Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

The "de-pegging" situation of Strategy Preferred Stock STRC is still intensifying.

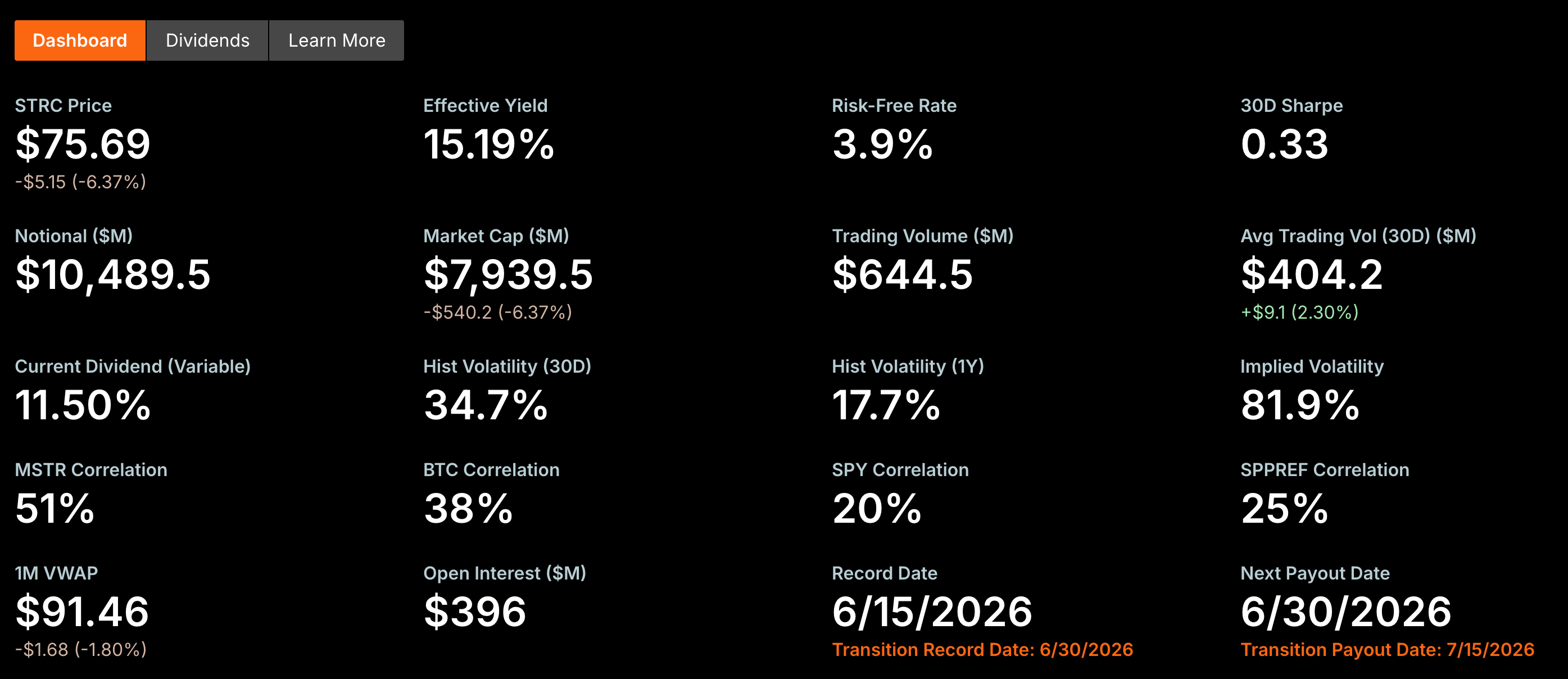

Yesterday, during U.S. stock trading, STRC first fell below the 80 mark, reaching a low of 73.62 USD at one point. Although it rebounded slightly by the end of the trading day, the price still closed at only 75.69 USD, nearly "de-pegged" by about 25% from its target par value of 100 USD.

Last week, we wrote an article titled "STRC de-pegged 11%, can Strategy's perpetual motion machine still keep running?", focusing on the reasons for STRC's de-pegging and briefly outlining its potential future impacts.

However, based on discussions within the community, it seems many readers are still unclear about how serious the consequences of STRC's ongoing de-pegging are, so we decided to write another article to break down this issue.

Strategy's most important financing channel has failed

What exactly is STRC? In one sentence, it is Strategy's cheapest and most efficient financing channel.

The essence of Strategy's business model is to continuously finance to increase BTC holdings and then continue to finance and increase holdings. This is a cycle that must keep running. Strategy's high valuation largely comes from the market's belief in its ability to sustain financing and continuously buy BTC. As long as its financing ability remains intact, it can keep expanding its BTC holdings; and the ever-growing BTC holdings will further support market expectations of its future financing capabilities.

In the past few years, Strategy has tried almost all financing methods—issuing common stock, issuing convertible bonds, issuing various types of preferred stock, and then continually investing the raised funds into BTC. Among all financing tools, STRC was once viewed by the market as the closest to "perfect" and was Michael Saylor's proudest creation. Saylor boldly stated that “STRC is a product designed by AI, something humans cannot design.”

As a preferred stock, STRC's advantages are very clear. If common stock were issued, existing shareholders might find their equity diluted; if convertible bonds were issued, the company would have to bear future debt repayment pressure; while STRC, as a perpetual preferred stock, has no maturity date and does not dilute common stock shareholders, only needing to pay fixed dividends. For Strategy and Saylor, this is almost the lowest cost and most efficient form of financing.

From the very beginning, STRC was designed to be a product pegged at 100 USD. Strategy's idea was to dynamically adjust the dividend rate to keep STRC trading around the 100 USD mark in the long term (does this give you a sense of algorithmic stablecoins?). As long as the secondary market can maintain this price, the company can continue to issue new STRC at close to par value, continuously raising new funds and continuing to buy bitcoins.

In other words, the core value of STRC lies in its continuous financing ability, but this ability is predicated on maintaining the price close to the target par value. When STRC continues to de-peg, this financing channel is effectively blocked. Because for any investor, if the same STRC can be bought in the secondary market for only 75 USD, it is impossible to participate in the company's new preferred stock issuance at a price close to 100 USD.

For Strategy, it either has to continually raise the dividend rate to attract funds (which has proven to have limited appeal) or accept the reduced efficiency of discounted issuance (which is tantamount to actively breaking the original target par value). Either way, this means that its financing machine is beginning to experience increasing friction.

Financing tools have become a cash flow burden

If only the financing capability were temporarily ineffective, it would be one thing, but the bigger issue is that STRC requires Strategy to continuously pay high cash dividends.

According to the latest data released by Strategy, as of now, the issuance amount of STRC has reached about 10.49 billion USD, and the current dividend yield is 11.5%. This means that just for STRC alone, there is an annual cash dividend obligation of over 1.2 billion USD. Adding in other preferred stocks issued by Strategy, such as STRD, STRK, STRF, this number would further rise to about 1.7 billion USD.

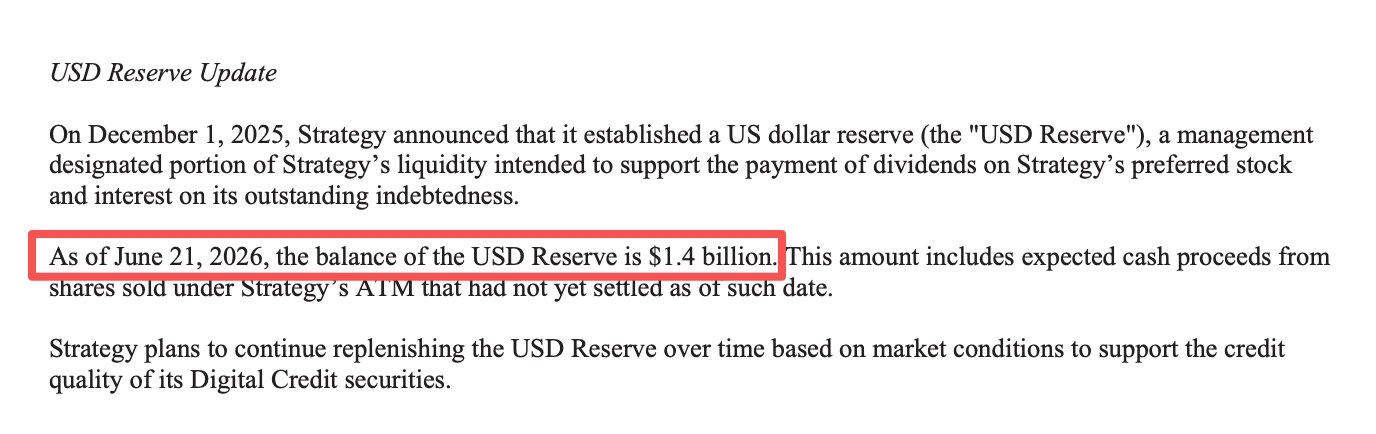

In the common stock issuance document dated June 21 (note it is common stock, will explain in detail later), Strategy disclosed that the company's cash reserves were around 1.4 billion USD. Based on this cash reserve level, Strategy’s book cash can cover less than a year's preferred stock dividend payments.

Breaking the deadlock requires money, but where does the money come from?

Whether to sustain its own business model, escape the current dire cash flow situation, or avoid a dividend payment default (which is more urgent currently), Strategy needs more funds. Theoretically, there are only three paths left for Strategy to "make money."

First, issue common stock.

This is currently the most direct and mature financing method. Through the ATM (At-the-Market Offering) plan, Strategy can continuously sell MSTR common stock to raise funds.

But financing through common stock is not without its costs. Continuous issuance means that the number of outstanding shares keeps increasing, and if the growth speed of the newly raised funds for buying BTC cannot outpace the expansion speed of the shares, the corresponding BTC per share will slow down, risking continuous dilution for common stock shareholders—note, this is crucial.

Second, continue issuing bonds.

In recent years, Strategy has repeatedly raised funds through convertible bonds and other debt instruments, which were also important sources of financing for their early large-scale BTC purchases.

However, as the scale of preferred stock expands and fixed cash expenditures continue to increase, the market has become more concerned with Strategy's liquidity and debt repayment capacity. In the current financing environment, if the company issues bonds again, investors will likely demand a higher risk premium, which means financing costs will be significantly higher than before.

More importantly, unlike preferred stock or common stock, bonds have rigid interest payments and principal repayments. In the context of declining cash reserves and increasing dividend expenditures, continuing to expand the debt scale will undoubtedly further burden the company’s finances and compress future financing space.

Third, sell BTC.

From a financial perspective, this is the fastest way to replenish cash reserves. Strategy must have considered this route; it previously stated on its official X regarding dividend payment pressure: “If considering its huge Bitcoin reserves, it is enough to cover 32 years of dividend payments.”

However, for Strategy, this is also an extremely risky choice. Earlier this month, Strategy sold its Bitcoin holdings for the first time, and although the sale was only for 32 coins, the company packaged it as a "proactive market desensitization test," mentioning that "more will be bought back later," but this move caused a significant short-term drop in the market.

As the largest single holder of Bitcoin in the market, Strategy's actions can easily trigger chain reactions in the market. If it increases the volume of sales in the future, it will undoubtedly have a significant impact on the already fragile BTC price. If BTC further declines, Strategy's so-called "reserves" will also rapidly shrink.

Overall, under the current circumstances, every viable financing channel for Strategy comes with a higher price than in the past.

Has Strategy made a choice?

From the latest developments, besides hinting at the possibility of selling BTC, the company seems to have already chosen which path to take.

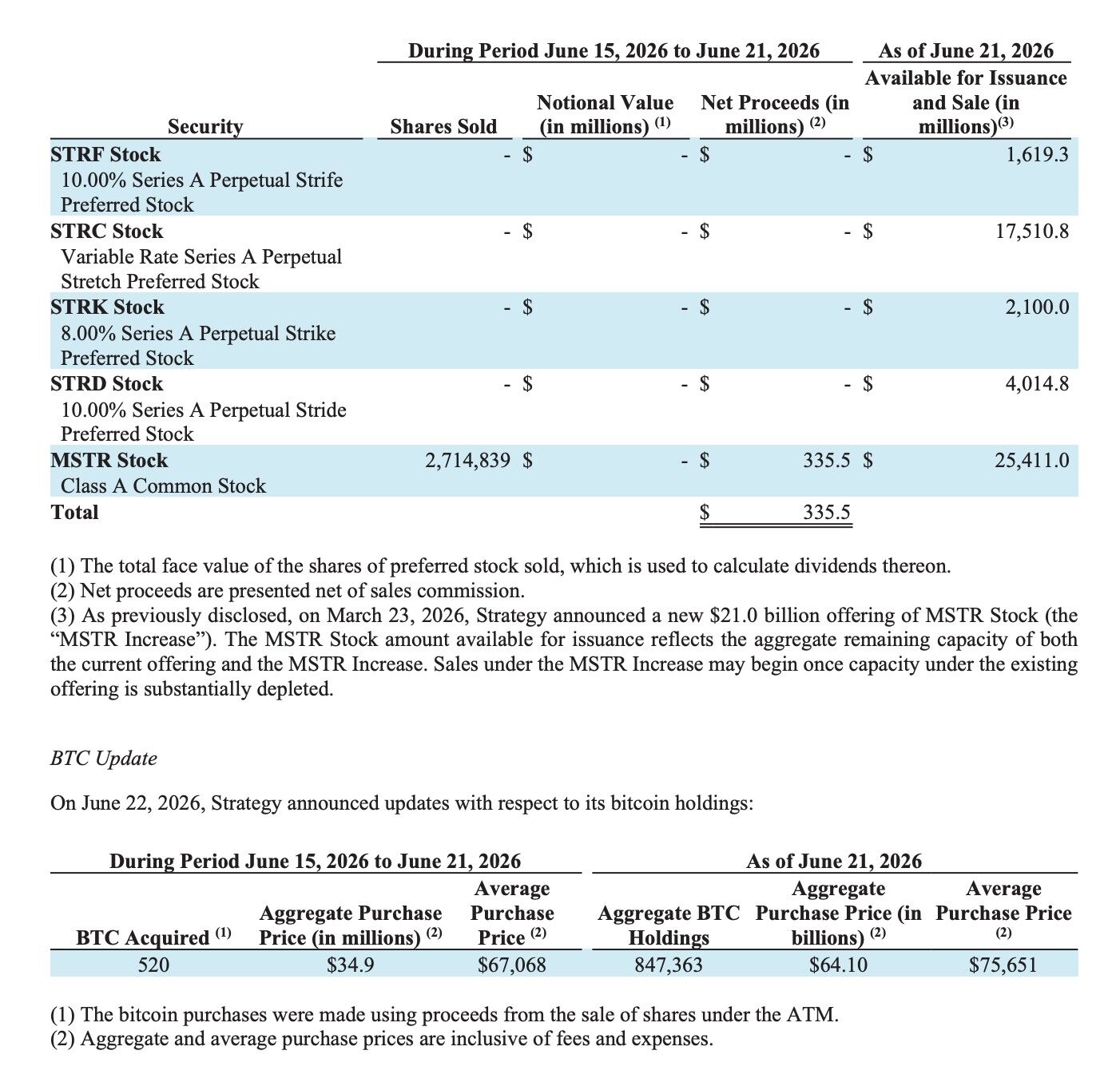

Since June, Strategy has relied on the common stock ATM (At-the-Market Offering) plan for financing for three consecutive weeks, with the latest financing on June 22 being particularly characteristic.

According to the latest 8-K filing submitted by Strategy, the company sold a total of 2,714,839 shares of MSTR common stock in one week, raising a total of 335.5 million USD, but during that week, Strategy bought only 520 BTC for a total expenditure of 34.9 million USD, with an average buy-in price of about 67,068 USD. In other words, out of the raised 335.5 million USD, only about 10% was actually used to continue increasing BTC holdings, while the remaining funds were mainly used to replenish the company's cash flow reserves, raising cash from about 1.1 billion USD to around 1.4 billion USD.

It seems quite effective? But there is another trap.

For MSTR common stock shareholders, the most critical information to pay attention to is how much BTC the funds raised from each new issuance of common stock can ultimately buy back and whether it is enough to cover the BTC equity that this share should correspond to. If the new financing can buy back more BTC than originally corresponded to this share, then the common stock shareholders' rights are effectively enhanced; conversely, if the funds raised cannot buy back sufficient BTC to cover the equity of the new shares, then common stock shareholders will face dilution.

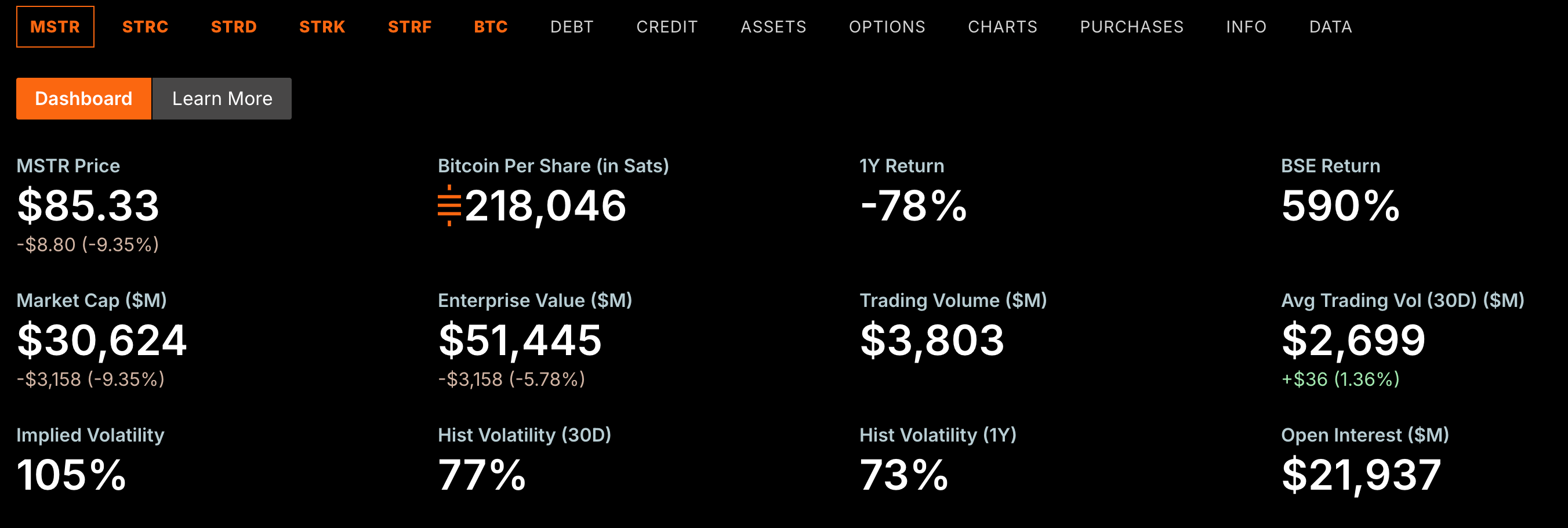

Clearly, Strategy's recent issuance of common stock comes at the cost of diluting common stock equity. Official data from Strategy also indicates that the BTC per share corresponding to MSTR has dropped from its peak of 220,900 Sats to 218,046 Sats.

This is also the greatest limitation of common stock financing. For most listed companies, issuing common stock is just one of many financing methods; but for Strategy, common stock itself is a crucial part of its business model.

In recent years, the reason Strategy has been able to continually grow is fundamentally because of the continuous operation of the "financing ➡️ buying coins ➡️ reinforcing market expectations ➡️ refinancing ➡️ buying coins again..." feedback loop. The core market expectation for Strategy is that it can sustainably create more BTC equity for common stock shareholders, not dilution.

However, when Strategy increasingly has to rely on common stock financing to replenish cash reserves rather than continue increasing BTC holdings, the logic of this feedback loop will change. While common stock financing can indeed alleviate Strategy's cash pressure in the short term, it is difficult to become a long-term solution to replace STRC.

If common stock financing continues to erode each share's BTC equity, the foundation on which MSTR's high premium exists may also face challenges, and this is precisely the core competitive advantage of the entire Strategy business model.

What will happen to BTC?

In recent years, Strategy has become the most important marginal buyer in the BTC market (without hesitation), having accumulated 847,363 BTC, accounting for about 4% of the current supply of BTC, worth over 50.7 billion USD. The market has long been accustomed to Saylor's steady and substantial purchases each week.

However, this situation is changing. Strategy can still raise funds through common stock, but most of the money is no longer flowing into BTC, but rather prioritized for replenishing cash reserves. This means that with the same scale of financing, the new buying pressure entering the BTC market is decreasing.

Even more unfavorable is that this condition may persist. If STRC cannot peg for the long term and preferred stock financing continues to be hindered, Strategy will have to rely on common stock financing to maintain cash flow in the long term, potentially further reducing the proportion of funds used to buy BTC. For the BTC market, this means the most stable and certain institutional buying will no longer continue to grow as it has in previous years.

But what is even more concerning is that if the issuance of common stock overly dilutes MSTR shareholders' equity, Strategy may have to consider another financing channel—selling coins.

From the decrease of new buying pressure to the potential emergence of selling pressure, the current Strategy is no longer the biggest marginal buyer of BTC but instead a giant blade hovering over BTC.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。