Original Author: Long Yue

Original Source: Wall Street Insight

A piece of news about Meta selling excess computing power brings several of the most sensitive issues in AI trading to the forefront: Is there really a shortage of computing power? Will Meta reduce its capital expenditure? How long can Neocloud still be profitable?

Wall Street Insight mentioned that Meta is formulating a cloud business plan that may offer two types of services externally: one is managed models/API access, similar to AWS Bedrock; the other is rental of "raw computing power" like Neocloud.

As soon as the news broke, shares of the new generation GPU cloud star provider CoreWeave plummeted 13%, Nebius fell 15%, and the AI hardware sector, including chips, faced a severe setback. If Meta starts selling computing power, investors will naturally question three things:

First, did Meta overpurchase computing power?

Second, is Meta no longer making significant investments in models and AI products?

Third, will the demand curve for AI hardware and Neocloud change?

According to news from the Fengfeng Trading Desk, on July 1, UBS, Morgan Stanley, and Bernstein quickly analyzed this event. This may not be a collapse of AI fundamentals, but rather a pragmatic move by the tech giants to find a balance between computing constraints and financial returns. This event should not simply be equated with "Meta no longer needs computing power." However, it has different implications for different assets.

For Meta, renting out computing power may serve as a transitional bridge for income and EPS. UBS assessed: “Selling cloud computing power or model access rights will theoretically bring in quicker recent income compared to waiting for Meta Business Agents and Meta AI chatbots to scale, and ease concerns about flat or declining EPS in 2027.”

For companies like CoreWeave and Neocloud, this is a potential competitive pressure.

For the chip and server chains, the market is more concerned about whether the pace of subsequent capital expenditure will change.

"Having spare capacity for rent" does not equal "industry-wide computing power surplus."

The market trades in the shortest possible terms: Renting out computing power = computing power surplus = capital expenditure reduction.

Meta may have a phase of computable rented power, but this does not automatically equate to a surplus across the entire industry. Different institutions use different capacity metrics and cannot be directly aggregated.

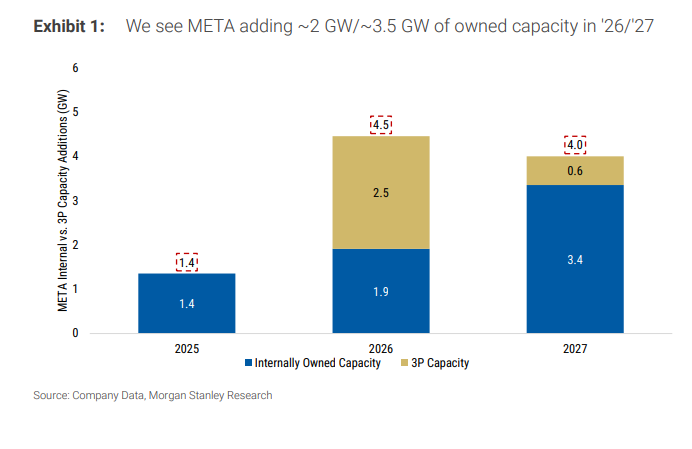

In Morgan Stanley's model, Meta is expected to add about 2GW and 3.5GW of its own operational IT capacity in 2026 and 2027, respectively, against a baseline of about 3GW by the end of 2025. By contrast, supercloud providers like Amazon and Google may add IT capacity levels of 5GW and 9GW by 2027. In other words, even if Meta rents out part of its owned capacity, it will be difficult to independently change the overall investment agenda of cloud providers in the next three years.

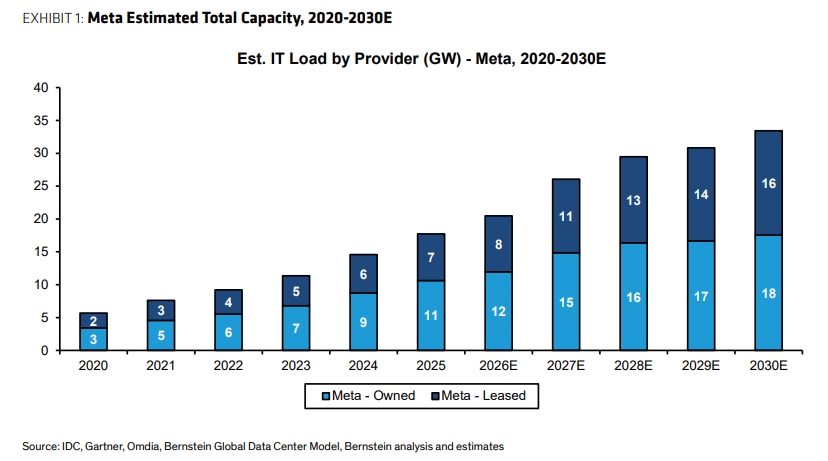

Bernstein uses a broader total data center footprint metric: Meta's current global capacity is estimated at about 20GW, and it will add about 14GW over the next few years, including a mix of owned and leased capacity. This number looks substantial, but it does not represent "all rentable AI computing power," nor does it equate to GPUs of the same generation, the same load, or the same price curve.

There is also a more aggressive reverse estimation method in market calculations: using contracts and capacity plans from Google with Anthropic, AWS with Anthropic/OpenAI, and Microsoft with OpenAI as anchors, the total AI computing power of several cloud providers may be around 20GW or even higher; OpenAI's Stargate itself and the 10GW arrangements related to Nvidia and Broadcom are included as demand-side observations. The function of this measure is not to provide precise predictions, but to illustrate one point: Meta's partial rental does not suffice to prove that global AI infrastructure has entered into surplus.

Interestingly, Bernstein also noted over the weekend that Google reportedly restricted Meta's computing usage due to its own capacity limitations. If this claim holds, while Meta is still seeking external computing power, it is also preparing to sell part of its computing power externally in the future. This resembles a reallocation of resources across different generations, different uses, and different time windows, rather than simply "having excess capacity."

This is not the first time Meta has brought up "selling computing power."

On May 27, 2026, a shareholder asked whether Meta would develop cloud services and compete with AWS and Azure. Zuckerberg responded:

“Of course, this is definitely within our consideration... We haven't done that yet because we believe we can use this computing power ourselves. But clearly, if we reach a point where we feel we're overbuilding, that's one of the options we have, which is also part of why we are confident in continuing to invest in building.”

Earlier, on October 29, 2025, Zuckerberg also discussed similar logic:

“Any computing power we don’t need, we are quite confident that we can absorb a very large portion of it... Of course, it is possible that we may overbuild. If we really do... We see significant new demand from both internal and external sources. Almost every week, external companies come to us, hoping we can build API services or asking if they can obtain different types of computing power from us. We haven’t done that yet. But clearly, if you reach a stage of overbuilding, this can become an option.”

This explains why UBS called it "not new news."

For Meta shareholders, selling computing power seems more like an "EPS bridge," not a new main business.

For Meta, the most direct benefit of renting out computing power is converting long-term AI investments into short-term income.

In UBS's table, Meta's diluted EPS for 2026 and 2027 is about $32.6 and $33.0, respectively, and the market is concerned that EPS in 2027 will be essentially flat or even contract compared to 2026. Renting out computing power or selling model access rights can at least provide a period of revenue and profit buffer before Meta Business Agents and Meta AI chatbots are genuinely scaled up.

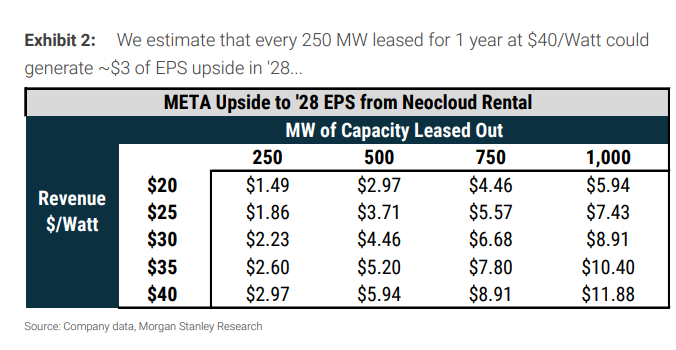

Morgan Stanley's sensitivity calculation is more intuitive: each time 250MW of computing power is rented for a year at a price of $40/Watt, it could bring approximately $2.97 in incremental EPS for Meta in 2028, which is about an 8% upside potential. If the capacity expands to 500MW, 750MW, or 1000MW, or if the price changes, the EPS elasticity will continue to amplify or shrink.

This is also why the market does not interpret this solely as negative news. From the perspective of Meta shareholders, Zuckerberg simply gained an exit strategy: if the internal AI products cannot consume all the computing power in the short term, they can be sold to external AI labs to recoup some of the investments.

The market also draws a comparison with xAI renting computing power to Anthropic: 500MW corresponds to approximately $1.25 billion per month, equating to about $30 billion/GW/year. If this pricing holds, the implied returns are very high, which instead indicates that high-quality computing power is still tight in certain scenarios. It is not evidence that "no one wants computing power," but rather evidence that "idle capacity can be snapped up at a high price."

However, this can only be called a bridge, not the main line. Morgan Stanley still places the key to Meta's valuation on frontline product innovation: whether Meta AI, business agents, messaging services, diffusion offerings, subscriptions, etc., can bring more sustained interaction and revenue growth. Selling computing power can supplement EPS, but cannot automatically lift valuation multiples.

Capital expenditures may not necessarily be revised down; establishing a complete cloud may actually be more costly.

The market's greatest concern is whether Meta will revise its capital expenditures down for 2027, leading the entire AI hardware chain to lower its expectations.

However, the current Morgan Stanley model assumes that Meta's capital expenditure will increase from $145 billion in 2026 to $175 billion in 2027 and $205 billion in 2028. The premise of this model is that Meta is primarily building capacity for its own frontline products, rather than creating a complete ultra-large-scale cloud service provider.

If Meta indeed expands its external cloud services, especially by creating a model/API platform, rather than just temporarily renting bare computing capacity, the capital expenditure may actually come under upward pressure. Because a complete cloud business requires longer-term data center capacity, a more complex software platform, and delivery capabilities aimed at enterprise customers.

Bernstein also places this issue out to 2027 and beyond. Meta is one of the most important "checkbooks" in the AI market, and any change in construction pace will affect the supply chain. However, "temporary rentals" and "permanent cloud business expansion" have different implications for capital expenditures and cannot be mixed together.

The larger demand side remains reasoning and agent applications. The HY Computer & AI computing power market consolidation references an OpenAI article from the weekend regarding Codex/agentic AI as a demand signal: personal non-developer users increased by 137 times, organizational user numbers increased by 189 times, and the internal user count at OpenAI grew by 12 times. This perspective emphasizes that the expansion of new scenarios may continue to push up reasoning computing power demands.

So, the key to this divergence is not "Will Meta sell computing power?" but whether the AI demand curve is still steepening. If overseas ARR accelerates, reasoning applications grow, and cloud providers continue to revise capital expenditures upward, then Meta renting out computing power looks more like a phase of asset realization; if subsequent earnings reports collectively revise capital expenditures down, then this will become a signal of an industry inflection point.

Selling bare computing power is easy, but creating a complete AI cloud is difficult.

Meta's potential business has two paths, with completely different levels of difficulty.

The first path is to sell "bare computing power" or raw chip capacity, similar to neocloud. Customers buy GPU/computing resources, and Meta does not have to immediately fulfill a complete enterprise software, developer tools, model platform, or sales system.

The second path is to provide managed model/API access, similar to AWS Bedrock or Google Vertex AI. This is not a business that can be done just by having server rooms and chips. It requires model capabilities, software stacks, developer experiences, enterprise customer sales, and service support to keep pace.

Morgan Stanley's model is more cautious about the second path. It mentions that Meta's Muse model family does not perform prominently on TerminalBench and SWE Bench Verified, and these tests are related to coding capabilities and third-party usage scenarios. If Meta wants to compete with cutting-edge models like Gemini, subsequent models need significant improvement.

This is also where the reasoning “Meta selling computing power means Meta is exiting the model business” falls short. The potential solution already includes model/API access, and Meta AI, business agents, messengers, diffusion offerings, subscription revenues, etc., remain the core of long-term valuation. The issue is not whether Meta will do models, but whether it can develop model capabilities sufficient to support cloud services that external customers are willing to pay for.

In the market discussions, some see Muse Spark, closed-source strategies, and management adjustments as evidence that Meta is still in the model game. However, these are better suited as follow-up items. At least from the three frameworks observed, the more definitive conclusion for now is that the execution barrier for selling bare computing power is low, while the barrier for establishing a complete AI cloud is high.

CoreWeave is the biggest "victim"? Clients become potential competitors.

This impact hits new cloud/GPUaaS companies like CoreWeave most directly.

Bernstein rates CoreWeave as Underperform, with a target price of $67; Meta is rated as Outperform, with a target price of $850. The logic is straightforward: If Meta provides cloud infrastructure externally, it could directly compete with CoreWeave.

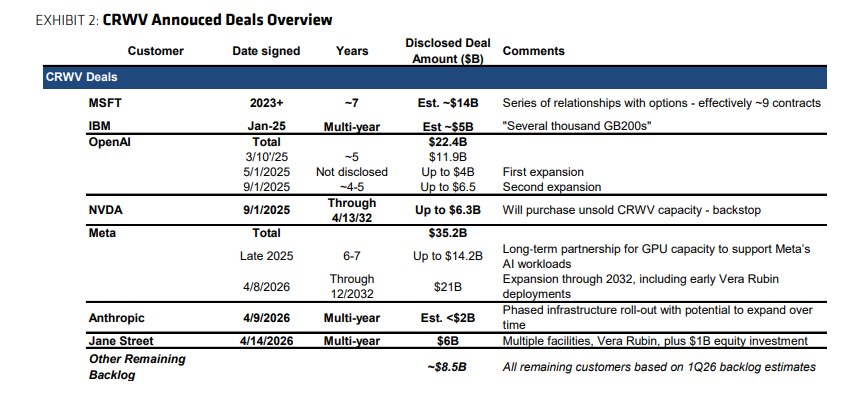

What's more complicated is that Meta itself is a major customer of CoreWeave. According to Bernstein, Meta currently has contracts worth $35.2 billion with CoreWeave, accounting for more than one-third of CoreWeave's order backlog. Additionally, with Microsoft's approximately $14 billion contract, nearly half of CoreWeave's orders come from clients that could become competitors during future renewals.

The short-term risks are not as immediate. Existing contracts are binding and not easy to exit immediately, so CoreWeave's short-term revenue and debt pressure may not worsen right away.

Long-term issues are more difficult to handle. If clients build their own clouds and sell computing power, new cloud companies will see their bargaining power diminish. Especially during renewals, CoreWeave will no longer be facing just demanders, but potential suppliers that are wealthy, have technology, and experience in data centers.

JPMorgan's trading desk noted that the market's reaction to CRWV falling 13% and NBIS falling 15% is relatively easy to understand: Meta has transformed overnight from a customer into a potential competitor. For chip hardware, the impact is more indirect; for GPUaaS, the impact resembles a business model stress test.

Why hardware fell first: beyond fundamentals, there’s also crowded positions.

In the short-term trading aspect, the market is not only trading on fundamentals.

The JPMorgan trading desk argues on two sides: one side is whether the Meta news represents a shift in CSP capital expenditures and AI computing demands; the other side notes that crowded positions, deleveraging, and profit-taking amplified the declines. Its inclination is that the latter bears more weight, and whether the fundamentals have indeed shifted will depend on the upcoming earnings season statements.

The positioning background is not light. Major indices have just gone through rebalancing, and total flows and leverage levels are high; in the past four weeks, both long and short positions have increased at +2 standard deviations; over the past five years, July has often seen hedge funds deleverage, with changes typically between -1 to -3 standard deviations. Semiconductor and memory holdings are approaching the 100th percentile.

This explains why a piece of Meta news could impact the entire AI hardware chain. When crowded trades encounter a narrative of "computing power may not be scarce," it is easy to sell first and ask questions later. On the same day, software, crowded shorts, and Chinese ADRs rose more than 1.4 standard deviations, aligning with the characteristics of short covering during deleveraging.

Subsequent reversal signals, the market mainly looks at a few things: Whether Meta clarifies; whether overseas AI application ARR accelerates; whether cloud providers continue to revise capital expenditures upward; whether Q2 earnings exceed expectations. The timeline is focused on July to August. Currently, it feels more like a watch period rather than a conclusion having been reached.

There's also a tail-end issue: the higher the stock price, the harder it becomes to ignore equity financing rumors.

If Meta's stock price is pushed up by this narrative of "computing power can be monetized," it may actually increase the probability of equity financing rumors.

The logic is that if the EPS for the 2027 fiscal year is below 17 times, Meta is unwilling to engage in dilutive financing; if the valuation is pushed above 20 times based on this news and strong Q2 earnings, the market should not be surprised by potential equity financing.

This is not the main line in the frameworks of the three foreign capital sources, nor has any company confirmed it. But it explains why Meta's stock price reaction may not be straightforward. Selling computing power can alleviate investment return anxieties, while equity financing rumors may bring dilution concerns. Both forces will simultaneously affect trading.

The three valuations do not regard Meta as “a computing power selling company.”

UBS maintains a buy rating for Meta with a target price of $865, based on an annual diluted GAAP EPS of $33.26 through the first quarter of 2028 and a 26 times price-to-earnings ratio; the company has not adjusted its forecast as it has not confirmed potential power sale news.

Morgan Stanley maintains an Overweight and Top Pick rating for Meta with a target price of $775. Its baseline scenario implies about 23 times the 2027 price-to-earnings ratio, still focused on advertising revenue, Reels monetization, engagement improvements brought by AI, efficiency improvement, and options on new products.

Bernstein maintains an Outperform rating for Meta with a target price of $850, while keeping CoreWeave at Underperform with a target price of $67. This combination illustrates the market's divergence well: Meta's options have increased, while CoreWeave faces greater competitive pressure.

However, risks have not disappeared. Downside factors include: a rebound in the advertising cycle, regulatory pressures, uncertainties in Reality Labs investment returns, and potential long-term capital intensity resulting from execution missteps in data center construction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。