Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@azuma_eth)

In the early hours of June 25th, Beijing time, the highly anticipated Micron Q3 fiscal report for 2026 was officially released.

Before the release of this quarter's report, Micron faced a somewhat awkward situation. On one hand, everyone knew it would deliver a good performance. On the other hand, everyone also knew that the market had already factored in this "good" performance into the stock price.

In the past few weeks, market participants have been engaged in a battle around the same question—For a storage giant that has already positioned itself at the center of the AI wave, how strong does its performance need to be to continue driving up its stock price and inject confidence into an already crazed semiconductor bull market?

The answer is—more exaggerated than anyone expected!

The market has been aggressive enough, but still conservative

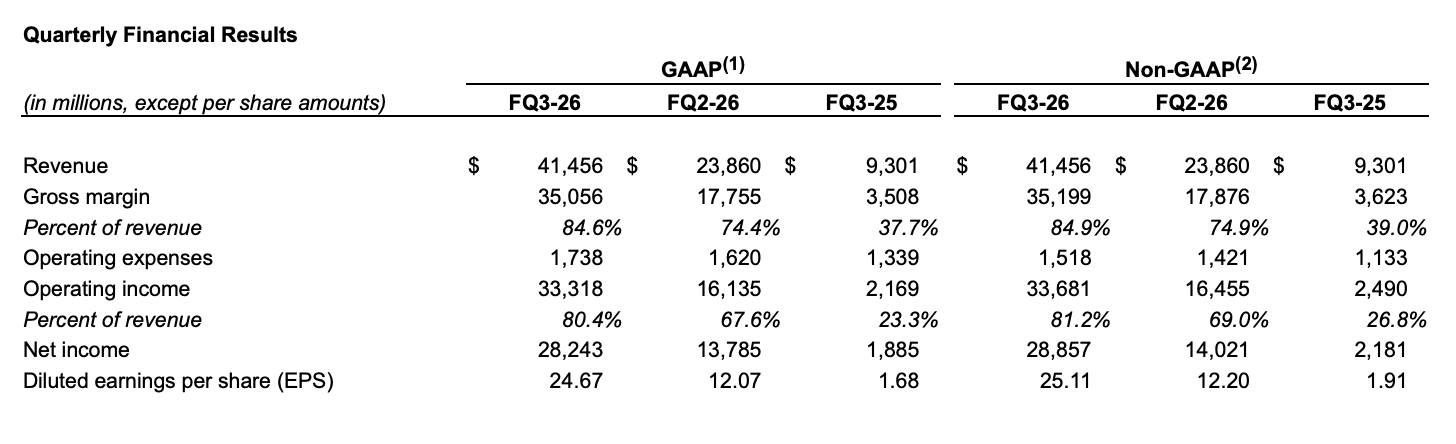

The Q3 report released this morning showed that Micron's revenue for the third quarter reached $41.456 billion (market general expectations were around $35.4 billion), an astonishing 346% year-on-year increase; GAAP net profit was $28.243 billion, nearly 15 times year-on-year; adjusted earnings per share were $25.11.

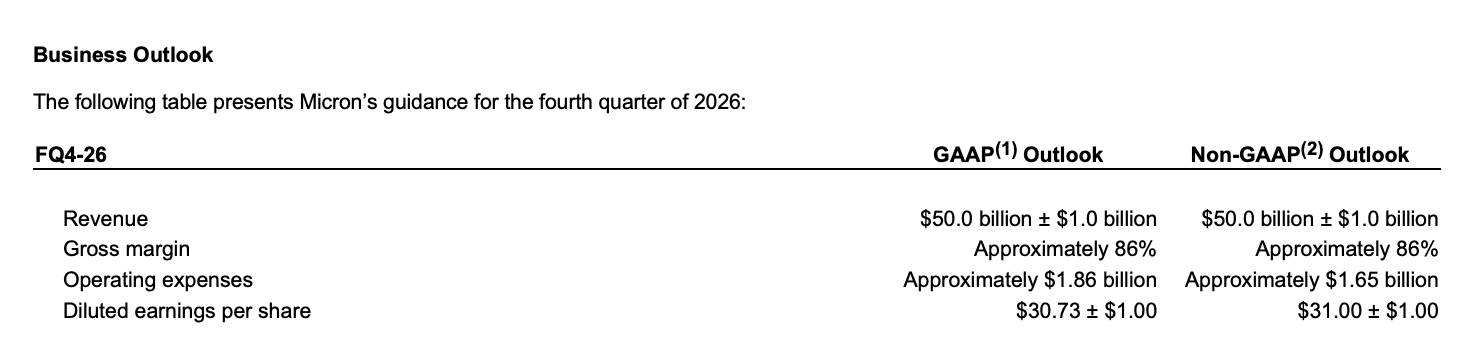

Even more exaggerated is the guidance for the next quarter. Micron expects its Q4 revenue to reach $50 billion (fluctuating by $1 billion), far exceeding the market's previous expectation of approximately $42.9 billion and Goldman Sachs' aggressive expectation of $48.8 billion (generally regarded as the most optimistic scenario); the gross margin for the fourth quarter is expected to be around 86%, and earnings per share are expected to reach about $31.

This is why many investors expressed the same exclamation right after the report was released, calling such a report a super invincible spiral explosion to the sky!

From HBM to SSD, the entire storage stack is racing

If we were to find a core driving force for this growth, the answer is still AI. However, compared to the past year’s repeated discussions about HBM, what’s more worthy of attention in this report is—AI's influence has begun to spread throughout the entire storage industry chain.

From a business structure perspective, nearly all of Micron's core businesses are growing in sync, among them:

- Cloud memory business revenue reached $13.77 billion, up over 300% year-on-year;

- Core data center business revenue reached $11.52 billion, up over 600% year-on-year;

- Data center SSD revenue surpassed $5 billion;

- Mobile and client business grew over 250% year-on-year;

- Automotive and embedded business also achieved over 300% growth;

- Gross margin for various business lines generally maintained around or even above 80% level.

This means that the current AI wave has led to not just a single product boom, but a comprehensive benefit across the entire storage industry chain.

On one hand, HBM remains the most direct beneficiary. Micron stated that HBM4 has already been shipped in bulk to core customers, and samples have been sent to multiple end customers; HBM4E is progressing as planned and is expected to enter mass production in 2027. At the same time, the company reiterated that its HBM capacity for 2026 has sold out.

On the other hand, the continuous expansion of AI training and inference demand is also concurrently driving the demand growth for high-end DRAM, enterprise-grade SSD, and NAND products. As more advanced production capacity is prioritized for HBM, traditional DRAM and NAND market supply becomes further tightened, thereby pushing the entire storage market into the strongest pricing cycle in recent years.

This is also why Micron remains extremely optimistic about the industry outlook. Management expects that the tight supply and demand conditions in the DRAM and NAND markets will continue beyond 2027. In other words, in Micron's view, the current industry is not nearing the top of the cycle, but rather, it resembles the early stages of the AI infrastructure construction cycle.

Long-term agreements extend as far as 2030

If this earnings report is merely interpreted as a victory for HBM, it may still underestimate its true significance. Because compared to the revenue guidance of $50 billion, the most noteworthy figure in this report is actually another set of numbers—$100 billion.

During the earnings call, Micron disclosed that as of now, the company has signed 16 long-term strategic customer agreements (SCA), covering data centers, consumer electronics, and automotive clients. Most of these agreements last for 5 years, with some automotive client agreements having a duration of 3 years, extending to the end of 2030.

These agreements cover approximately 20% of DRAM shipments and about one-third of NAND shipments. As more agreements materialize, over half of future revenue is expected to fall under the long-term agreement framework.

It is particularly important to emphasize that these agreements are not traditional supply contracts. Management confirmed that the related agreements adopt a strongly binding Take-or-Pay model. Even if customers do not fully take delivery in the future, they still need to fulfill their established purchase obligations. Some major agreements even set price floor and ceiling mechanisms, with the price ceiling anchored to market prices in the second quarter of fiscal year 2026, and even if executed at the price floor in the agreement, the corresponding gross margin level remains far above Micron's historical cycle highs.

Based on the data disclosed by Micron's management, 14 agreements currently correspond to a guaranteed revenue of approximately $100 billion. At the same time, customers will also provide a total of about $22 billion in performance guarantees, of which about $18 billion is in cash, which can be directly used to support future capacity construction and R&D investment.

For the storage industry, this is almost a historic change. For decades, the logic of operation in the industry has always been "expand production first, then wait for demand to digest"; now, Micron is gradually shifting to another model—lock orders first, then expand capacity.

This is also the most exciting aspect for the capital markets. Because it means that Micron's current profitability is no longer solely based on expectations of the economic cycle, but is backed by long-term contracts.

Expand, expand, and expand again, Q4 will invest $10 billion

If long-term agreements answer the question of "where does demand come from," then capital expenditure answers another question—how does Micron plan to meet this demand.

The financial report shows that Micron expects capital expenditures for the fourth fiscal quarter to reach approximately $10 billion (higher than Wall Street's previous expectation of about $8.9 billion), and it is anticipated that total capital expenditures for fiscal year 2026 will be approximately $27 billion, with quarterly capital expenditures for fiscal year 2027 expected to exceed the levels of the fourth quarter of 2026. New investments will mainly be used for HBM, advanced DRAM, and advanced packaging capacity construction.

In the past, such capital expenditure figures might have raised market concerns. After all, for the storage industry, "large-scale expansion" has never been a strange term. Historically, whether it was Samsung, SK Hynix, or Micron itself, they all ramped up investment at the industry's peak, ultimately leading to supply oversaturation, price crashes, and personally ending the last bull market.

But this time, the situation seems to be changing. The reason is simple—these new production capacities are not built on optimistic predictions of future demand, but are based on already signed long-term orders.

On one side are the $100 billion in guaranteed revenue, $22 billion in performance bonds, and long-term agreements extending to 2030; on the other side are the continuously expanding HBM, advanced DRAM, and advanced packaging capacities. By comparing this data, the current expansion activities seem more like executing already locked orders rather than the traditional bet on the economic cycle based on demand forecasts.

Micron's financial report reignites the semiconductor bull market

Before Micron's earnings report was released this season, sentiment around this semiconductor bull market had actually begun to soften slightly.

Earlier this week, the Korean semiconductor sector just experienced a noticeable pullback, with major companies like SK Hynix and Samsung Electronics coming under pressure together. Some investors began to worry whether AI trading had become too crowded after the crazy rise over the past year.

Micron provided a rather straightforward answer—it’s not that demand has peaked, but that the market still underestimates the demand.

From the greatly exceeding expectations Q3 performance to the guidance for Q4 revenue reaching $50 billion; from sold-out HBM capacity to long-term strategic agreements extending to 2030, all are conveying the same signal—AI infrastructure construction is still accelerating, not slowing down.

After the report was released, Micron surged 16% in after-hours trading, driving shares of U.S. semiconductor companies like Intel, ASML, Marvell, and Qualcomm to rise collectively; South Korean and Japanese stocks opened high and continued to rise, with the Korean stock market once again experiencing a circuit breaker, leading to significant rebounds for Samsung and Hynix; after the A-share market opened, the semiconductor industry chain also strengthened, leading with memory and advanced packaging sectors.

In a certain sense, this is no longer just a report belonging to Micron, but another strengthening of confidence for the entire semiconductor industry. Because the market has once again confirmed one thing—the AI story is far from over, and storage is becoming an increasingly important protagonist in this story.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。