Leveraged ETFs' rebalancing funds have become amplifiers of volatility in US stocks.

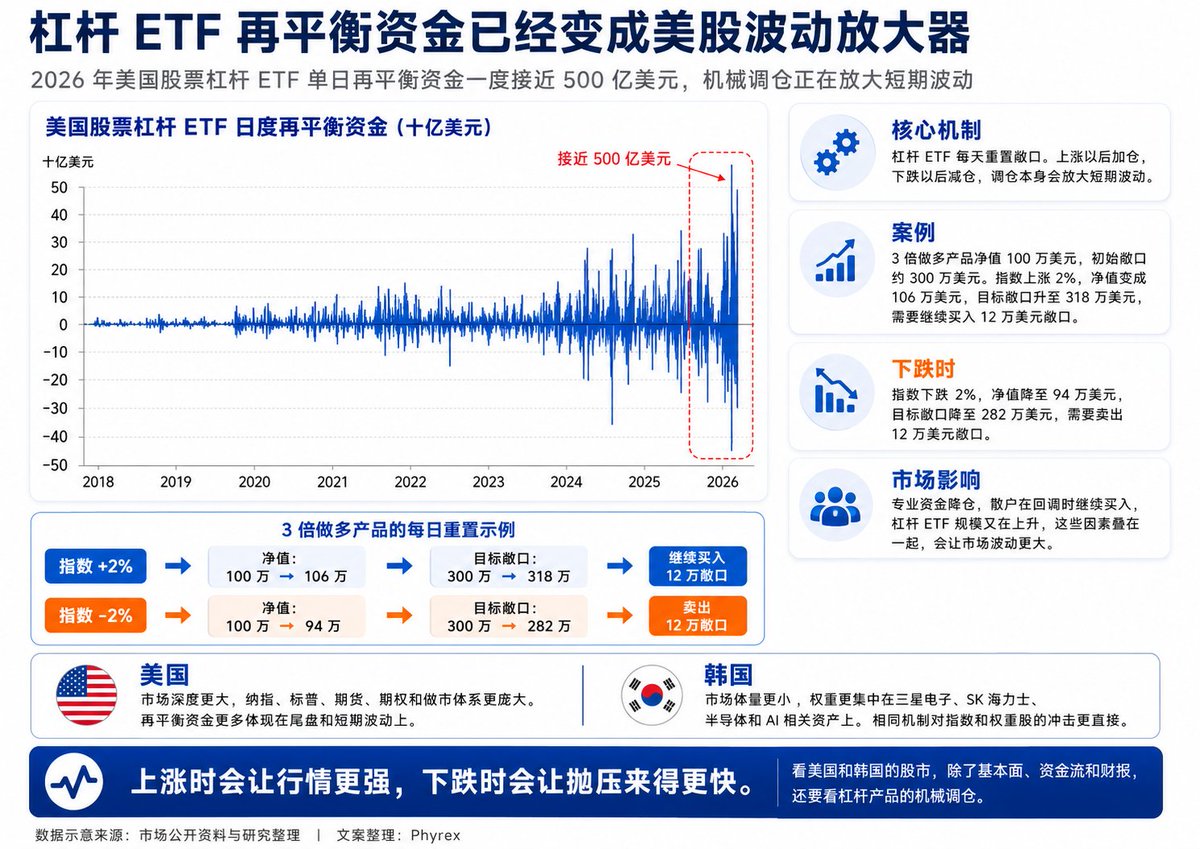

The single-day rebalancing funds of US leveraged ETFs have once approached $50 billion. This figure primarily reflects the mechanical trading generated by leveraged ETFs to maintain 2x, 3x, or more long and short leverage through passive adjustments of underlying exposures before and after daily market close.

Just today, I saw Brother Link @CryptoSociety42 discussing the issue of TQQQ, so let's take an example together.

The core of leveraged ETFs is daily rebalancing. This is the key!

For example, a 3x long QQQ ETF aims to maintain approximately 3 times the exposure every day. After the market rises, the fund’s net value increases, and to continue maintaining 3x leverage the next day, it needs to continue buying underlying assets or futures. After the market falls, the fund’s net value decreases, and it needs to sell exposure to rebalance the leverage back to the target level.

To illustrate with a simple example, a 3x long ETF managing $1 million has an initial market exposure of about $3 million. If the index rises by 2% that day, the fund's net value will rise to about $1.06 million.

On the next day, to maintain 3x leverage, the target exposure becomes $3.18 million. The original $3 million exposure, after rising, becomes $3.06 million, resulting in a difference of $120,000, which needs to be bought additionally.

If the index falls by 2%, the fund's net value will drop to about $940,000, and the target exposure changes to $2.82 million. The original $3 million exposure, after falling, has $2.94 million left, resulting in an excess of $120,000, which needs to be sold.

Thus, the rebalancing mechanism of leveraged ETFs is quite simple: increase positions after an increase, and reduce positions after a decrease. There is no directional judgment, only adherence to rules, but this mechanism itself amplifies short-term volatility.

The scale of individual products' adjustments is already significant. If you combine 2x, 3x, long, short, Nasdaq, S&P, and semiconductor leveraged products together, extreme conditions can generate mechanical buying and selling worth tens of billions or even hundreds of billions of dollars.

By 2026, the single-day rebalancing funds of US stock leveraged ETFs have approached the level of $50 billion, indicating they have become an important variable in the short-term volatility of the market.

In fact, the leveraged ETFs in South Korea operate under the same mechanism. South Korean retail investors heavily use leveraged ETFs to chase after Samsung Electronics, SK Hynix, semiconductors, and AI assets. After the market rises, leveraged ETFs continue to increase positions, pushing the market hotter; when the market falls, leveraged ETFs passively reduce positions, leading to sharper pullbacks.

The difference between the US and Korea lies in the market's capacity.

The US market has a greater depth, with large systems for Nasdaq, S&P, futures, options, and market-making; the $50 billion mostly amplifies late-day and short-term volatility. The South Korean market is much smaller, with a concentration of weights in a few semiconductor companies, and the same leveraged rebalancing mechanism will have a more direct impact on the index and weighted stocks.

Therefore, when observing the current stock markets in the US and South Korea, in addition to fundamentals, capital flow, and earnings reports, one must also consider the mechanical adjustments of leveraged products. During rises, they can make the market appear stronger, but during falls, they can also cause selling pressure to emerge more quickly.

The recent series of data we have seen indicates that professional funds are withdrawing, while retail investors are exerting pressure; whether in the US or South Korea, leveraged ETFs are increasing significantly. All of these are reasons for considerable market volatility.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。