TL;DR

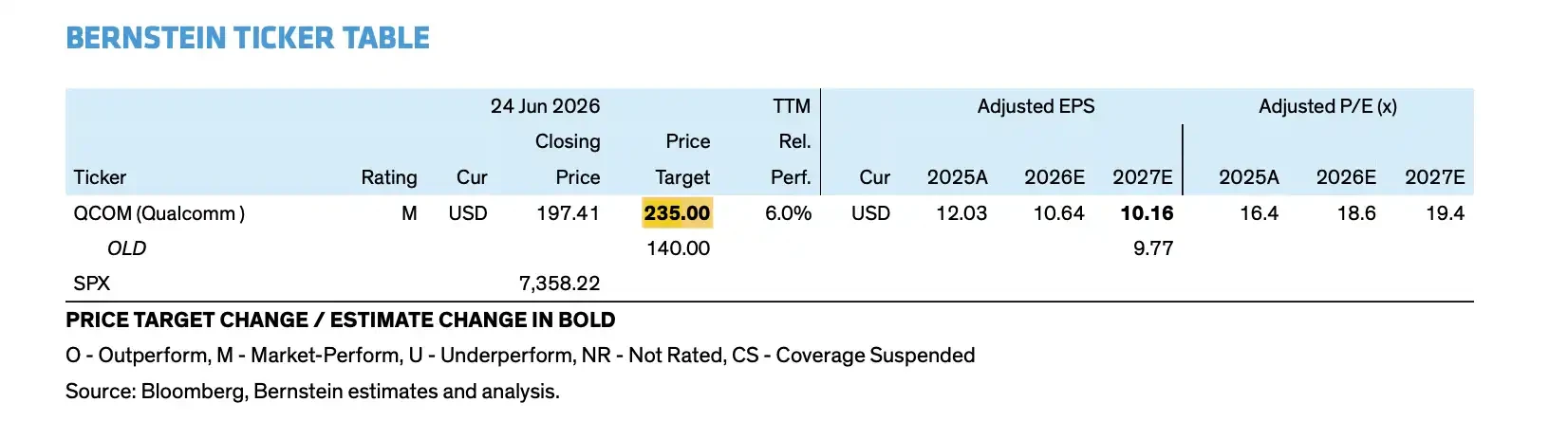

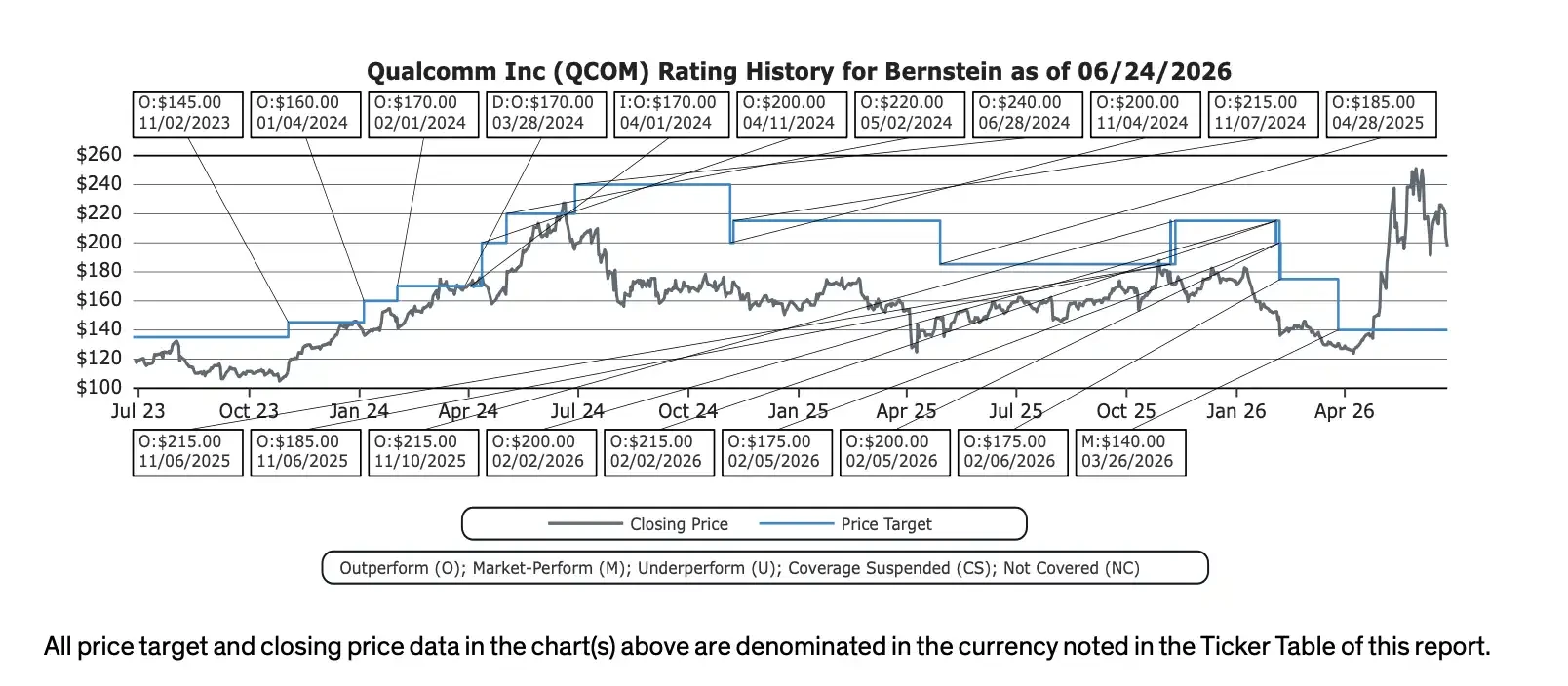

- Bernstein raised Qualcomm's target price from $140 to $235, but the rating remains Market Perform.

- Qualcomm's FY2029 target bets on data centers, automotive, and IoT, with non-mobile revenue goals of about $40 billion.

- Decline in mobile business, rising OPEX, and uncertainty in data center gross margins remain core constraints for not adjusting the rating.

Target price soars, but rating does not follow

After Qualcomm's Investor Day in New York, the company presented a larger set of long-term growth targets to the market. Bernstein subsequently raised Qualcomm's target price from $140 to $235, but the rating remains Market Perform.

The target price increase indicates that Bernstein acknowledges Qualcomm's long-term story is becoming more significant. The company no longer positions itself solely as a mobile chip supplier but aims to enter broader computing markets such as AI data centers, automotive, IoT, and personal AI devices. According to Qualcomm's official targets, by FY2029, the company expects non-mobile revenue to reach approximately $40 billion, with data center revenue exceeding $15 billion, and non-GAAP EPS exceeding $18.

However, the unchanged rating also indicates that the sell-side does not believe this story is sufficiently certain. The real constraint lies in the timeline: the realization of data center and automotive business will come later, while the decline in mobile business, Apple's revenue exit, increased OPEX, and gross margin pressure will hit financial reports sooner.

This explains why the $235 target price does not equate to a "buy" signal. Bernstein admits that the long-term valuation ceiling for Qualcomm has been raised, but given the current stock price reflects some optimistic expectations, the risk-return does not yet tilt significantly towards the buy side.

A new story: shifting from mobile cycles to AI data centers

The most important new story for Qualcomm is data centers.

The company’s official targets show that FY2029 data center revenue will exceed $15 billion. Compared to the current base of approximately $30 million in data center revenue, this means Qualcomm must truly enter the cloud vendors' AI infrastructure budgets in the coming years, rather than just remaining in the mobile chip and edge computing markets.

Qualcomm’s revealed data center roadmap includes custom ASICs, AI inference accelerators, the Dragonfly C1000 CPU, connectivity products, and related software layers. The company also mentioned two unnamed Hyperscaler customers, which are expected to each contribute over $1 billion in custom silicon revenue by FY2027.

The partnership with Meta is another important validation point. Qualcomm announced a multi-generation collaboration for data center CPUs with Meta, planning to begin production of the Dragonfly C1000 CPU in the second half of 2028. However, caution is needed here: the official statement indicates that Qualcomm will be one of the suppliers, without disclosing amounts, capacity, or exclusivity.

The automotive and IoT sectors form the second growth curve. Qualcomm's official targets indicate that FY2029 automotive revenue will reach $10 billion, with IoT revenue exceeding $14 billion. The automotive design-win pipeline has increased from $45 billion 18 months ago to $65 billion, as the company continues to bet on digital cockpits, advanced driver assistance, and in-car connectivity.

$235 target price bets on 2029 rather than next year

The core of Bernstein's target price increase is not that Qualcomm's short-term performance suddenly improves, but that the valuation model begins to incorporate larger data center revenues and a more balanced business structure.

According to Bernstein's model, Qualcomm's FY2029 revenue is estimated at about $64.8 billion, with EPS around $18.12, closely aligning with the company’s long-term target of "non-GAAP EPS exceeding $18." In contrast to the past when the market primarily priced Qualcomm around the mobile cycle, the data center, automotive, and IoT segments present the company with opportunities for a higher valuation multiple.

The target price of $235 corresponds to a higher valuation framework. Bernstein employs an average EPS of about $11.75 for FY2027/FY2028 with a 20x price-to-earnings ratio; the previous target price of $140 corresponded to a multiple of about 14 times. In other words, the key to the target price increase is not significant upward adjustments in next year's earnings, but rather that the market is starting to be willing to pay a higher multiple for Qualcomm's AI data center and diversified revenue story.

However, there is also divergence here. Bernstein's model assumes that data center business gross margins will be about 40%, which is lower than Qualcomm's current average level. Even if data center revenues ramp up, it may not necessarily boost overall profit quality initially. Estimates in the report suggest that as the business structure evolves, Qualcomm's overall gross margin could decrease from 55.2% in FY2026 to 51.6% in FY2029.

Mobile pressure arrives first, while data center realization still awaits

Qualcomm aims to use data centers, automotive, and IoT to demonstrate a change in revenue structure, but the pressure in the mobile business has not disappeared.

Sell-side reports and management Q&A indicate that FY2027 Android phone revenue is expected to remain flat or slightly decline. Combined with the exit of Apple's revenue, total handheld device revenue may decrease year-on-year by $5 billion to $6 billion. The handheld business remains Qualcomm's largest revenue source, and this decline will directly affect the profit base for the next two years.

The company’s long-term assumptions for Android phones are also more cautious. From FY2026 to FY2029, the compound annual growth rate for Android handheld revenue is expected to be around 5%, significantly lower than the high growth phase in previous cycles. Qualcomm may still maintain an advantage in high-end Android devices, AI phones, and radio frequency fronts, but it is difficult to fully offset the pressure from Apple's exit and the slowdown in the smartphone industry.

The expense side will also face pressure sooner. Qualcomm has clearly stated that FY2027 OPEX will see double-digit growth. To advance data center CPUs, AI accelerators, custom silicon, and software ecosystems, the company needs to invest in R&D, sales, and customer support in advance. Revenue recognition typically lags behind expenditures, which means that EPS forecasts before and after FY2027 may carry downward revision risks.

This is the crucial point of the target price increase but unchanged rating: Qualcomm's long-term story is larger, but the profit curve for the next two or three years may not necessarily be smoother. Investors need to accept two simultaneous judgments: FY2029 EPS may be elevated by AI data centers, but the profit pressure around FY2027 may also be more apparent.

Differences hinge on whether $15 billion data center revenue can turn into real profits

Bernstein's report does not simply have a bearish view on Qualcomm but, while re-pricing Qualcomm, reminds the market not to treat long-term goals as already realized performance.

In a downturn scenario, if data center revenue is significantly below the $15 billion target, and growth in personal AI and computing businesses is also limited, Qualcomm's FY2029 EPS could still reach about $15. This indicates that Qualcomm's fundamentals are not weak, and automotive, IoT, licensing, and cost control can still support a certain level of profitability.

However, the gap between $15 and above $18 EPS has a significant impact on valuation. If the market has already priced Qualcomm based on more optimistic data center revenue and higher valuation multiples, the company must prove three things: cloud vendor customers can ramp up as planned; data center gross margins will not continuously drag down overall profitability; and the decline in mobile business will not excessively depress EPS before new business is realized.

Therefore, the $235 target price is not a conclusion that "Qualcomm's AI transformation has been successful," but a new price incorporating long-term diversification prospects into the valuation. Qualcomm's story is indeed larger than in the past, and more akin to a chip platform company spanning mobile, automotive, IoT, and AI data centers.

However, the Market Perform rating reminds that until the headwinds in the mobile sector ease, data center revenues ramp up, and gross margins withstand verification, the market has every reason to not rush to consider Qualcomm a definite AI winner. What truly needs verification next is not whether Qualcomm can articulate the $15 billion data center goal, but whether that target can timely convert into revenue and eventually turn into sufficient profit.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。