Worried about STRC plummeting? STRC dropping 25% is scary? There’s something scarier!! -- The life and death of Strategy’s preferred stocks

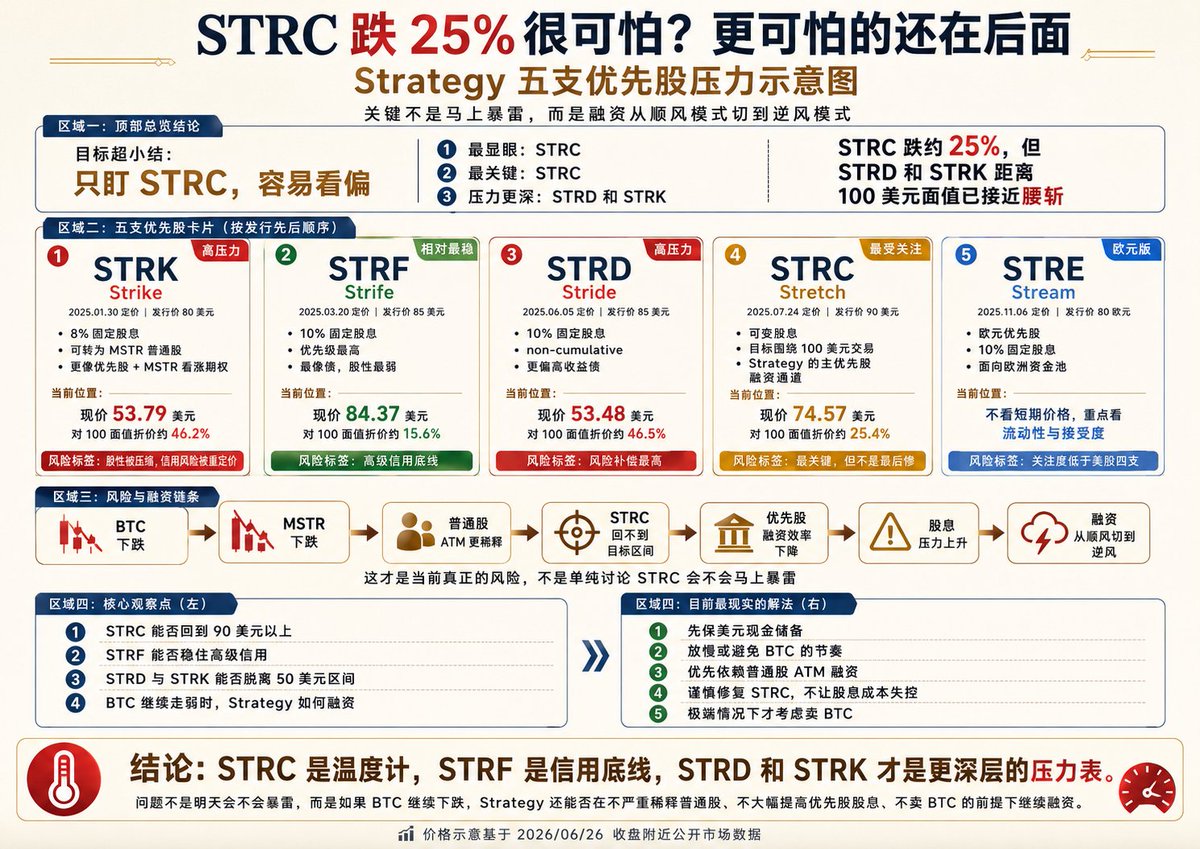

Many friends are currently focusing on $STRC, which is mainly well-known and the setup around 100 dollars seems quite novel, but in fact, STRC is not the only preferred stock in Strategy; there are actually five preferred stocks in total including STRC.

The order of issuance is as follows:

1. $STRK, Strike

This is the first one, priced on January 30, 2025, at an issue price of 80 dollars, with a settlement on February 5. Its characteristics are an 8% fixed dividend, plus a convertible attribute, allowing each STRK to initially convert into 0.1 shares of MSTR, making STRK more like a preferred stock plus a bullish option on MSTR.

When MSTR rises, STRK has equity features, and when MSTR falls, the market will reassess it as a high-risk preferred stock yielding 8%.

2. $STRF, Strife

This is the second one, priced on March 20, 2025, at an issue price of 85 dollars, with a settlement on March 25. It is the one among the five that leans towards high credit, featuring a fixed annual dividend of 10% with quarterly cash distributions.

The official Strategy also calls it the senior-most perpetual preferred stock, which means it has the highest priority among perpetual preferred stocks. Simply put, STRF is the one that resembles debt the most among the five, with the weakest equity features and the most stable ranking.

3. $STRD, Stride

This is the third one, priced on June 5, 2025, at an issue price of 85 dollars, with a settlement on June 10. STRD offers a fixed annual dividend of 10%, with quarterly distributions, and its dividends are non-cumulative, meaning there is no obligation to make up for dividends if they aren’t declared during any period.

STRD is more akin to high-yield bonds among the five; while it has a high nominal yield, it also carries the highest risk compensation.

4. $STRC, Stretch

This is the fourth one, priced on July 24, 2025, at an issue price of 90 dollars, with a settlement on July 29. The biggest feature of STRC is its variable dividend, designed to have a par value of 100 dollars. Strategy aims to keep STRC trading as close to 100 dollars as possible by adjusting the dividend rate.

STRC is the one that resembles high-yield cash management products the most among the five and is the most critical. If STRC falls too far, it indicates that the market no longer believes the dividend mechanism can support the price.

5. $STRE, Stream

This is the fifth one and also the euro version, priced on November 6, 2025, at an issue price of 80 euros, with a settlement on November 13. STRE has a par value of 100 euros, with a fixed annual dividend of 10%, and quarterly cash distributions.

STRE is the high-yield preferred stock issued by Strategy targeting the European capital pool, closely resembling euro versions of STRF and STRD but with noticeably lower liquidity and market attention compared to the four U.S. stocks.

So if one is only focusing on STRC right now, it’s easy to miss the key points.

STRC is indeed the most famous one and at the core of the current controversy. The reason is simple: the design goal of STRC is to keep it trading around 100 dollars, and now dropping to over 70 dollars looks like a failure of that peg, so everyone naturally focuses their attention on STRC.

However, looking at all five preferred stocks together, STRC is actually not the worst off at the moment.

Although STRC has dropped by about 25%, which is certainly unattractive, STRD and STRK have already dropped to 53 dollars, close to being halved from their 100 dollar par value. This difference is important because the problem with STRC is mainly market pressure, whereas the issues with STRD and STRK are closer to credit ranking pressure.

STRC at least has a clear price-support logic. Strategy can attempt to pull STRC's price back up to around 100 dollars by raising its dividend rate. Whether this mechanism will continue to be effective is another question, but at least the market knows what STRC’s design goal is and why Strategy values STRC.

Because STRC is too important to Strategy.

STRC is already the largest among the five preferred stocks and is also the main channel through which Strategy continues to finance using preferred stocks. If STRC can maintain around 100 dollars, Strategy can continue to finance through STRC, using the proceeds to buy BTC, bolster cash reserves, and pay dividends on preferred stocks.

However, once STRC lingers around the 70 dollar mark for an extended period, the issue will not just be ugly prices but rather that this financing channel will be blocked.

Currently, the yield corresponding to STRC's market price has already exceeded 15%, indicating that the market is telling Strategy that the 11.5% dividend is no longer sufficient. If the dividend rate continues to be raised, Strategy’s financing costs will increase, and if it doesn't raise, STRC may continue to fall below the target price, leading investor confidence in this mechanism to further decline.

This is the true pressure on STRC. But it is still just pressure and doesn’t yet qualify as the biggest risk.

The greater risk actually lies with STRD and STRK.

STRD is more like a high-yield bond among the five, with a fixed dividend of 10% and now its price has dropped to 53 dollars, bringing its apparent yield close to 19%. This yield looks attractive, but a high yield indicates that the market demands a higher risk compensation.

Especially given that STRD ranks lower and its dividend protection is weaker, the market naturally applies a deeper discount.

STRK is facing another kind of problem. STRK originally had an 8% fixed dividend and could also convert into MSTR common shares, so when MSTR was performing strongly, STRK could showcase its equity and upward elasticity.

But now, after a significant drop in MSTR common shares, STRK's conversion value has been compressed, and the market is no longer willing to pay much premium for this part of its equity. The result is that the equity feature isn’t being realized, and the credit risk is being repriced, hence STRK has also fallen to 53 dollars.

This is the most accurate depiction of the current state of Strategy’s preferred stocks.

If STRC falls, it indicates that the most important preferred stock financing tool of Strategy has encountered problems.

If STRF drops sharply, it signals that the market is beginning to doubt the entire high credit of Strategy.

If STRD and STRK linger at over 50 dollars for a long time, it shows that the market is demanding a very high risk compensation for lower-tier preferred stocks, making it increasingly difficult for Strategy to continue financing through preferred stocks.

Therefore, what is truly worth worrying about right now is not whether Strategy will collapse or if STRC has enough money to pay dividends. Rather, it is that Strategy's financing is starting to shift from a tailwind mode to a headwind mode!!

In the past, Strategy's logic was that when BTC rose, MSTR rose, both common stocks and preferred stocks were easy to sell, and the money from sales was reinvested in BTC, creating a positive cycle.

Now the pressure has turned into BTC falling, MSTR falling, and common stock issuance becoming more diluted, STRC dropping below the target range, preferred stock financing efficiency decreasing, dividends still needing to be paid, cash reserves, and common stock ATMs becoming more important.

Financing difficulties, purchasing Bitcoin is reduced; curling up to endure the winter is what Strategy currently needs to face.

Currently, there is no basis to state that Strategy is collapsing because Strategy still holds a large amount of BTC assets, along with cash reserves, and the preferred stock dividends and debt interests still have short-term buffers. Moreover, even if Strategy needs to sell Bitcoin for survival, it will not dump it in the secondary market.

Of course, what may occur is that if BTC continues to fall, MSTR continues to weaken, and preferred stocks continue to trade at a discount, then Strategy's subsequent financing will become increasingly expensive, and common stock shareholders will face further dilution. This is indeed a possible scenario and has already happened three times in history.

So now the biggest headache for Strategy should be how to finance if bitcoin:native continues to decline!! And to do so while avoiding significant dilution of common stock, not significantly raising preferred stock dividends, and without selling BTC.

End?? Not yet!

Since the problems are understood, are there any solutions?

It’s too lengthy; I’ll write it in the next article.

#Bitget is here, just VIP! Crypto, U.S. stocks, CFD, one-stop layout for global opportunities

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。