TL;DR

- Bank of America raised its capital expenditure forecasts for Alphabet, Meta, and AWS, stating that the total capacity could reach 57GW by 2027.

- Model breakdown shows that each GW of AI capacity for Meta has an implied value of approximately $4 billion, far lower than the two major cloud providers.

- Meta appears to be the cheapest, but its enterprise AI sales, power access, and customer payments have yet to be fully proven.

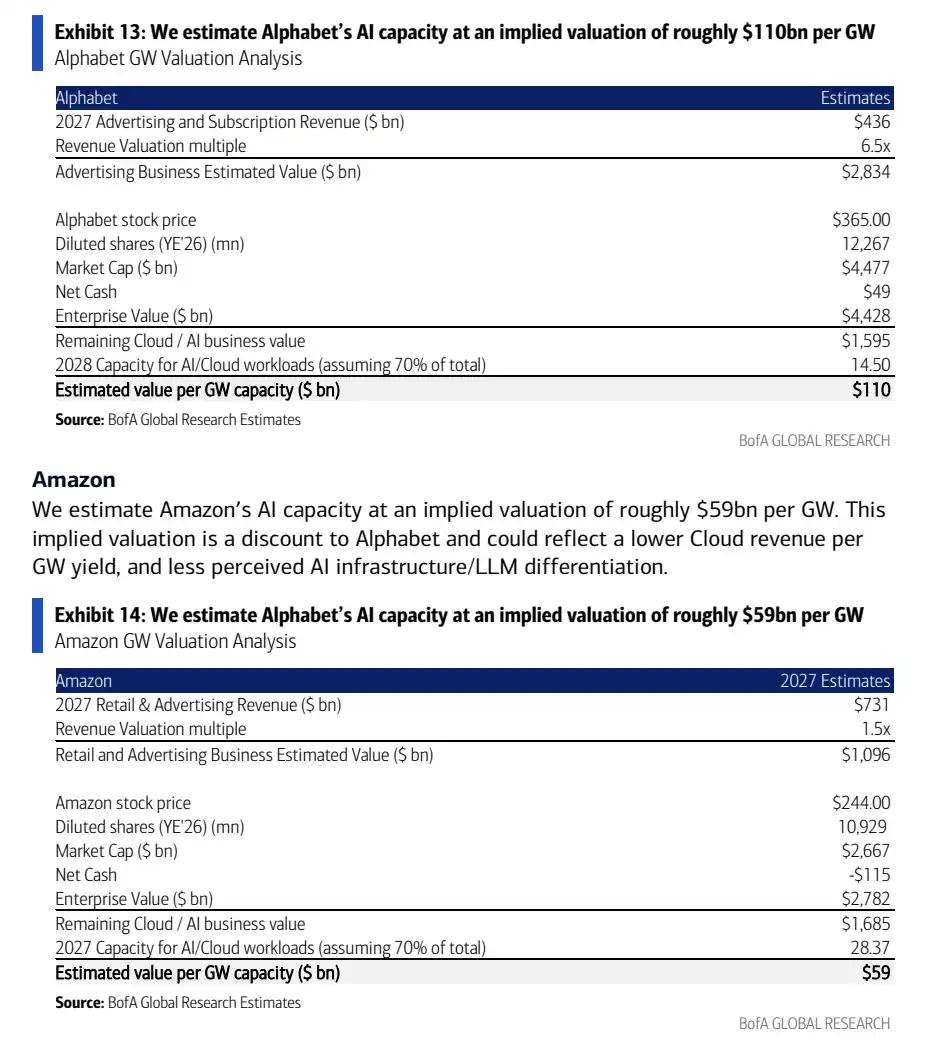

In its latest report, Bank of America upgraded its forecasts for the future capital expenditures and data center capacities of Alphabet, Meta, and Amazon AWS, providing a stark contrast in valuation breakdowns: according to its model, each GW of AI capacity for Meta has an implied value of only about $4 billion at the current stock price, much lower than Alphabet's approximately $110 billion/GW and Amazon's approximately $59 billion/GW.

The highlight of this report is not who spends the most, but how the market assigns completely different prices for similar AI data center expansions across different companies. AWS and Google Cloud already have mature cloud businesses that allow them to sell computing power to enterprise clients. Meta relies more on its advertising business, AI recommendation efficiency, and its still nascent enterprise AI products, and thus the data center value reflected in its stock price is lower.

For investors, AI capital expenditures ultimately need to answer a real question: can power, GPUs, and data center capacities translate into cloud revenue, enterprise AI service revenue, or higher advertising efficiency? The discounted valuation of Meta signifies that the market has not fully accepted this question yet.

The Three Giants Expect a Capacity of 57GW by 2027, Capital Expenditures Being Revised Upward

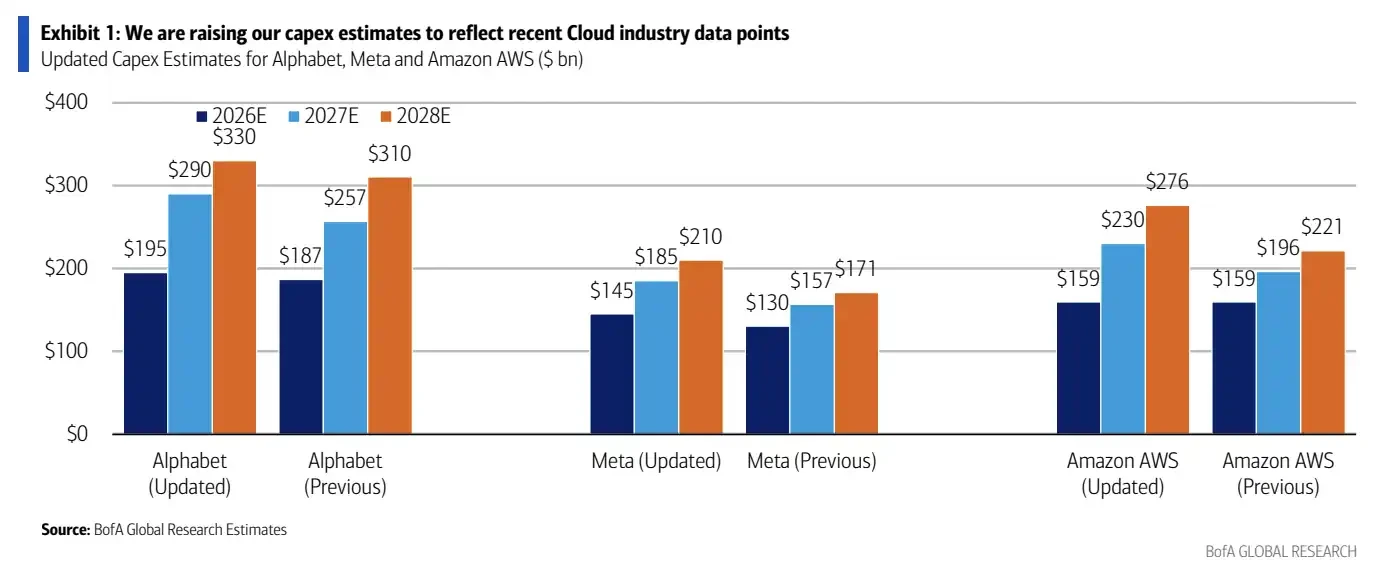

According to Bank of America's forecast, the overall capital expenditure expectations for Alphabet, Meta, and AWS from 2026 to 2027 have been revised upwards. Specifically, Alphabet's capital expenditure expectation for 2026 has been raised from $187 billion to $195 billion, and for 2027 from $257 billion to $290 billion. Meta's expectation has been raised from $130 billion to $145 billion for 2026, and from $157 billion to $185 billion for 2027. AWS is maintaining its expectation of $159 billion for 2026, while its 2027 figure has been raised from $196 billion to $230 billion.

These figures are closer to Bank of America's model forecasts and do not entirely align with the publicly stated guidance from the companies. In the public statements, Meta had previously raised its 2026 capital expenditure guidance to $125 billion to $145 billion, while Alphabet's public guidance is about $180 billion to $190 billion.

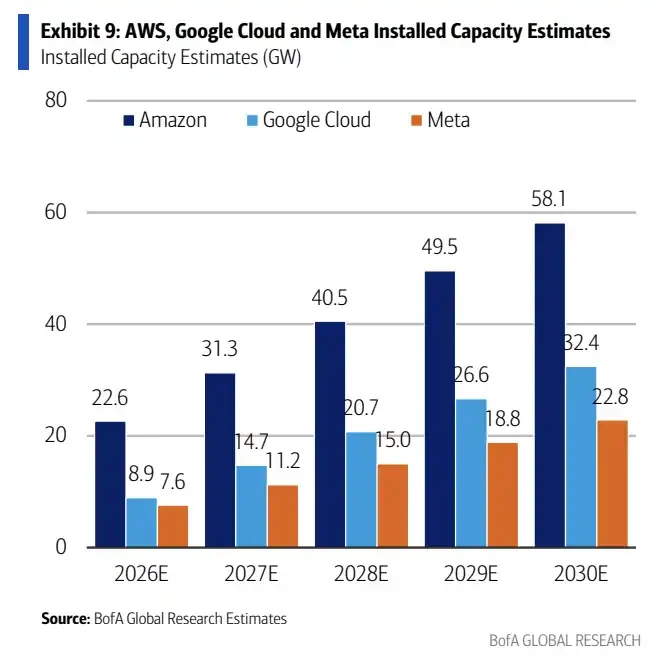

In terms of data center capacity, Bank of America estimates that the three companies will collectively reach about 27GW by the end of 2025, rising to 39GW in 2026 and further to 57GW in 2027. In other words, they will add around 30GW of capacity in two years.

The largest addition will come from Amazon. From 2026 to 2027, AWS is expected to add about 15GW, Google about 9GW, and Meta about 6GW. AWS itself has a larger cloud infrastructure base and is able to better absorb customer demand, internal e-commerce, and AI services, resulting in the largest scale of expansion.

Comparison of old and new capital expenditure forecasts for Alphabet, Meta, and AWS from 2026 to 2028, showing the most significant upward revision for 2027.

Building the same 1GW capacity comes with different costs. According to Bank of America’s estimates, the cost of adding each GW of capacity in 2026 will be about $25 billion for Amazon, $37 billion for Google, and $45 billion for Meta. Amazon has the lowest costs, mainly due to scale advantages and self-developed chips. Meta has the highest costs, affected more by early civil construction investments and reliance on external GPUs.

This places Meta in a more awkward position: its added capacity is not the highest, but the construction costs per GW are more significant. Should it fail to smoothly generate enterprise revenue in the future, or not clearly reflect that in advertising efficiency, the market will find it more challenging to assign a higher valuation to this portion of its assets ahead of time.

Valuation Gap Widens: Meta is Worth Only $4 Billion per GW

Bank of America’s valuation breakdown method first strips away the traditional business values of the three companies, then reverse-engineers the implied value the market assigns to AI capacity.

After calculating based on the 2027 multiples of core advertising, retail, and other revenues, Meta's implied valuation for each GW of AI capacity is only about $4 billion. Alphabet's is about $110 billion/GW, while Amazon's is around $59 billion/GW.

This gap directly points to the different commercialization paths of the three companies. The market is already more willing to consider the data center capacities of Alphabet and Amazon as realizable assets, but remains noticeably cautious about Meta's AI capacity.

Comparison of implied valuations per GW: Alphabet approximately $110 billion, Amazon approximately $59 billion, Meta approximately $4 billion.

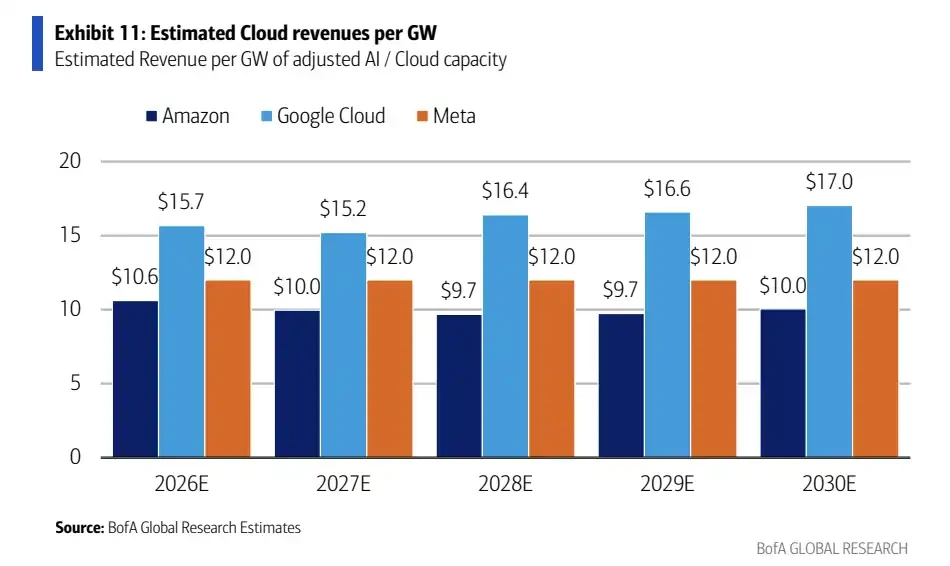

AWS and Google Cloud’s capacities are more readily linked to cloud revenue. According to Bank of America's model, AWS generates about $10.6 billion per GW in cloud revenue in 2026, while Google Cloud generates about $15.7 billion. The revenue paths for enterprise customers purchasing cloud computing power, AI training, and inference services are relatively clear.

Meta, on the other hand, is different. It has a vast advertising business and AI recommendation system, but its enterprise AI revenue is still in the early stages. Even if Meta accelerates its AI data center construction, the market will still ask: is this capacity mainly enhancing its own advertising efficiency, or can it be sold externally like a cloud provider?

If it is primarily used for internal products, the valuation method will be more aligned with advertising efficiency improvements rather than independently assessed cloud infrastructure assets. For Meta to achieve a higher valuation per GW, it needs to demonstrate clearer paths for enterprise AI products, subscription revenue, or Business Agent sales.

Meta's Upside Potential is Stuck on Whether It Can Sell the Capacity

In Bank of America’s optimistic estimates, by 2030, Meta's data center capacity could reach about 22.8 to 23GW. If 40% of this is used for enterprise AI sales, and revenue is calculated at $12 billion/GW, it corresponds to a potential enterprise revenue opportunity of about $110 billion.

This remains a model assumption, not a management target, nor a confirmed revenue opportunity. It explains where the “Meta is undervalued” narrative comes from: if Meta can productize part of its AI capacity in the future and sell AI services, subscription products, or Business Agent capabilities to enterprises, then the current implied value of about $4 billion per GW seems very low.

Growth forecast of installation capacities for Amazon, Google Cloud, and Meta from 2026 to 2030, with Meta's capacity expected to reach about 22.8GW by 2030.

The problem is that this assumption has not yet materialized. AWS and Google Cloud already have clients, contracts, and cloud revenue metrics, while Meta needs to prove that it is not merely “building capacity for itself,” but also capable of generating sustainable enterprise AI revenue.

The potential catalysts listed in the report include improvements in cloud gross margins, enhanced visibility of Meta's enterprise AI and subscription products, and greater disclosure of AI revenue breakdowns. Some products and collaborations further out still remain hypothetical and cannot be directly considered as having contributed to actual business.

Estimated cloud/AI revenue per GW from 2026 to 2030, with AWS around $10-10.6 billion, Google Cloud around $15.2-17 billion, and a conservative assumption for Meta around $12 billion.

For Meta, what can truly change market perception is not the announcement of another larger data center plan, but showing investors what revenue these capacities can generate. In particular, the proportions, product forms, and revenue disclosures for enterprise AI sales are still not clear enough.

The Cheapest Asset Needs to Prove Itself the Most

Meta appears to be the cheapest in terms of AI capacity valuation among the three companies, but being cheap itself is not the answer.

The first constraint is power. A previous page from the U.S. Department of Energy cited an EPRI estimate that by 2030, data centers may account for up to about 9% of U.S. electricity consumption, while in 2023 it was about 4%. Recent studies from EPRI and Lawrence Berkeley National Laboratory indicate even higher ranges, showing that electrical pressure may continue to rise. Power access, transmission, local approvals, and energy prices will all impact whether the planned GW capacity can be realized on time.

The second constraint is chip and construction delivery. GPU supply, networking equipment, power infrastructure, and civil construction cycles will all affect the pace of production. An increase in capital expenditure does not mean that capacity will go online immediately, nor that revenue will be confirmed promptly.

The third constraint is customer payment. The demand for enterprise AI is still growing, but how much customers are willing to continuously pay for reasoning, training, and intelligence agent services at scale still needs more financial reporting data to verify. For Meta, if enterprise AI revenues cannot be clearly disclosed for an extended period, the market will find it difficult to value its data center capacity according to cloud provider standards.

Therefore, the report from Bank of America does not conclude that “Meta has realized its AI value,” but rather presents a more direct valuation contrast: against the backdrop of the three major internet giants continuing to expand AI capital expenditures, the market assigns the lowest price to Meta's data center capacity. What it needs to prove is the most, both in building out capacity and convincing investors that this capacity can transform into observable revenue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。