TL;DR

- Goldman Sachs expects most semiconductor sub-segments to still have room for upward adjustment in the second quarter, but the SOX index has risen approximately 87.8% in a single quarter.

- AI capital expenditures, DRAM/HBM, advanced packaging, and EDA tools are the main sources of profit upgrades this round.

- Goldman prefers AMD, AMAT, and ON, is more cautious about ARM and KLAC, and suggests maintaining limits on Qnity after its rise.

Before the semiconductor earnings season, stock prices have already run quite a bit. The Nasdaq's second-quarter review shows that the PHLX Semiconductor Index rose 87.8% in the second quarter, marking its best quarterly performance since its establishment in 1994, far exceeding the broader U.S. stock market during the same period. Goldman Sachs stated in a semiconductor second-quarter outlook that there is still room for upward adjustment in fundamentals, but the sector, after its rise, is no longer suitable for "buying all together." AI servers, memory, advanced packaging, and design software remain the strongest main lines, while the weakness in smartphones, changes in expenditure structures, and export restrictions will amplify individual stock differences.

Semiconductors still have room for adjustments, but the AI chain has begun to stratify

Goldman’s report mentions that performance or subsequent guidance from computing, memory storage, semiconductor equipment, and some analog chip companies in the second quarter may still exceed market expectations.

The main focus in the computing field remains on AI servers. Server CPU demand, cloud vendors’ ASIC projects, and AI accelerator cards continue to support data center revenue expectations for companies like AMD. Memory and storage benefit from tight supply and demand for DRAM/HBM, improving HDD pricing, and expectations for the NAND cycle, with limited additional supply pressure in the short term.

The highlights of the equipment chain lean more towards the medium term. AI servers require more HBM and advanced packaging, and the expansion and technological upgrades by memory manufacturers will drive demand in deposition, etching, and other processes. Some equipment companies’ order visibility has already stretched to 2028.

Analog semiconductors are not seeing a broad recovery. Goldman prefers companies with higher exposure in industrial, aerospace and defense, and data centers, and is more cautious about targets more reliant on the smartphone or traditional automotive cycles.

This divergence is also reflected in Goldman’s tactical choices. The report prefers Applied Materials, AMD, and ON Semiconductor, while being more cautious about ARM and KLA. For semiconductor materials and electronic solutions company Qnity, Goldman remains optimistic about the rising wafer utilization rate and execution performance but believes that with the stock price increase, the risk-reward balance has been reached, mainly from the report's perspective.

AMD and Applied Materials are Goldman’s two most clear bullish cases

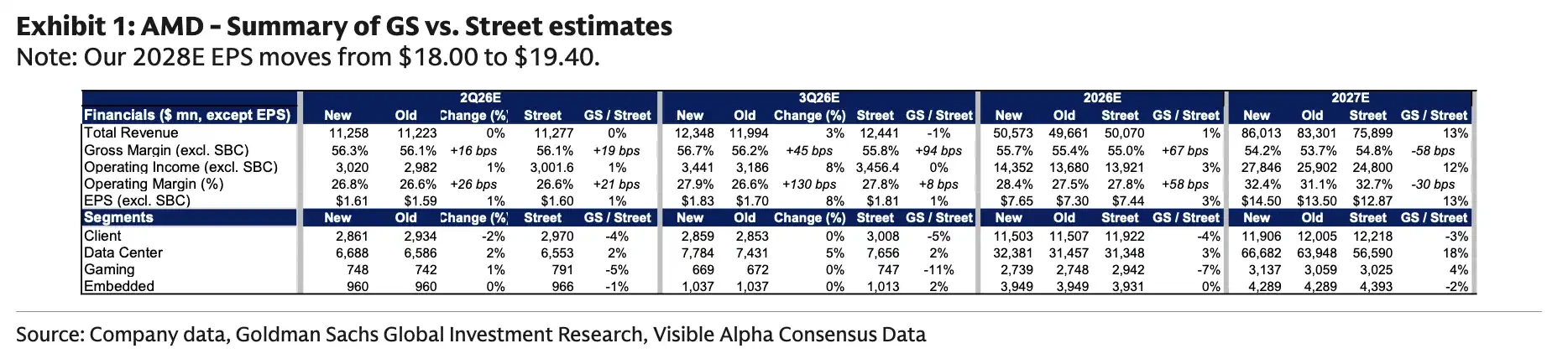

AMD is one of Goldman’s most clear bullish cases in the computing chain. Goldman’s model shows that AMD’s 2027 EPS forecast has been raised to $14.50, approximately 13% higher than the market consensus. The 2027 data center revenue forecast is $66.682 billion, about 18% higher than market expectations.

Supporting this judgment is the strong demand for server CPUs, improvement in data center business gross margins, and the operational leverage brought by the subsequent ramp-up of AI chips. AMD previously announced that the Advancing AI 2026 event will be held in San Francisco on July 23, 2026, and will be broadcast live. Outside of the earnings season, the market will focus on whether AMD can provide a clearer AI server roadmap, customer progress, and revenue rhythm during this event.

Goldman’s model shows that AMD’s 2027E EPS is $14.50, higher than the market’s $12.87. The 2027E data center revenue is $66.682 billion, surpassing the market’s $56.590 billion, driven by the ramp-up of server CPUs and MI450.

Applied Materials, on the other hand, represents a stronger end of order visibility in the equipment chain. Goldman has raised the target price for Applied Materials from $520 to $645, based on a 32 times, $20 normalized EPS valuation. The key assumption of the report is that strong DRAM investments will drive its best-in-class growth by 2026, and WFE demand visibility could extend to 2028.

DRAM is the focus here. The rising demand for HBM and high-performance memory from AI servers will drive memory manufacturers to expand production and upgrade processes. The advantage of equipment companies lies in their longer order cycles, leading to higher revenue visibility. The risk is also very direct; if cloud vendors or memory manufacturers slow down capital expenditures, the market’s expectations for medium-term revenue will quickly adjust downward.

Goldman’s model shows that AMAT's total revenue for CY2027E is $45.972 billion, a year-over-year increase of 25%. The DRAM division is expected to contribute $12.4 billion, a year-over-year increase of 41%, being the main source for equipment growth.

ON Semiconductor is positioned relatively positively in the mix, not due to substantial upward adjustments, but because short-term expectations have already eased. The company announced on June 25 its plans to acquire Synaptics in an all-stock transaction, with an enterprise value of approximately $7 billion, expected to be completed by mid-2027, still requiring the approval of Synaptics shareholders and others. Goldman believes that after a pullback in investor expectations, ON Semiconductor's quarterly performance may be slightly better than expected.

ARM and KLA illustrate: the greater the increase, the harder it is to overlook earnings flaws

Goldman maintains a sell rating on ARM, setting a 12-month target price of $150, corresponding to 50 times, $3 normalized EPS. The pressure mainly comes from two aspects: continued weakness in smartphone demand and operating expenses higher than expected.

ARM is still viewed by the market as a potential beneficiary of AI and high-performance computing, but in the short term, the most direct revenue and profit pressures stem from smartphone licensing income and cost expansion. For stocks already boosted by AI narratives, the market will be more concerned about whether recent revenue, profit margins, and guidance can be fulfilled.

KLA’s pressure comes from the structure of equipment spending. Goldman expects its quarterly performance and guidance may see a slight upward adjustment, but may still lag behind peers since WFE spending is leaning towards DRAM. Compared to logic chips and foundry services, DRAM exhibits less strength for inspection metrology equipment. The overall equipment cycle may be upwards, but this does not mean all equipment segments benefit equally.

Qnity’s situation lies in between the two. The company announced in the first quarter that its net sales for Q1 2026 were $1.315 billion and raised its annual guidance. Goldman still holds a positive view on improved wafer utilization and company execution, but the report suggests that the further upside and downside risks of its stock price increase are now more closely balanced. For stocks that have already anticipated a recovery, earnings not only need to deliver good results but also provide sufficiently strong guidance for the next stage.

EDA and Qualcomm are also pulled into the earnings test by AI

AI expectations are not limited to the GPU, CPU, and memory chain, but are also spreading to chip design software and data center chips.

Cadence is one of the companies in the EDA chain that Goldman is optimistic about. Public information shows that the company has raised its 2026 revenue outlook to approximately 17% year-over-year growth after the first quarter and has launched engineering solutions aimed at agentic AI chips and system design with NVIDIA. Goldman further anticipates that driven by the monetization of agentic AI tools, IP businesses, and core EDA demand, the company’s 2026 revenue guidance may still have upward adjustment potential.

Qualcomm’s data center business has also come back into focus. The company previously mentioned in its Investor Day materials that the data center business will contribute billions of dollars in revenue starting from FY27. Goldman’s model sets Qualcomm’s FY27 and FY28 data center revenues at $5 billion and $8.2 billion, respectively. For Qualcomm, this represents that the growth narrative is expanding from mobile chips to data centers, but orders, customers, and gross margins still need to be continuously realized.

The key question this earnings season aims to answer is straightforward: can AI capital expenditures continue to allow semiconductor companies to upgrade their earnings? Over the past quarter, stock prices have already given an optimistic outlook. Moving forward, the strength of server CPUs, ASICs, HBM, EDA, and equipment orders must enter the revenue and profit models for 2026 and 2027 for valuations post-increase to remain supported.

Whether the upgrades can catch up with the stock price determines the degree of differentiation in the earnings season

The highlights of the semiconductor second-quarter earnings season are not whether the market still has upward expectations, but whether the magnitude of the upward adjustments can cover the already risen stock prices.

Goldman’s outlook gives a more differentiated answer. AI capital expenditures, DRAM/HBM, advanced packaging, and EDA tool monetization are still pushing up profit expectations for some companies. With the SOX having significantly outperformed the broader market, the market's tolerance for flaws is declining.

Weak smartphone demand will suppress ARM, WFE leaning towards DRAM will weaken KLA’s relative advantages, and supply chain constraints, export restrictions, and geopolitical risks may also affect order fulfillment. Companies like AMD and Applied Materials, which still have room for model adjustments, will be questioned about the speed of realization. Companies that have already risen significantly, but have limited fundamental elasticity in the short term, will face greater pressure in the earnings season if their guidance is not strong enough.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。