Original Report: BofA Global Research "Global Memory Tech", July 2, 2026

Compiled & Organized by: DaiDai, MSX Maitong

Edited by: Frank, MSX Maitong

Key Points Overview:

- BofA believes that the recent concentrated pullback in storage stocks is mainly due to risks such as Meta's orders, Changxin Storage entering Apple's supply chain, and South Korea's expansion plans, and does not indicate a reversal in the industry's fundamentals;

- Meta's external provision of data centers or cloud services is more likely about monetizing computing power and diversifying business, rather than a significant reduction in storage demand, as its demand for HBM, LPDDR5, and enterprise-grade SSDs continues to grow;

- Changxin Storage is unlikely to become a significant DRAM supplier for Apple in the short term; Apple is more likely to use it as a bargaining chip in price negotiations with Samsung, SK Hynix, and Micron;

- Research into the Japanese supply chain shows that DRAM and NAND prices are still expected to rise quarter-on-quarter in the third and fourth quarters, and the industry may continue to face shortages in 2027, with manufacturers' capital expenditure and wafer production still relatively restrained;

- The storage industry remains in a strong cycle, but as product prices and related stocks have risen significantly, the future market will depend more on earnings realization, and fluctuations within the sector and differentiation among individual stocks may become more pronounced;

In the past week, global storage stocks have experienced a significant pullback.

The market quickly found three seemingly reasonable explanations for this decline: Meta is preparing to sell some computing power externally, possibly indicating previous overbuilding of data centers; Apple is assessing Changxin Storage's DRAM, which may disrupt the supply pattern dominated by Samsung Electronics, SK Hynix, and Micron; South Korea has announced a large-scale semiconductor industrial cluster plan, further exacerbating worries about future supply overcapacity.

All three narratives ultimately point to the same conclusion: demand may have peaked, supply is about to expand, and the storage supercycle may be nearing its end.

However, BofA's assessment in the latest edition of the "Global Memory Tech" report is exactly the opposite.

In its view, the above risks do not entirely exist, but the market has clearly overestimated their impact on the short-term supply-demand landscape; whether it’s cloud providers' capital expenditures, South Korea's semiconductor exports, or spot and contract prices for DRAM and NAND, none have yet shown a directional reversal in the storage cycle.

The real change is not that the fundamentals have shifted from strong to weak, but that after experiencing significant price increases and stock revaluation, the industry is starting to enter a new phase where the fundamentals remain strong, but trading difficulties have significantly increased.

1. Assessing One by One: Are Market Concerns Justified?

1.Meta Selling Computing Power Does Not Mean Reduction in Storage Orders

The concern about Meta in the market comes from a seemingly reasonable inference: If Meta begins to open its data centers to external customers or sell cloud services, does that mean the company has previously procured too many servers and can no longer digest the existing computing power internally?

If the answer is yes, then demand for AI hardware such as GPUs, HBM, server DRAM, and enterprise-grade SSDs may subsequently decline.

However, the BofA report indicates that industry chain feedback suggests that storage chip manufacturers believe Meta will continue to adopt high-performance storage products like HBM, LPDDR5, and enterprise-grade SSDs more actively in AI data centers, therefore market speculations on "Meta renting out over-invested AI servers or cloud infrastructure" lack sufficient basis.

In fact, some NAND controller chip and packaging substrate material manufacturers have indicated that Meta's chip and component orders are still increasing, thus suggesting that Meta's opening of its own data centers to external customers is more likely an attempt at asset monetization and business diversification, rather than a forced response to a severe overcapacity issue.

2.Changxin Storage Entering Apple's Supply Chain is More Like a Negotiation Chip

BofA's report anticipates that the probability of Apple widely adopting Changxin Storage DRAM in the short term remains low.

If enumerated, there are primarily three constraints:

- First is the policy and supply chain limitations: Apple needs to consider relevant restrictions imposed by the U.S. on the Chinese semiconductor industry, along with the associated compliance and supply chain risks;

- Second is the technology specifications: Apple has high requirements for the transmission speed, power consumption, and reliability of mobile DRAM, including transmission speeds above 10Gbps, approximately 1.1V low power design, and ECC error correction capabilities. Whether Changxin Storage can consistently and stably meet these requirements on a large scale still needs further validation;

- Finally, there are intellectual property risks: core DRAM patents have long been concentrated in leading manufacturers such as Samsung, SK Hynix, and Micron. If Apple adopts products with insufficient patent coverage on a large scale, it may face potential lawsuits and supply interruption risks;

Theoretically, Changxin Storage could aim for low-end iPhone 18e orders, but considering the scale of related models in the Chinese market, the actual procurement volume is expected to be limited.

Rather than genuinely restructuring the supply chain, Apple is more likely to use this to enhance its bargaining power in contract price negotiations in the second half of 2026 or 2027, thus this event is more likely to affect Samsung, Hynix, and Micron's pricing expectations in the short term, rather than immediately altering the global DRAM supply-demand landscape.

3. South Korea's Large-Scale Expansion Does Not Mean Supply Will Be Out of Control in the Short Term

Another current concern arises from South Korea's new round of semiconductor industry cluster planning.

Some investors believe that the South Korean government's plan to invest about 800 trillion Korean won to build new memory wafer fab clusters in the southwestern region may indicate that the storage cycle is nearing its peak, but the BofA report takes a negating stance and anticipates that the project is unlikely to form large-scale effective supply before the early 2030s, and at this stage priority needs to be given to the expansion of the Yongin and Pyeongtaek industrial clusters in 2026-2035.

Therefore, an industrial plan spanning over a decade cannot be directly equated with an imminent supply crisis within the next two or three years; long-term capacity expansion is worth continuous tracking, but it is insufficient to directly support the judgment that the current storage cycle has peaked.

4. Japanese Supply Chain Research Remains Optimistic

BofA's recent supply chain research conducted in Japan has further reinforced the optimistic judgment about the storage industry.

Japanese investors generally acknowledge the current industry's prosperity, but as product prices and related stocks have risen rapidly, the market is also beginning to pay more attention to potential downturn cycles, and compared to investors' caution, the judgments given by supply chain management remain relatively positive:

- Second-quarter storage ASP performance was strong, especially for NAND;

- ASP in the third and fourth quarters is expected to remain above the second quarter;

- DRAM and NAND may continue to be in a state of shortage in 2027;

- Long-term supply agreements are increasing, but mainly focus on procurement quantity agreements;

- Capital expenditures and wafer production continue to be restrained, especially among Japanese NAND manufacturers;

This indicates that while the market has begun to discuss the next supply cycle in advance, from the actual expansion by manufacturers and customer procurement behavior, the industry has not yet entered a significantly uncontrolled supply phase.

5. Samsung’s Storage Business May Still Exceed Expectations

In a report released on July 2, BofA anticipated that due to extraordinary bonus expenses and pressure on smartphone business profit margins, Samsung Electronics' overall operating profit in the second quarter might be slightly below market's more optimistic expectations; however, due to strong average selling prices for DRAM and NAND, the operating profit of the storage business calculated separately is still expected to exceed market expectations.

Five days after the report was released, Samsung announced preliminary results for the second quarter on July 7: consolidated sales of about 171 trillion Korean won, operating profit of about 89.4 trillion Korean won, representing year-on-year increases of 129.3% and 1810.3% respectively. The operating profit exceeded the market's previous expectation of about 86 trillion Korean won, indicating that BofA's assessment of the group's overall profit possibly being slightly lower than optimistic expectations did not materialize.

However, what Samsung disclosed this time is still preliminary data at the group level, and detailed profit data for the storage, foundry, and mobile businesses have yet to be released, so whether the storage department exceeded expectations still requires confirmation from the complete financial report. In light of the second quarter's DRAM, NAND price increases and significant growth in South Korea’s semiconductor exports, it is highly likely that the storage business remains the core force driving Samsung's profit surge this round.

2. What Signals Have Exports, ASP, and Product Prices Released?

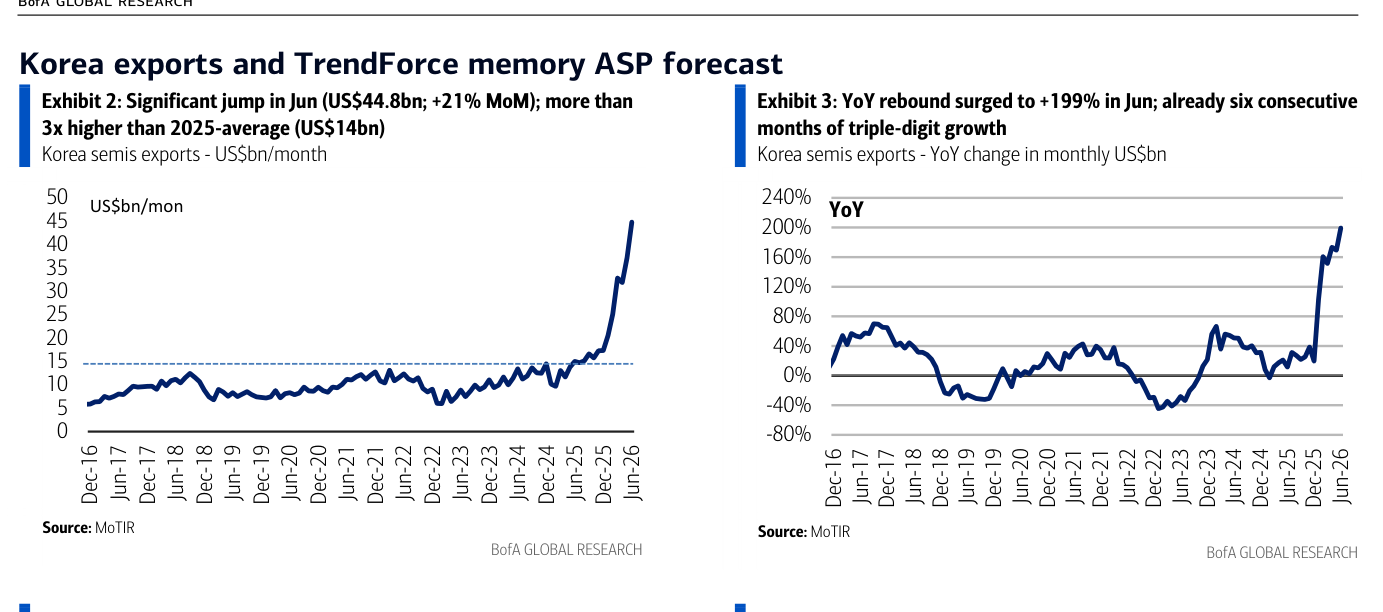

1.South Korea's Semiconductor Exports Have Seen Significant Growth

In June 2026, South Korea's semiconductor exports reached $44.8 billion, a month-on-month increase of 21% and a year-on-year increase of 199%, achieving triple-digit year-on-year growth for six consecutive months.

This figure is approximately three times the monthly average of $14 billion in 2025, reflecting that the current increase in storage prices has begun to significantly translate into export income and corporate profits.

Of course, the increase in export volume does not entirely represent a synchronized increase in shipment volume, as a large part of the increment comes from the rapid increase in product average selling prices, but this also precisely indicates that the core contradiction in the current supply chain remains the rising prices and tight supply, rather than inventory buildup or significant demand shrinkage.

South Korea's semiconductor export value and year-on-year growth rate: Significant spike in exports in June 2026 (Original Report Page 2)

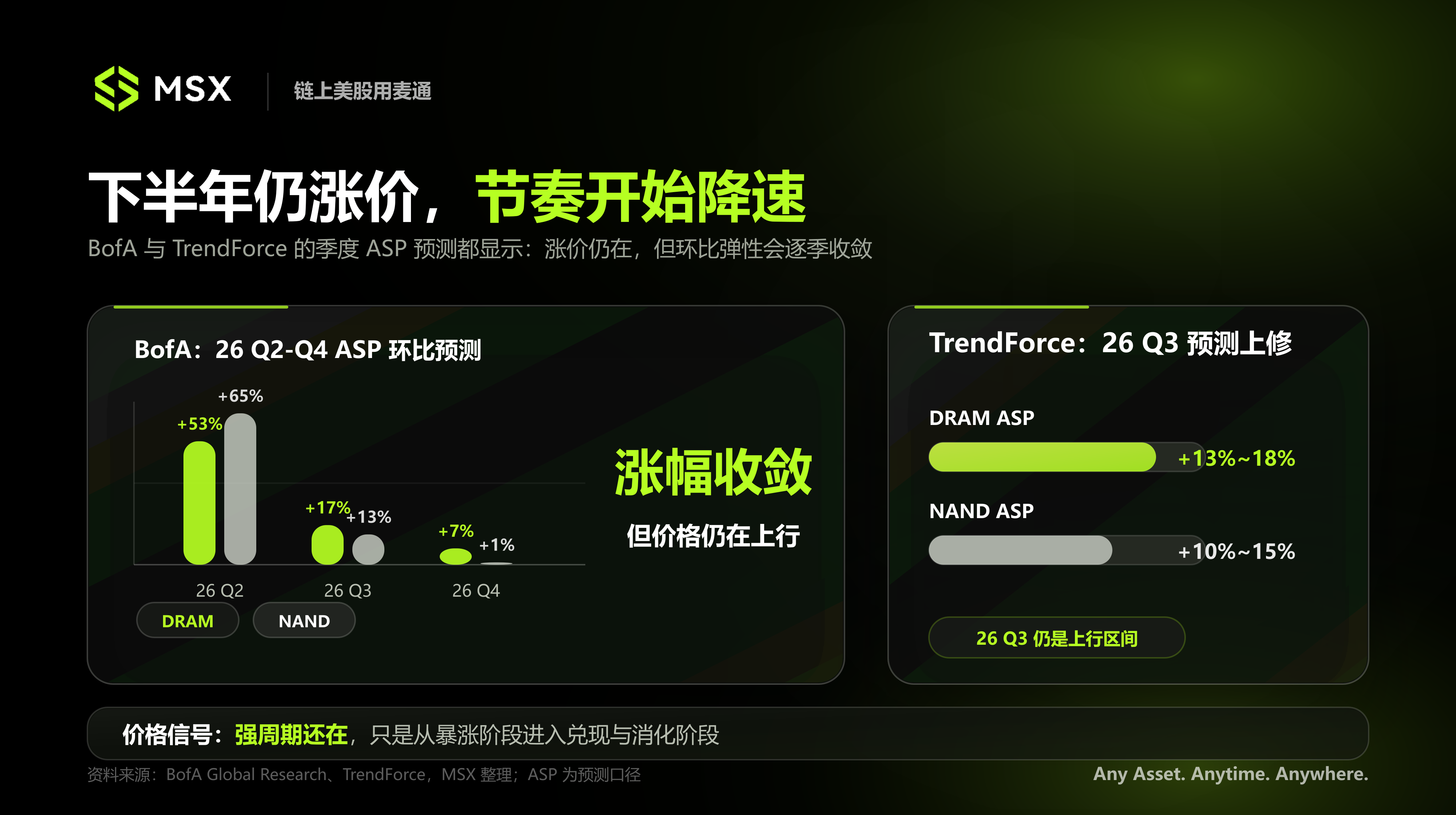

2.DRAM Remains the Strongest Storage Category

TrendForce has revised its third-quarter 2026 DRAM ASP forecast from a quarter-on-quarter increase of 3%-8% to 13%-18%; BofA estimates that DRAM ASP will rise quarter-on-quarter by 53%, 17%, and 7% respectively in the second to fourth quarters of 2026.

The specific criteria of the two forecasts may differ, but they point to the same trend, which is that DRAM prices will continue to rise in the second half of the year, but the quarter-on-quarter increase may gradually slow down as the price base rises.

As of early July 2026, the spot price for 16Gb DDR5 is about $47, while for 16Gb DDR4 it is about $75, both significantly above the price peaks of the previous storage cycle. The core reason is not just terminal customers replenishing stocks, but rather that storage manufacturers are continuously shifting wafer capacity towards higher-margin HBM and server DRAM.

As advanced capacity is absorbed by AI-related products, the supply available for traditional DDR4 and standard DDR5 decreases correspondingly.

Especially for DDR4. With the leading manufacturers gradually exiting mature products, DDR4 has seen a pronounced structural shortage, with the contract prices for 16Gb DDR4 and DDR5 rising to the $35-$40 range, essentially eliminating the technological premium that DDR5 had over DDR4.

This does not mean the market prefers the older generation DDR4, but rather that the speed at which manufacturers exit is faster than the rate of customer product transitions, resulting in a situation where mature products become even scarcer.

3.NAND Price Increases Slow, But Absolute Prices Remain High

Compared to DRAM, the marginal changes in NAND prices are more pronounced.

The spot price of 512Gb NAND wafers peaked in March 2026 and gradually stabilized or slightly declined from April to June, but still increased by more than 50% within the year, approximately eight times the low point in February 2025.

NAND contract price is around $25, about ten times the low point of $2.5 in February 2025. After experiencing significant rises in Q4 2025 and Q1 2026, the month-on-month increase in NAND contract prices in April to June has reverted to around 1%-5%.

This does not mean NAND prices have reversed; it indicates that customers’ tolerance for high prices is gradually nearing its limit, and the pace of price increases is returning to normal.

The changes in client SSD prices are particularly intuitive. By June 2026, the price of a 512GB client SSD increased from $73.1 at the end of 2025 to $137.5, nearly doubling, reflecting that the upstream NAND price increases are being continuously transmitted to terminal products.

Therefore, NAND's current more accurate state is that absolute prices remain very high, but the quarter-on-quarter increases are slowing down.

4.Server Memory Continues to Reach New Highs

Server memory also continues to show strong performance.

The price of 64GB server DRAM modules has set a historical high, with DDR5 around $1400 and DDR4 about $1100. In June 2026, the contract price for DDR5 server DRAM rose again, while DDR4 prices remained relatively unchanged.

This indicates that even though the price increase rate for some consumer-grade storage products is beginning to slow down, the high-end storage demand related to AI servers and data centers remains robust.

3.Cloud Capital Expenditure Remains the Demand Anchor, But Investment Logic Is Changing

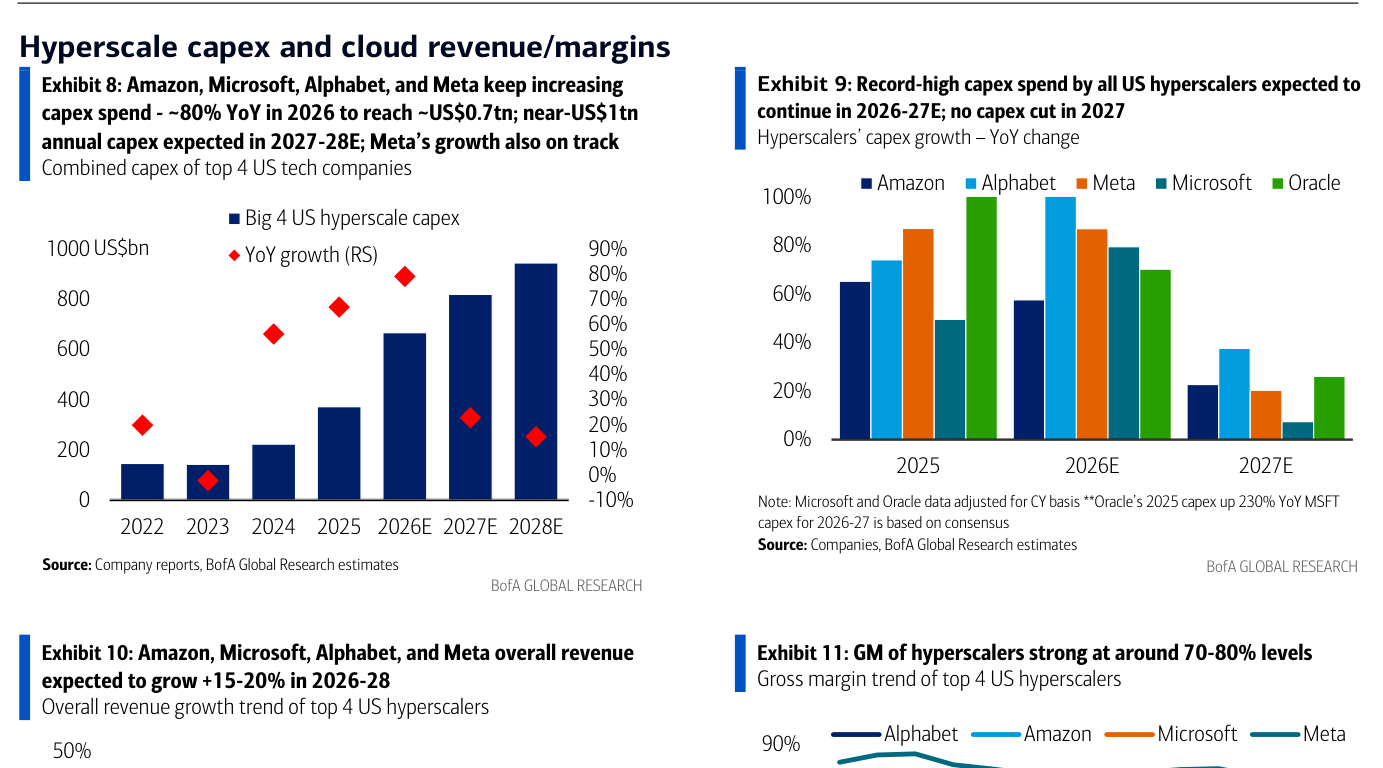

1.Hyperscale Cloud Providers Continue to Expand

Hyperscale cloud providers like Amazon, Microsoft, Alphabet, and Meta are becoming the most important source of new demand for storage. The report expects that the capital expenditures of these four companies will total about $700 billion in 2026, representing a year-on-year increase of about 80%; in 2027-2028, the annual capital expenditure scale may approach $1 trillion further.

Moreover, BofAhas not seen signs of significant cuts in capital expenditures by major cloud providers in 2027, which means these investments will ultimately be converted into more AI accelerators and HBM, more server DRAM, more enterprise-grade SSDs, more data centers, and AI inference infrastructure.

Trends in capital expenditures, revenue, and gross margins of major U.S. hyperscale cloud providers (Original Report Page 3)

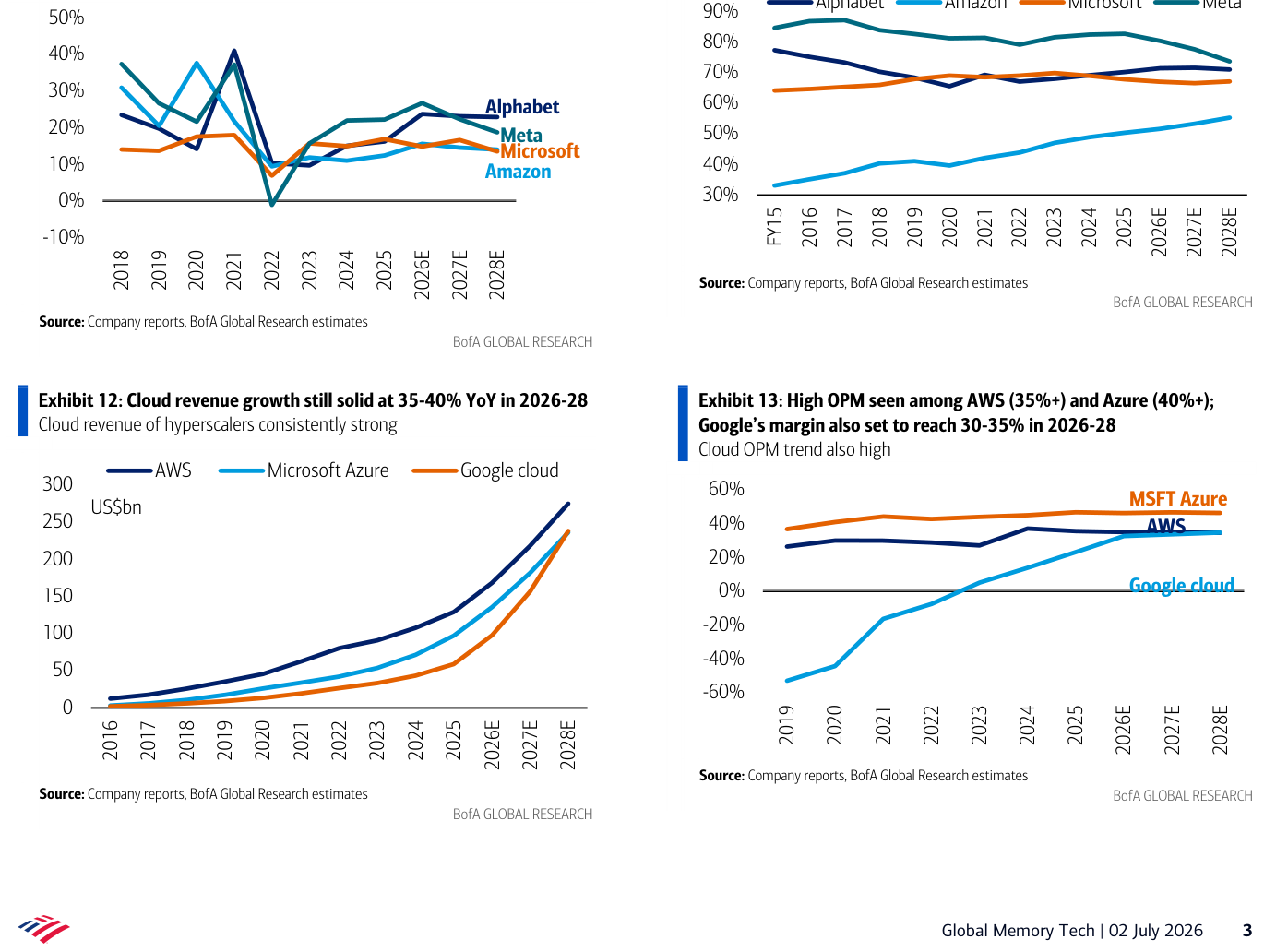

The report predicts that from 2026 to 2028, the overall revenue of the four major tech companies is expected to grow by 15%-20%, with cloud business revenue year-on-year growth potentially reaching 35%-40%.

Among them, AWS’s operating profit margin is expected to remain above 35%, Azure may exceed 40%, and Google Cloud is expected to reach 30%-35%.

As long as the cloud business can maintain high revenue growth rates and profit margins, tech giants will still have the business motivation to continue expanding investments in AI infrastructure.

Cloud revenue and operating margin trends (Original Report Page 3)

2.This Round of Cycle Is No Longer Just About Consumer Electronics Restocking

The biggest difference between this round of storage cycle and the past is that demand no longer primarily relies on restocking of smartphones and personal computers.

In past storage cycles, changes in inventory of personal computers and smartphones often drove the dynamics, forming typical cyclical characteristics, such as rising terminal demand, customer restocking, and increasing storage prices; subsequently, manufacturers expanded capacity, inventory gradually accumulated, and prices entered a downward cycle again.

However, the structure of this round of storage cycle is more complex, with current demand already expanding beyond single consumer electronics restocking to include:

- HBM;

- Server DRAM;

- Enterprise-grade SSD;

- AI inference infrastructure;

- Hyperscale cloud providers' capital expenditures;

- Structural shortages caused by the exit of DDR4 capacity.

This means that merely observing PC and smartphone sales is insufficient to judge the entire storage cycle—even if some consumer electronics demands are under pressure due to high prices, AI servers and data centers may still continue to absorb high-end capacity, keeping overall supply relatively tight.

However, this also means that differentiation within the sector will become more evident. In short, HBM, server DRAM, enterprise-grade SSD, and companies related to advanced packaging may continue to benefit from stronger orders and profit margins; manufacturers overly reliant on client, mobile, and consumer-grade NAND may experience a decline in demand elasticity sooner.

3.Shifting from Industry-Wide Gains to Earnings Realization

Since 2026, NAND, HDD, and DRAM-related stocks have generally experienced significant increases.

Charts in the original report show that SanDisk and Kioxia have seen increases of over 800% this year, and DRAM manufacturers and some semiconductor companies have also risen significantly.

In this scenario, even if the fundamentals of the industry have not changed directionally, any news regarding customer orders, capital expenditures, new supply, or price negotiations could trigger drastic fluctuations.

Therefore, BofA's judgment on the storage industry can be summarized as the fundamentals still showing a bullish tendency, but stock prices are no longer in a phase where risks can be ignored. Overall, future performance in the sector will depend more on three factors:

- First, whether storage prices can maintain levels that continue to drive upward profit revisions;

- Second, whether actual enterprise profit growth can absorb the previous valuation expansion;

- Third, whether new capital expenditures continue to remain restrained, avoiding premature deterioration of long-term supply expectations;

This is also why the pullback in the past week does not necessarily mean the end of the storage supercycle, but rather indicates that the sector is transitioning from "industry-wide gains" to "earnings validation" and "stock selection."

Final Thoughts

Objectively speaking, Meta providing cloud services externally, Changxin Storage entering Apple's supply chain, and South Korea launching large-scale expansion plans are not risks that can be entirely ignored.

However, at least based on the data presented in this BofA report, they have not changed the three most important facts in the storage industry:

- Capital expenditures for hyperscale cloud providers are still increasing;

- DRAM and NAND prices remain at historically high levels;

- New advanced capacity still requires a long time to form effective supply;

Therefore, it is more accurate to say that the pullback in the past week indicates "cycle peaking" rather than the market attempting to reprice for the next phase.

This current storage cycle has not yet shown clear fundamental turning points, but with high prices, high expectations, and high increases all occurring simultaneously, the questions that investors need to answer next are no longer limited to whether the storage industry will continue to rise, but rather broadened to which products are still in short supply, which companies can realize profits, and which stocks have already over-leveraged future gains?

The industry fundamentals remain strong, but the phase of indiscriminate revaluation for the entire sector may be gradually coming to an end.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。