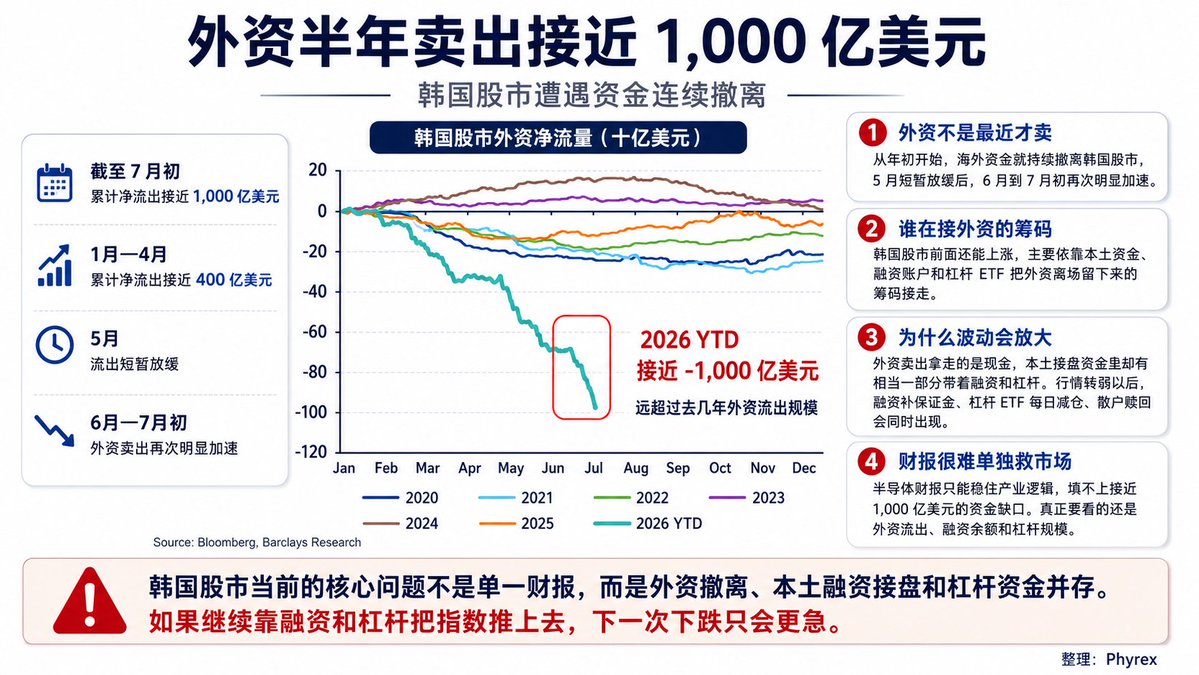

Foreign capital has sold nearly 100 billion dollars in six months, and the South Korean stock market is experiencing continuous withdrawal of funds.

I mentioned earlier that the recent decline in the South Korean stock market, the semiconductor earnings reports are merely superficial; the biggest trouble is the simultaneous occurrence of financing, leveraged ETFs, and the withdrawal of foreign capital.

By early July, foreign capital's cumulative net sell-off of South Korean stocks has approached 100 billion dollars. In the past few years, the most severe outflow of foreign capital was about 20 to 25 billion dollars, while this year's outflow in just over half a year has far exceeded the total for previous years.

From January to April, the cumulative net outflow was nearly 40 billion dollars. After a brief slowdown in May, it accelerated again in June, and by July it was directly approaching 100 billion dollars.

This indicates that while the South Korean stock market was rising earlier, overseas funds not only didn’t increase their positions but were actually selling off. The continued rise of the South Korean stock market largely relies on domestic funds, financing accounts, and leveraged ETFs taking over the chips left behind by the exit of foreign capital.

With foreign capital selling close to 100 billion dollars, KOSPI was still able to set new highs, indicating that the buying power of domestic funds at that time was very strong. However, the stability of this rise is very poor because foreign capital took cash away, and a significant part of the funds coming back from domestic investors is sourced from financing and leverage.

When the market is rising, the margins in financing accounts are sufficient, and leveraged ETFs will passively increase their exposures daily, allowing domestic funds to continue to push the market higher. Once prices start to fall, financing accounts need to top up margins, leveraged ETFs must reduce their positions daily, and retail investors might redeem due to losses.

The funds that previously absorbed the foreign capital sell-off will turn into new selling pressure during a decline.

This is also why the volatility of the South Korean stock market has been increasing recently. Since the beginning of the year, foreign capital has been continuously withdrawing, and the remaining positions in the market increasingly rely on domestic financing and leverage to maintain. As long as Samsung Electronics, SK Hynix, or the semiconductor sector experience continuous corrections, the entire capital structure will start to shrink.

Good earnings reports can only temporarily stabilize emotions, making it very difficult to fill the foreign capital gap of nearly 100 billion dollars.

The healthiest outcome is for the market to consciously reduce positions and leverage while waiting for the foreign capital selling pressure to gradually finish. If the index continues to be pushed up through financing and leverage, it will only make the next decline even more frightening.

@Gate Crypto, US stocks, Hong Kong stocks, Korean stocks, gold, CFD, one-stop trading for market predictions

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。