TL;DR

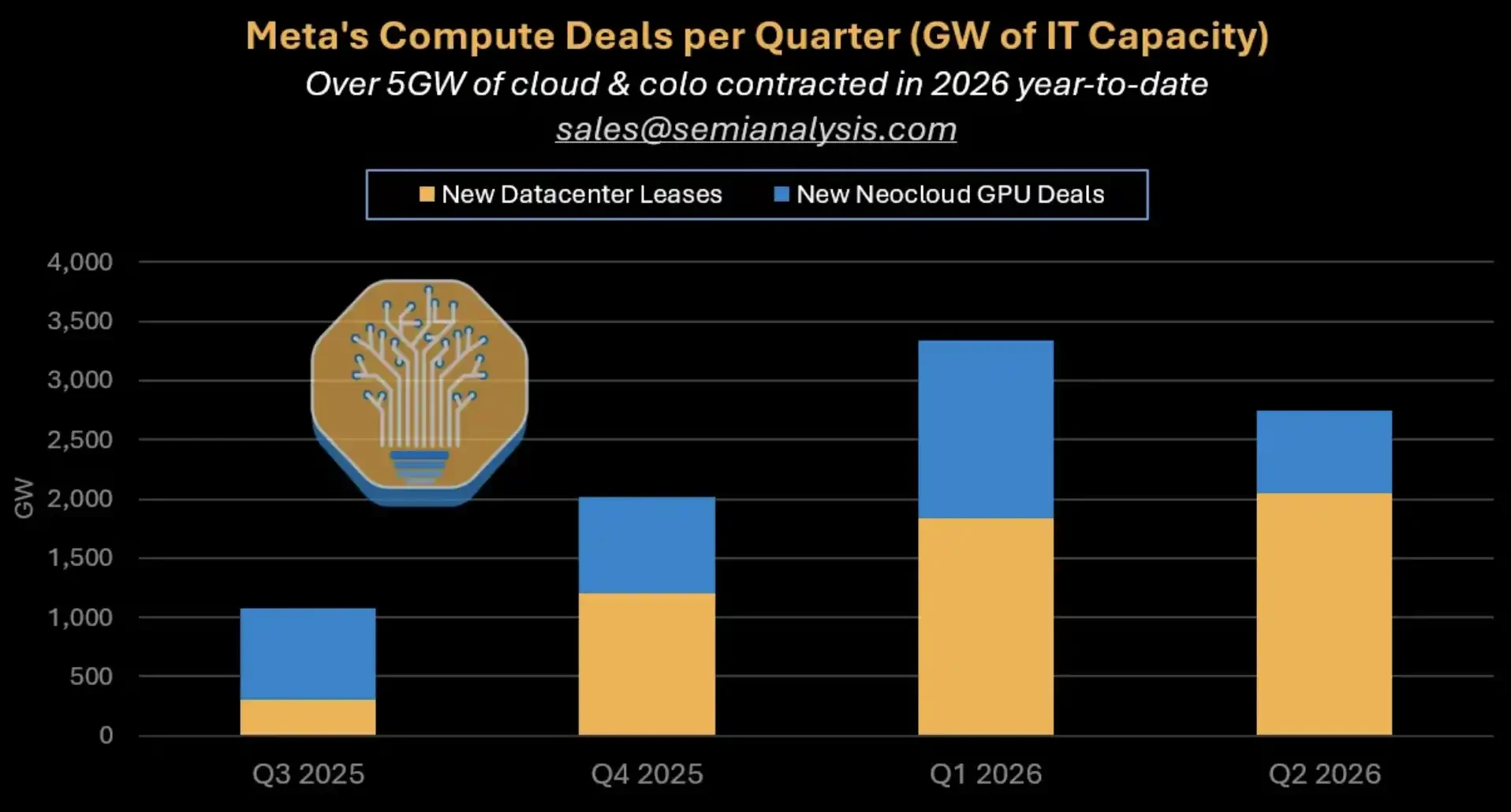

- Meta signed over 5GW capacity in cloud and hosting in the first half of the year, excluding the self-built data centers that are being developed simultaneously.

- The new computing power can flow into MSL training, ad recommendations, private instances of Claude, and short-term high-priced external transactions.

- CoreWeave and Nebius's RPO may benefit, but the catch-up of MSL and contract flexibility remain risks.

The Neocloud sell-off triggered by Meta may have bet on the wrong direction. SemiAnalysis released a report on July 2 stating that Meta has signed over 5GW of IT capacity in cloud services and hosting by the first half of 2026, and this figure does not include the self-built data centers that are being accelerated simultaneously.

This is contrary to the market's worries in recent days. According to a Bloomberg report on July 1, Meta is developing a business to sell excess AI computing power in the cloud, with related plans still under development and strategies subject to change. Following this news, shares of Neocloud companies like CoreWeave and Nebius faced a sell-off, as investors worried that Meta would shift from being a major customer to a potential competitor, leading to an excess supply of AI data centers.

SemiAnalysis provides another explanation: Meta is not reducing its outsourcing but is using third-party Neocloud to obtain capacity faster. Since early 2024, Meta has signed nearly 10GW in contracts, with most of the new capacity still being fulfilled through third parties. For suppliers like CoreWeave and Nebius, Meta's orders might continue to push up the remaining performance obligations, i.e., RPO.

Meta quarterly computing power transaction breakdown: over 5GW cumulatively signed in cloud and hosting in the first half of 2026, distinguishing new data center leases from Neocloud GPU transactions.

Market Worries Meta Becomes a Seller, Report Sees a Larger Buyer

The focus of this controversy is not whether Meta will enter the cloud computing resale business but rather who will build the newly massive computing power, who will absorb it, and who will bear the revenue risk.

If Meta simply leases out GPUs and becomes a bare-metal IaaS provider with a gross margin of about 30%, the market's concerns over Neocloud's valuation would make sense. When a major customer starts supplying, the bargaining power of existing suppliers may be weakened, and the industry could enter low-price competition.

However, in the framework provided by SemiAnalysis, the additional capacity from Meta resembles a "pool of optional computing power." It can allocate resources between internal cutting-edge models, ad recommendations, enterprise-level model services, and high-priced external transactions, instead of merely low-cost GPU leasing.

This is also the key to countering the claim that "only 5GW of data centers are under construction in the U.S." Meta's two largest construction parks alone correspond to about 2.5GW of capacity under construction. When combined with third-party cloud and hosting contracts, the actual construction intensity is higher than some pessimistic estimates.

To put it more directly, what the market needs to judge now is not whether Meta buys computing power but whether so much capacity can be absorbed by high-value scenarios.

Four Ways to Absorb New Computing Power, MSL Is Not the Only Outlet

Meta's first priority for new computing power remains Meta Superintelligence Labs, abbreviated as MSL, for training cutting-edge models. This is the most direct narrative of capital expenditures: Meta needs to catch up with OpenAI and Anthropic, requiring a sufficiently large training cluster, talent, and room for trial and error.

However, even if MSL's progress does not fully meet expectations, Meta does not have to resort to low-priced GPU leasing.

The second avenue is the ad recommendation system. Meta's official financial report shows that in the first quarter of 2026, ad impressions grew by 19% year-on-year, while the average unit price increased by 12%. Meta Engineering previously introduced that the GEM-related training stack effectively trained FLOPs increased by 23 times, MFU improved by about 1.43 times, and the GPU scale expanded 16 times; after doubling the GEM training GPU, the conversion rates for Instagram and Facebook Feed ads increased by 5% and 3% respectively.

This path is easier for investors to understand: if more computing power can enhance ad conversion rates, it is not merely "burning money to buy GPUs," but rather part of the ad revenue and pricing capability. As for the certain order metrics improvement mentioned in the report, publicly available independent data is limited and is better suited as assumptions in the SemiAnalysis model rather than confirmed facts from Meta.

The third avenue is a model service platform, similar to AWS Bedrock or Google Vertex. SemiAnalysis stated that Meta is negotiating with Anthropic regarding private instances of Claude and is attempting to build a "token-as-a-service" platform. This type of capacity can be utilized internally as well as sold on SaaS or distributed externally, but related transactions still need to be viewed with the prospect of "possible realization," rather than as already realized revenue.

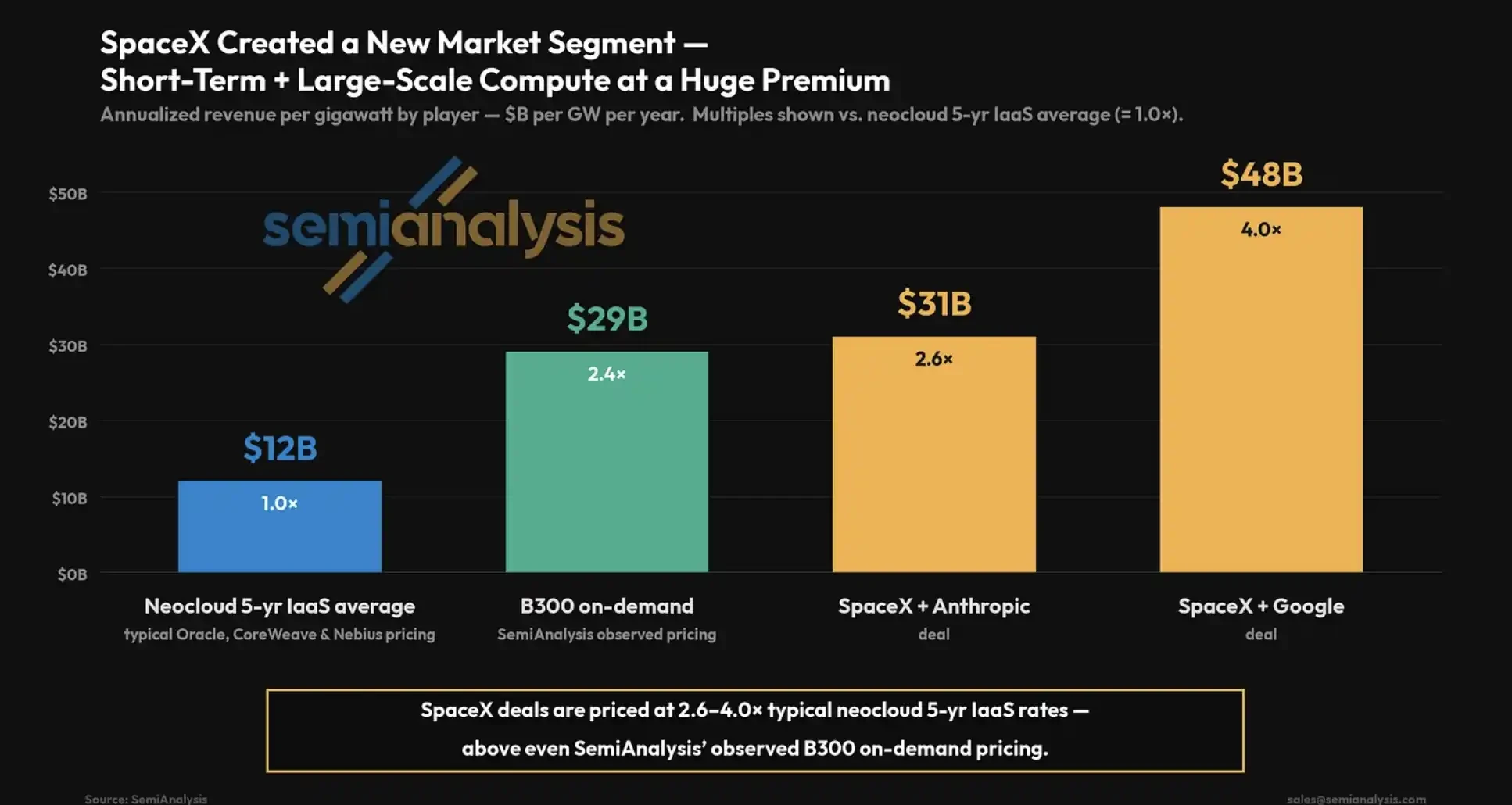

The fourth avenue is large-scale, short-term, and high-premium on-demand computing power transactions similar to SpaceX. This is also the most impactful group of numbers in the report.

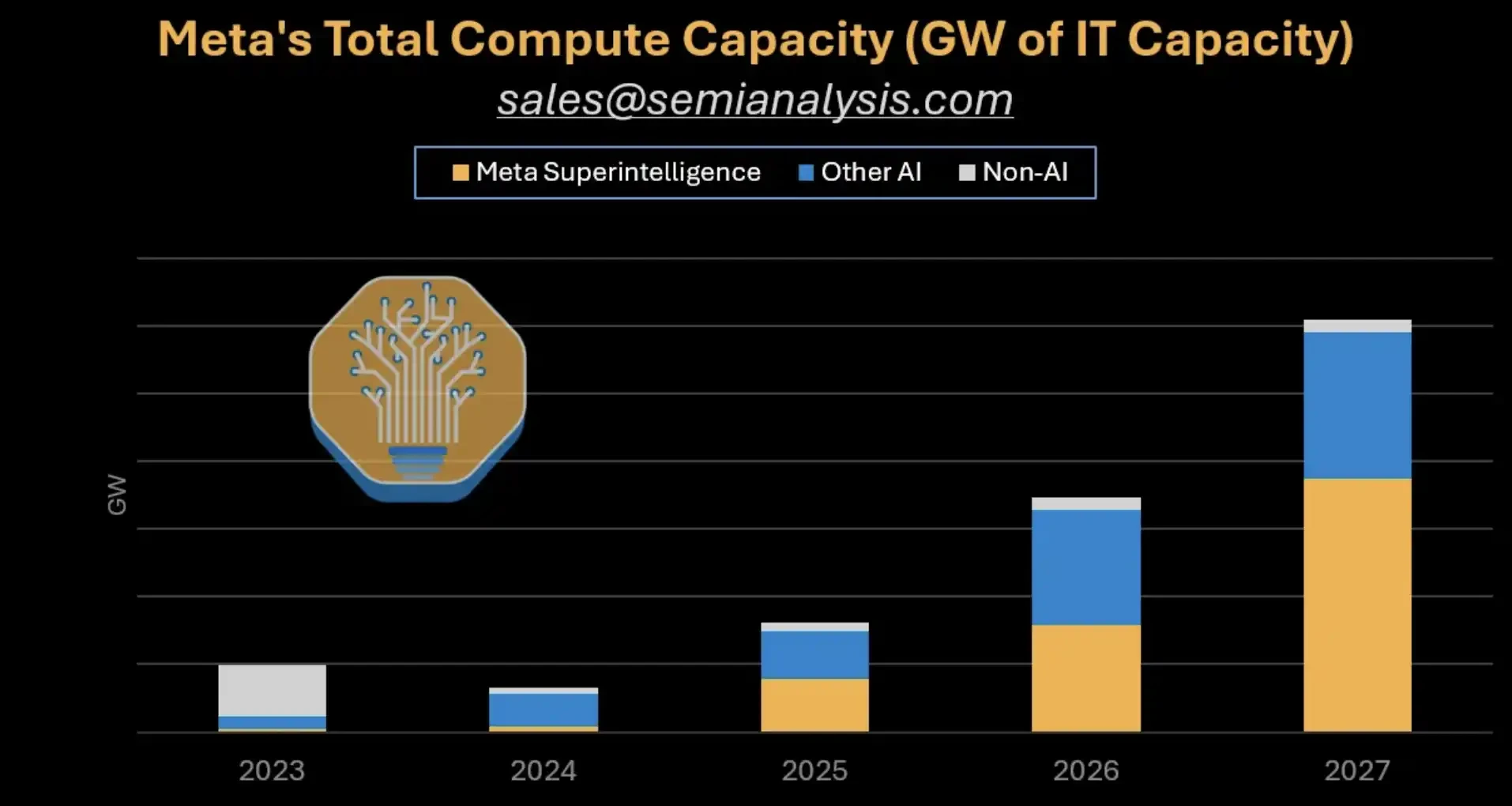

Meta total computing power capacity forecast: from 2023 to 2027, the stacked column chart distinguishes MSL, Other AI, and Non-AI, with significant capacity expansion from 2026 to 2027.

High-Priced Short-Term Contracts Change Revenue Expectations for "Selling Computing Power"

The key to SpaceX-like transactions is not merely "renting GPUs" but the differences in pricing and contract structures.

SemiAnalysis estimates that the annualized revenue per GW from SpaceX's transaction with Anthropic is about $3.1 billion, which is 2.6 times the typical five-year IaaS average of Neocloud; the contract with Google is even higher, around $4.8 billion/GW/year, equivalent to 4 times. Independent public sources have limited confirmation of these contract details, so this set of numbers is better suited as scenarios in the report to illustrate that there may be high premiums for tight short-term computing power.

If Meta only offers 200MW for similar external transactions, based on the report's public page calculations, the annualized revenue could exceed $10 billion. This scale is enough to change the market's intuition about "Meta externally selling computing power": it does not necessarily have to be low-margin leasing, but may also involve quickly launched data center capacity sold to major clients urgently needing computing power.

The report also mentions that Meta's fast-launch data center design is compatible with such transactions. Its value is not in long-term rental at the lowest cost, but in its ability to deliver quickly when model companies, AI applications, or large clients temporarily need a large amount of computing power.

However, this remains an optional path, not stable realized revenue. Meta may replicate a portion of the high-premium transaction structures, but that does not mean it has become a SpaceX-like computing power seller.

SpaceX pricing premium comparison: typical Neocloud five-year IaaS approximately $1.2 billion/GW/year, SpaceX and Anthropic approximately $3.1 billion, SpaceX and Google approximately $4.8 billion.

CoreWeave and Nebius's Pressure May Not Come from Demand Disappearing

For Neocloud companies like CoreWeave and Nebius, the prior market concern was: if Meta builds or resells computing power, the original external procurement would decrease, and industry orders might be drawn away.

However, based on existing contracts, Meta is still accelerating its use of third-party Neocloud. Public data shows that CoreWeave has a $21 billion contract with Meta, and Nebius's contract with Meta can reach a maximum of $27 billion. In its shareholder letter for Q1 2026, Nebius noted that it secured its second major contract with Meta, with contract capacity exceeding 3.5GW, and mentioned commitments from Microsoft and Meta clients.

Meta’s willingness to pay a premium for speed is also why third-party suppliers still have value. As long as Meta believes that the computing power can be absorbed by MSL, advertising systems, model services, or high-priced short-term trading, there are reasons for Neocloud to build clusters first rather than waiting for self-built projects to be delivered slowly.

"Overcapacity" should not only focus on the total GW number. The truly scarce part of AI data centers is often not just the theoretical power but also the available GPUs, network, room delivery speed, customer migration costs, and contract flexibility. If Meta needs to quickly secure large amounts of capacity, third-party Neocloud remains useful.

This does not mean that Neocloud companies are without risk. Their valuations still depend on customer concentration, financing costs, GPU depreciation, long-term contract quality, and whether clients truly consume future capacity. The growth in RPO brought by Meta, if accompanied by high capital expenditures and high customer concentration, will still be discounted by the market.

If MSL Cannot Catch Up, 5GW Will Become Capital Expenditure Pressure

The report's most necessary restraint is not to portray every optional path for Meta as already successful.

There remains significant uncertainty about whether MSL can catch up with OpenAI and Anthropic. Competing in cutting-edge models is not solely a matter of GPU numbers; data strategy, research teams, training stability, product distribution, and inference costs will all impact the outcomes.

Contract terms can also affect the level of risk. SemiAnalysis states that transactions similar to SpaceX typically contain 90-day mutual cancellation clauses. This arrangement gives both buyers and sellers flexibility: if a team is not progressing well, the computing power can be quickly reclaimed; if demand changes, they will not be locked in for the long term. Details of relevant clauses lack public independent confirmation and are more suited to be treated as report assumptions.

For Meta, flexibility itself has value. It can first reserve enough power and GPUs for MSL to conduct cutting-edge attempts, while directing some capacity towards ad recommendations, private instances of Claude, or high-priced short-term contracts.

Conversely, if Meta ultimately signs a large number of long-term computing power transactions that lack flexible exit arrangements, the risk will increase. Once the cutting-edge models fail to catch up, and ad and model services cannot absorb the newly added capacity, the surplus computing power exceeding 5GW will more directly become pressure on capital expenditures.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。