Strive's zero debt," nor that STRC is more attractive solely based on its higher yield. The 61 basis points spread is quite narrow, and the actual choice depends on which risk investors are more concerned about: a complex debt structure or the financing and liquidity risks of a small issuer.

6.2 When SATA May Exhibit Relative Value

Four types of misalignments may be closely monitored:

- Price declines while fundamentals remain unchanged: If SATA declines but BTC coverage, cash, and ATM conditions do not continue to deteriorate, rising yields may create value;

- Coverage continues to deteriorate while price remains stable: If the number of SATA shares grows much faster than BTC, the market may continue trading it close to par, potentially underestimating risk;

- SATA and STRC yield spreads unusually widen: It is necessary to determine whether this is a liquidity shock or differences in issuer fundamentals;

- Coupon adjustments diverge from market price: A board increase in coupon may support price but also increase future cash burden.

7. Conclusion

SATA's innovation is real. It transforms a traditionally monthly or quarterly paid perpetual preferred stock into a public instrument that generates cash flow every business day; it also allows investors in traditional brokerage accounts to obtain a high-yield security related to a BTC balance sheet without needing to hold the currency directly.

However, the price and asset changes in late June corrected several overly optimistic judgments:

- SATA is not a BTC collateral bond, but rather a corporate-level cumulative perpetual preferred stock;

- Daily dividends have not created low volatility, and principal prices can erase several months' worth of dividends within a few days;

- The increase in BTC quantity has not prevented the coverage ratio from declining from 2.44 times to 1.52 times;

- About 940 basis points is the coupon spread, while the current market spread has expanded to about 1,117 basis points;

- The cash buffer is strong, yet the dividend burden and financing costs are also rising simultaneously;

- SATA's structural advantages remain but have been repriced by the market from "near par yielding product" to "deeply discounted high-risk perpetual credit."

SATA's action is: to slice a BTC treasury company's balance sheet into a tradable, cumulative, perpetual preferred equity layer, and let the market reprice this equity layer every day.

A mature asset class will not only have a spot price but will also develop financing rates, priority, credit spreads, durations, and paths of default.

However: the frequency of cash flows can be engineered, but risks will not disappear; they will merely shift from price fluctuations to coverage ratios, financing costs, perpetual durations, and corporate governance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。