Original Author: Andjela Radmilac

Original Compilation: Luffy, Foresight News

Cathie Wood's ARK Invest accumulated $77 million worth of shares in crypto-listed companies in June. According to ARK's daily trading disclosure data, during Bitcoin's worst monthly performance in four years, the fund increased its holdings by $44 million in Coinbase, $25.25 million in Circle, and $8.2 million in Bullish.

Wood has stuck to the same investment logic with several institutions over the years: crypto-listed companies provide investors with compliant channels to share in the cyclical benefits of the crypto industry without directly holding Bitcoin. However, an analysis of CryptoSlate's market data as of July 2 revealed the significant hidden costs of this stock investment pathway.

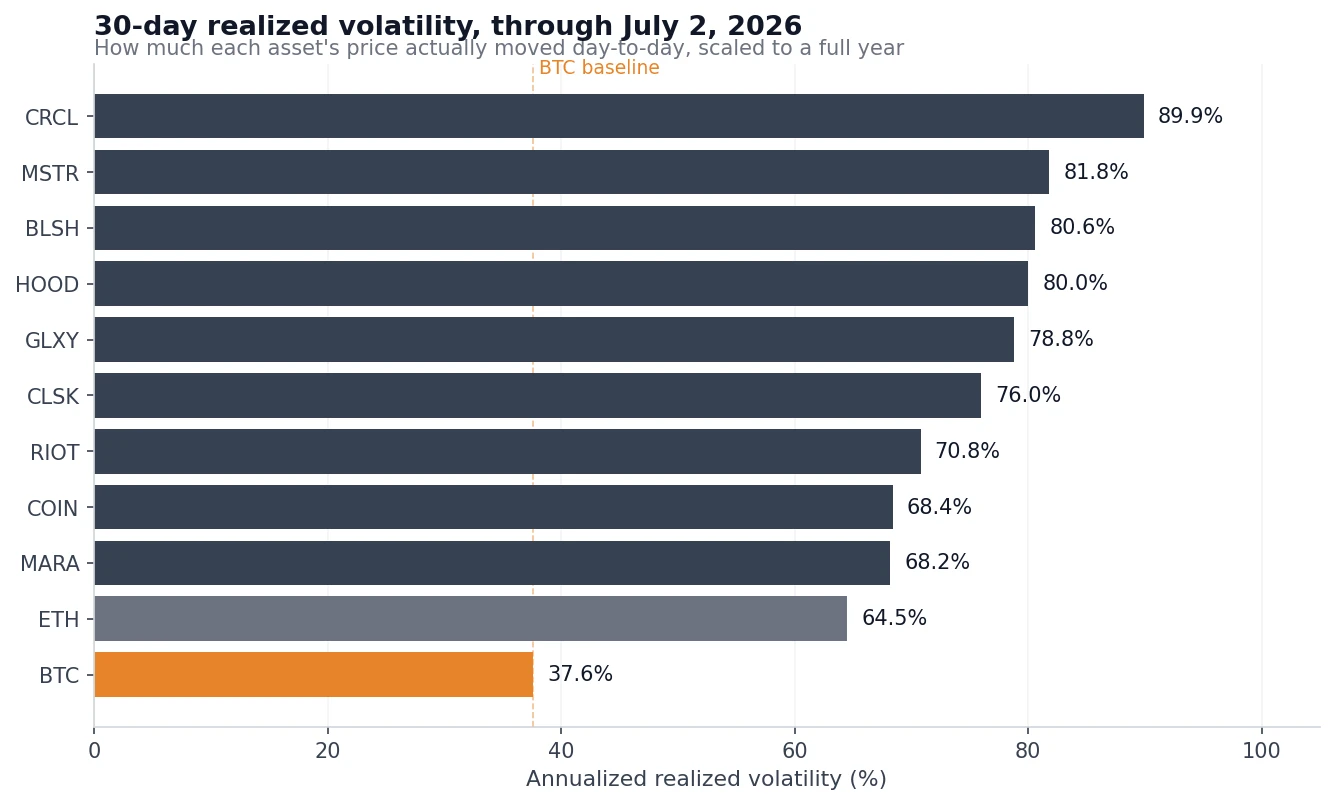

The annualized 30-day actual volatility range for nine US-listed crypto companies is 68%-90%, nearly double Bitcoin's volatility of 37.6%. Extending to a 90-day dimension, Circle's volatility soared to 103.6%, while Bitcoin's was only 37.8%. The drawdown discrepancies are likewise significant: Circle's drawdown from its peak was 51.4%, MSTR's was 48.6%, and Bullish's was 43.6%; whereas Bitcoin fell 36.4% from its nearly $97,000 peak in January, with all declines smaller than those of the mentioned stocks.

Annualized realized volatility of BTC, ETH, and nine US-listed crypto company stocks from January 1, 2026, to July 2

Looking at volatility alone, crypto stocks appear to be leveraged Bitcoin, but the correlation data reveals a completely different truth. Over the past 90 trading days, the correlation coefficients of Circle, Robinhood, and Bullish with Bitcoin were only 0.55-0.58 (with a correlation range from 0 to 1, where 1 indicates complete synchronization, and 0 indicates no correlation), meaning Bitcoin price fluctuations can only explain about a third of the volatility in crypto company stocks, while the remaining volatility stems from company-specific risks: quarterly earnings reports, industry competition, financing activities, and equity dilution from stock issuance, etc. Investors originally aimed to access the crypto industry through stocks but ended up only obtaining partial exposure to Bitcoin prices while additionally bearing a full set of business risks unique to the stock market.

Only one stock truly tracks Bitcoin

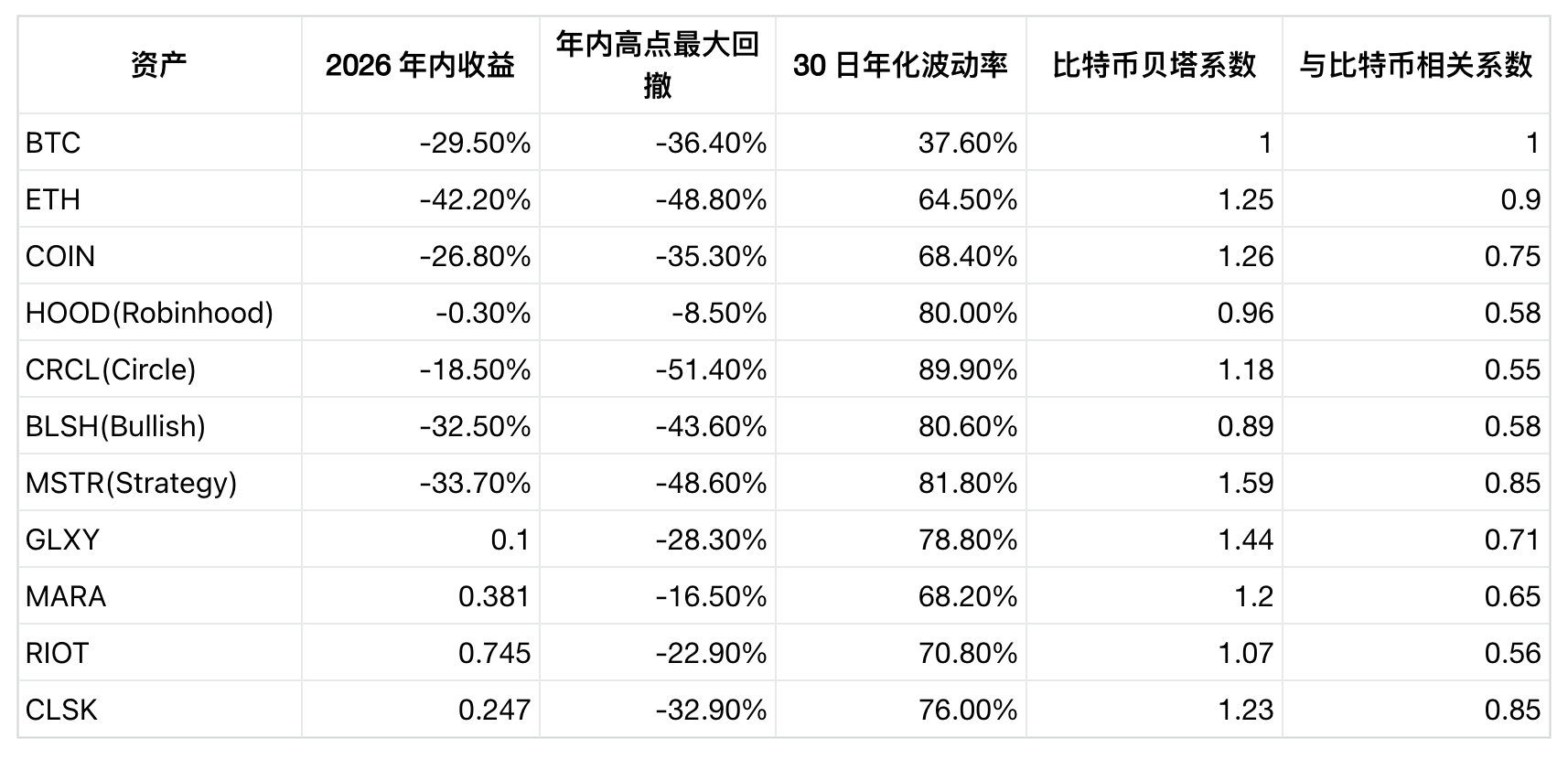

The table below summarizes the correlation of crypto company stocks with Bitcoin from the end of 2025 to the present. The beta coefficient represents the percentage change in the corresponding stock for every 1% fluctuation in Bitcoin.

Only MSTR in the entire market can be considered a substitute for Bitcoin. With a beta of 1.59 and a correlation of 0.85, it essentially acts as a leveraged equity instrument holding Bitcoin. In the recent decline, its year-to-date drop and drawdown have both far exceeded Bitcoin's.

Coinbase is a relatively balanced choice, with a year-to-date drop of -26.8%, slightly smaller than BTC, a beta coefficient of 1.26, and a correlation of 0.75, making it the second most correlated to Bitcoin in the sector. However, its volatility still approaches twice that of Bitcoin, with its stock price down 60.6% from the historical high of $419.78 in July 2025; investors who bought at that peak faced losses much greater than those who entered at Bitcoin’s historical high in October 2025.

Circle perfectly exemplifies "enterprise risks under a crypto guise." Its correlation with Bitcoin is the lowest in the entire sector, and its 90-day volatility is the highest. The trigger occurred on June 30: the official launch of the Open USD stablecoin, backed by over 140 companies including Coinbase, Stripe, Visa, Mastercard, and BlackRock, caused CRCL to plummet 17.5% in a day. This massive drop was almost entirely unrelated to Bitcoin's performance and was purely a negative from the competition for market share in the stablecoin sector.

Robinhood serves as a counter-example, also confirming the independence of individual stocks from the crypto market. The stock fell only 0.3% year-to-date, with the largest drop being only 8.5% year-to-date. The crypto business is but a small part of its overall brokerage operation in stocks, options, and derivatives, with its diversified business buffering declines; conversely, during a crypto bull market, it also struggles to provide investors with substantial gains tied to coin prices.

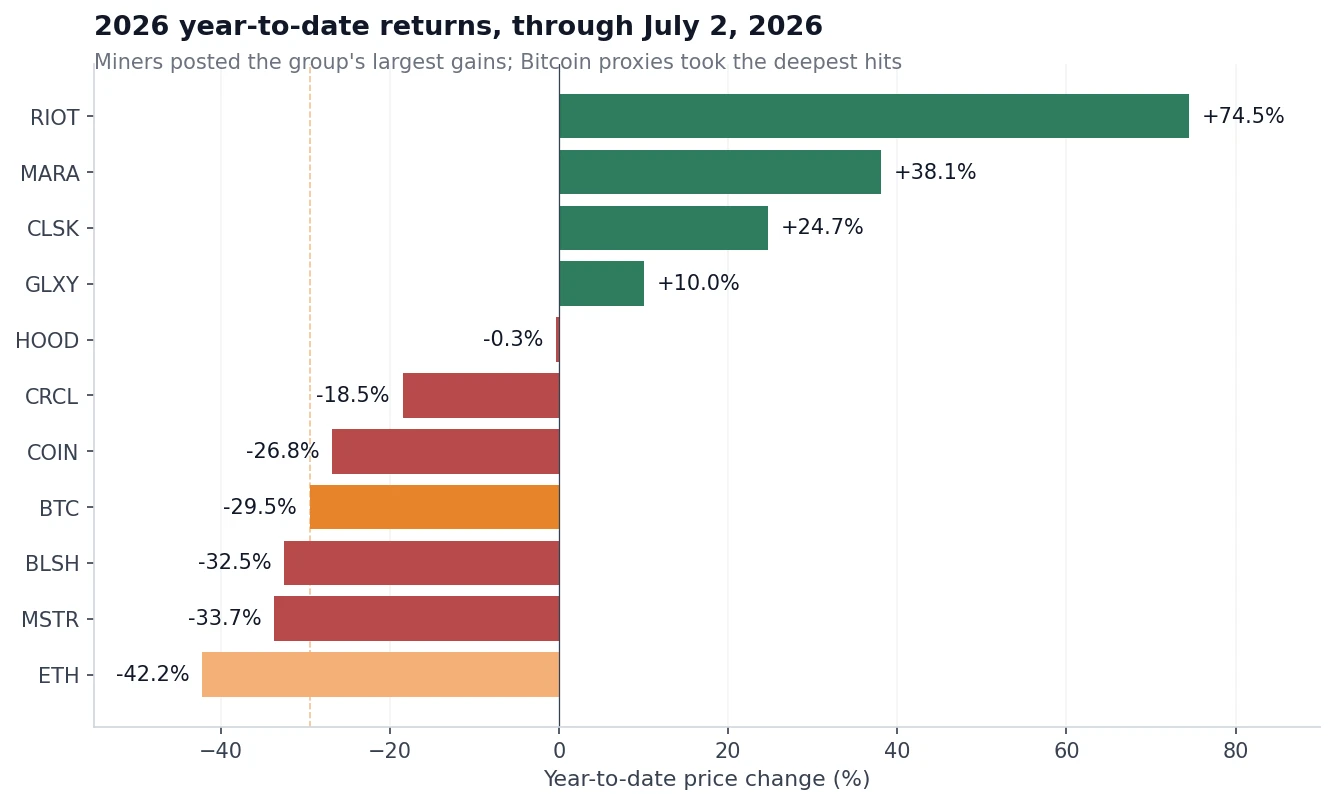

Mining companies exhibit the most anomalous trends. Bitcoin has fallen 29.5% year-to-date, while RIOT soared 74.5%, MARA increased by 38.1%, and CleanSpark rose by 24.7%. The core logic behind this is the transformation of mining companies into AI high-performance computing service providers, signing hundreds of billions of dollars in computing leasing contracts and continually reducing Bitcoin holdings. Although they still follow Bitcoin's fluctuations on a daily basis (with beta coefficients greater than 1), their annual returns are entirely driven by AI-managed operations, completely decoupling from coin prices.

Price changes of BTC, ETH, and nine US-listed cryptocurrency stocks year-to-date

Bitcoin itself is not without volatility. The Volmex Bitcoin 30-day volatility index fell to a low of 24.5 in late May, peaked at 68.7 in early February and rose to 41.6 in early July. Even so, the vast majority of crypto stocks still have doubled volatility.

Strategy Case: Equity Structure Brings Additional Risks

Holding Bitcoin only requires bearing the price fluctuation risk; buying stocks in crypto-listed companies adds layers of variables such as business performance, equity dilution, loss of valuation premiums, financing pressures, and changes in capital structure.

Strategy has recently laid bare all the hidden dangers over the past month. At the end of June, its price-to-net-asset ratio (mNAV) fell below 1 for the first time, which measures the total company valuation compared to its net assets. A ratio below 1 indicates that the market values the entire company less than its cash and Bitcoin holdings. As of June 22, it disclosed holding 847,363 Bitcoin; on the day mNAV fell below 1, the value of this batch of Bitcoin was approximately $50 billion.

An mNAV greater than 1 is the foundation of Strategy's entire growth engine. Previously, the company could issue common and preferred shares at a premium, raise funds, and continue to increase its Bitcoin holdings, enhancing the amount held per share. Once mNAV drops below 1, this cycle inversely erodes shareholder value — issuing shares for funding to buy Bitcoin is equivalent to selling existing Bitcoin assets at a discount.

CryptoSlate reported as early as January that companies holding Bitcoin fall into categories of valuation premium or discount. At the end of June, Strategy's total market value was $29.54 billion, less than half of its peak of over $71 billion in 2024, with all four types of preferred shares hitting historical lows.

Strategy announced a response plan, launching a stock buyback program of up to $1.25 billion on June 29, while authorizing the sale of Bitcoin to restore liquidity, covering preferred stock dividends and debt interest. In the weeks prior, the company made its first Bitcoin sale since 2022 on June 1, selling just 32 Bitcoin. Following the announcement, the company's stock surged 12.6% in a single day, ending an eight-day losing streak. The world's largest holder of Bitcoin had to sell assets in a bear market to generate cash flow, a constraint not encountered by directly holding Bitcoin and a unique risk of stocks.

This is precisely the background of ARK's counter-cyclical accumulation. On June 25, as crypto stocks collectively fell sharply, Wood's fund purchased $3.27 million worth of Robinhood in a single day, while simultaneously increasing its holdings in Coinbase, Circle, and Bullish. Wood believes that the long-term target price for Bitcoin is at the million-dollar level and is currently making heavy discounted investments in crypto-listed companies that have significantly corrected since their peaks in 2025.

Data reveals the true nature of these companies.

- Strategy = Leveraged Bitcoin + Equity Dilution Risk;

- Circle = Payment enterprise in the stablecoin sector, deeply mired in market share competition;

- Robinhood = Comprehensive brokerage, with crypto as just a sideline.

Wood's comprehensive purchase of these company stocks essentially bets on different combinations of business models, with varying strengths of crypto exposure among each.

Each individual stock has its own independent investment logic: Coinbase has outperformed Bitcoin year-to-date, Robinhood has maintained its early-year price, while the mining sector has led overall returns. Yet the core question remains: does buying crypto stocks genuinely carry less risk than directly holding coins?

The data from the nine listed companies indicates that stocks either amplify Bitcoin volatility or add layers of business risks unrelated to coin prices.

This year, the truly strong cryptocurrency stocks rely on independent growth businesses such as AI computing, brokerage traffic, and payment products, with Bitcoin being a secondary influencing factor.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。