Original Author: Jia Liu

Today's Micron has delivered a historic financial report that has significantly boosted confidence in the semiconductor sector.

FY2026 Q3 revenue reached $41.46 billion, exceeding market expectations by nearly $6 billion. A storage company that has been labeled a "low-margin commodity" for decades has issued gross margin guidance on par with software companies. After hours, the stock price jumped directly by 13% to 14%, raising its market value to $1.16 trillion.

Micron's rise this year has been astonishing. As of the close on June 22, it was $1211.38, having more than tripled in value this year and over 850% in the past 12 months, making it the third-best performing stock in the S&P 500 for 2026, following SanDisk and Western Digital, both also in storage. The entire sector is moving up at this scale. SK Hynix has risen over 800% in the past 52 weeks, while Samsung has seen its share price grow over 400% in the same timeframe.

With such price increases, many people's first reaction is certainly "too expensive." However, the fact is that a high stock price does not necessarily equate to a high valuation. From many perspectives, storage remains a very "cheap" hot sector.

Stock Prices Soar 9-Fold, Yet PE Stays Flat

One of the most common indicators for determining whether a company's stock is expensive is the PE, or price-to-earnings ratio.

In simple terms, the PE measures how much the market is willing to pay for every dollar of profit a company earns. A PE of 10 means investors are willing to pay $10 for every $1 of annual profit. A high PE usually indicates strong future growth that the market expects; a low PE might mean the stock is cheap or that the market believes the company's current profits are just at a cyclical peak and will soon decline.

The most counterintuitive aspect of storage stocks right now is that their prices have risen significantly, yet their PEs remain low.

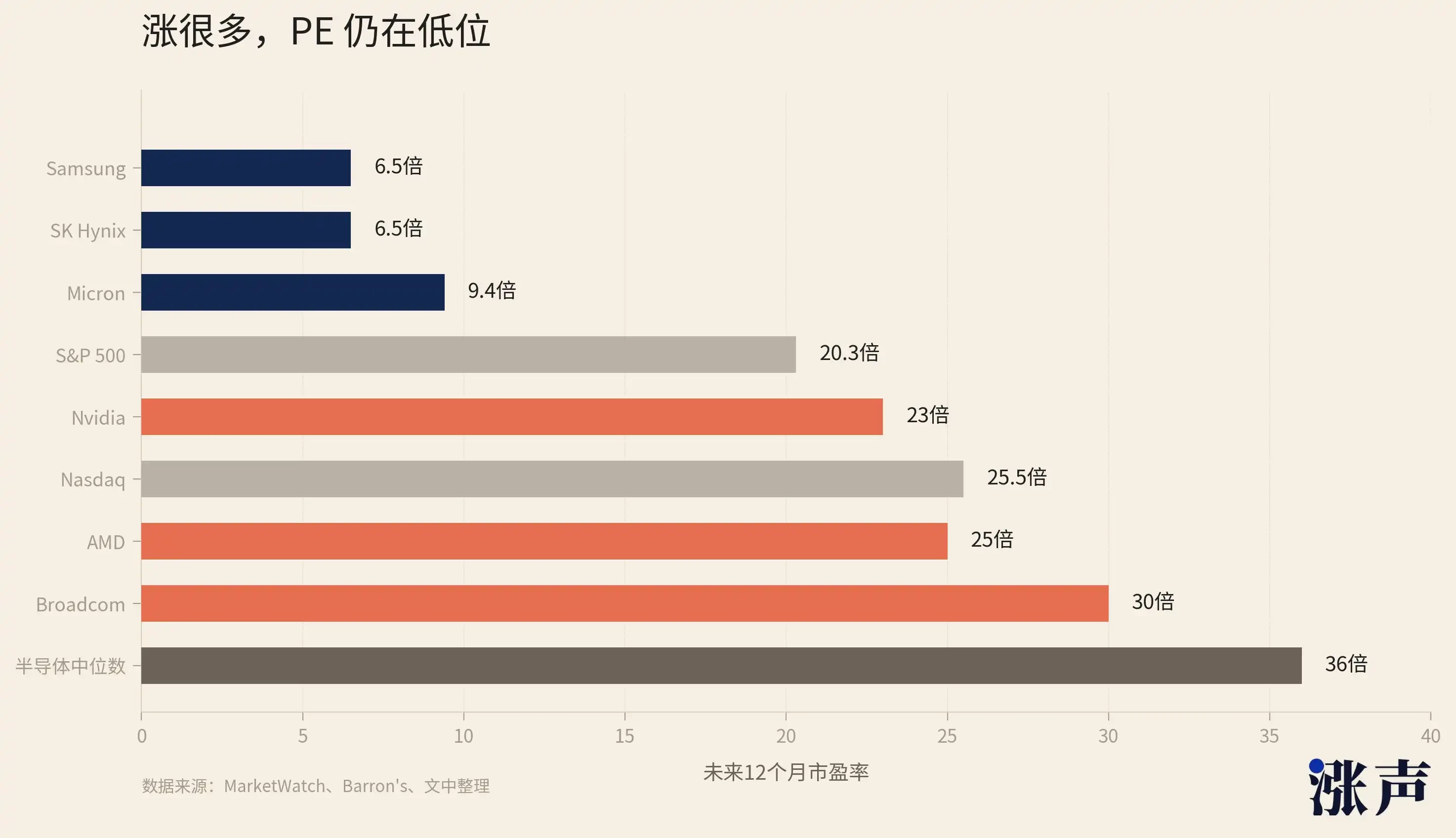

According to FactSet data, a report by market observers in mid-June provided a set of figures: Micron's forward 12-month PE is approximately 9 times, while SK Hynix and Samsung are around 6.5 times. Barron's also noted that Micron's forward PE is about 9.74 times, compared to approximately 25.5 times for the Nasdaq Composite Index and about 20.3 times for the S&P 500. GuruFocus data from June 21 shows Micron's Forward PE is 9.90 times, with SK Hynix at 5.92 times at the end of May and Samsung around 5.45 times.

In other words, most data sources speculate that the forward PEs of the three major storage companies are all in the single digits to just above 10 times.

When these figures are viewed in the context of the entire AI industry chain, they are among the lowest.

NVIDIA's forward PE is about 23 times, Broadcom around 30 times, AMD approximately 25 times, and TSMC about 20 times, with the median for the semiconductor industry overall around 36 times. This means that the valuation levels for the three major storage companies are roughly one-third that of NVIDIA and only one-quarter of the semiconductor industry median.

Ironically, the money from the AI industry is increasingly being generated by the storage segment.

AI servers don't just have GPUs. Every high-end AI accelerator card requires HBM, every inference server needs high-capacity DRAM, and KV cache, model weights, local cache, and data throughput all rely on SSDs. Without HBM, there wouldn't be GPU training clusters; without server DRAM, there wouldn't be inference clusters; and without high-capacity NAND, the storage and caching costs for AI applications cannot be minimized.

Storage has become more than just a regular component in the AI industry chain; it is a physical bottleneck that cannot be circumvented for all AI capital expenditures. A number from Micron's recent financial report illustrates this point: revenue from data centers for a single quarter is $25 billion, with enterprise-level SSD sales totaling $5 billion, accounting for 20% of data center revenue.

It can be observed that this bottleneck has even begun to transmit to consumer electronics.

The AI data centers are driving up the prices and capacities of HBM, DRAM, and NAND, forcing even a negotiation-strong end-user company like Apple to face cost pressures and pass on some price increases to consumers. In the past, discussions about AI profits often centered on NVIDIA; now, it is becoming increasingly clear that a significant portion of this AI bill is flowing towards storage manufacturers.

The stock prices of storage shares have surged, but profits are increasing even faster.

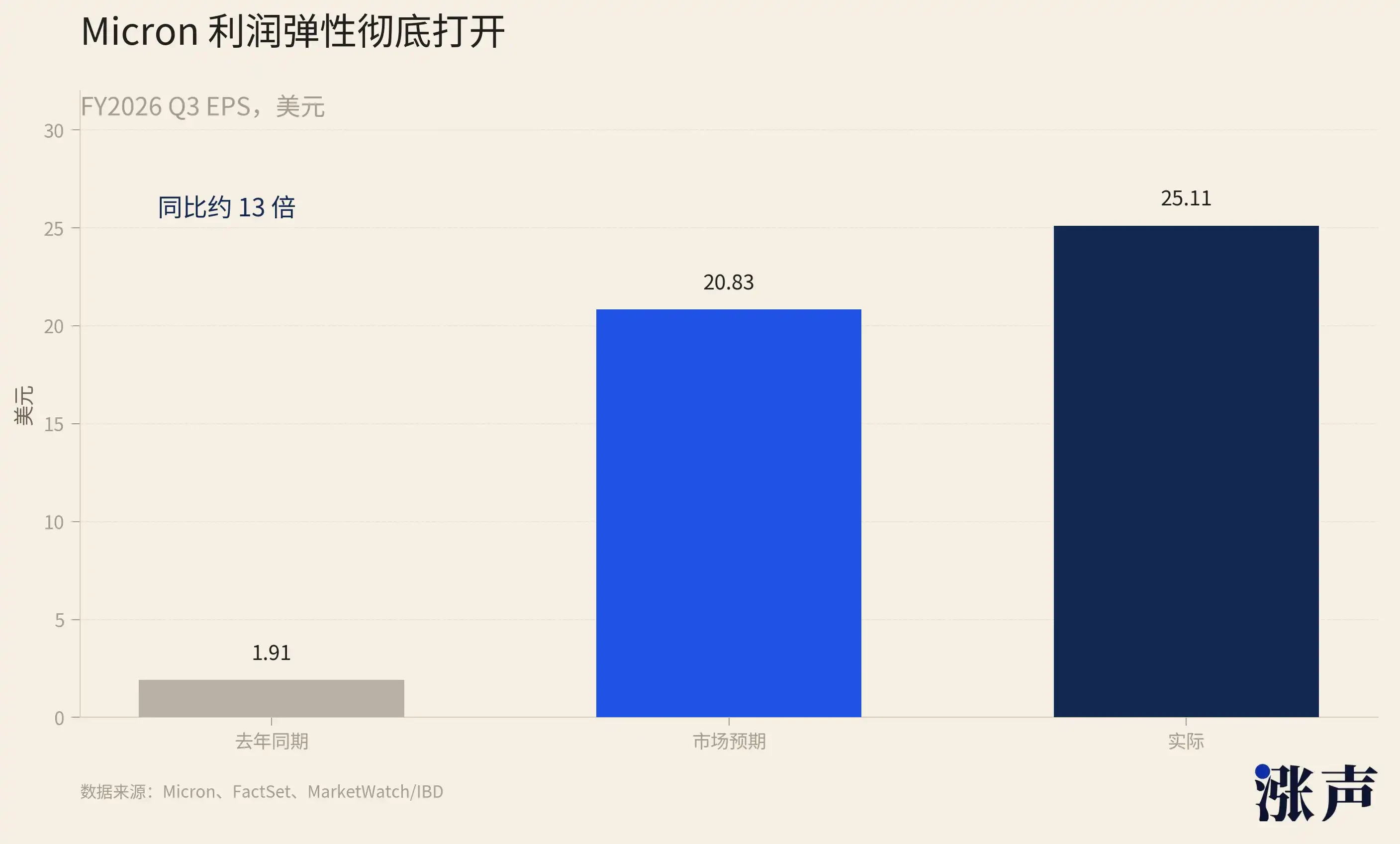

Micron recently reported Q3 EPS of $25.11, up from $1.91 in the same period last year, more than a ten-fold increase. SK Hynix recorded an operating profit of 37.61 trillion won in Q1 2026, a 405% year-over-year increase. Samsung's semiconductor division had an operating profit that was over eight times higher year-over-year in Q1. Stock prices have risen several times, but profits have multiplied even more, with PE ratios remaining uninflated.

AI's money is genuinely flowing into the income statements of storage manufacturers.

Sector Concentrates to Release Positive News, Micron is Just the First Shot

Micron's financial report is the starting gun for this round of storage earnings season.

Next, the storage sector enters an information-dense month: TSMC on July 16, Samsung on July 23, SK Hynix and Western Digital on July 29.

The momentum from Micron's report has already set the tone for the remaining companies. Its most critical information isn't just the quarterly upside surprise, but the Q4 guidance of $50 billion in revenue and an 86% gross margin.

This guidance essentially tells the market that price increases have not peaked and are accelerating. The subsequent four companies are essentially validating or invalidating the same trend indicated by Micron's guidance across different markets and with different product structures.

First, let’s look at TSMC, which will report on July 16.

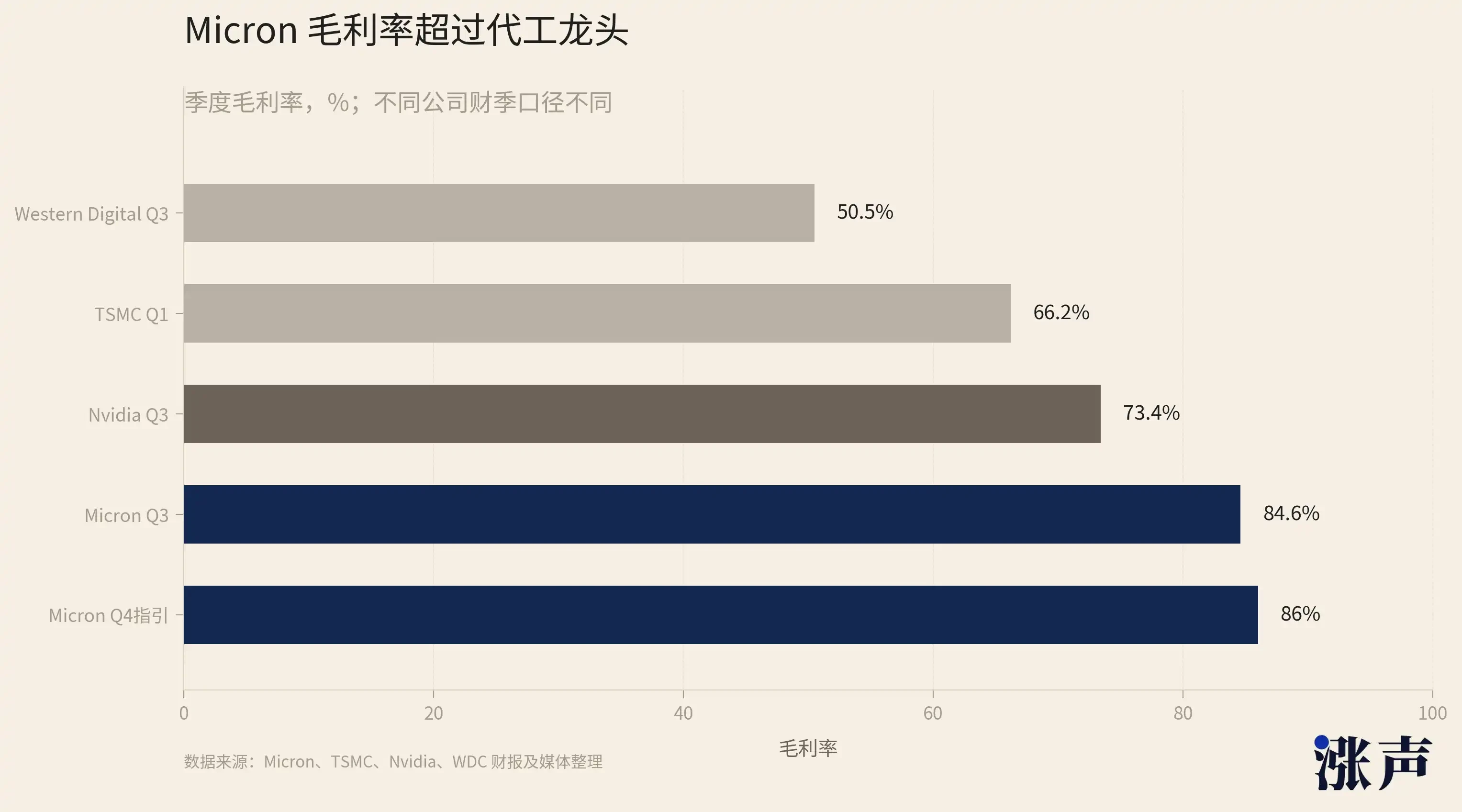

TSMC does not produce storage, but it is the foundation of the entire AI chip supply chain. NVIDIA's GPUs, Broadcom's custom accelerators, and AMD's data center chips all come from its production lines. TSMC addresses an even more fundamental question than storage: Has the capacity bottleneck for AI chips been opened? Q1 revenue was $35.9 billion, a year-over-year increase of 40.6%, with a gross margin of 66.2%, and advanced processes accounted for 74% of wafer revenue. Q2 guidance is for revenue between $39 billion and $40.2 billion.

The relationship between TSMC and storage is multiplicative. Each additional advanced process wafer it sells produces an extra AI accelerator downstream, and each new accelerator requires multiple HBM stacks. The HBM capacity paired with NVIDIA’s Vera Rubin platform GPU is several times that of the previous generation. The more aggressively TSMC sells, the tighter the storage capacity becomes.

July 23 is Samsung's earnings report.

15 brokerages expect Samsung's Q2 operating profit to be approximately 88.3 trillion won, with an operating profit margin remaining flat or even higher than Q1's 66%. A conglomerate that makes everything from mobile phone panels to home appliances has seen its profit margins pulled to this level by one storage sector.

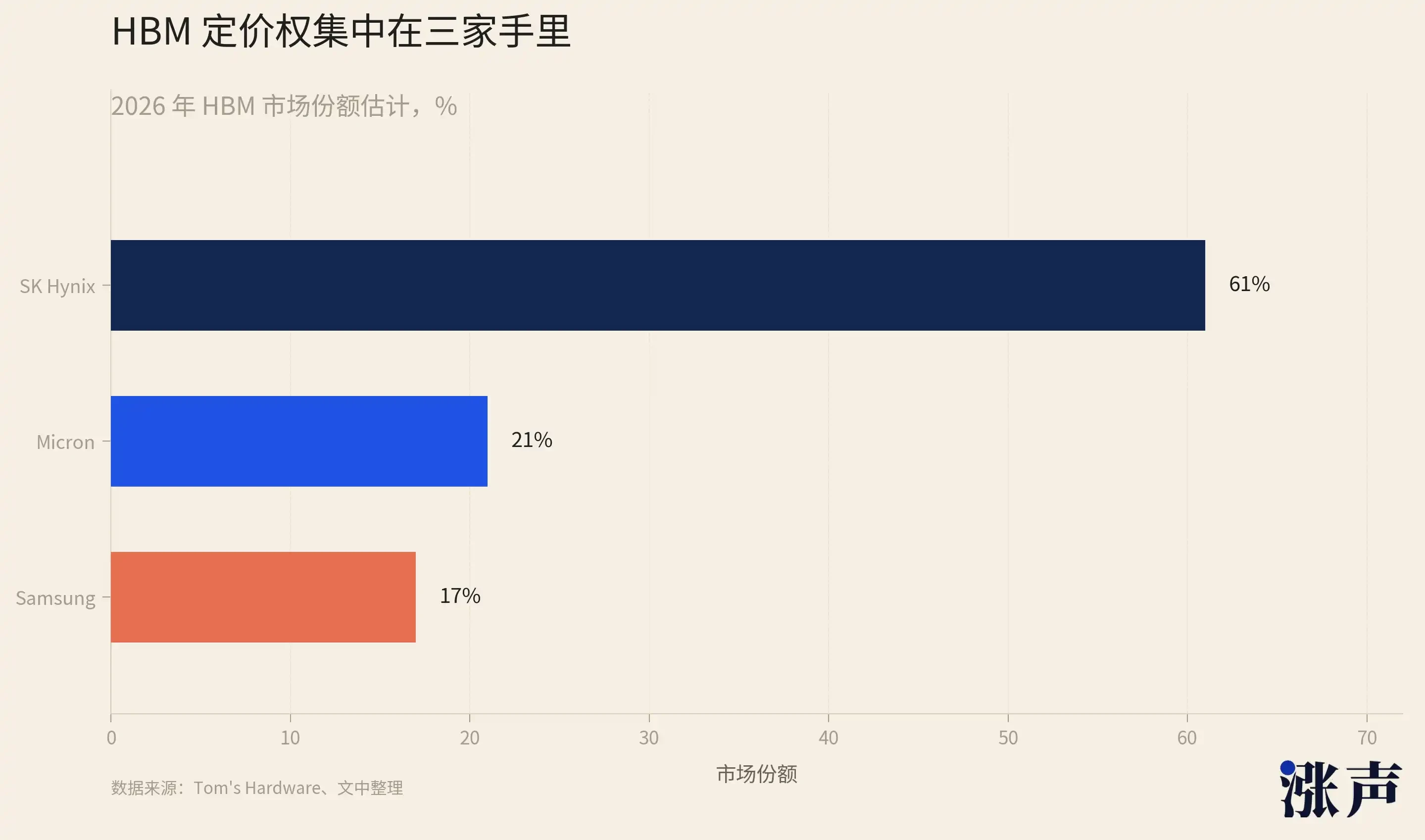

However, the most important aspect of this Samsung report is not the profit figures, but HBM4. Samsung holds only about 17% of the HBM market, lagging far behind SK Hynix's 62% and Micron's 21%. The generational transition of HBM4 is the only window for Samsung to close the gap. In the Q1 conference call, it mentioned that HBM sales would increase by over three times year-over-year in 2026, and that HBM4 would account for over 50% of HBM sales starting in Q3. Micron has just disclosed that HBM4 36GB 12-Hi has already begun mass production and delivery. The positioning battle among the three regarding HBM4 will be the battle to watch in the second half of the year.

On July 29, SK Hynix and Western Digital will report on the same day.

SK Hynix's Q1 performance is textbook-level: quarterly revenue of 52.6 trillion won, a year-over-year increase of 198%, and an operating profit margin of 72%, net profit margin of 77%. Achieving a 77% net profit margin as a hardware manufacturer outstrips Apple's approximately 25% and NVIDIA's approximately 58%. Some brokerages predict that Q2 operating profit margin may approach 80%. Micron has already pushed its operating profit margin to 81.2%, exceeding TSMC. SK Hynix, as the number one player in the HBM market, is expected to deliver results comparable to Micron in Q2. The combined operating profit for Samsung and SK Hynix in Q2 is expected to exceed 150 trillion won, and together with Micron, the three giants' single-quarter profits will set a new record.

Western Digital will also report its Q4 results on the same day; it produces only NAND and SSD, with no DRAM or HBM. It provides another dimension to AI storage demand: the KV cache for inference requires large-capacity SSDs. Q3 revenue from Cloud increased by 48% year-over-year, with a record gross margin of 50.5%. Notably, Western Digital and its spin-off SanDisk are the best-performing two stocks in the S&P 500 for 2026, ranking ahead of Micron. The growth in NAND lines is not as dramatic as DRAM, but the direction is entirely consistent.

AI Turns Storage from a Commodity into a Luxury Item

Stock prices hit a new high while PE remains low, and reports are becoming increasingly explosive.

At this point, there may still be doubts about whether all of this is sustainable, or if this is just another cycle that will eventually collapse.

We can take another look at the analysis by Jukan, a semiconductor analyst at Citrini Research.

Back in Q1 2024, while SK Hynix and Micron were still grappling with DRAM inventory excess and low stock prices post-pandemic, the Citrini team proclaimed these two would outperform. In retrospect, these stocks have each risen several times to nearly 10 times their original value. They have accurately predicted the entire storage market trend this round. A detail from early June further illustrates their position in the market: Jukan shared a report from SemiAnalysis regarding NVIDIA's Rubin server memory configuration adjustments, which immediately put visible pressure on Micron and SK Hynix stocks.

Jukan's bullish argument for storage does not stem from short-term judgments like "prices will rise," but rather from the belief that AI has transformed storage from a commodity into a luxury item.

First, HBM has broken a trend that has lasted for sixty years. From 1957 to 2020, the cost of DRAM per Gb fell about an order of magnitude every five years, with prices continuously declining. This is a foundational pattern in the storage industry, with the competition and valuation frameworks of the entire sector built upon it. Jukan points out that the HBM demand brought about by AI has completely shattered this rule. Manufacturers are shifting their production capacities to more complex, silicon-area-heavy HBM, squeezing the supply of traditional DRAM.

Currently, no manufacturer plans to revert HBM production lines back to traditional DRAM. The reason is simple: the profit margins for HBM far exceed those of ordinary DRAM, and rational manufacturers would not trade high-profit production lines for low-profit products. This has transformed supply tightness from a cyclical phenomenon into a structural one that won't reverse as long as AI demand remains.

Consequently, the continued price hikes in HBM storage will be long-lasting.

The annual volume and price for HBM were basically set at the start of the year, giving manufacturers strong profit visibility. Data from TrendForce supports this: in Q1 2026, traditional DRAM contract prices rose 90% to 95% quarter-over-quarter, marking the largest single-quarter increase on record, with further increases expected in Q2. The price rise phase for normal DRAM cycles typically lasts for 4 to 6 quarters before peaking; this round has been rising for nearly 8 quarters with no signs of stopping. JPMorgan even predicts that DRAM prices may rise for four consecutive years, which has never happened in industry history.

Therefore, it can be said that storage has transformed from a commodity into a luxury item.

The main distinction between luxury goods and commodities lies in pricing. The price of a commodity is determined by marginal costs, allowing anyone to increase production, ultimately driving profits down to zero, which is why it has a low valuation. The price of luxury goods is determined by scarcity and pricing power, with supply being controlled, enabling profits to remain at high levels for the long term, thus commanding a premium. The old rule of "low PE equals peak" assumes that profits will revert to that long-term declining trend line. However, if the trend line itself has already turned around, where it reverts to becomes an open question.

Returning to the earlier contradiction: stock prices are at historic highs while valuations are at historic lows. This anomaly exists because the market is still using the old commodity framework to price an industry that has become a luxury. Micron has just delivered a financial report with an 84.9% gross margin and guidance for an 86% gross margin, delivering a heavy blow to this old framework. If the reversal doesn't occur, the current PE of 5 to 10 times is incorrect.

Therefore, we believe that even with new highs, storage stocks remain inexpensive.

After HBM, Is NAND the Real Main Course?

As each significant market trend reaches its midpoint, the market always asks the same question: After the leaders rise, who will take over next?

HBM and DRAM are the absolute main characters of this round of storage market trends, with much of the three giants' explosive growth attributed to them; NAND has continued to play a supporting role.

However, a close look at the supply and demand structure reveals a counterintuitive fact: the NAND, which has been treated as a side dish, may actually be the main course, as its tightness is, in some respects, even more severe than that of HBM.

First, let’s discuss why HBM is so popular. HBM is the standard configuration for AI accelerator cards, with high prices, substantial profits, and high technical barriers. SK Hynix has achieved a 62% market share and a 77% net profit margin through it. These are all true. But HBM has one characteristic: while supply is tight, the path for expansion is clear. The three major players are all fiercely investing in HBM to expand capacity; Samsung and Micron are racing to catch up with SK Hynix, with generations of HBM4 and HBM4E rolling out. Supply is increasing at a visible pace but is simply lagging behind demand.

On the other hand, NAND manufacturers have not expanded production for several years.

The NAND price crash from 2022 to 2023 scared all players. Capital expenditures on NAND by Kioxia, Western Digital, Samsung, and SK Hynix were slashed to very low levels, and new production lines have been delayed repeatedly, with the earliest waiting until 2027.

The three giants have prioritized wafer capacity and capital expenditure for HBM and high-end DRAM, reducing the resources available for NAND. Micron even directly shut down its consumer-grade Crucial business to free up capacity for enterprise-level and GPU-level storage.

There is a lack of supply in NAND, but the demand is substantial.

Large model inference requires vast amounts of KV cache and data throughput, leading to explosive demand for enterprise-grade SSDs (eSSD). In Q1 2026, global eSSD revenue grew 86% quarter-over-quarter. Another factor is the shortage of HDDs. The supply of mechanical hard drives is also tight, forcing data centers to replace HDDs with high-capacity SSDs, which has shifted some demand originally intended for HDDs onto NAND.

According to the CEO of Phison Electronics, "Every NAND manufacturer has told us that by 2026, they will be sold out." Kioxia has also confirmed that its NAND capacity for the entire year of 2026 is fully booked. The price of a 1Tb TLC NAND has risen from about $4.8 in July 2025 to about $10.7 by the end of 2025, more than doubling in just a few months.

HBM is tight, but supply is deterministically increasing; NAND is tight, but there is virtually no increment from the supply side. The tension in HBM has a remedy, just a slow-acting one; the tension in NAND currently has no remedy because there’s no one providing the medicine. From this perspective, the supply and demand gap for NAND is even more rigid than for HBM, and its price sustainability may be stronger.

This is also why the best-performing two stocks in the S&P 500 for 2026 are not the HBM leader SK Hynix or Micron, but Western Digital's pure NAND and SSD and its spin-off SanDisk. The market has already voted with its feet, quietly shifting NAND from the supporting role to the leading role, although most people have yet to notice.

Of course, NAND also carries its risks. Unlike HBM, which is bound by a strong need for AI accelerator cards, downstream demand still includes the cyclical fluctuations of consumer electronics. The logic for NAND's tightness holds only if both AI inference and HDD replacement can sustain. But at least at present, from the perspectives of contract prices, inventory cycles, and willingness to expand production, NAND's tightness is purer than that of HBM.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。