This morning, a report ignited the DeFi community.

CoinDesk cited three informed sources stating that the crypto exchange Kraken is negotiating to invest in Aave. The structure of the transaction is as follows: Kraken will contribute 35,000 ETH in exchange for 250,000 AAVE tokens, plus 15% equity in Aave Group, with the entire deal priced at approximately 71 million dollars, corresponding to a 385 million dollar valuation. The report also mentioned that this is the first transaction in a series by Payward Asset Management, and Kraken intends to promote it publicly, aiming to take a more proactive role in DeFi and other investment opportunities in the future.

The most striking aspect of this deal is the valuation of the transaction. At 385 million, it is nearly 70% lower than the market value of the AAVE token, which is around 1.24 billion dollars. Aave has consistently emphasized that the value of the protocol entirely belongs to the token, so what exactly is Kraken getting by spending real money to acquire 15% of the equity? If all value is supposed to flow to the AAVE token, why does Kraken still want an equity position?

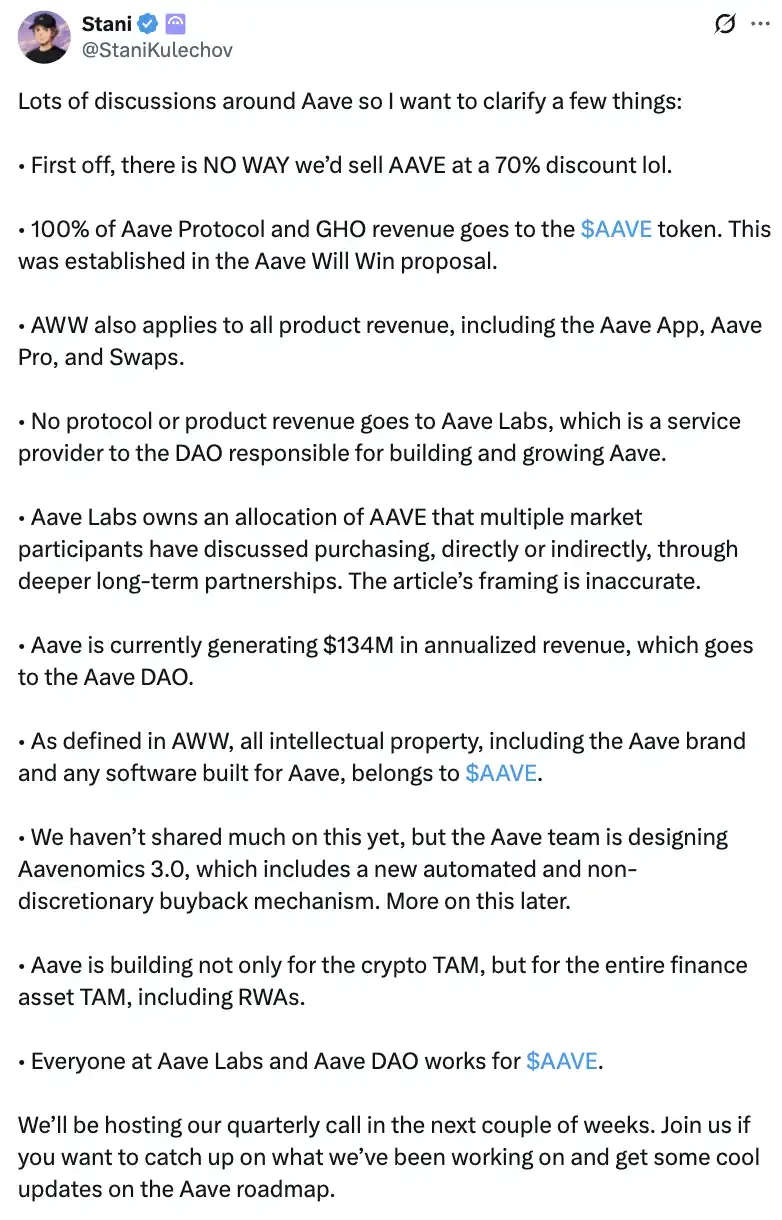

A few hours later, Aave founder Stani Kulechov came out to clarify.

He denied the framework of the report point by point. Aave Labs would never sell AAVE at a discount; what was discussed was the portion of AAVE held by Labs itself, negotiated through "deeper long-term cooperation" with multiple market participants, unrelated to the protocol layer. He emphasized that all revenues from the Aave protocol and the GHO stablecoin flow into the AAVE token, as established by the "Aave Will Win" proposal, including revenues from products like Aave App, Aave Pro, and Swaps; Aave Labs is simply a service provider for the DAO and does not take a share of protocol revenue.

Stani also revealed that the team is designing Aavenomics 3.0, which will introduce an automatic, non-discretionary buyback mechanism.

According to him, what is being sold is not discounted AAVE; CoinDesk's comparison of the total price of the equity transaction with the market value of a single token is misleading in itself.

If Stani's statement is correct, CoinDesk's report indeed contains misleading elements.

However, Stani did not address the initial question from retail investors. If the value of the protocol truly all belongs to the token, what exactly does Kraken get by buying 15% of Aave Group? This point he has avoided. The value attribution between equity and tokens remains a muddled issue.

The details of the transaction are still uncertain, and Kraken has not commented directly on the report.

However, their motivation is clear. CoinDesk mentioned in the report that Kraken's parent company Payward has characterized this transaction as "the opening of a series of asset management actions." A company preparing for an IPO is turning its investment in the leading DeFi protocol into its signature move.

In the past year and a half, Kraken has made new moves almost every quarter, advancing along three main lines.

Firstly, building its own infrastructure.

Kraken has incubated its own L2 "Ink", attempting to replicate the paths taken by Binance and Coinbase, bringing CEX users onto the chain for lending and trading. The most active protocol on Ink is the perpetual DEX "Nado", which offers spot, margin, and unified perpetual margin accounts; relying on a points program and airdrop expectations, it attracts many real users.

Secondly, strategic acquisitions.

In the past year and a half, Kraken's acquisitions have been quite intensive: it spent 550 million dollars to acquire the derivatives exchange Bitnomial, including the full suite of CFTC licenses for brokerage, clearing, and exchange; 600 million dollars to buy the stablecoin payment company Reap, filling in the business of issuing cards and cross-border settlement; at the end of last year, it purchased Backed Finance, which is behind the tokenized stock protocol xStocks; in February of this year, it acquired the token management platform Magna.

The third line is its regulatory identity.

In March of this year, Kraken became the first digital asset bank in the U.S. to obtain a Federal Reserve master account, able to settle dollars directly on Fedwire without going through intermediary banks. In the same month, Nasdaq announced a partnership with Kraken to build a framework for stock tokenization, retaining issuer control, stockholder voting, and dividend rights. A crypto exchange is changing into an identity recognized in traditional finance.

Kraken is evolving from a crypto exchange into an all-stack financial infrastructure company.

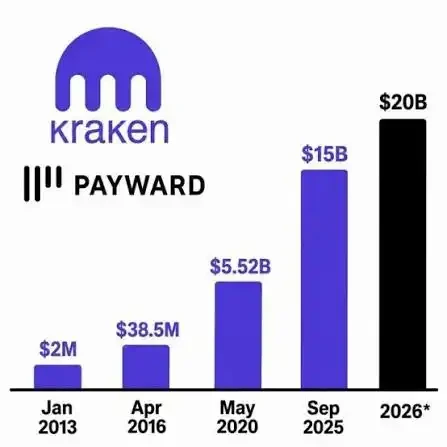

IPO is the main driving force behind all these strategic moves. In November of last year, Payward raised 800 million dollars at a 20 billion dollar valuation, and in two months, the valuation increased by 30%, with investors including Citadel Securities, Jane Street, and Apollo Global Management.

Viewing this logic retrospectively, it is easy to understand why Kraken wants to invest in Aave—it extends the narrative of "we can do any financial business" into DeFi itself. Acquiring a stake in a leading protocol is much faster than building a lending protocol from scratch and is more suitable to be included in the narrative about growth sources in the IPO prospectus.

However, Kraken's IPO journey has not been smooth.

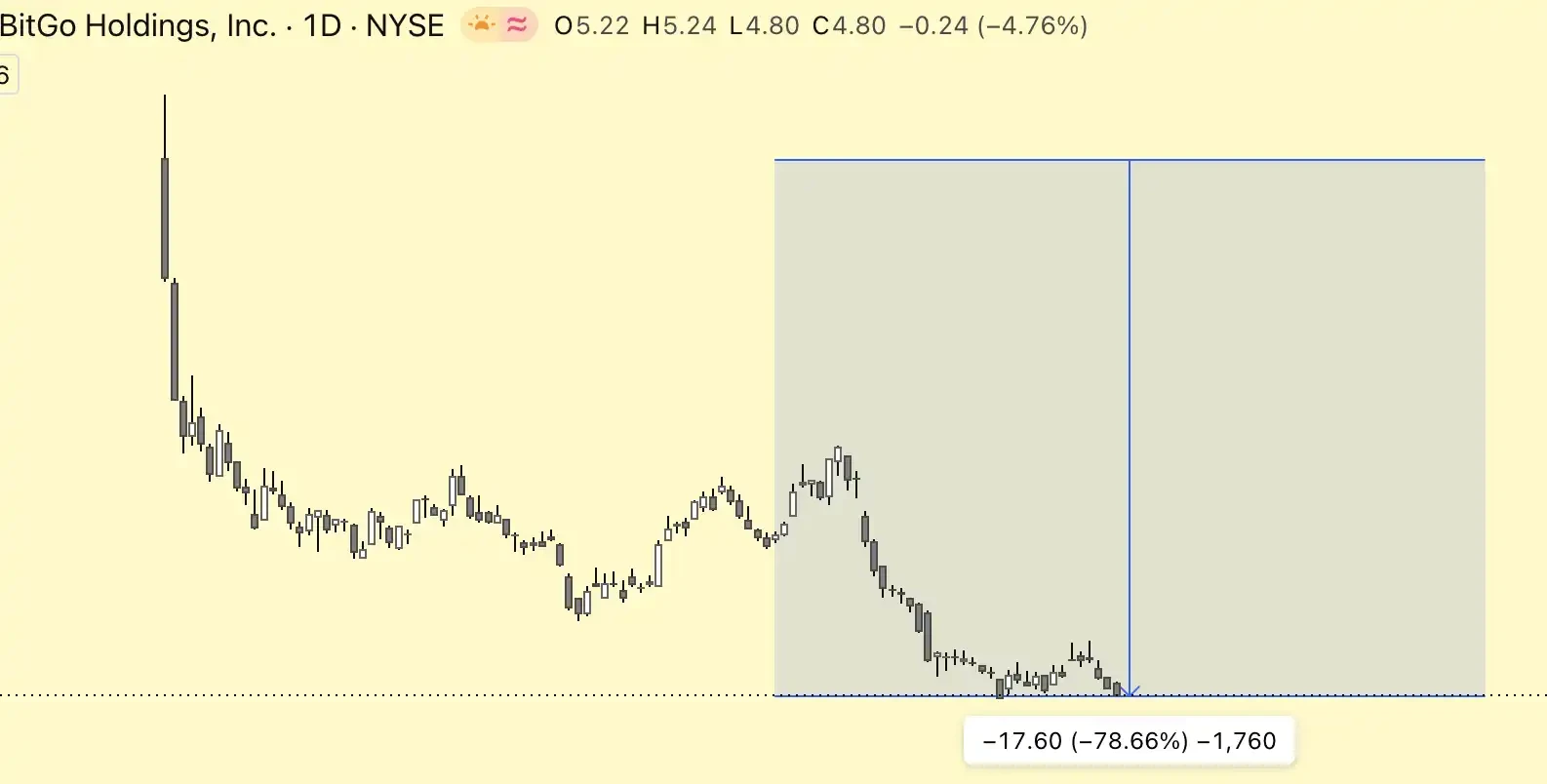

On March 18 of this year, Kraken's IPO was put on hold. The core reason is the dismal market conditions; Bitcoin has dropped from 126,000 dollars in October last year to around 65,000 dollars, with the entire market evaporating over one trillion dollars in market value. BitGo, which went public before it, is the only digital asset company listed in 2026, and after going public, its stock price fell by 44%, serving as a cautionary tale for everyone.

The market taste is also changing—at least 11 crypto IPOs are expected to raise a total of 14.6 billion dollars in 2025, but the start of 2026 is much colder; advisors say that investors are now scrutinizing financial infrastructure targets more closely, reviewing compliance maturity, recurring revenue, and stress resistance—each item must be reconsidered. Just a month before the IPO suspension, Kraken replaced its CFO, who had only served for 16 months, handing duties to a newly promoted Deputy CFO. Replacing the financial leader right before the finish line is itself a red flag for a company under due diligence scrutiny.

However, a pause does not mean exit.

In May of this year, reports indicated that Payward was raising a new round of funds at a 20 billion dollar valuation, Co-CEO Arjun Sethi has also stated multiple times in recent months that the company's goal is to complete the IPO by the end of 2026. It can be anticipated that in the next six months, Kraken may take more frequent actions to add weight to the valuation in the prospectus.

The rumors of investing in Aave are just the latest step in this effort. As for whether this transaction will be completed and what exactly the 15% equity has purchased, we may have to wait until the S-1 document is made public to get a written answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。