TL;DR

- Citi expects the global optical interconnect market to reach $92 billion by 2028 and has raised price targets for New Yisheng, Dongshan Precision, and Tianfu Communication.

- The migration from 800G to 1.6T, 3.2T, and CPO/NPO is driving demand for high-speed optical modules, silicon photonics, and laser chips.

- The Chinese optical communication supply chain is the most direct beneficiary, but laser chip supply, yield, and high valuations will still limit the pace of realization.

Behind $92 Billion: Data Centers Taking Over Optical Interconnect Demand

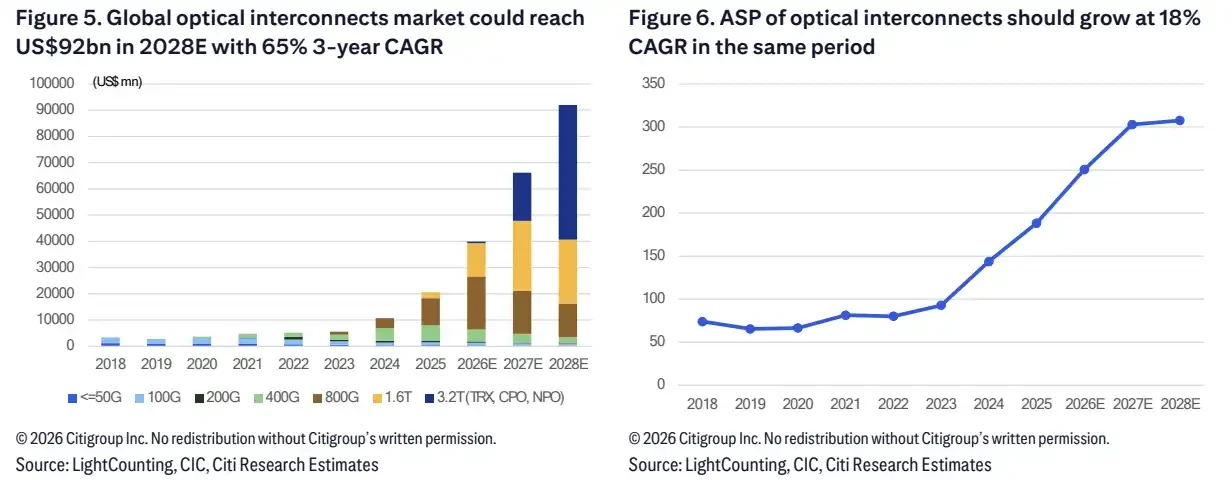

Citi raised its AI optical interconnect market forecast on June 24, expecting the global optical interconnect market size to reach $92 billion by 2028, with a compound annual growth rate (CAGR) of about 65% from 2025 to 2028. In the same round of adjustments, the price targets for Chinese optical communication companies such as New Yisheng, Dongshan Precision, and Tianfu Communication were significantly raised.

The basis for this judgment is not complicated. As AI data centers grow larger, the amount of data that needs to be transported between GPUs and ASICs increases, leading to a rise in connection demand among cabinets, switches, and servers. High-speed optical modules, silicon photonics, and laser chips are no longer just supporting equipment for data center expansion, but are key components for efficient connectivity of computing power.

Citi's model indicates that the average selling price of optical interconnects is expected to still have a CAGR of about 18% from 2025 to 2028, mainly driven by the increase in the proportion of high-speed products like 800G, 1.6T, and 3.2T.

The global optical interconnect market size is expected to rise to $92 billion by 2028, with the ASP stabilizing after maintaining an 18% CAGR from 2025 to 2028.

After 800G: 1.6T, 3.2T, and CPO/NPO Take Over

Ordinary investors need to first understand one change: this round of adjustments primarily comes from data center interconnect, rather than traditional telecom networks or enterprise networks.

In Citi's model, global optical interconnect shipments are expected to increase from 110 million units in 2025 to 300 million units in 2028, with a compound annual growth rate of about 40% over three years. The proportion of data center business in total shipments will rise from 71% in 2025 to 89% in 2028.

Product specifications are also increasing. The proportion of high-speed products above 800G in data center optical interconnect is expected to rise from 37% in 2025 to 89% in 2028. This means that the incremental demand is not just about "buying more optical modules," but rather higher-spec products accelerating the replacement of lower-speed alternatives.

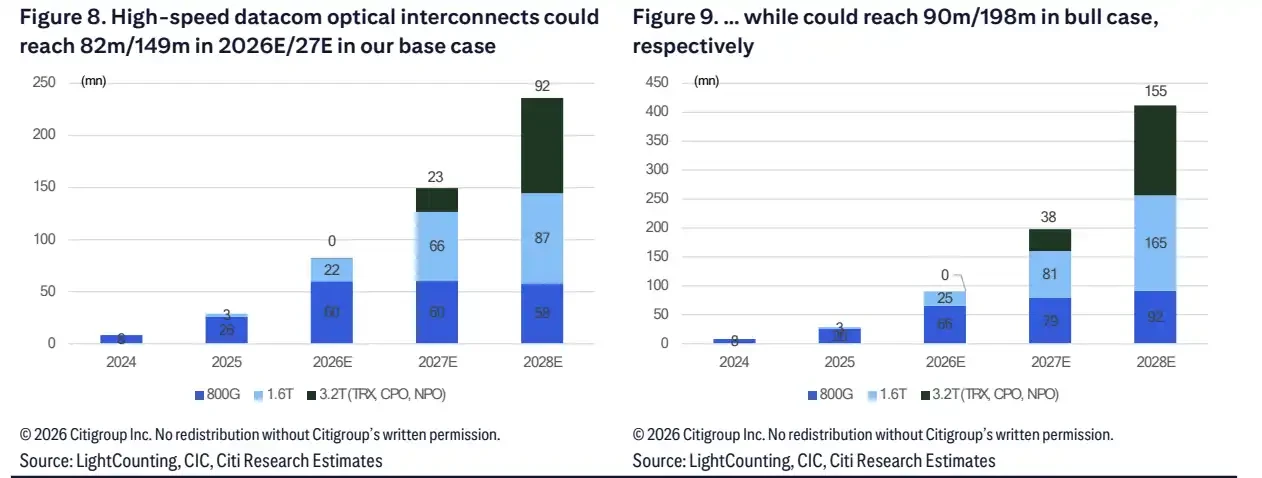

800G remains one of the mainstays in recent years, but the growth rates of 1.6T, 3.2T, and newer packaging solutions are higher. Under the basic scenario, the shipment CAGR of 1.6T transceivers from 2025 to 2028 will reach 215%. 3.2T will start from 2027, with shipments of 4 million units in 2027, rising to 35 million units in 2028.

CPO and NPO are considered later stages of technology migration. Under the basic scenario, shipments of CPO/NPO are expected to reach 18 million and 56 million units respectively by 2028. In the optimistic scenario, they can rise to 33 million and 116 million units by 2028. The difference between the two scenarios is significant, mainly depending on cloud vendor demand, yield improvement, and the pace of implementation for platform architectures like those of Nvidia and Google.

The demand for high-speed optical interconnects will clearly diverge after 2027, with 1.6T and 3.2T/CPO/NPO being the main sources of elasticity between the baseline and optimistic scenarios.

Silicon Photonics Rising to 60%: Value Shifting to Laser Chips and Optical Engines

If the $92 billion refers to market space, then "silicon photonics" and "laser chips" determine the allocation of this growth within the supply chain.

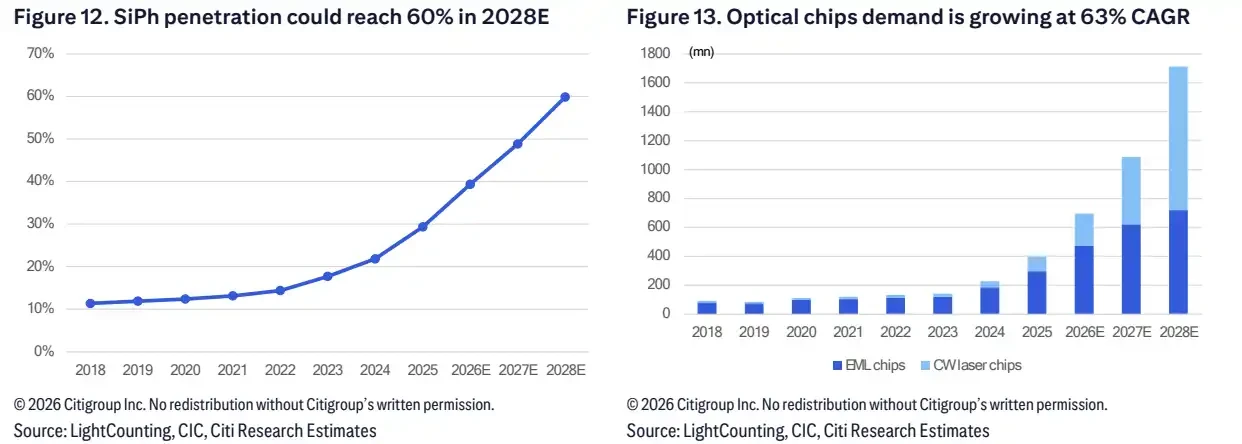

Citi expects the penetration rate of silicon photonics solutions in high-speed optical modules to rise from 29% in 2025 to 60% in 2028. Under this assumption, the total demand for optical chips in 2028 is about 1.714 billion units, with a CAGR of about 62% from 2025 to 2028.

Among them, the demand for EML chips is expected to reach 718 million units, with a three-year CAGR of about 34%. CW laser chips will grow even faster, with demand expected to reach 987 million units by 2028, with a three-year CAGR of about 114%.

This is also the reason why supply tightness has been repeatedly mentioned. After high-speed optical modules scale up, the bottleneck may not necessarily occur in the module assembly process but could arise in laser chips, packaging yields, and upstream capacity locking. Pure module manufacturers secure upstream supply through long-term agreements and strategic investments, essentially positioning themselves early for the subsequent scale-up of 1.6T, 3.2T, and CPO/NPO.

Silicon photonics penetration is expected to rise to 60% by 2028, with optical chip demand around 1.714 billion units in 2028, and a CAGR of CW laser chips reaching 114%.

Dongshan Precision, New Yisheng, Tianfu Communication Upgraded, Taicheng Technology Downgraded

On the individual stock level, the most direct changes are seen in New Yisheng, Dongshan Precision, and Tianfu Communication.

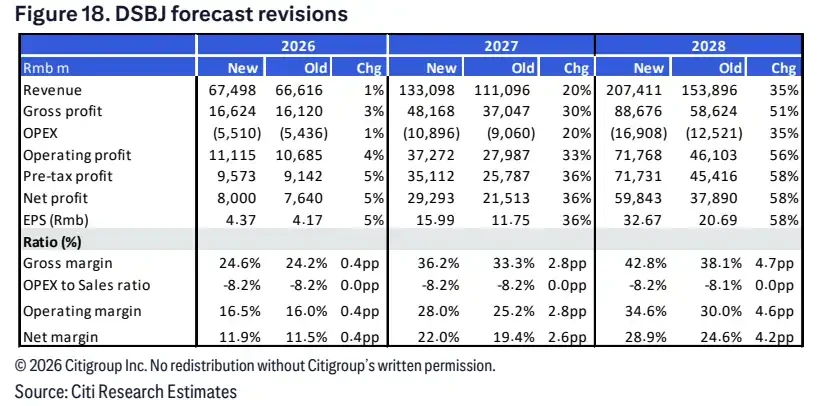

Dongshan Precision stands out as one of the most notable companies in this round of adjustments. Citi raised its price target from 225 yuan to 350 yuan and upgraded net profit forecasts for 2026 to 2028. The research report suggests that AI optical business is seen as a main growth driver, expected to significantly enhance profit contributions in the coming years.

In terms of valuation, Dongshan Precision is broken down into traditional business, optical modules, optical chips, and AI PCBs. This breakdown indicates that the market's view of Dongshan Precision is no longer solely based on traditional PCB or electronic manufacturing businesses, but also on its ability to convert AI optical business into profits.

New Yisheng's price target was raised from 353.57 yuan to 701 yuan, mainly driven by the 3.2T transceivers and NPO. Tianfu Communication’s price target was raised from 318.57 yuan to 419 yuan, benefiting mainly from CPO scale-up and 3.2T optical engines.

Dongshan Precision profit forecast upgraded.

Differentiation is also emerging. Taicheng Technology (300570.SZ) was downgraded from Buy to Sell, with the price target reduced from 156 yuan to 152 yuan. Citi adjusted its EPS forecasts for 2026 and 2027 downward, mainly considering risks related to decoupling from Corning, intensified competition in the Asian supply chain, and high valuations. According to the report, Taicheng Technology's current valuation is about 59 times the 2027 P/E ratio, while its price target corresponds to 31.8 times the 2027 P/E ratio.

This set of rating changes indicates that the adjustment in AI optical interconnect demand does not mean that all companies in the supply chain will benefit simultaneously. The market places more emphasis on the capabilities of high-speed products, the deployment of silicon photonics and laser chips, customer structure, supply chain stability, and whether current stock prices have already reflected growth.

It is noteworthy that these price targets still belong to broker model assumptions and are not company commitments. For investors, the price target increases reflect institutions raising expectations for AI optical interconnect demand, product upgrades, and shares of the Chinese supply chain together, but the follow-up still depends on whether orders, deliveries, and profit margins can keep up.

The Growth Story Stuck on Laser Chips, Yields, and Valuations

This round of adjustments does not mean that AI optical interconnect has entered a risk-free growth phase.

The first constraint is supply. Both EML and CW laser chips may become tight, especially under scenarios where silicon photonics penetration rapidly increases and 1.6T and 3.2T scale up quickly, upstream capacity and yield will directly affect final shipments. If key chip supplies do not keep up, orders and expectations may rise first, while revenue recognition will have to wait for delivery rhythms.

The second constraint is technological realization. CPO/NPO is regarded as an important increment after 2027, but whether the new architecture can scale according to optimistic scenarios depends on cloud vendor capital expenditures, network architecture choices, equipment yields, and the pace of progression of solutions from platforms like Nvidia and Google. The gap between basic and optimistic scenarios is significant, indicating that shipments over the next two years are not locked in yet.

The third constraint is valuation. Taicheng Technology has been downgraded by Citi from Buy to Sell, citing risks of decoupling from Corning and high valuations. LightSpeed Technology has also maintained a Sell rating, with similar pressures stemming from valuations.

The $92 billion market forecast brings AI optical interconnect to the forefront, but stock prices have already reflected many optimistic expectations in advance. The real differentiation lies not just in how many AI orders are secured but in who can penetrate higher-end product generations, lock in upstream laser chip supply, and transform the scaling of 1.6T, 3.2T, and CPO/NPO into sustainable profits.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。