Options Classroom (Part Two) Let me translate this trading method of options

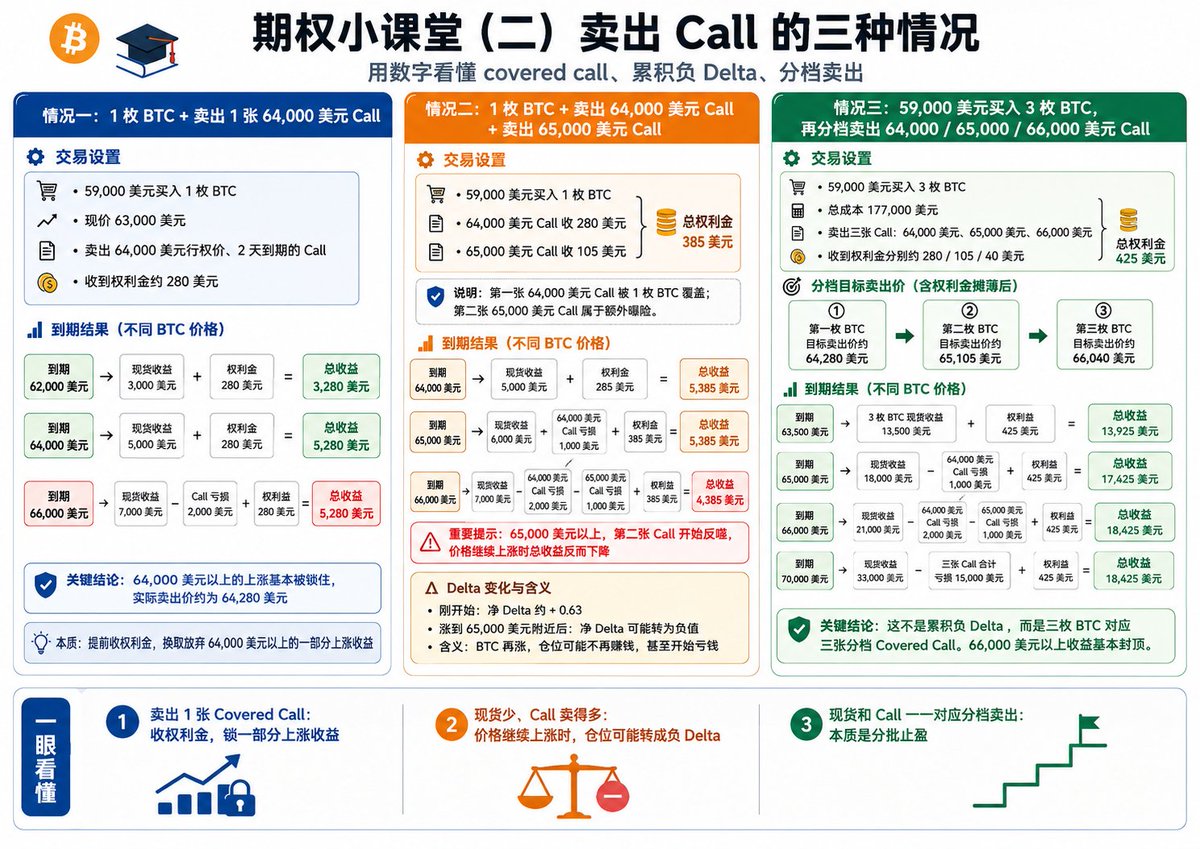

Assume @CryptoRounder bought 1 bitcoin:native spot at $59,000.

Now that BTC has rebounded to $63,000, his paper profit is:

63,000 - 59,000 = $4,000

If he does nothing at this point, he is purely a spot long, for every $1,000 rise in BTC, he probably earns an additional $1,000, and for every $1,000 drop in BTC, he probably loses $1,000.

Then he starts selling calls.

For example, he sells a BTC call option with a strike price of $64,000 and an expiration in 2 days; the Delta at this point in the screenshot is approximately 0.26, and the annualized return is about 81%.

This 81% annualized translates to an actual premium of approximately:

64,000 × 81% × 2 / 365 ≈ $284

So he sells this call and collects approximately $280 in premium initially.

At this point, his position changes to:

1 BTC spot = +1 Delta

Selling 1 64K call = -0.26 Delta

Net Delta = +0.74

In plain terms, if BTC rises another $1,000, he theoretically earns around $740, not the original $1,000 from pure spot. The upside profit is reduced, but he has received $280 in option fees.

Of course, the Delta friends do not need to worry; in any case, he has received some premium in advance. The lower price is the most cost-effective, while the upper price will earn a bit less. Moving on

At expiration, there will be several outcomes.

If BTC expires at $62,000, this $64,000 call expires worthless, no need to settle, and he keeps the full $280 premium.

His total profit (paper profit + actual profit) is:

Spot profit: 62,000 - 59,000 = $3,000 (paper profit)

Option profit: +$280 (actual profit)

Total profit: $3,280

If BTC expires at $64,000 (which is actually unlikely, it's just an example), the call essentially incurs no extra loss, and he still takes away $280.

His total profit is:

Spot profit: 64,000 - 59,000 = $5,000 (paper profit)

Option profit: +$280 (actual profit)

Total profit: $5,280

If BTC expires and rises to $66,000, then the 64K call sold is breached.

If settled in cash:

Spot profit: 66,000 - 59,000 = $7,000 (actual profit)

Loss from selling call: 66,000 - 64,000 = -$2,000 (actual loss)

Premium income: +$280 (actual profit)

Total profit: 7,000 - 2,000 + 280 = $5,280

So it can be understood that if it exceeds the selling price ($64,000), regardless of what the final BTC price is, his profit is locked close to a fixed range (around $5,280).

This means "breaching leads to settlement".

Then there is another type of cumulative negative Delta which looks quite complex, but is not difficult.

Assuming he still has 1 BTC spot, purchased at $59,000. Now BTC rebounds to $63,000, and he begins selling calls.

The first one sold is a call with a strike price of $64,000, assuming a premium of $280 is received. This call means that if BTC rises above $64,000 at expiration, he is willing to sell this BTC for $64,280. Because he has 1 BTC spot, this call is covered by the spot.

Then he sells a second call with a strike price of $65,000, assuming he receives another $105 in premium. At this point, he has received a total of $385 in premium from the two calls.

The problem lies with the second call.

Because he has only 1 BTC spot, the first $64,000 call has basically locked in the upside profit above $64,000 for this BTC. Selling the second $65,000 call is equivalent to additionally selling a call without spot coverage.

If BTC expires at $64,000, the spot price rises from $59,000 to $64,000, with a profit of $5,000 in the spot. Both calls have no loss, and adding the received $385 premium, the total profit is $5,385.

If BTC expires at $65,000, the spot rises from $59,000 to $65,000, making a profit of $6,000 in the spot. However, the $64,000 call has been breached, leading to a loss of $1,000. The $65,000 call is exactly at the strike price and has not incurred an additional loss.

In the end, the profit is 6,000 - 1,000 + 385 = $5,385.

This means that the total profit did not increase when BTC rose from $64,000 to $65,000, because the $1,000 increase was offset by the first call.

If BTC expires at $66,000, the spot rises from $59,000 to $66,000, yielding a profit of $7,000 in the spot. However, the $64,000 call will incur a loss of $2,000, and the $65,000 call will also begin to incur a loss of $1,000.

In the end, the total profit is 7,000 - 2,000 - 1,000 + 385 = $4,385.

BTC rising from $65,000 to $66,000 results in only $1,000 more in the spot, but the two calls together incur a loss of $2,000, leading to a total profit decrease of $1,000.

This is the meaning of cumulative negative Delta.

Of course, if there are spots of Bitcoin at these three positions, it would be a different matter.

Assume he bought 3 BTC at $59,000, with a total cost of:

59,000 × 3 = $177,000

Now BTC rises to $63,000, and he begins to sell calls in batches.

Selling three calls:

The first is a call with a strike price of $64,000, assuming he receives a premium of $280.

The second is a call with a strike price of $65,000, assuming he receives a premium of $105.

The third is a call with a strike price of $66,000, assuming he receives a premium of $40.

The three calls yield a total of: 280 + 105 + 40 = $425

The structure means dividing the three BTC into three tiers for sale:

The first BTC is willing to sell at 64,000 + 280 = $64,280.

The second BTC is willing to sell at 65,000 + 105 = $65,105.

The third BTC is willing to sell at 66,000 + 40 = $66,040.

If at expiration BTC is below $64,000, for example at $63,500, all three calls expire worthless. He still holds 3 BTC while receiving $425 in premium, making the profit:

4,500 × 3 = $13,500

Adding the premium of $425, the total profit is:

13,500 + 425 = $13,925

If BTC expires at $65,000, the three BTC would earn a total of:

65,000 - 59,000 = $6,000

6,000 × 3 = $18,000

However, the sold $64,000 call has been breached, incurring a loss of:

65,000 - 64,000 = $1,000

The other two $65,000 call and $66,000 call have not incurred losses yet.

So the total profit is:

18,000 - 1,000 + 425 = $17,425

This is equivalent to the first BTC being sold near $64,280, while the other two BTC continue to benefit from the rise.

If BTC expires at $66,000, the three BTC would earn a total of:

66,000 - 59,000 = $7,000

7,000 × 3 = $21,000

However, the $64,000 call incurs a loss of:

66,000 - 64,000 = $2,000

The $65,000 call incurs a loss of:

66,000 - 65,000 = $1,000

The $66,000 call hits exactly the strike price, incurring no additional loss yet.

So the total profit is:

21,000 - 2,000 - 1,000 + 425 = $18,425

This is equivalent to the first two BTC being sold near $64,280 and $65,105 respectively, while the third BTC is still waiting for delivery near $66,040.

If BTC rises to $70,000, the three BTC would earn a total of:

70,000 - 59,000 = $11,000

11,000 × 3 = $33,000

However, all three calls are breached:

$64,000 call incurs a loss of $6,000

$65,000 call incurs a loss of $5,000

$66,000 call incurs a loss of $4,000

All three calls collectively incur a loss of:

6,000 + 5,000 + 4,000 = $15,000

Finally, the total profit is:

33,000 - 15,000 + 425 = $18,425

Thus, once BTC rises above $66,000, the profit is basically capped.

This is the core of this strategy.

Buying 3 BTC at $59,000, then selling calls at $64,000, $65,000, and $66,000 after rebounding to $63,000. This means setting three selling positions in advance, just without directly placing a spot sell order, but instead collecting a premium first by selling calls.

If BTC does not rise, he continues to hold BTC and earns additional premiums.

If BTC rises, he will sell BTC step by step at $64,000, $65,000, and $66,000.

If BTC surges to $70,000, he will not benefit from the rise above $66,000, as the upside profits from the three BTC will be offset by the three calls.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。