Irrelevant to fluctuations — The South Korean stock market has now entered a very abnormal trading state

This year, the KOSPI in South Korea has recorded single-day volatility reaching crisis levels, often resembling a pile of highly leveraged funds accelerating and braking against each other. The index was originally meant to disperse some individual stock risk, but now the core stock index of a country is frequently showing individual stock-level volatility, which is quite alarming.

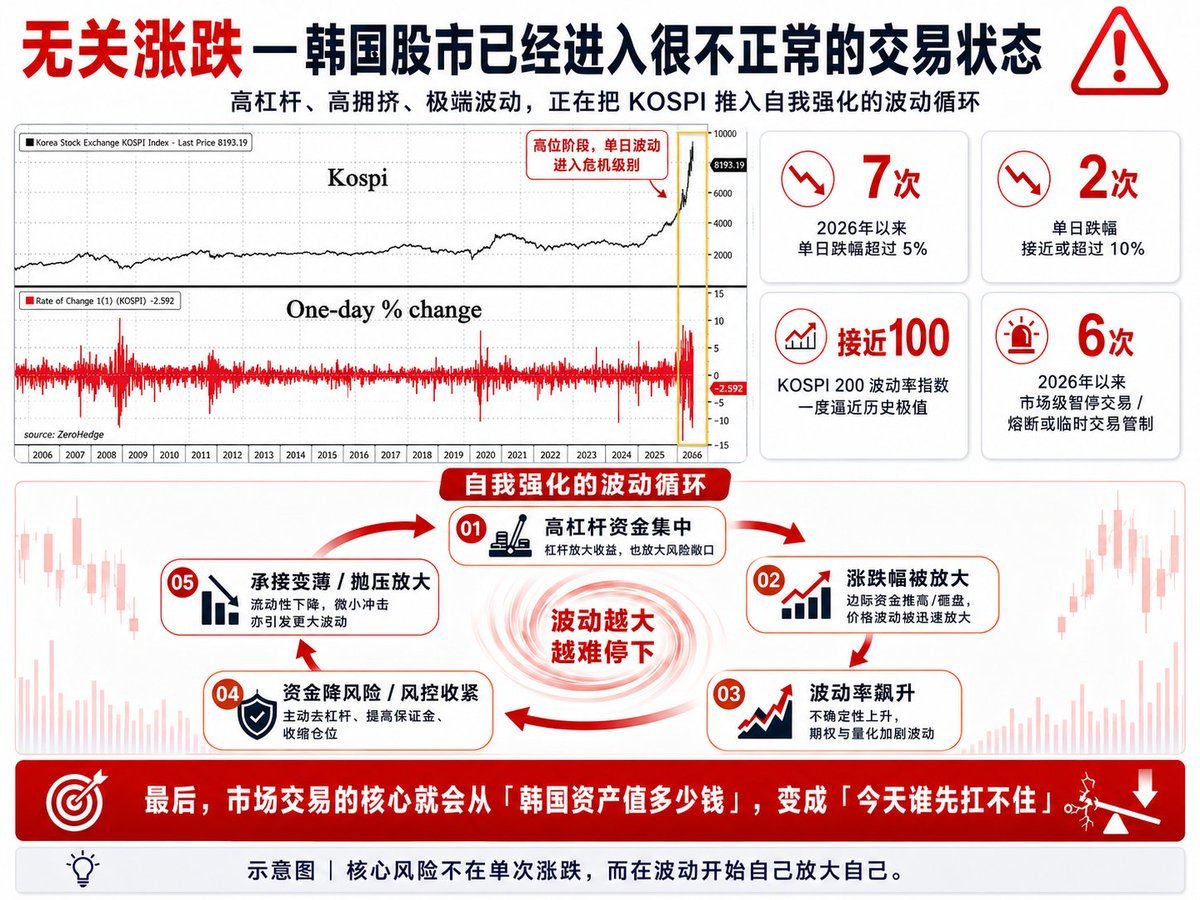

Since the beginning of this year, the KOSPI has experienced at least 7 instances of single-day declines exceeding 5%, with 2 of those instances seeing declines close to or exceeding 10%. Such fluctuations may be understandable for small-cap stocks, but when it occurs within South Korea's core stock index, it indicates that the market's trading condition has clearly gone out of control.

More critically, the South Korean version of VIX, or the KOSPI 200 volatility index, recently approached 100, setting a new historical high. This level has surpassed that of the 2008 financial crisis and the pandemic crash in 2020.

A volatility close to 100 signifies that the market has started trading South Korean stocks with an extremely high risk premium. To put it plainly, funds have already implicitly accepted that there will be severe fluctuations tomorrow, prompting some to rush for rebounds while others scramble to exit, naturally causing prices to soar and plummet.

Even more concerning is that since 2026, the South Korean market has triggered multiple circuit breakers or temporary trading halts due to trading restrictions. This system has been in operation since 2000, and over the last twenty years, half of all market trading halts have occurred this year.

One circuit breaker can be viewed as an unexpected event, two or three times can be seen as extreme sentiment, and six times concentrated in a single year indicates that the trading structure of the South Korean stock market has become very perilous.

The South Korean stock market rose too quickly initially, with funds becoming too concentrated, spinning mainly around Samsung and SK Hynix related products. As the scale of single-stock high-leverage products grew larger, the profit effects during rises were amplified, while the selling pressure and panic during declines were also magnified.

The result is that what may have originally been a 2% or 3% adjustment can easily transform into 5%, 8%, or even 10% in an environment of high leverage and high crowding. The greater the decline, the higher the volatility. The higher the volatility, the tighter the funds. The tighter the funds, the easier it is for the subsequent selling pressure to be magnified.

Therefore, the current problem in the South Korean stock market has evolved into a self-reinforcing cycle of volatility. High leverage magnifies the rises and falls, those rises and falls amplify volatility, which in turn forces funds to lower risks, and lowering risks makes the market more prone to significant rises and falls.

In the end, the core of market trading has shifted from "how much is South Korean assets worth" to "who cannot hold on today."

@Gate Crypto, US stocks, Hong Kong stocks, Korean stocks, gold, CFD, one-stop trading for predictive markets

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。