TL;DR

- Kioxia and SanDisk have launched BiCS-10 production at their Kitakami K2 facility, with 1Tb TLC samples already shipping.

- The BiCS-10 interface speed has increased to 4.8Gb/s, but it will primarily rely on BiCS-8 volume until March 2027.

- The target price is approximately 110,000 yen, corresponding to about 32% upside potential, with risks in customer certification, K2 ramp-up, and supply disruptions.

Kioxia and SanDisk announced on July 3 that they have begun production of the 10th generation 3D Flash, known as BiCS-10, at the Kitakami facility Fab2/K2 in Iwate Prefecture, Japan. On the same day, Kioxia started shipping 1Tb TLC BiCS-10 samples, primarily for enterprise and data center SSDs.

This allows Kioxia's AI data center storage roadmap to enter the ramp-up stage for mass production, but it does not yet signal immediate profitability. Samples are used for customer functionality confirmation, and mass production specifications may still be adjusted, requiring further enterprise SSD certification, product onboarding, and K2 factory ramp-up.

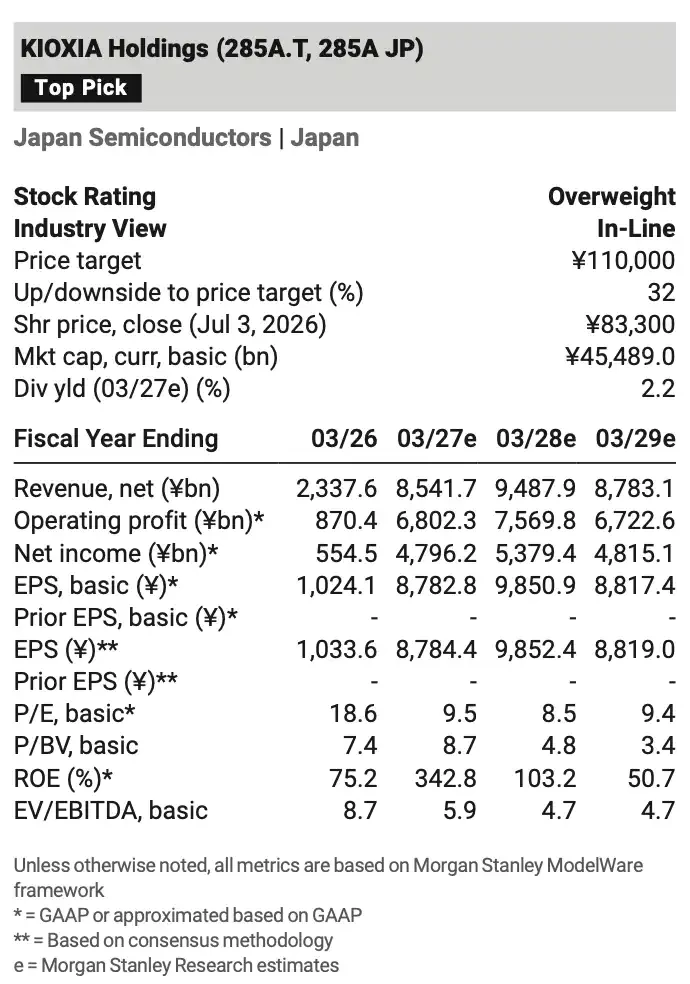

Morgan Stanley maintains an "Overweight" rating on Kioxia in their latest report. Based on the target price of around 110,000 yen and the stock price of 83,300 yen on July 3, this corresponds to approximately 32% upside potential. This judgment does not bet on the short-term volume of BiCS-10, but rather on Kioxia's ability to convert faster interfaces, higher bit densities, and lower power consumption into market share for AI data center SSDs and improved cash flow.

The financial forecast table shows FY2027e revenue of approximately 8.54 trillion yen, with FY2028e revenue of approximately 9.49 trillion yen, with profit outlook tied to product structure upgrades.

Interface Elevated to 4.8Gb/s, Kioxia Targets High-Bandwidth AI SSD

The most direct change in BiCS-10 is the increase in NAND interface speed from BiCS-8's 3.6Gb/s to 4.8Gb/s, an increase of about 33%. This metric may not be intuitive for consumer storage, but for enterprise SSDs and AI servers, interface speed affects data throughput, latency, and cache efficiency.

The 1Tb TLC samples shipped by Kioxia are aimed at enterprise and data center SSDs. In the 2026 Investor Day materials, the company positions the CM Series as "High Bandwidth SSD with TLC Flash Memory" and mentions compatibility with NVIDIA CMX Server, optimized for KV cache workload. This means NAND in AI servers is not just cheap large-capacity storage, but also has to bear data caching and access tasks closer to the computation side.

BiCS-10 is still 332-layer 3D Flash. Compared to BiCS-8, the officially disclosed bit density has increased by 59%, write power efficiency has improved by 18%, and read power efficiency has improved by 30%. Bit density affects the capacity produced per wafer, while power consumption affects the operational costs of data centers. What cloud vendors ultimately see are the costs per TB, SSD performance, and overall energy consumption.

However, leading technical specifications do not equate to commercial readiness. Enterprise SSDs typically have long certification cycles, especially for high-performance, low-latency, and AI load products. BiCS-10 has launched production and started shipping samples but is still distant from becoming Kioxia's main source of shipments and profits, needing confirmation of customer orders.

Short-Term Profit Still Relies on BiCS-8, Not Immediate Volume from BiCS-10

What may be more easily overlooked is that Kioxia's cost improvements over the next one to one and a half years will mainly still come from BiCS-8.

Morgan Stanley's model predicts that from 2026 to the first half of 2027, the company's output expansion and GB cost reductions will still be driven by BiCS-8. By the end of March 2027, BiCS Gen.8 is expected to account for over 80% according to production GB metrics. BiCS-10 is more like a starting point for medium to long-term product structure upgrades, rather than a single catalyst to immediately change short-term financial reports.

This rhythm is not contradictory. The new generation of NAND manufacturing processes usually goes through production line changes, yield ramp-ups, customer validations, and product mix adjustments from pilot production and sample shipments to mass onboarding. The K2 factory began operations in September 2025, previously producing the 8th generation 3D Flash. With the introduction of the 10th generation product, overall capacity will continue to expand, but the profit and loss statement will wait for capacity utilization rates, yields, and customer orders to catch up.

Kioxia's medium to long-term goal is to increase the sales ratio from the data center and enterprise market to over 60%. The significance of BiCS-10 lies here: if the new generation of NAND successfully enters high-end enterprise SSDs and increases its share in AI server storage, Kioxia's revenue structure will lean more towards the enterprise market.

32% Upside Comes from Valuation and Product Structure Realization

The approximately 32% upside potential stems not just from a bet on rising NAND prices but from combining technology upgrades, improved data center SSD market share, and enhanced free cash flow.

In terms of valuation, the target price is based on a FY2028e free cash flow yield of approximately 10%, implying a price-to-earnings ratio of around 11 times. In the model, FY2027e revenue is about 8.54 trillion yen, with FY2028e further rising to approximately 9.49 trillion yen; basic EPS is approximately 8,782.8 yen and 9,850.9 yen, respectively. The premise here is that Kioxia can transform technology upgrades into better product pricing and cost structures between demand growth and supply constraints.

The market is willing to give Kioxia a higher valuation, partly due to AI storage demand. Compared to consumer electronics and traditional PC cycles, data center SSDs are more driven by cloud capital expenditures, AI cluster construction, and enterprise storage upgrades. If BiCS-10 enters high-end enterprise SSDs, Kioxia's revenue quality and cycle volatility may improve.

However, this realization chain is long. Technical parameters must first become products, products must pass customer certification, and after certification, they will turn into shipments, ultimately entering revenue and profit. Any delays in any link will affect the market's view on profitability after 2027.

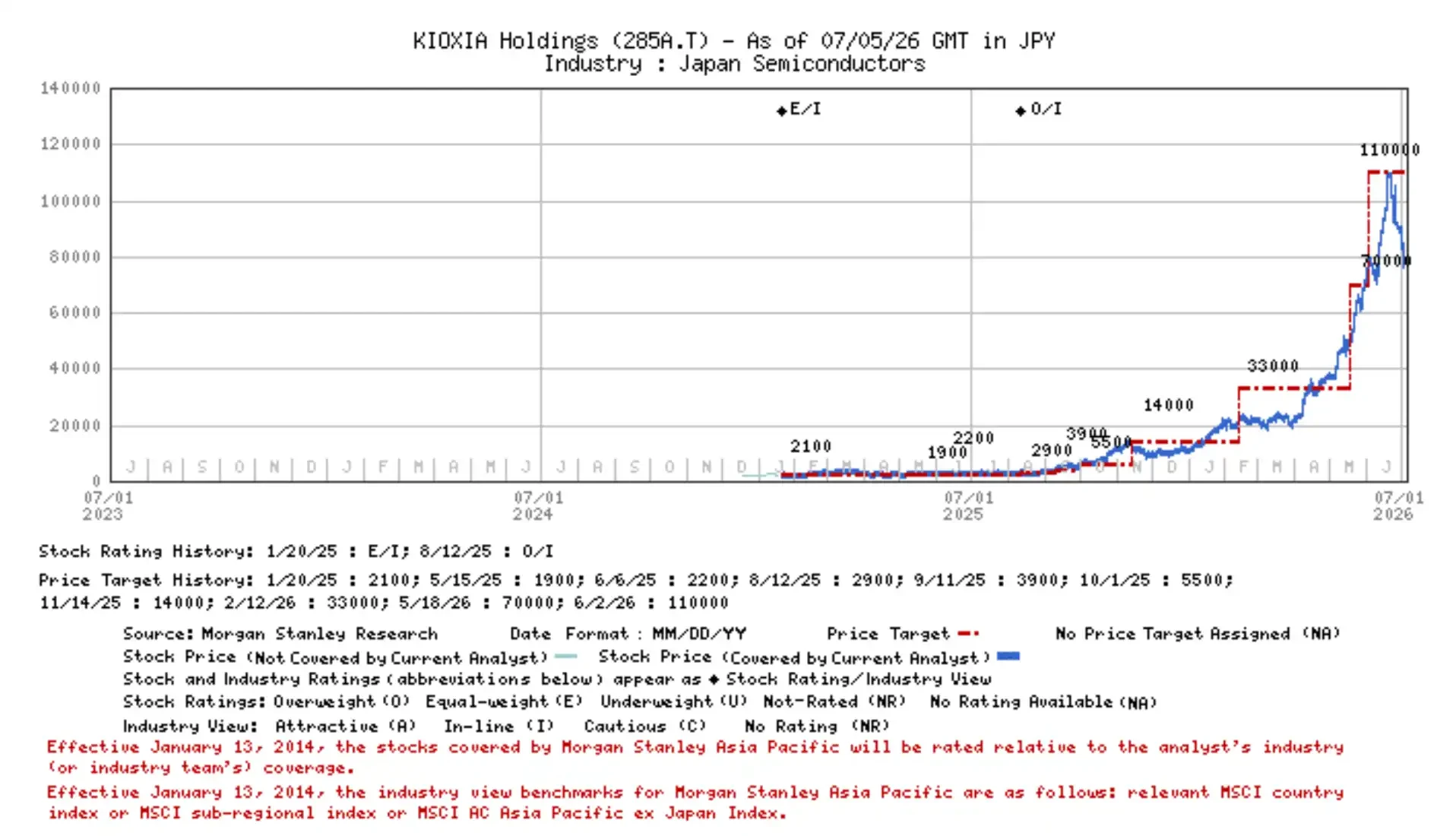

The historical stock price chart shows Kioxia's stock price at approximately 83,300 yen as of July 3, 2026, marked with an "Overweight" rating.

Discrepancies Not in Technical Parameters, But in Ramp-Up and Supply-Demand

The direction of BiCS-10 is relatively clear, but the real uncertainty lies in execution.

The first aspect is customer certification. High-end enterprise SSDs entering the cloud vendor and data center customer ecosystem need to meet performance, stability, power consumption, and long-term supply requirements. Sample shipments are just the beginning; certification time and order scale determine when BiCS-10 will make a substantive contribution to revenue.

The second aspect is K2 factory ramp-up. New process transitions typically affect yield and cost curves. Even if production lines have already started, increasing capacity utilization rates will take time. If the ramp-up is slower than expected, the unit cost advantages and bit density benefits of BiCS-10 will be delayed.

The third aspect is the industry's supply. NAND expansion by Chinese manufacturers may disrupt the global supply-demand balance, especially when demand recovery does not meet expectations, as new supply will lower prices and profit margins. Kioxia still faces changes in storage price cycles and competitive landscapes to achieve a higher revenue share from AI SSDs.

Exchange rates are also a direct risk. Morgan Stanley's sensitivity analysis indicates that for every 1 yen appreciation of the yen against the dollar, Kioxia's annual operating profit decreases by approximately 6 billion yen. For globally selling storage firms that report in yen, exchange rate fluctuations will amplify uncertainties in profit forecasts.

BiCS-10 appears more like Kioxia's ticket to conquer the AI data center SSD market, rather than a victory already realized. Short-term financial reports still depend on the increase in the share of BiCS-8 and cost reductions, while the medium to long-term focus is on BiCS-10 certification, K2 ramp-up, and enterprise SSD customer onboarding. If these steps go smoothly, the approximately 32% upside potential will have stronger support; if any of these links are delayed, technical leadership will still await confirmation in financial reports.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。